Shouldn’t Matt Hall sell his downtown properties or resign as mayor so the regular political process can be conducted?

There will be no moratorium on development in the Village and Barrio.

The City Council decided to not move forward with the proposal brought forward by Councilwoman Barbara Hamilton during its June 25 meeting after receiving feedback from city staff and discussion regarding a lack of standing to make such a move.

Cities can adopt interim, urgency ordinances prohibiting uses in conflict with a general plan, specific plan or a zoning proposal. However, a four-fifths vote is needed, along with a finding of a current and immediate threat to public health, safety or welfare.

But since Mayor Matt Hall was recused due to financial interests in the Village and Barrio, a majority vote would have been required for a moratorium.

However, Hamilton, who represents District 1, which covers the Village and Barrio, received approval to bring back five items for further discussion for the council workshop on July 9 and approval for a portion of the Village and Barrio Master Plan on Aug. 20.

Those issues include housing and parking in-lieu fees, historical preservation, permitted uses and “decision-maker definition.” The council also passed a decorative lighting study in the Village, 4-0 (Hall was recused).

Hamilton said she her goal was to take a step back from the construction and ongoing redevelopment to assess the area’s needs on a larger scale. Specifically, affordability was a big topic of discussion as the council attempts to incorporate more affordable housing in those neighborhoods.

“As development continues, and we continue to offer housing in-lieu and parking in-lieu, both of these fees haven’t been reviewed in years,” Hamilton said. “These don’t seem to incentivize affordable housing or mobility solutions for the community. The end goal is to take advantage of the authority that we have as council to restrict the use of housing in-lieu and parking in-lieu.”

A majority of speakers, meanwhile, railed against the proposed moratorium saying it would only increase rents and negatively affect businesses.

Michael McSweeney, senior public policy advisor for the San Diego Building Industry Association, did not hold back against the proposed moratorium.

“This is something unprecedented,” he said. “In the middle of a housing crisis, we want to talk about stopping. That’s the equivalent, in my mind, if there’s a wildfire we’ll talk about water rationing.”

He, along with others, also questioned where the danger to public health safety was to call for a discussion about a moratorium, which must have been proven to enact an urgency ordinance of 45 days.

Brendan Foote, who does adaptive reuse, said the council is missing one point regarding affordable housing, the cost of land. A starting point of $200,000, for example, to purchase the land, plus thousands of dollars for city fees and then construction costs make affordable units unattainable.

“I love and respect the charm of Carlsbad Village and don’t see it going anywhere,” Foote said. “We want to see positive change. We need to get a little more creative and look at this dwelling units per acre.”

Hamilton then pivoted away from the moratorium and asked for her other concerns be prioritized before the council.

Councilwoman Cori Schumacher said it was not prudent for a moratorium, as it is up to the council how to apply the tools at their disposal for development. Also, the council does not have final authority over projects in the Barrio under the new master plan.

The Planning Commission has final say, but the council will consider taking over final approval when the master plan returns on Aug. 20.

