We can expect that the government entities will be trying to jam affordable housing into every possible nook and cranny from now on. The idea of redeveloping larger areas, like Kearny Mesa, and include a nice compliment of affordable housing into an overall plan to uplift an entire area makes more sense to me:

Hat tip to just some guy for sending in this article:

Thanks to the COVID-19 pandemic, more deep-seated, tectonic-sized questions beyond markets and interest rates are being asked this time around that no one really has the answers to yet—like will people feel safer living in the south and southwest where they can spend all year social distancing outside? What if companies let workers work remotely for the rest of their lives? Why go back to retail shopping when I’m already ordering everything online? What’s the point of living “downtown” if half of the restaurants, bars, and museums never open back up?

How these questions get answered will fundamentally re-order how Americans live in the “new” pandemic normal, and as a result will play a huge X-factor in which cities and states will experience growth, demand, and price appreciation over the next 3-5 years, and which ones will stagnate and lose out. More broadly for large metropolises like Washington, D.C., New York City, and Philadelphia, the answers risk slowing or even reversing a wave of gentrification and wildly profitable downtown revitalization that’s been accelerating since before the Great Recession.

Against this backdrop, real estate’s new normal is also creating huge swathes of opportunity. Dozens of cities and counties that were once considered too small, too southern, too hot, too flat, or lacking in amenities, culture, or sophistication are now finding themselves being swooned to the top of the real estate desirability lists as Americans seek warmer, healthier, less dense, better educated, and more mobile places to live that offer closer access to the outdoors, better hospitals, and more open space with no clear end to the pandemic in sight.

To get a better view on what’s really happening to real estate in America right now I decided that it was time to do a deep dive into the actual data from the experts—including CoStar, Zillow, and Realtor—on how COVID-19’s great migration is actually shaking out and where the money and bodies are moving.

Here’s what I found out.

No matter who I spoke with, a few words kept resurfacing as we lurch into the post-pandemic future: warmer, safer, smaller, stabler, lower taxes, less regulation, and fewer lockdowns.

Regardless of where people come from or where they’re going, these things aren’t new on the list of what most Americans generally expect from the places they live, especially as they get older. (Northeasterners have been moving south and west for generations). The more interesting pandemic sub-text is the acceleration factor—and how the places where Americans are moving in the midst of COVID-19 may finally be expressing a more fundamental preference for how they reallywantto live instead of where they haveto stay because of their job location or where their kids go to school. It also says a lot about where many American’s heads are right now, and more importantly, the specific criteria with which they’re considering making one of the most important next decisions of their lives in an era of unprecedented uncertainty.

It’s likely US health officials will know whether a Covid-19 vaccine is safe and effective as early as next month, Fauci said Monday. “I think comfortably around November or December, we’ll know whether or not the vaccine is safe and effective,” he said.

There are currently 10 Covid-19 vaccine candidates in late-stage, large clinical trials around the world, according to the World Health Organization. Several of those are in the US and at least two have been in Phase 3 trials since late July.

Once a vaccine is deemed safe and effective, it’s likely companies will already have doses to begin distributing, Fauci said.

“There will be vaccines available, likely, for some people, limited amount, by the end of this calendar year, the beginning of 2021,” Fauci predicted. Experts including Fauci say health care workers and people with underlying health conditions will likely take priority for vaccinations.

It didn’t make this article, but he also said that vaccines are already being manufactured, and they should be available for the masses by the middle of next year.

