After another weekend of multiple-offer situations where the listing agents made no attempt whatsoever to create a bidding war, and instead just shut down the showings, it’s hard to believe there is any downturn coming our way. When you can get a mortgage rate in the twos, the demand is unyielding.

But some authors still want you to believe that doom is around the corner – they should talk to realtors on the street! An excerpt:

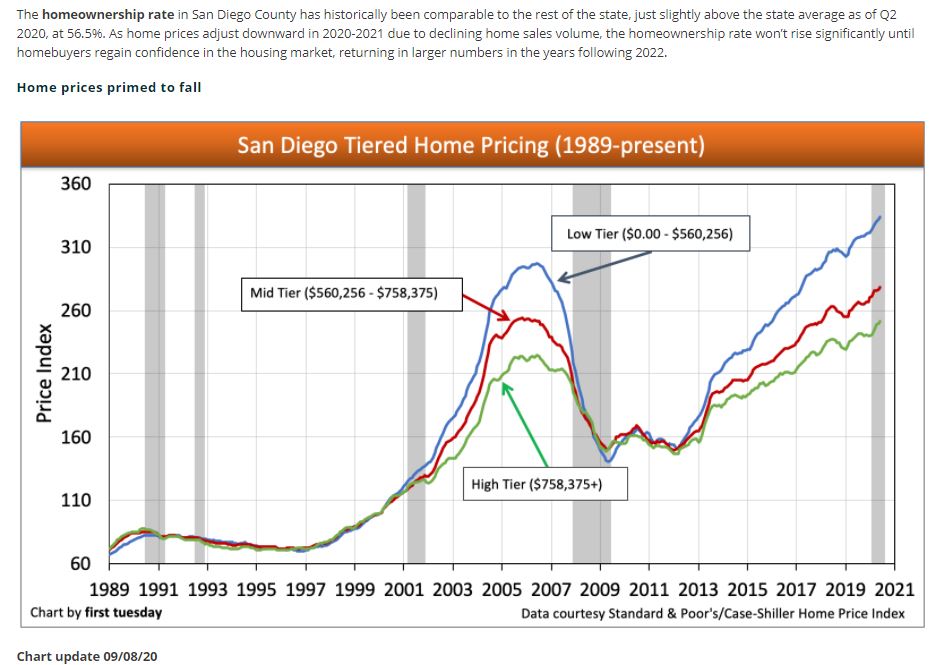

The price of low-tier housing in San Diego County skyrocketed after the latter half of 2012. 2015 experienced another price increase, due to the boost given by decreased mortgage rates throughout 2015 and 2016. Lower mortgage rates free up more of a buyer’s monthly mortgage payment to put towards a bigger principal. Thus, San Diego’s high home prices continued to find fuel from increased buyer purchasing power.

But in 2018, home price increases sharply declined in reaction to slowing sales and rising interest rates, which began in late-2017. Home prices have since turned back up, but today lack the fundamental support of home sales volume to continue. The annual pace of increase is now just 5%, lower than in recent years when the annual rise averaged around 10%.

Accurate home price reports run about two months behind current events. Even when caught up, sticky prices tend to persist several months beyond the moment when home sales volume begins to slow. Starting in March 2020, economic volatility and shelter-in-place orders caused home sales volume to decline dramatically. However, historically low interest rates have provided a boost for buyer purchasing power, which has propped up home prices thus far.

Later in 2020, the impact of record job losses will see downward pressure on home prices. The overall home price trend for the next couple of years will be down, the result of job losses and plummeting sales volume. As during the 2008 recession, the drop in sales volume and prices will first be most volatile on the coast, before rippling outward to inland areas.

Sales and pricing should be directly connected to inventory.

When there is hardly anything to buy, sales may decline, but pricing would stay the same or go higher because only the quality homes would be selling. A surge of homes-for-sale in 2021 would fuel the demand and energize the marketplace…..to a point.

There will be a fine line between frenzy and glut!

We are hitting peak performance when the median sales price is going up around 2% per month. With the wicked combination of low inventory and rates, it could continue – and after a year we could be up +24%!

It reminds me of my first blog post from 2005, which was the last time these types of conditions were in play. Our 15th anniversary is next week! Hat tip Susie!

