We know that the ultra-low mortgage rates and tight inventory have been driving the market wild.

But here’s an extra boost – the strict mortgage underwriting that began in April is being relaxed:

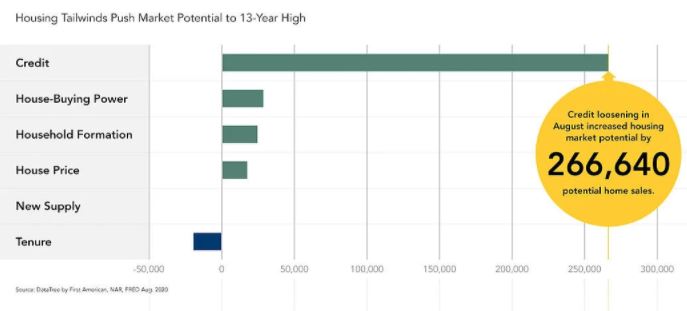

Credit Loosening: According to the NFCI credit index, a composite measure of credit conditions, credit tightened dramatically in mid-April to its most conservative level since 2009 due to the increased economic uncertainty driven by impacts from the pandemic. Since then, credit availability has loosened, even reaching pre-pandemic levels in August. This credit composite takes into consideration many different credit indicators, giving a comprehensive picture of credit conditions in the U.S. When lending standards are tight, fewer people can qualify for a mortgage to buy a home. Likewise, when standards are loose, more people can qualify for a mortgage and buy a home. Credit loosening in August compared with last month increased housing market potential by 266,640 potential home sales.

https://blog.firstam.com/economics/housing-market-potential-reaches-highest-level-since-2007

The graph above is somewhat misleading because they are only reflecting the month-over-month differences. The improvement of ‘house-buying power’ due to low rates has already been in place for months now, so the increase from July isn’t that dramatic.

I’ve heard that the qualify-using-bank-statements mortgage is back, so that will add a few self-employed buyers who can’t qualify using their tax returns. More competition!

0 Comments