The doomers living in mom’s basement want you to believe that the sky is falling.

They’ve never owned a house before, let alone sell real estate for years. Yet, their voice is loud enough that they are winning the battle of opinions about where the market is going – mostly because the entire realtor industry is just standing quietly on the sidelines, instead of providing guidance.

There is one simple correction underway.

The gap is back!

The difference between the fixers and the creampuffs is back, and it is growing, thankfully. The homes that aren’t spruced up are getting hammered on price. It’s probably not that obvious yet because they are the listings that are just lying around not selling. But once they have been on the market for 2-3 months, they are going to get lowballed – and by then, there isn’t much the seller or listing agent can do.

Take your pick. Sell early, or sell low.

The doomers are living in your head now. They don’t take the time to dive deep into the results, or look at an open house. They just group all sales into the same bucket, check the median sales price or the Case-Shiller Index, and declare bloodbath because those too-simple measurements are down a couple of ticks.

It causes buyers to wait for the creampuffs, and ignore the fixers – or lowball them.

I made this observation in the original Coffee Bet in 2006. It was more dramatic and easier to spot back then because the banks didn’t have a problem giving away the dumps, and the downdraft was swift and certain. But these days, the sellers – all loaded with equity – are much more likely to hold out. They saw fixers selling for ridiculous prices during the frenzy, and want to believe that will still happen. But it’s the only change we need to throw the market into tumult, because nobody points out the gap.

Expect that there will be few superior properties for sale, and they’ll sell for a premium. And the rest won’t.

It would be nice if local realtors would adopt this sentiment, and publicize it.

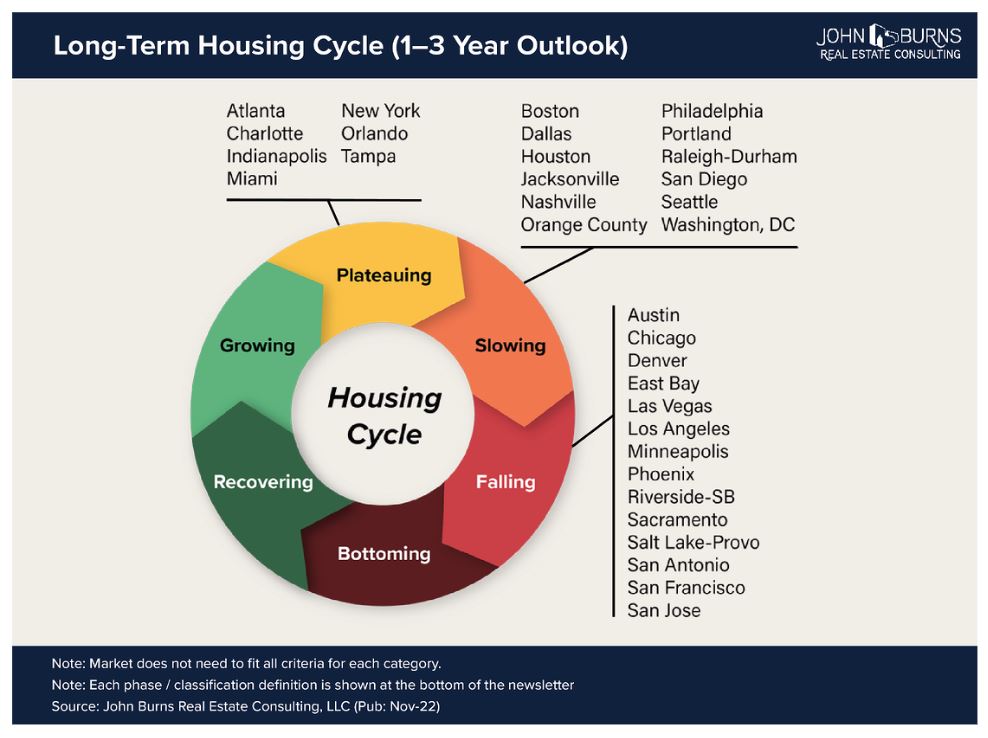

Our friends at JB have been on the forefront of market tracking for years now. They have staff that travels around the country to gather data from builders in particular, and have built a tremendous network.

I don’t mind being labeled as ‘slowing’ because…..well, I guess it beats falling!

Their definition of Slowing:

Markets in the Slowing phase face alarming affordability levels, decelerating (or even declining) home price appreciation, and rapidly slowing sales—making capital investments less attractive. Several of these slowing markets were among the first to recover from the initial COVID panic in April 2020.

In-migration and job growth, fueled by the proliferation of work-from-home policies, set these markets apart as higher wage workers relocated due to the relative affordability—most notably Dallas, Jacksonville, and Raleigh-Durham.

Current employment is well above prior peak levels in all of these markets. While strong job growth from high-wage sectors has buoyed these markets, it has also been the primary driver of their now strained affordability, with a significant number of locals now completely priced out of ownership.

YOY home price growth is decelerating rapidly, and construction volumes are pulling back from very high levels.

Their business focus is tilted towards builders and new homes, but their analyses about the general market conditions are applicable to the resale market too.

Each area will have several variables that makes it unique, but we are a society that wants to label everything with one word. I have one word for you – auction. If an auction company took over real estate, we wouldn’t need opinions, analyses, or realtors!

Yesterday I was delivering pies throughout North County, and visiting with our great supporters – who were mostly past clients. Predictably, the conversation turns to real estate, and observations about what’s going on in the market, now and in the future.

In case the subject comes up at your Thanksgiving, here are things we discussed:

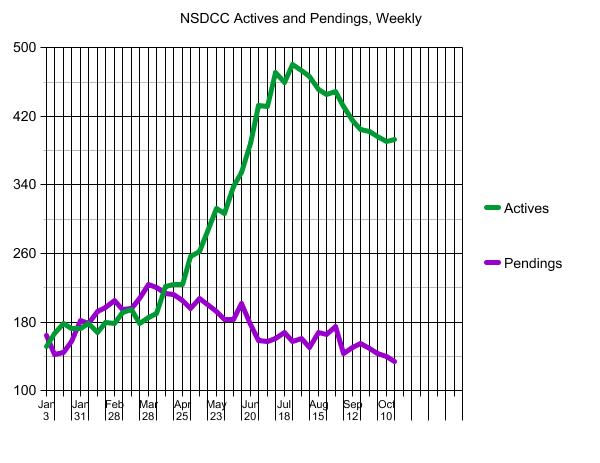

Sales are down, but they aren’t zero. There are roughly 400 houses for sale between La Jolla and Carlsbad, and the vast majority have been languishing on the market. But at least 100 of them find a way to close escrow every month – and they tend to be the spectacular homes that are priced attractively.

Sales are being hampered by the light inventory. The number of listings are 40% lower than in 2019, and next year I expect there will bethe same or fewer homes for sale as sellers decide to wait until the “market gets better”.

Mortgage rates in the 5s are tolerable, and above that is problematic. Higher rates don’t only make homes less affordable – they also cause buyers to have a psychological expectation that sellers should come off their price. The higher rates go, the more standoff there will be between buyers and sellers.

To get deals, the buyers have to cause them – and they are happening. We saw how two sales near my latest listing knocked off more than 10%, and here’s another one from yesterday:

I am re-examining one of my favorite seller slogans from many years ago; I’m Not Giving It Away. Back when potential sellers had little, if any, equity, they would fight like crazy just to make sure they came out of escrow with at least enough for a steak dinner. But everyone has gobs of equity now….and those who need to move bad enough are giving up decent chunks of it. It means we could have a much faster decline in pricing than ever before.

I am still convinced that by March/April, the spring selling season will kick in and homes will be selling briskly for all the money. It’s likely that we’ll get off to a slow start as both sellers and buyers wait for someone else to go first, but by the end of March or April we will see bidding wars again.

Realtors are woefully ill-equipped to handle these conditions. They have no strategies for a soft market and are very reluctant to price aggressively or reduce a list price properly. Here is a discussion of typical agent comments.

The blog is picking up momentum, which hopefully means more people are looking to get better-educated about the market conditions, which is encouraging:

Thank you for being here! I appreciate all of you and Happy Thanksgiving!

Try out Grandma Klinge’s pumpkin bread (mastered by Natalie) from the Compass cookbook:

Could we have a decent spring selling season next year?

Is there any precedent of our market settling down that quickly?

Home sales had been struggling for months, and then the Lehman Brothers collapse in September, 2008 helped to trigger the Great Recession, and millions of foreclosures and short sales.

Yet, just seven months later, home pricing hit the bottom in San Diego (see graph above).

We are enduring a once-in-a-lifetime spike in mortgage rates that are rightfully taking some time to digest. But people need to move, and by next spring, many will be buying and selling homes around here.

The Fed will have slowed down by then, the political landscape looks like it will drift more towards the center, and realtors are figuring it out that you have to have a spectacular-looking home with an attractive price to have a chance at selling. All will play a role in giving home buyers more confidence.

My listing from two weeks ago that generated 18 offers – 17 of them financed – and got bid up by 27% over the list price is proof that, in spite of the common perception that the market is dead, there is a strong demand right under the surface, just waiting for the right house, at the right price.

Those who were reading this blog in the 2008-2013 will remember how negative we were about the market, and how long it would take before it bottomed out – most figured it would be years and years. True, we aren’t going to get the government stimulus this time, but I don’t think we need it.

There will be a lot of skepticism in the market – and most people will wait until others go first before they think of entering the market themselves. We probably won’t ever see the sizzling frenzy conditions again, but a healthy semi-surge for a couple of months next spring seems like a good possibility. If it happens, it will be because sellers and agents got smart about selling in the post-frenzy era.

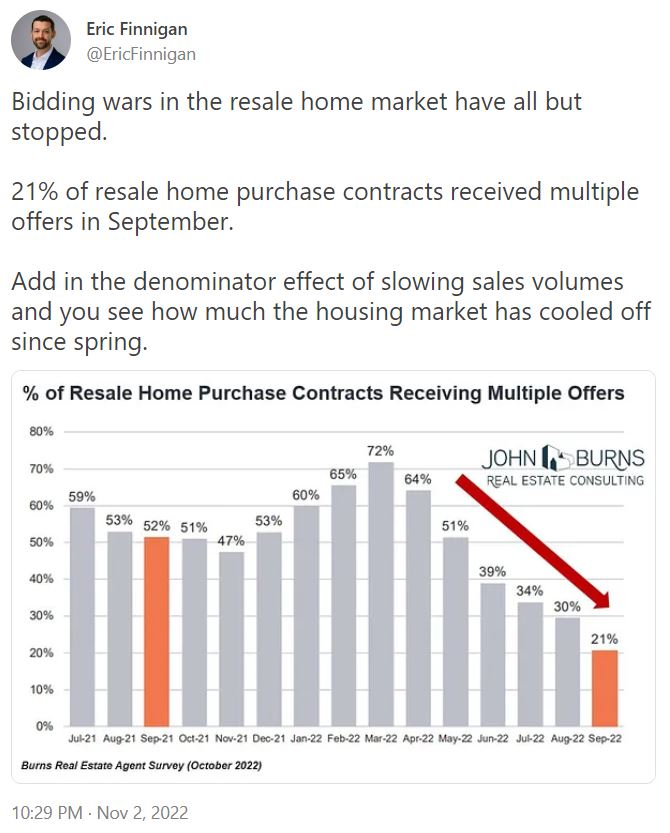

Of course the current conditions look worse when comparing to the hottest real estate market ever. Having bidding wars on 21% of homes for sale sounds great to me.

The discouraging part about Bill’s post today is how the realtors have bought into the negativity.

This is the first downturn to be affected by amateurs on social media, and realtors can either price ’em high and repeat these same negative talking points seen everywhere now, or they can get better at their craft, price their listings attractively, and be part of the solution:

#Houston, TX: “Home prices have most first-time home buyers priced out of home ownership. It’s even worse with the higher interest rates decreasing what the buyers can qualify for.”

#Denver, CO: “Cost of living [and] interest rate [increases] are keeping most buyers from buying.”

#Baltimore, MD: “The market is transitioning. Inventory is still low and the number of buyers looking is less due to rising interest rates. Buyers are qualifying for less, so they are pulling back. [I am] seeing less as-is sales, more home inspections, and negotiations overall.”

#Sarasota, FL: “I’ve had numerous buyers looking but the prices are much higher than they want to spend. Many pulled back waiting for the market to go down.”

#LosAngeles, CA: “Skyrocketing interest rates are pushing buyers out of the market (they can no longer afford homes that were in their price range just a few months ago) and making homes more difficult to sell for sellers and their agents.”

#Phoenix, AZ: “Buyers are very nervous about making a decision.”

#NewYork: “Open house attendance is weaker than usual, and sales take longer.”

#Minnesota, MN: “Still seeing a fair number of cash sales as competition to financed sales.”

#StLouis, MO: “Things are slowing down slightly, but I have found that the good properties are still moving quickly with multiple offers and going above ask.”

#Barre, VT: “Our local market in Lamoille County is very flat and challenging. Local working families are outpriced by the prices and interest rates. The neighboring resort town has slowed but there are still cash buyers for the million plus market.”

#OrangeCounty, CA: “Interest rates have put the brakes on the market.”

I did sign up to be on their realtor-comments list!

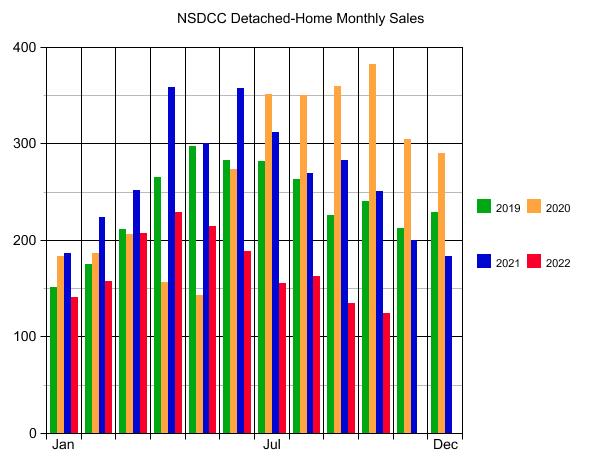

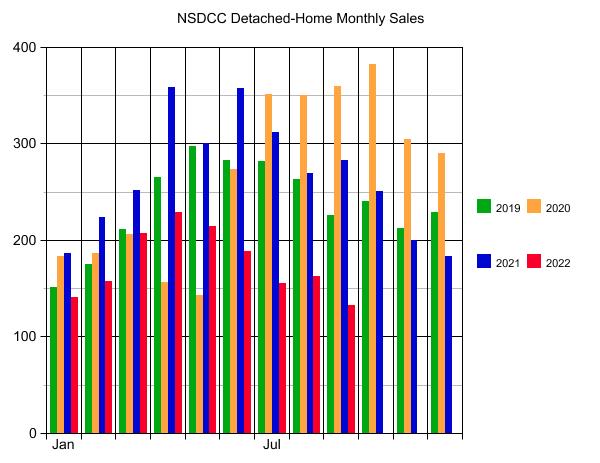

I’ve been hoping for 100+ sales per month the rest of the way this year.

Currently, the October count is 108, so it should get up to around 120 sales by mid-November. Here are the monthly sales and pricing for 2022:

NSDCC Detached-Home Monthly Sales & Pricing, 2022

Jan

140

$2,828,988

$2,855,213

$2,234,944

$2,240,000

Feb

158

$3,063,331

$3,108,907

$2,149,500

$2,386,500

Mar

207

$3,247,251

$3,337,348

$2,400,000

$2,625,000

Apr

227

$3,190,161

$3,251,604

$2,350,000

$2,550,000

May

214

$2,941,080

$3,030,794

$2,350,000

$2,480,000

Jun

188

$2,871,956

$2,881,314

$2,297,500

$2,350,000

Jul

152

$2,892,729

$2,833,588

$2,272,000

$2,280,000

Aug

161

$2,953,967

$2,849,332

$2,200,000

$2,150,000

Sep

134

$2,652,892

$2,560,764

$2,134,500

$2,020,000

Oct

108

$3,168,167

$3,042,502

$2,250,000

$2,150,000

I noted last week that the September average and median sales prices were both 23% lower than they were in March. It looks like the final October data could end up being higher.

The average and median sales prices are easily affected by the types of homes that are selling. The recent environment has had smaller, less-expensive homes selling, while the higher-end market has been languishing.

Let’s include more statistics to fill out the picture:

Month

Sales

Average SP

Avg $$/sf

Avg SF

Median SP

Med $$/sf

Med SF

Mar

207

$3,337,349

$1,028/sf

3,498sf

$2,625,000

$853/sf

2,800sf

Sep

134

$2,560,764

$911/sf

2,887sf

$2,020,000

$790/sf

2,598sf

Oct

108

$3,042,503

$931/sf

3,387sf

$2,150,000

$782/sf

2,840sf

While the October average and median sales prices make it look like we’ve turned the corner, once you analyze the house sizes and $$/sf, you’ll see that buyers are still getting more for their money today.

Unfortunately, none of the talking heads in the media will look any further than the median sales price.

Once their house-hunting vacation concludes in February, all potential home buyers will do is decide if the change in the median sales price supports their mindset about purchasing.

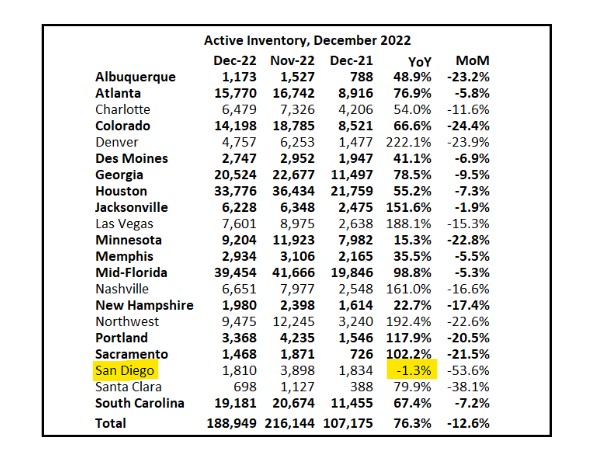

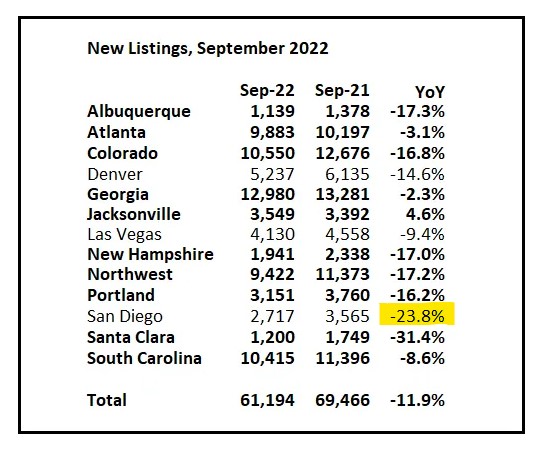

Bill has been following the inventory in different markets, and San Diego is faring much better than other areas. He is showing a 23.8% drop in new listings YoY, but last year was the record low. Look at the previous years:

September New Listings, San Diego County Detached and Attached Homes:

2005: 6,325

2006: 5,735

2007: 5,448

2008: 5,101

2009: 4,328

2010: 4,696

2011: 4,013

2012: 3,578

2013: 4,265

2014: 4,367

2015: 4,185

2016: 4,267

2017: 3,953

2018: 4,506

2019: 3,959

2020: 4,389

2021: 3,570

2022: 2,853

Everyone talks about the demand-side, but our market is being impacted by the lack of supply too.

Could there be demand that isn’t being satisfied because there aren’t more quality homes for sale listed by good agents at attractive prices?

I had 100+ people come to open house this weekend, and there were legitimate buyers in the group.

I wanted to show a house this weekend, and the showing instructions said to text the listing agent. I started via text on Wednesday, but literally never got a response, so I didn’t show it. The listing is still active today.

Higher rates haven’t changed the frustration of finding the right house, at the right price.

The inventory is probably going to dry up further and more sellers get convinced that now isn’t a good time to sell. With a tight selection of quality homes for sale, those who are willing to sell now aren’t going to be deterred from trying peak pricing, or close.

Example: My $1,800,000 listing in Aviara? This just popped up around the corner, priced at $2,295,000:

Those folks might sell, and they might not, but they should help me with mine! My point is that we are not seeing an increasing flow of new listings being priced lower and lower in an attempt to get out now. It’s actually quite the opposite.

I tell potential home buyers to keep looking because you never know when you will find the right house – which is the most important part of the equation. Most will convince themselves that it will be easier to find the right house if prices came down, and besides, the current crop isn’t that interesting.

To keep it simple, let’s just calculate how mortgage rates have changed the equation:

Purchase Price: $2,000,000

Loan Amount: $1,600,000

30-yr jumbo rate: 3%

Monthly pmt: $6,746

Buyers who expect the sellers to make up the entire difference with a lower sales price will have to wait until they can find a home that meets this description:

Purchase Price: $1,400,000

Loan Amount: $1,120,000

30-yr jumbo rate: 6%

Monthly pmt: $6,715

If home prices come down 30%, it will enable buyers to buy the same house for the same monthly payment – and with a $120,000 smaller down payment too. If it happened over the next five years, it means we only need to drop about 6% per year, and we’ve already dropped more than that in 2022.

Or let’s say you want to roll back to pre-pandemic pricing.

NSDCC homes that sold in February, 2020 closed at a median of $509/sf, and last month the median was $793/sf which means we’d need a 36% decline to get back to pre-pandemic pricing.

How are you going to play it?

Are you going to wait until you actually see homes selling for 30% to 36% off to get back into the game?

Are are you going to wait until rates come back to 3%?

Or do we acknowledge that the buyers who have more horsepower are going to jump back in sooner, and there’s not much chance of prices dropping the full 30% to 36%? The highly-motivated affluent folks will probably be satisfied with 20% off, and they will derail a full decline. It’s what happened in 2012.

Can you live with 20% off?

Because if you can, then you need to stay in the game.

If the #1 variable is buying the right house, then #2 is timing.

I think the affluent will be looking next spring, and if they find a suitable house, they are going to buy it. By then, some of the statistical pricing gauges will be showing 10% to 20% declines, either nationally or in isolated markets. Because the local pricing isn’t that nuanced and buyers just want a house, they will decide that’s close enough and go ahead with the purchase.

To support my suspicion, I’ll note that during the frenzy, it was the same mentality, just in reverse.

When people found the right house, they just paid whatever it took – even if it meant paying $500,000 to $1,000,000 over the list price! Nothing else mattered besides getting the right house.

Most buyers won’t believe their eyes, and the volume will be thin. But sellers will appreciate any momentum and be encouraged to price their home for about what they thought they could get, with not much discount. Buyers who want discounts will be relegated to scouring through the dent-and-scratch bin, or hope that moving during the off-season might be more fruitful. Great for them.

The number of NSDCC detached-home sales in September is up to 133 today, which is pretty good. There are only 138 pendings currently, but 34 sales have already closed in October so there is a decent chance that we’ll have 100+ sales this month too!

The drastically-lower YoY sales will give participants the idea that the market conditions keep deteriorating, but to me, it is a sign that sellers are holding out on price.

If we can just average 100 sales per month in the fourth quarter, I’d consider it a successful end to 2022!

It’s natural for most buyers to want to see what happens in springtime, and I think we can all predict what’s coming. The 2023 home sellers aren’t going to believe that the old comps don’t matter any more – and they will price their home within 5% of the peak pricing.