Our Serra Mesa townhouse listing garnered five offers – one at list price, and four over! It will be the highest sale in the history of the complex. Hat tip to ‘just some guy’ for sending this in:

In the ultra-competitive Westchester market, the odds were stacked against Heather Harrison and her client. A stately suburban home that was listed on Tuesday already had 30 showings lined up for that upcoming Saturday.

“I put in a full price offer at $1.275 million, that was the asking price,” Harrison said. “The client went to highest and best on Monday at 5 p.m., and I counseled my client to bid accordingly, waive his mortgage contingency, then we bid $1.45 million and we got it.”

With the suburbs seeing record volume, agents and brokers like Harrison, who runs Compass’ operations in Westchester alongside her husband Zach, are counseling their clients on how to prevail in a fierce bidding war.

According to Redfin, offers on single-family homes in August were most likely to be involved in a bidding war, at 56.6% of offers, followed by townhomes at 54.7% and condos at 41.3% – 54.5% of offers overall engaged in bidding wars.

Time waits for no buyer in the suburbs

With record-low interest rates, paltry inventory and a surge in buyers, agents are advising clients to be extraordinarily aggressive to win.

“You’ve got to really advise your clients appropriately, quickly and make sure that they know there’s not even a week to come see the property – you’ve got to go,” Harrison said. “The property comes on within 24 hours, and if it meets your buyers criteria you want to get them out to see it.”

When it comes to counseling a client through a bidding war, education is paramount, Harrison said. Prospective buyers need to be armed with as much data as possible about the market they’re targeting. Another critical element, according to agents, is not to make the deals contingent upon things like inspections and not to “nickel and dime” the seller. That will set the prospective buyer apart, Harrison said.

“I’ve also been encouraging them to write kind of like a love letter so to speak to the sellers, so they’re not just like an offer on a piece of paper, they’re giving a little color about themselves, why they’re moving, why they like their house, and giving a picture of them so that the sellers can feel good about who they’re selling to and it’s not just about the numbers,” Harrison said.

To win, waive those contingencies goodbye

Susan Hamblen, broker and owner of Long Island-based EXIT Realty Achieve, said that her agents are slammed with business, and homes that are “priced right” are getting offers within the first 24 hours.

“Homes are going $40,000 to $60,000 over ask, easily,” Hamblen said, attributing the bidding wars partly to the influx of buyers from New York City. “We have about two months of inventory and the buyer demand is just crazy.”

Eugene Cordano, vice president and director of sales at Halstead in New Jersey, said that in his market, bidding wars have triggered offers between 15% and 20% over asking, across all home prices.

To that tune, Cordano agreed with Harrison that it’s important to stick out in a bidding war.

“The old axioms of real estate do not change,” Cordano said. “But the highest bid does not always prevail.”

The influx of buyers from New York City to New Jersey at the beginning of April through June meant that there was more money to spend on homes.

“For our seller-clients, we were counseling them on how the buyers waive appraisals or waive mortgage contingencies,” Cordano said. “With the influx of New York City buyers bidding these houses up, oftentimes waiving the financing/mortgage/appraisal contingencies was not a difficult thing to ask for and most of them did that.”

When it comes to buyers, it’s a different story.

“If the buyer really wanted that home, it was often, “How do we structure this offer to make sure that it stands out and wins the day?’” Cordano said. “That’s not a scientific process. Sometimes that is something that’s very emotionally driven, or driven to the point where the buyer really wants it and is just willing to pay and will offer, either in price or in terms, something that will win the day versus all the other buyers that were there.”

Spreading out in the hottest market will cost you

Vickie Mox, an agent with RE/MAX Dallas Suburbs, covers the Collin County area, north of Dallas. She said the surrounding towns are busiest right now.

The Dallas suburbs of Frisco and Plano are the hottest because they have low rates of inventory and are priced to sell, spurring bidding wars, Mox said.

“Houses that are more unique with large lots and that have been totally updated [sell quicker], and there’s nothing for the buyer to do but move in,” Mox said. “[That listing] could conceivably have 10 offers, and that’s usually between the price range $250,000 to $400,000.”