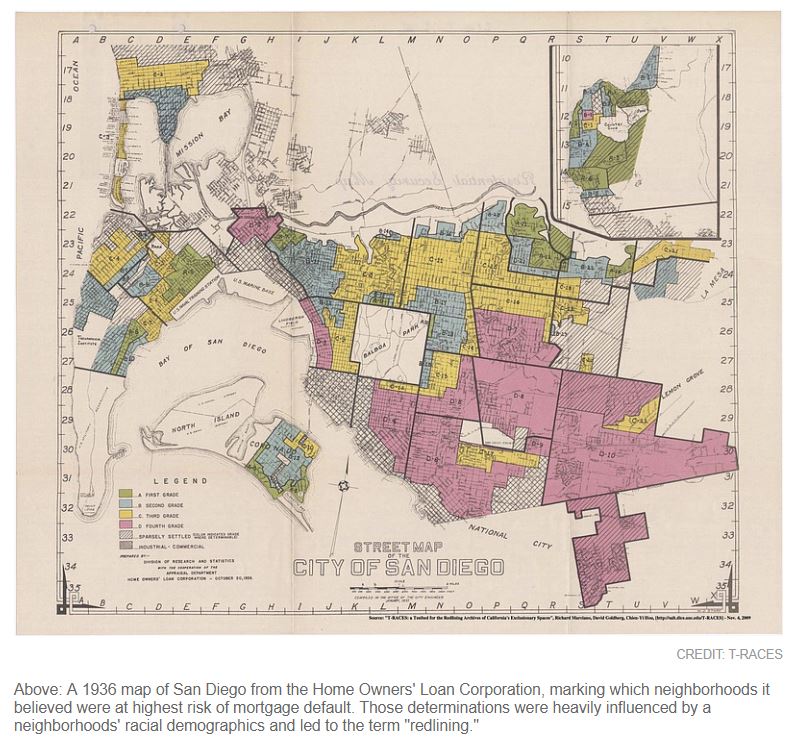

The history of housing discrimination is getting a lot of attention these days, and rightfully so. If you, or someone you know, wants to contribute, KPBS is looking for stories:

KPBS is doing an investigation into the legacy of “redlining” in San Diego.

This is the historic practice of excluding minorities from certain neighborhoods through regulations on mortgages, leases and home purchases. We’re looking into the impact this practice has had on the economic prosperity of different neighborhoods in San Diego.

Some families in San Diego may have benefitted from this history, through no fault of their own. Others may have been hurt by it.

If you or your family has any connection to this history, or if you know someone who does, please reply to this email or send an email to sources@kpbs.orgwith “Redlining” in the subject line.

Thank you for sharing your knowledge and becoming a trusted KPBS source!

There was actually a red zone in La Jolla around the Taco Stand on Pearl!

The market sure has been good to Ernie – hope he never has trouble paying the bills:

County Assessor Ernest Dronenburg announced Thursday that the county’s 2019 assessed value of taxable property is almost $575 billion, a nearly 6% increase over last year.

It’s the fifth consecutive year the assessment roll has increased by 5% or more, according to Dronenburg, who also serves as county Clerk and Recorder. The increase is likely due to improvements in the housing market, business property values and the economy in general, he said.

“Increases to the business roll are strong indicators that business owners are optimistic about the local economy and are making capital investments in property, plant and equipment,” Dronenburg said. “This year, 85% of San Diego’s taxpayers are protected by Proposition 13’s provisions, which limits their property increase to only 2%.”

According to Dronenburg, the net assessed value roll is $551.9 billion after deducting various property tax exemptions. About 1% of the net assessment roll, $5.51 billion, will be used to fund public facilities and services like schools, law enforcement departments and parks.

The assessment roll is composed of more than one million parcels of land, more than 50,000 businesses, 13,000-plus boats and nearly 2,000 airplanes and other aircraft.

Residents will be able to view the assessed value of their property assets on July 1 by visiting the Assessor/Recorder/Clerk’s website, sdarcc.com, or by calling Dronenburg’s office at 619-236-3771. In addition to assessed values, residents also have access to applications for property tax exemption.