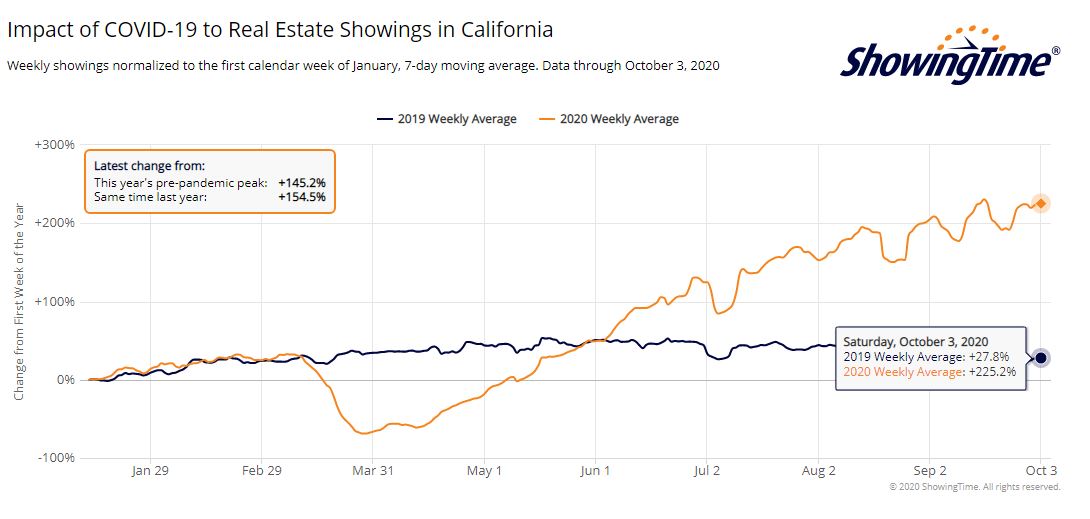

Just the thought of the pandemic coming to an end should be enough to goose the Spring Selling Season!

Not only does the current level of showings make up for the dip we had at the beginning of the Covid-19 market, but the 7-day moving average was higher on Saturday than all but two days this year (now 225% higher than it was during the first week of 2020).

As long as mortgage rates are under 3%, people will be looking!

Market conditions are subject to change! Hat tip to just some guy for sending in this article:

In five years as a San Francisco real estate agent, Emily Beaven has never experienced such a dry spell. She has several condos on the market right now that she’s representing and she has no offers and zero showings scheduled for them.

She decided it was time to get creative.

“We’re not even getting calls on things. It’s a bit of a ghost town. Then I started to see the incentive trend happening, ” Beaven said. “When you’re not in a super-strong seller’s market, when properties need that extra boost, that’s when [incentives] happen. We’re entering a period of desperation.”

Incentives are designed to entice the buyer or the buyer’s agent to get a property sold as soon as possible. Pre-pandemic, a higher commission for the buyer’s agent was a common incentive, as were restaurant gift cards, but when Beaven saw roundtrip tickets to Paris advertised recently as an agent incentive, she said they’d entered a new era.

As an incentive to purchase one of the SoMa studios she has on the market, Beaven is throwing in a session with a home organizer to help the prospective buyer maximize the small space.

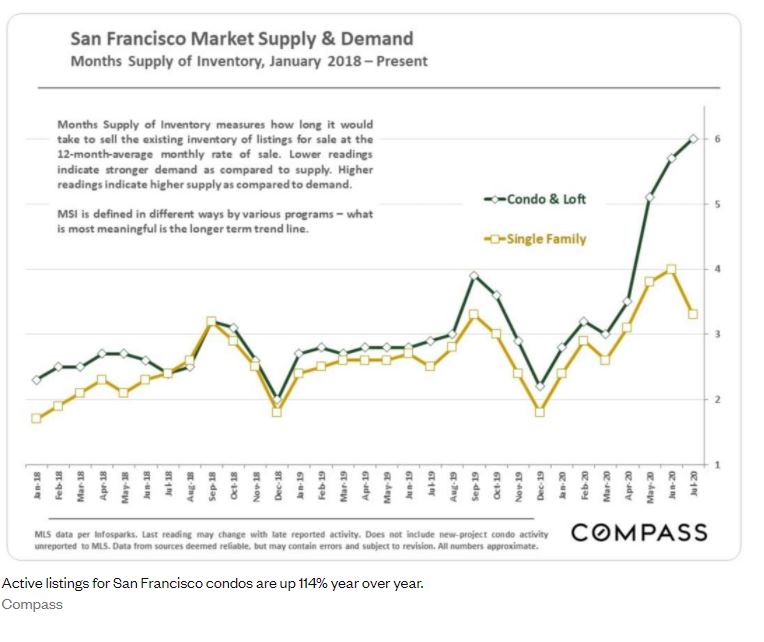

Active listings for San Francisco condos are up 114% year over year, according to Compass, and while condo listings typically exceed single-family home listings, there are now two condo listings for every single-family home listing. With supply at an all-time high, the average price per square foot has decreased 4% since 2019 and the amount of buyers overbidding asking prices is considerably diminished from levels seen in the past six years.