Once you get over $400,000 there are fewer buyers and there’s less demand for the property, according to Mox.

“But a $500,000 house could have multiple offers if it has everything the buyers are looking for which is being updated to a large yard or a three-car garage, in the right neighborhood and right school district,” she said.

In Colorado Springs, which Redfin said recently has the No. 1 hottest ZIP code right now, there could be at least three to five offers on a home in the first 48 to 72 hours of being listed, according to Keller Williams Associate Broker Scott Sanchez.

“The typical thing here in the Springs has been a $10,000-plus minimum to go over list price,” Sanchez told HousingWire.

“Maybe two years ago it was kind of common for five grand over, maybe $10,000 tops,” Sanchez said. “Last year, you start getting into the $10,000 to $15,000 range and this year it’s been $20,000 on the good homes that are well marketed and even if they’re priced up, they still will get 20 grand over.”

Bidding wars aren’t necessarily uncommon for Peck Barham, a real estate agent at TeamBarham, Keller Williams Homewood outside Birmingham, Alabama, but not at this rate.

“We haven’t seen [bidding] quite like this,” Barham said. “I think in August something like 600 homes went under contract in a three-week period, which for Birmingham is a lot. That’s a lot of homes going real fast.”

We kind of assumed they would have to keep rates low, but now it’s official:

The Federal Reserve announced a major policy shift Thursday, saying that it is willing to allow inflation to run hotter than normal in order to support the labor market and broader economy.

In a move that Chairman Jerome Powell called a “robust updating” of Fed policy, the central bank formally agreed to a policy of “average inflation targeting.” That means it will allow inflation to run “moderately” above the Fed’s 2% goal “for some time” following periods when it has run below that objective.

The changes were codified in a policy blueprint called the “Statement on Longer-Run Goals and Monetary Policy Strategy,” first adopted in 2012, that has informed the Fed’s approach to interest rates and general economic growth.

“Many find it counterintuitive that the Fed would want to push up inflation,” Powell said in prepared remarks. “However, inflation that is persistently too low can pose serious risks to the economy.”

We hear the term, ‘tight inventory’. What does it mean?

Fewer homes for sale?

Fewer of the lower-priced homes for sale?

Homes selling faster?

The best buys are flying off the market in the first day or two?

NSDCC detached-home statistics for Jan 1st – Aug 15th:

Year

# of Listings

Median LP

# of Sales

Median SP

Avg DOM

Median DOM

2016

3,727

$1,399,000

1,912

$1,150,000

43

22

2017

3,349

$1,425,000

1,994

$1,229,500

45

19

2018

3,390

$1,497,500

1,819

$1,320,000

40

18

2019

3,411

$1,550,000

1,789

$1,300,000

43

22

2020

2,991

$1,659,000

1,643

$1,400,000

41

18

20vs19

-12%

+7%

-8%

+8%

-5%

-18%

The average and median Days-On-Market metrics are within the normal range, so generally-speaking, homes aren’t selling faster than before.

We’ve had fewer homes for sale (-12% YoY), but sales are only down 8% which isn’t bad. The drop in sales between 2017 and 2018 was slightly more at 9% so we’ve endured this previously.

The overall volume is only down 0.4% YoY ($3,000,850,233 vs $2,988,471,818) – so those on commission (realtors, lenders, escrow, and title) shouldn’t be too concerned with ‘tight inventory’.

Who should be concerned?

Buyers on the lower-end of every market.

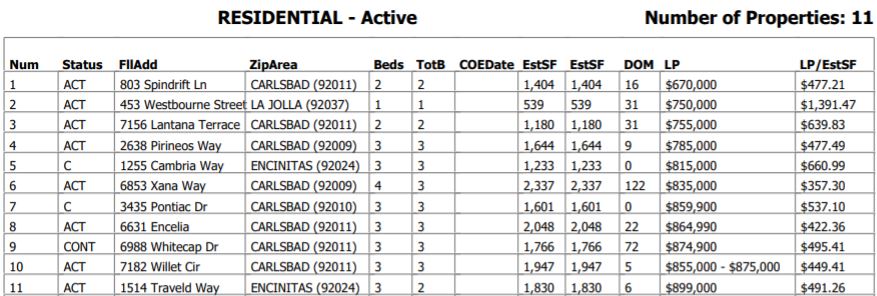

We have eleven NSDCC houses for sale priced under $900,000 (in an area of 300,000 people):

Two of those aren’t on the market yet (coming soon!), and a third has a contingent buyer.

Tight inventory = buyers are getting squeezed up on price.

My video on Monday touched on the different groups of buyers and sellers that should be very active in the 2021 selling season. Let’s break it down further, shall we?

SELLERS

Boomer liquidations – When we first started talking about boomer liquidations, people in their 60s scoffed and shrugged it off. Now they are in their seventies, and the burdens of homeownership have never been so apparent. Stuff needs to be fixed regularly, and that dang property tax bill keeps coming twice a year. If you didn’t mind leaving town, a homeowner’s equity position has never been so solid, and you could go to most towns in America and buy a house for cash and live happily ever after. It’s a temptation that aging boomers will find harder to resist in 2021.

Health considerations – Covid isn’t going away, and for those who are physically challenged, selling their house here and moving to a healthier location will feel like a life-or-death decision – they need to do it. Cashing out their equity is a nice bonus too, and provides enough grease to make it easier to leave San Diego. Let’s note that there are good doctors everywhere, and while the transition may be uncomfortable for the first couple of months, you’ll adjust.

Grandkids – Obviously, it is harder for the kids to get a foothold here than the parents who came 10-30 years ago – home prices have doubled. If the kids pack it up and take the grandkids somewhere that is affordable, it is inevitable that the grandparents will follow. They don’t have much time left, and they want to spend it with family. The grandkids may be the #1 factor in real estate decisions for the next few years.

Move-Uppers – For those who want to stay local, the best time to move up is when you can sell your existing home for more money than ever, AND get a lower interest rate. My rule-of-thumb for move-uppers is that you have to spend 50% more on the next house to make it worth the move – if you only spend 10% more, you only get an extra bedroom, and it’s not worth moving. There aren’t many in this group who finance – you still need a big cash infusion to make it work. Here’s an example:

If you bought your home for $500,000, with a loan of $400,000 at 4%, the payment is $1,910 per month. If you sell now for $1,000,000, and use $600,000 for your down payment to purchase a $1,500,000 house, the payment is $3,794 per month at 3%.

Most who are used to paying $1,910 per month will want to inject more capital into the equation.

Last Movers – You are of the age where you have one more move left in you, and it’s probably due to hanging on to the 2-story family homestead for a little too long. The kids have been gone for a while, and you’ve been rattling around in a house that should be passed on to the next generation before you fall down those stairs.

BUYERS

First-timers or Out-of-Towners – If you don’t own a house here yet, your motivation is substantially higher than those who do own and are just trying to re-position. It’s why current homeowners struggle to understand why homes keep selling for record amounts – because heck, they’d never pay that much. But first-timers and out-of-towners are more desperate to get in, and will pay an extra few bucks to finally get something.

Downsizers – Rarely do locals downsize in the same town – keeping the old house makes to much sense, and why we have such low inventory. But San Diego County is well-positioned to be a landing ground for those selling for big bucks in L.A./O.C./Bay Area and coming here where our prices look like a bargain. This may be the largest group of buyers, judging by how fast prices go up.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Next year’s selling season won’t be as predictable as they’ve been recently.

We are overdue for a surge of sellers.

It may be disguised in the overall stats as a blip, but if you have three houses on your street go up for sale, and two others on the next street over, don’t be surprised if buyers freeze up and wait it out. If you live in a neighborhood where most of the residents have been there for 10, 20, or 30 years, there only needs to be one from each of my five seller categories above to cause a glut of homes for sale within a week or two. If any of them are desperate for money and undercut the pricing to get out, it will affect all.

Next year will be exciting because each seller and buyer group could grow 10%+ without notice. Remember the graph that said 57% of boomers are delaying the sale of their home? Add a possible covid bump in the usual number of deaths, divorces, & job transfers and we could experience a surge of inventory that nobody sees coming.

If you are thinking of selling……are you willing to get out in February or March will all-time record money, or are you going to wait until June or July and try to milk it for another 5% because you can? And risk not getting out at all because those ‘lowball’ offers based on 2020 comps are insulting and unacceptable?

Our reader ‘just some guy’ sent in this article and quipped about these writers who insist on promoting a foreclosure scare due to the pandemic. But it is worth noting because it could become a self-fulfilling prophecy just due to the lack of a counter-argument being published at large.

This article is quick to point out that there isn’t a problem yet:

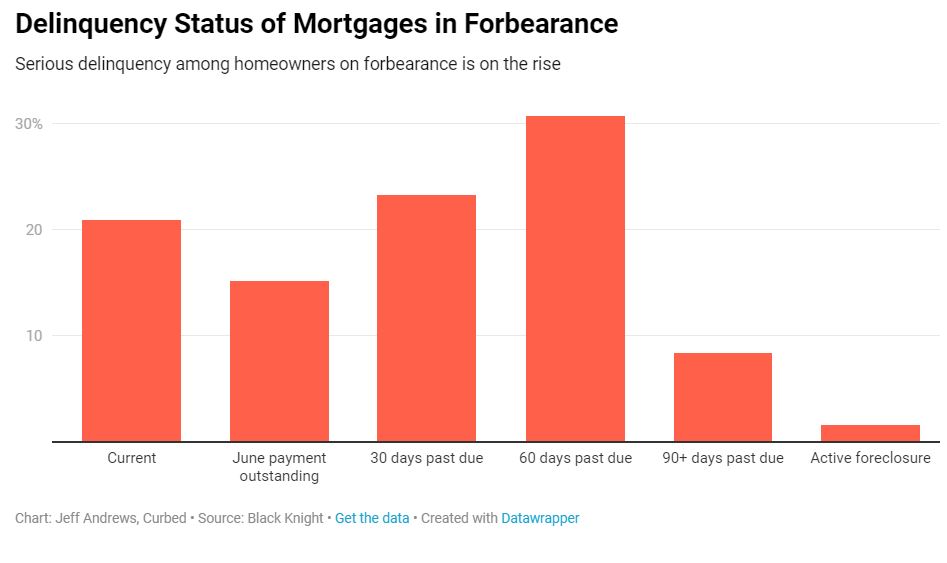

Even after the foreclosure moratorium expires, homeowners on a government-backed loan will have a forbearance option to fall back on, so there’s no need to panic just yet. But digging into mortgage-delinquency data shows how much water is building behind the dam that is these government backstops.

In January, just 3.22 percent of mortgages were in delinquency. By May, that number shot up to 7.76 percent — about three points shy of where the delinquency rate peaked during the financial crisis of 2008, which was at 10.57 percent.

Prior to the the pandemic in March, the number of mortgages in forbearance was fewer than 100,000. Currently, there are roughly 4.5 million mortgages in forbearance, although this is obviously a reflection of homeowners having the option of forbearance, but it gives you a sense of the scope.

Not every homeowner in forbearance is past due on their payments; some went into forbearance as a precaution, or just because they could. Some homeowners were in forbearance and have since gotten out, either because there didn’t end up being a need or they got a new job. For June, 21 percent of mortgages in forbearance were current on their payments, but as the pandemic goes on, more will enter into serious delinquency that would normally trigger a foreclosure.

With the forbearance option available for up to a year, economists have baked into their models a wave of foreclosures in the spring of 2021, which they say would cause a very rare drop in U.S. home prices.

I haven’t heard anyone predict falling home prices in 2021, and Zillow is forecasting a 5.7% increase.

We also know that the loan-modifications that worked last time will get employed again before banks lose a penny. The only people they might foreclose on are homeowners with sufficient equity, but if it comes to that, then those folks will sell their house instead and make out nicely.

It does add an interesting component to next year’s selling season though, which should be a humdinger!

BTW, I don’t have any insider info on the rumored Compass/Keller Williams merger. Even if it’s been discussed, it’s hard to believe the egos involved would allow for it.

We are 24 hours into having our new listing on the market and it’s already been shown six times and we have three offers – and all are over the list price!

I heard a rate quote today of 2.55% with less than a point cost, which feels like free money. As long as buyers can get a 2-something rate, the market should be extremely active!