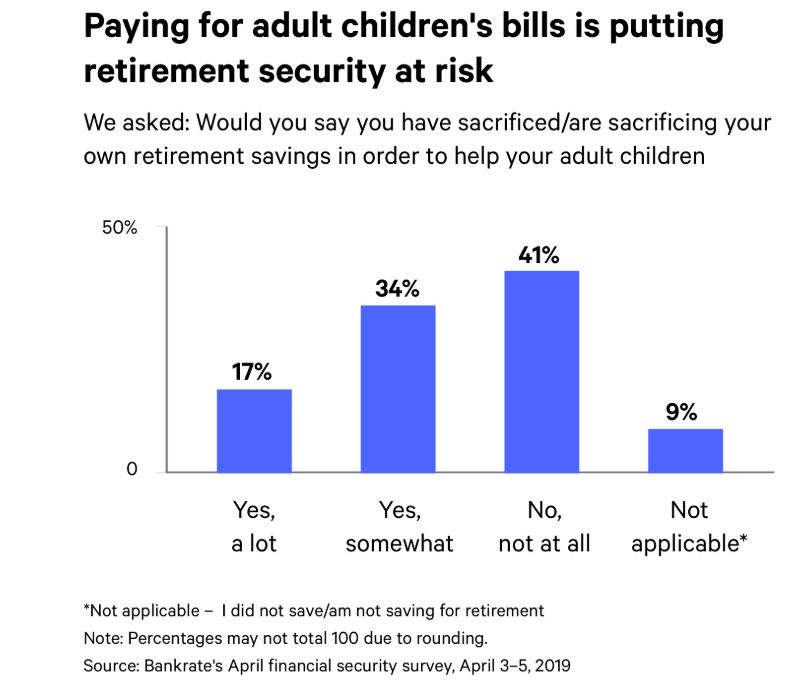

We were talking with some friends last night about how much financial support is going towards kids, and how it will affect real estate in the future.

On one hand, it’s the Bank of Mom and Dad, and helping to keep the market afloat when funding home purchases at these lofty prices for those kids with regular jobs.

However, for those kids who never get to the point of financial stabilization, the selling of the parents home will become the lottery ticket to solve their money issues.

I suggested that this is where the ibuyers could do the most harm by taking advantage of people who want and need a quick sale and who aren’t that familiar with the values.

When we were in Las Vegas for that one-day vacation, I saw more than one ibuyer ad on TV, and they were very enticing. The kids who have been strapped for years and then inherit their parents’ house might jump at the chance to get their hands on quick money – and likely leave some on the table.

Will anyone step up to protect the unsuspecting? A new challenge/opportunity for realtors!

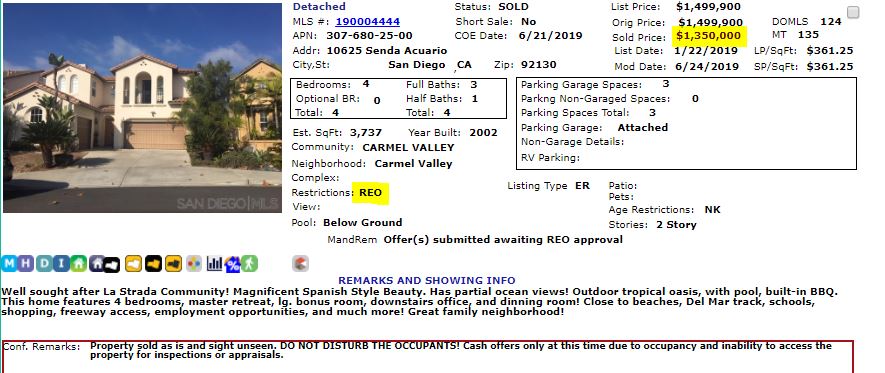

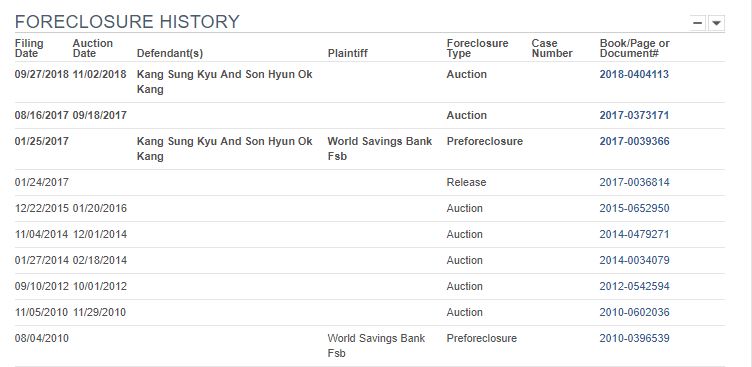

We featured this bank-owned property earlier as an online auction (which didn’t work out).

They did find a cash buyer – I hope they got in the house to take a look around!

This is a typical example of an REO sale these days. The former owners paid $1,650,000 in 2007, and used a 31% down payment. The original $1,137,500 mortgage was funded by World Savings, and undoubtedly it was a neg-am loan.