While that doesn’t mean we’re in a buyer’s market yet, that could change within a few months. Typically a buyer’s market exists at eight or more months of inventory. San Francisco is at six months right now.

Natalie Rome and Derek Chin had a condo listing in Hayes Valley that hadn’t received much interest in two weeks. That’s when the two started to talk about new ways to incentivize buyers and remembered that the garage space could only fit a subcompact car. Rome and Chin approached the current owners, who had purchased a Fiat 500 when they moved in, about including it in the sale for the right offer. They said yes.

“I think we’re going to see more creative incentives in the short term,” Chin said. “A lot of condos are vying for attention. Money talks for sure. A consultation for an interior designer, gift cards to home furnishings stores. I heard once an agent paid for flower delivery for every week of a year.”

For agent Rick Teed, that meant something you can’t get just anywhere. On a recent listing for condos in Russian Hill, he said one lucky buyer’s agent would win $500 in Bitcoin when they came to view the property. “I just feel like people always do the same things, 3% commission and an airline pass. I don’t see that working right now,” Teed said. “You have to look ahead at what’s happening in technology. You want to give them something they don’t have that piques their curiosity.”

My friend Ken Perlman at JBREC consults with new-home builders primarily, but these thoughts apply to the resale market too – notably, the 65+ generation growing by 17 million people in the next ten years!

With the national housing market surging, active adults have decided it is time to participate again. As discretionary buyers, they’ve had time to “restart” their purchasing process, and many of our developer and builder clients report that with proper health precautions in place, they’ve been willing to do so. In many age-qualified communities across the nation, home sales were particularly strong in August and September.

The pandemic hasn’t changed the size of the active adult population or its motivations. The active adult buyers are a key component of housing demand, as the 65+ population will grow by a net 17 million people over the next ten years. We know one of the highest priorities for this buyer set is being close to children and grandchildren. This means that as the Great American Move takes place in hot markets from Phoenix to Southern California’s Inland Empire to Sarasota, Florida, active adult buyers are following.

They are wealthy with large homes they can sell. Our active adult developer and builder clients told us one of the biggest fears their buyers had heading into the pandemic was the negative impact on their stock portfolios and on the homes they had to sell. Those fears have largely subsided with a rising stock market where the S&P 500 is up 10% year over year (YOY) and existing home Google searches up 30% YOY, as well as the Burns Home Value Index (BHVI) up 5.5% YOY.

4 Keys to Success

Active adult buyers are ready to buy now, so make sure you have inventory. Builders we spoke with in the active adult space told us standing inventory numbers are low, and some are tripling the number of standing inventory homes they produce to satisfy demand. Some are also simplifying what they offer in their homes, a process that streamlines housing production and keeps new home prices more attainable. Despite their wealth, these buyers are still prudent about how they spend their money.

Design elements that appeal to primary buyers also appeal to active adults. Per JBREC’s Consumer Products and Insights survey, more than 70% of new home shoppers between the ages of 55 and 69 included a member who worked at least part time. Work-from-home spaces were always critical to this buyer and are even more so today. Indoor/outdoor spaces are top of mind for active adult buyers, particularly those who live in warmer climates. Opportunities to live in the “healthy” outside while still maintaining cover is a big reason why open corner sliders and outdoor living rooms are immensely popular among this buyer set.

A strong virtual presence is essential. Active adult buyers are not afraid to use technology to search for a home; they rely on it. Active adult developers and builders around the country reinforce that their buyers are doing extensive research online before ever coming to the sales office, and we’ve heard reports of conversion rates among prospects in this space tripling post-pandemic. With travel more restricted and the market expanding rapidly, some active adult buyers are tying up their lots and homes efficiently via builder websites before ever visiting the neighborhood. Empire Communities in Atlanta told us, “We leveraged our virtual platforms, created new virtual platforms, optimized our online campaigns and online sales consultant initiatives, coached the sales teams to get out of their comfort zones, and shifted into a ‘we got this’ attitude.”

Active adult buyers still want to visit sales offices before they buy. While technology is helping buyers become educated, developers were universal in their opinion that this buyer cohort still want to make its final purchase in person. This means that an on-site sales office, decorated models, and well-organized system for coordinating appointments are still critical for selling homes to this buyer profile. Our clients across the country told us that with proper safety precautions in place, active adult buyers prefer visiting sales offices or models in person.

While the first-time and move-up buyers have clearly been the headlines of the housing market resurgence, the active adult buyer is starting to reemerge. We are assessing active adult housing across the country and watching product trends and buyer preferences. Let us know how we can be a resource for you. kperlman@realestateconsulting.com

Who is selling? The chart below tracks when the home was purchased by the sellers. Today’s numbers are from those sales closed between Aug 21-31 of this year:

Year Purchased

12/13/16

4/3/17

6/30/17

12/4/17

2/16/20

9/28/20

0 – 2003

57%

48%

32%

47%

34%

29%

2004 – 2008

19%

15%

12%

15%

18%

15%

2009 – 2011

6%

7%

14%

10%

4%

9%

2012 – 2020

13%

25%

34%

24%

35%

44%

New Home

4%

4%

7%

4%

9%

3%

So much for my theory about boomers leaving town! Today’s percentage of long-time owners sellers was the lowest yet…..but we know that over 50% of boomers delayed selling their home due to covid.

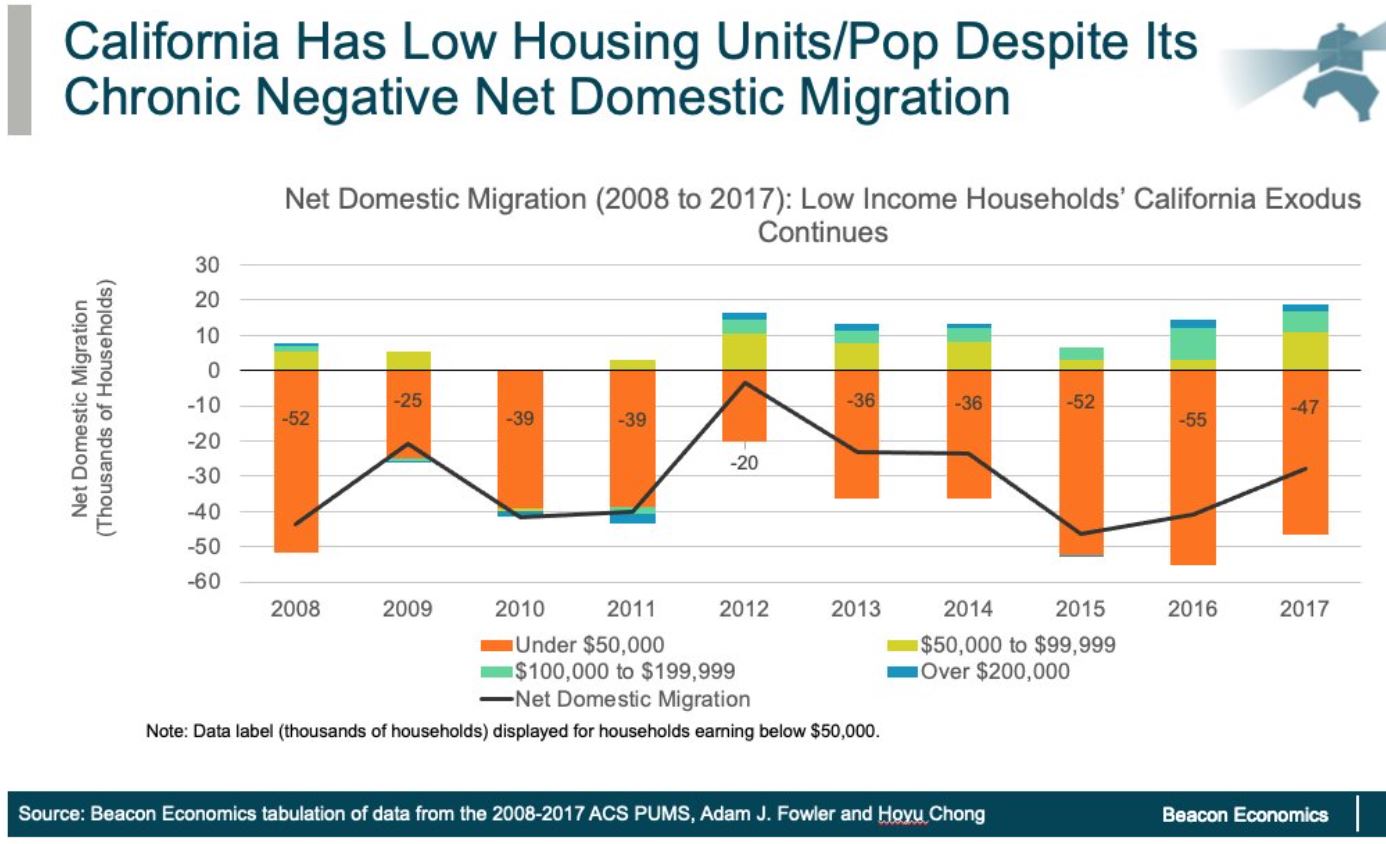

The chart at the top (click to enlarge) shows the California migration, and it’s a money thing.

People who leave the state find it too expensive here, and can do better elsewhere – and are willing to go for it! Younger people are probably more inclined to leave, at least at first. Grandparents to follow!

Of course, even the recent purchasers have no problem selling for a decent-to-huge gain, and more of them have been taking their profits – and hopefully buying another home, either here or elsewhere. Though the 2012-2020 group is the only one that grows just because we’re adding years over time.

More stats:

Other

12/13/16

4/3/17

6/30/17

12/4/17

2/16/20

9/28/20

# of Sales

144

112

99

99

116

130

Avg. $$/sf

$550/sf

$529/sf

$481/sf

$532/sf

$523/sf

$612/sf

Median SP

$1.291M

$1.274M

$1.11M

$1.25M

$1.18M

$1.46M

Avg DOM

42

54

43

52

47

39

0-10 DOM

35%

28%

45%

42%

28%

45%

Lost $$

7

7

0

1

2

0

DOM = 0

7

2

4

3

4

2

There were four flippers in today’s group, same as last time.

With the nation’s economy climbing out of a COVID-19 hole, home sales continue at a record pace. Total existing-home sales rose 2.4% from July to a seasonally-adjusted annual rate of 6 million in August. Sales were up 10.5% from a year ago.

After plummeting in March, home-buying demand continues to take steps towards recovery. On average, newly listed properties remained on the market for 22 days in August, down from 31 days in August 2019. Sixty-nine percent of homes sold in August 2020 were on the market for less than a month.

“The demand for houses is easily eclipsing the available inventory in metro areas across the country,” said Adam Contos, CEO of real estate brokerage RE/MAX Holdings. “Buyers are moving forward in record numbers, unfazed by inventory challenges and consistently higher prices. Homeowners in a position to sell are seizing the opportunity and benefiting from the one-two combination of enthusiastic, competitive buyers.”

The number of homes for sale continues to lag. Housing inventory totaled 1.49 million units at the end of August, down 0.7% from July and 18.6% from one year ago. Unsold inventory sits at a three-month supply at the current sales pace, down from the four-month figure recorded in August 2019. Six-months of supply is considered healthy.

Scarce inventory has been problematic for the past few years, an issue that has worsened in the past month due to a steep surge in lumber prices and a dearth of lumber resulting from the massive wildfires devastating Western states.

Here are nine predictions from housing industry experts on what the rest of the year will spell for the nation’s housing demand. (The text has been lightly edited.)

More exuberant but lower-motivated sellers will enter the marketplace committed to not giving it away! Their list prices will be 5% to 10% higher than today, causing some areas to be whipped into a frenzy, but in other areas, the unsolds stack up too quickly and become a glut. Buyers will determine which is which!

In the middle of a global pandemic, Southern California home prices keep setting records. The six-county region’s median price reached $600,000 in August, up 12.1% from a year earlier, according to data released Wednesday by DQNews.

That was the largest percentage increase since 2014 and the third consecutive month during which prices set a new all-time high. Sales rose 2.4% from a year earlier.

“We have had houses with 40 to 50 offers,” said Syd Leibovitch, president of Rodeo Realty, which has offices throughout the Los Angeles area. “It’s just bizarre.”

Although the price leaps may seem unlikely amid double-digit unemployment, analysts say the trend reflects the uneven effect of the coronavirus and its economic fallout.

Compared with low-wage workers, people who tend to have the financial ability to buy homes have been far less likely to lose their jobs, and in some ways, their ability to purchase a house has only expanded.

Interest rates have plunged, with the average rate on a 30-year fixed-rate mortgage now below 3%. And many typical entertainment and recreational activities are still closed or operating at reduced capacity, leading some households to save more at the very time they realize they could use much more space.

“Where are you going to take your Zoom calls where you don’t interfere with one another?” said Kevin Tidwell, an agent with Rodeo Realty.

The desire for more space, coupled with historically low borrowing costs, has helped boost sales and prices across the country. But part of the sharp double-digit increase in the median is simply its definition. The median is the point at which half the homes sold for more and half for less and thus reflects not only actual increases in value but also the types of homes selling at any given moment.

Jordan Levine, deputy chief economist at the California Assn. of Realtors, said a desire for larger homes could, in and of itself, push up the median. But more important is the uneven effects of the economic downturn.

Though many low-wage workers probably couldn’t have bought a home before the crisis, Levine said the country’s economic pain has been felt on a sliding scale, with middle-income households hit less than low-income households, but harder than the wealthy, factors that are causing a shift toward the luxury segment of the market.

For example, homes that sold for $1 million or more accounted for 22% of all homes sold in California last month, up from 16% in August 2019, the trade group’s data show. The share of homes that sold for less than $500,000 fell to 38% of all sales in August, down from 46% a year earlier.

Selma Hepp, deputy chief economist at CoreLogic, said the coronavirus is making the problem worse: Millennials are increasingly entering their prime home-buying years, but baby boomers who own large swaths of the housing stock are at heightened risk for complications from COVID-19.

“They don’t want to be moving right now,” she said of the older generation.

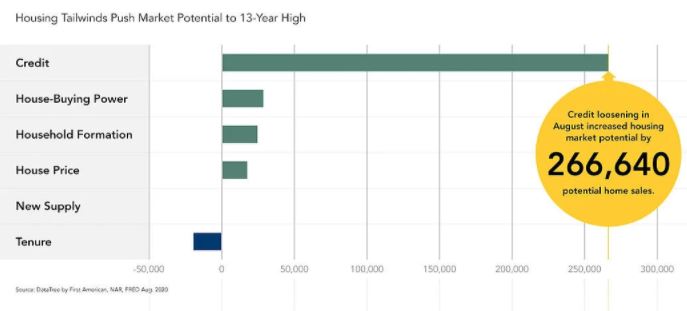

We know that the ultra-low mortgage rates and tight inventory have been driving the market wild.

But here’s an extra boost – the strict mortgage underwriting that began in April is being relaxed:

Credit Loosening: According to the NFCI credit index, a composite measure of credit conditions, credit tightened dramatically in mid-April to its most conservative level since 2009 due to the increased economic uncertainty driven by impacts from the pandemic. Since then, credit availability has loosened, even reaching pre-pandemic levels in August. This credit composite takes into consideration many different credit indicators, giving a comprehensive picture of credit conditions in the U.S. When lending standards are tight, fewer people can qualify for a mortgage to buy a home. Likewise, when standards are loose, more people can qualify for a mortgage and buy a home. Credit loosening in August compared with last month increased housing market potential by 266,640 potential home sales.

The graph above is somewhat misleading because they are only reflecting the month-over-month differences. The improvement of ‘house-buying power’ due to low rates has already been in place for months now, so the increase from July isn’t that dramatic.

I’ve heard that the qualify-using-bank-statements mortgage is back, so that will add a few self-employed buyers who can’t qualify using their tax returns. More competition!