It looks like the buyers stopped paying in 2010, but instead of foreclosing and losing a truckload, the bank (Wells Fargo, who bought World Savings) just waited until they knew market value was high enough that they wouldn’t lose money:

The price at the trustee’s sale in November was $1,365,016, and they sold it traditionally for $1,350,000. It means that after paying closing costs, the bank received 100% of the principal back, plus around $150,000 of the neg-am interest that accrued.

These days, banks are only foreclosing once they can make money on them!

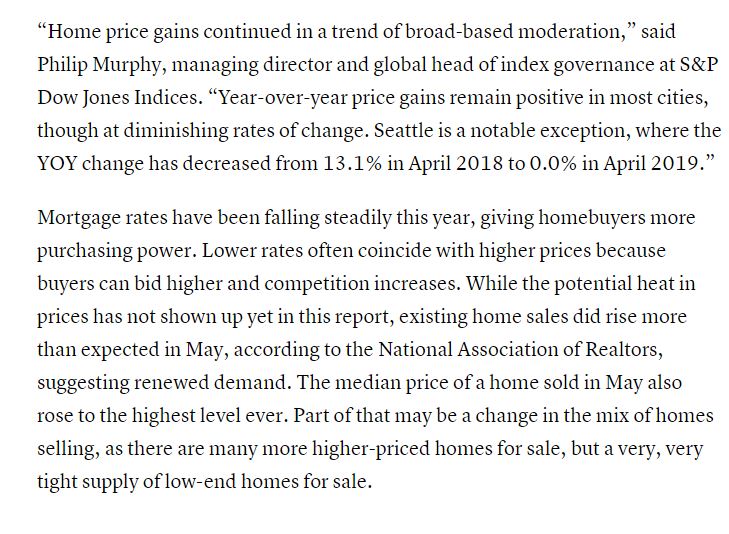

“Since last year, several forces have helped increase the market potential for existing-home sales,” said Fleming. “House-buying power, driven by falling mortgage rates and rising household income, contributed to a gain of 183,000 potential home sales compared with one year ago. Compared with May 2018, rising house prices also contributed positively, increasing the market potential for home sales by 41,000.

“Additionally, loosening credit standards boosted the marketing potential for home sales by more than 60,000 sales over the last year. Some modest growth in new-home construction also added 1,000 potential home sales,” said Fleming. “Finally, the growth in household formation, as millennials continue to form households, contributed nearly 81,000 potential home sales compared with a year ago. Despite all the positives, the market potential for home sales remains nearly 80,000 units below the level of a year ago.”

Unprecedented Homebody Era is Here

“Collectively, the aforementioned market forces contributed to a positive gain of 366,000 potential home sales, but it was not enough to offset the loss of 446,000 potential sales due to the impact of rising tenure. The average tenure length, the amount of time a typical homeowner lives in their home, has increased dramatically in the last year,” said Fleming. “Since existing homeowners supply the majority of the homes for sale and increasing tenure length indicates homeowners are not selling, the housing market faces an ongoing supply shortage – you can’t buy what’s not for sale.

“Before the housing market crash in 2007, the average length of time someone lived in their home was approximately five years. Average tenure length jumped to seven years during the aftermath of the housing market crisis between 2008 and 2016,” said Fleming. “The most recent data shows that the average length of time someone lives in their home reached 11.3 years in May 2019, a 10 percent increase compared with a year ago.

“Two trends are driving the increase in tenure length. The majority of existing homeowners have mortgages with historically low rates, so there is limited incentive to sell if it will cost them more each month to borrow the same amount of money from the bank,” said Fleming. “While mortgage rates have come down compared with last year, they are still below the 3.5 percent mortgage rates of 2016.

“The second trend influencing tenure is seniors aging in place. A recent study from Freddie Mac shows that if seniors and adults born between 1931-1959 behaved like earlier generations, nearly 1.6 million housing units would have come to market by 2018,” said Fleming. “Improvements in health care and technology have made aging in place easier, which has meant fewer homes on the market.

“So far in 2019, the market potential for existing-home sales has benefited from lower mortgage rates and rising household income, all contributing to stronger house-buying power,” said Fleming. “Surging consumer house-buying power coupled with rising household formation has resulted in strong demand for homes.

“Yet, today, we are in an unprecedented homebody era as many existing homeowners continue to feel rate-locked into their homes and seniors continue to age in place. Looking ahead, more than half of all existing-homes are owned by baby boomers and the silent generation and they will eventually age out of homeownership,” said Fleming. “But right now, housing supply remains tight – you can’t buy what’s not sale — and market potential is lower because of it.”

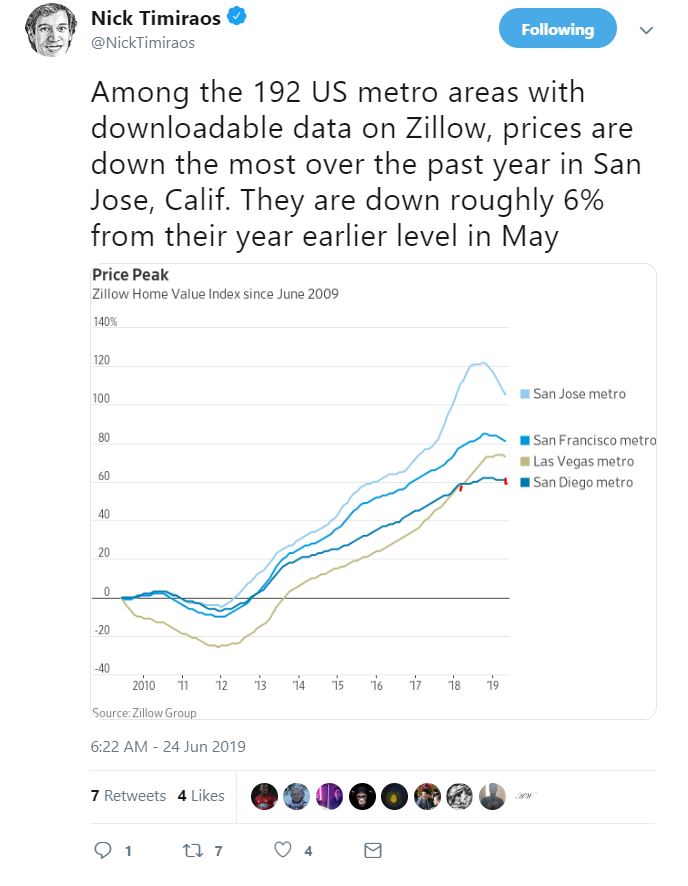

Yesterday’s Zillow index showed San Diego’s pricing to be fairly flat, and now April’s Case-Shiller Index has a similar-sounding +0.8% increase year-over-year.

We’ve bounced back from six months of negative readings, just to get back to where we were last year – and we’re still not as high as the June and July 2018 readings:

San Diego Non-Seasonally-Adjusted CSI changes:

Observation Month

SD CSI

M-o-M chg

Y-o-Y chg

January ’18

248.16

+0.8%

+7.3%

February

250.91

+1.1%

+7.5%

March

253.41

+1.0%

+7.6%

April

255.63

+0.9%

+7.7%

May

257.07

+0.6%

+7.3%

Jun

258.44

+0.6%

+6.9%

Jul

258.49

0.0%

+6.2%

Aug

257.32

-0.5%

+4.7%

Sept

256.13

-0.4%

+3.9%

Oct

255.26

-0.1%

+3.7%

Nov

253.37

-0.6%

+3.3%

Dec

251.68

-0.7%

+2.3%

January ’19

251.30

-0.2%

+1.3%

Feb

253.66

+0.9%

+1.1%

Mar

256.39

+1.2%

+1.3%

Apr

257.68

+0.5%

+0.8%

The high-tier index is similar with just a +0.5% increase over last April, and not as high as June, 2018:

The San Diego ZHVI has been mostly flat for almost two years!

The price exceptions are the superior homes and locations, particularly the one-story and newer homes, which tend to sell for more than ever before. But those cases are dwindling.

What’s saving us is how inventory has remained in check – no panic among sellers in 2019, which is quite a bit different than it was last year: