People get excited about home prices going up or down based on the median price statistics, which are easily skewed. The explanations are humorous too, where the declines tend to be dismissed, and increases lauded (in bold below).

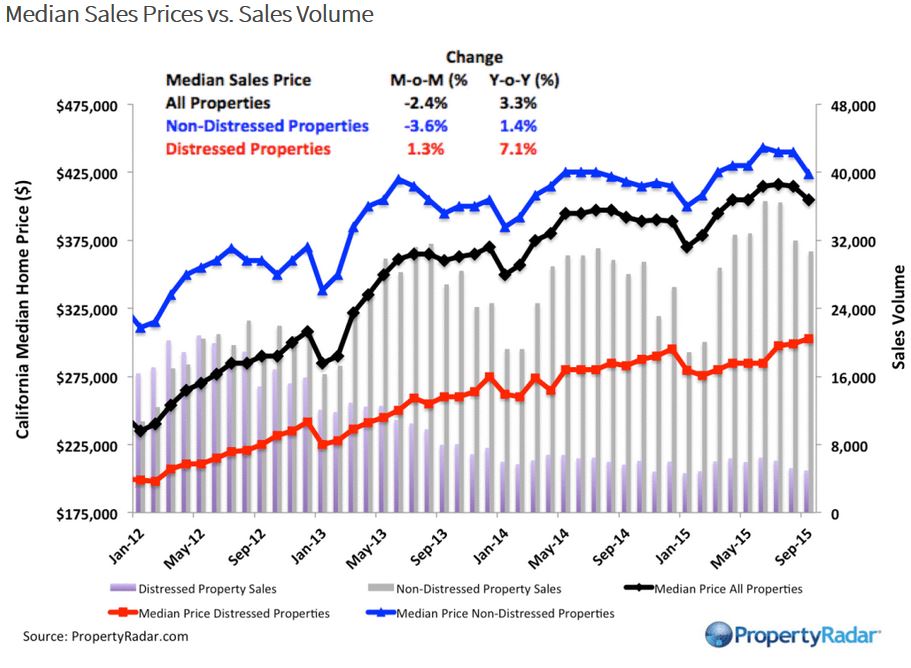

According to PropertyRadar’s report, the median price of a California home in September was $405,000, which was down 2.4% from a revised $415,000 in August. It was also down 2.6% from the 2015 high of $416,000 in July.

On a year-over-year basis, the median price of a California home was up 3.3% from $392,000 in September 2014.

Prices may be up on a yearly basis, but Schnapp said that price appreciation in many parts of the state has slowed or stopped entirely.

In fact, on a monthly basis, prices were lower in 21 of California’s 26 largest counties, Schnapp said.

According to PropertyRadar’s report, the counties with the largest price declines were Contra Costa (-5%), Kern (-5.2%) and San Mateo (-3.3%).

San Francisco prices fell 11.8% for the month but the decline is likely an artifact of the mix of homes sold rather than an actual price decline, PropertyRadar’s report showed.

On an annual basis, prices are still appreciating, but in general at a much slower pace.

Home prices in a few northern California counties, mostly concentrated in the Bay Area, continue to appreciate rapidly. Counties experiencing the highest annual price appreciation were Santa Cruz (+18.1%), Merced (+15%), Santa Clara (+13.8%) and San Mateo (+11.3%).

“Homes in the Silicon Valley corridor, consisting of San Francisco, San Mateo and Santa Clara counties, continue to buck statewide trends and are experiencing double-digit price appreciation,” Schnapp said. “The increased demand from plentiful well-paying jobs, sky high rents, and fear of higher mortgage interest rates have propelled home prices into the stratosphere.”

Schnapp said that in September, more than half of all homes sold in San Francisco and San Mateo counties exceeded $1 million.

“I am frequently asked how long can this continue?” Schnapp said of the San Francisco price explosion. “My answer is, ‘Until you run out of eager buyers and bankers willing to lend,’ and we clearly are not there yet.”

These builders have been successful with their ‘Modern Farmhouse’ look (thanks TT!) in two different locations around Encinitas, where the surrounding neighbors were somewhat inferior.

Without having the unique farmhouse look (and larger yards) to help propel the sale, these could be more of a challenge:

The Silicon Valley market is on hyper-speed, but you have to wonder if the same trend is happening in slow motion around other tony coastal communities:

Have you seen the remark, “Back on market, no fault of property”?

Well then……..whose fault was it?

The agents.

Somebody allowed the buyers and sellers to believe they had a deal. Rarely is it intentional – and almost always it’s due to a condition that could have been remedied in advance, if both agents were on their game.

When a buyer does want to cancel, it is their agent’s duty to craft a real whopper of an excuse so there is no conflict in getting the deposit back. As a result, the real reason for cancelling is rarely known.

The most common excuses:

Buyer didn’t qualify.

Some other babbling, semi-conscious drivel.

There is no excuse for getting offers accepted with buyers who don’t qualify. The frenzy is over, so there is no reason to rush an offer before the lender has taken a full application and has had it underwritten.

I’m even reluctant to believe that the buyer got laid off – come on, they had no idea that their job was in peril? It’s hard to believe any employee would be out shopping for homes if they thought there was any unrest at work.

But it is a great excuse for cancelling – how can the sellers blame you?

If the excuse given is just a smoke screen to ensure the deposit is returned, then what was the real reason? Could there be a solution to the real reason?

Two places where agents screw up:

Don’t verify the prequal (for buyers who really cancel for that reason).

They don’t try to save the deal.

Upon being notified of an impending cancellation, listing agents rush to their computer and quickly mark the listing BOM (back-on-market). Many will add ‘no fault of the property’ (which is really code for ‘flaky buyers’, ‘stupid buyer’s agent’, or both), and the listing agent goes back to their prayer vigil.

If the listing agent took the best of many offers received during the first week, then you can’t blame them for being confident that other buyers might still be interested. But if they’ve been struggling for weeks or months to find a buyer, the writing is on the wall – the price isn’t working.

Price can fix anything. Either agent can take the initiative too.

It happened to me yesterday. My buyers and I went the conventional route, and conducted the home inspection after our offer was accepted (which included a seller’s counter-offer insisting upon a 7-day inspection period). We scrambled to complete the inspection promptly, but it revealed enough problems that my buyers said ‘forget it, let’s cancel’.

But because I had also gotten repair quotes on items we thought could be an issue, I was at least able to put a price on it. I urged my buyers to consider buying the property, if the price was right.

They said they would buy it, if I could get the seller to knock off $20,000.

We had made our offer the first day the house was on the market, and according the the listing agent, there were multiple offers. The $20,000 reduction seemed like a tall order, but anything is possible!

I went to work on crafting a powerful and compelling case on why the sellers should do it (without including any repair quotes or complaints because those just start a fight over what is worthy).

I included a concession (a must) that if agreed, we would release all contingencies the same day, and that we would close in two weeks.

The sellers agreed to the $20,000 reduction.

For those who wonder why you should have me assist you with your real estate needs – this is it. In every sale, there are opportunities where agents can make or break a deal. I know they are coming – I’m looking for them – and I find ways to save deals and create a win-win for all.

The “11 semi-custom and personalized estate homes designed with Agrarian inspired architecture” on the corner of Santa Fe and Lake in Encinitas are different than most new houses we see these days. The lots are 30,000sf to 53,000sf, and detached guest houses and shops can be added too.

Millennials have tough new competition for the condominiums and apartments heating up the nation’s housing market: Mom and Dad.

Roughly 10,000 baby boomers are retiring each day, and recent data shows that half of those who plan to move will downsize when they do. Many are seeking the type of urban living that typically has been associated with young college graduates — so much so that boomers are renting apartments and buying condos at more than twice the rate of their millennial children.

“There’s not one thing I miss about my house,” said Abby Imus, 57, who recently moved with her husband into a condo in downtown Bethesda, Md., three miles and a lifetime away from the house they lived in for more than two decades. “I was so ready to leave.”

This new generation of empty nester is reshaping the recovery in real estate after the industry suffered its worst setback in half a century during the Great Recession. Boomer demand has helped fuel a surge in high-end housing that features two-bedroom units and large kitchens reminiscent of boomers’ suburban homes. That could have big implications for cash-strapped millennials, who had hoped to snag affordable studios in buildings developed to house 20-somethings.

The data suggests that boomers who are downsizing are relatively well-off. Harvard University’s Joint Center for Housing Studies found that those ages 55 and older accounted for 42 percent of the growth in renters over the past decade. In addition, the wealthiest tier of American households made up about one-third of new renters between 2011 and 2014.

“Boomers will pay a premium if you can give them exactly what they want,” said Matt Robinson, principal at MRP Realty in the District. “Something closer to what was in their house, and that pushes up the price; they’re happy to pay for it.”

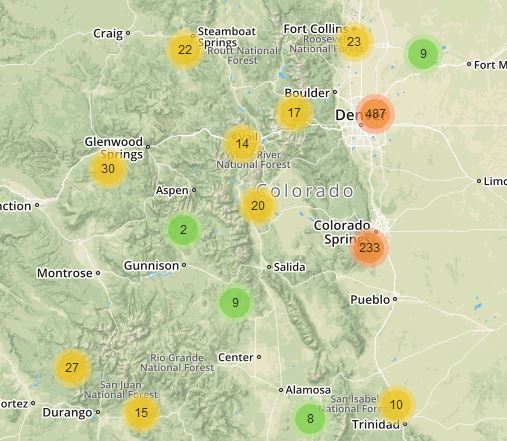

We will probably see more initiatives on the ballot about legalizing marijuana in California – maybe as soon as 2016? Look at the boost it has given Denver’s real estate market – and paying wild premiums too:

One in 11 industrial buildings in central Denver is full of marijuana.

The state’s cannabis industry occupies at least 3.7 million square feet of industrial space in Denver, clustered in areas of older warehouse stock, including the Interstate 25-Interstate 70 junction, Montbello, central Denver and along the Santa Fe Drive corridor in southwest Denver, according to commercial real estate firm CBRE.

Between 2009 and 2014, the industry’s appetite for real estate was voracious, with marijuana cultivation gobbling up more than a third — 35.8 percent — of all industrial space leased in Denver during that five-year period.

Braoden mortgage access to those who don’t have a credit score? Counting income from those not on the loan? Traditionally, the term ‘family member’ has been a loosely-defined concept in mortgage qualifying. From the wsj.com:

Collecting pay stubs for a home-mortgage application has been a time-honored tradition, barring a few ill-fated years running up to the financial crisis. But if changes announced by mortgage-finance company Fannie Mae catch on, that process could go the way of the dodo.

Fannie Mae on Monday said it would allow lenders to use employment and income information from a database maintained by credit bureau Equifax to verify borrowers’ ability to handle a loan, rather than relying on the traditional documentation process of collecting physical copies of pay stubs and tax data. The move is expected to make the mortgage process easier for borrowers and lenders alike.

Fannie announced other changes it said could broaden mortgage access for some borrowers.

The mortgage giant will ease the lender process for granting loans to borrowers who don’t have a credit score, a key issue for advocates for certain minority groups that are less likely to have traditional credit histories.

Likewise, Fannie in mid-2016 also will require lenders to begin collecting “trended” credit data from Equifax and TransUnion, which includes longer-term borrower credit histories.

In August, Fannie rolled out a new program that let lenders count income from nonborrowers within a household, such as extended family members, toward qualifying for a loan.

But for more than a year, some advocates and industry groups also have pushed the Federal Housing Finance Agency, which regulates Fannie and Freddie, to allow the companies to use alternative credit-score models that take into account utility or rent payments.

When police responded to reports of a squatter at a San Francisco mansion over the weekend, they didn’t expect to catch an alleged art thief believed to have stolen and sold paintings valued at more than $300,000.

While squatting in the home, Jeremiah Kaylor, 39, took 11 paintings from the walls and sold them through social media and pawn shops, said Officer Carlos Manfredi, a spokesman for the San Francisco Police Department. Nine of the 11 paintings have been recovered.

Kaylor was charged with trespassing and 10 counts of burglary, Manfredi said.

The initial call about a possible squatter at the home on the 3800 block of Washington Street came Saturday just before 11 p.m. When police made contact with Kaylor, he produced documents allegedly showing he was going to be the proprietary owner of the home, police said.

“This individual produced some type of paperwork that looked like it was official, saying he had a right to stay there,” Manfredi said. “It is a little sophisticated … not typical for squatters to do.”

When police were unable to reach the homeowner and sales agent, they left. But the next day, the sales agent called police and said no one should be inside.

Kaylor may have been squatting there for as long as two months, Manfredi said.

Trustindex verifies that the original source of the review is Google.

We sold a home with Jim and Donna and from beginning to end they were consummate professionals. Their initial walk through the property resulted in a list of items to be repaired or updated. They supplied a list of vendors and job quotes to do the repairs and updates. We originally wanted to sell ‘as is’ and just get it over with. They gave us a selling price for ‘as is’ and options for doing a few updates/repairs to doing it all with the selling price for each option. We agreed to do all they suggested and we sold for the exact price they predicted. For every dollar spent we got back more than $2 back in the selling price. And they got that price in a rising interest rate environment! Donna and Jim are extremely detailed and guide you through ever aspect of the sale. There were no surprises thanks to their guidance. We couldn’t be more pleased with their representation.

Thank you Donna and Jim,

Jerry and Mary

Heather Quejada

March 27, 2025

Trustindex verifies that the original source of the review is Google.

We have known Jim & Donna Klinge for over a dozen years, having met them in Carlsbad where our children went to the same school. As long time North County residents, it was a no- brainer for us to have the Klinges be our eyes and ears for San Diego real estate in general and North County in particular. As my military career caused our family to move all over the country and overseas to Asia, Europe and the Pacific, we trusted Jim and Donna to help keep our house in Carlsbad rented with reliable and respectful tenants for over 10 years.

Naturally, when the time came to sell our beloved Carlsbad home to pursue a rural lifestyle in retirement out of California, we could think of no better team to represent us than Jim and Donna. They immediately went to work to update our house built in 2004 to current-day standards and trends — in 2 short months they transformed it into a literal modern-day masterpiece. We trusted their judgement implicitly and followed 100% of their recommended changes. When our house finally came on the market, there was a blizzard of serious interest, we had multiple offers by the third day and it sold in just 5 days after a frenzied bidding war for 20% above our asking price! The investment we made in upgrades recommended by Jim and Donna yielded a 4-fold return, in the process setting a new high water mark for a house sold in our community.

In our view, there are no better real estate professionals in all of San Diego than Jim and Donna Klinge. Buying or selling, you must run and beg Jim and Donna Klinge to represent you! Our family will never forget Jim, Donna, and their whole team at Compass — we are forever grateful to them.

Lou F

March 27, 2025

Trustindex verifies that the original source of the review is Google.

WeI had the pleasure of working with Klinge Realty Group to sell our home in Carmel Valley, and I cannot recommend them highly enough!

Jim and Donna demonstrated exceptional professionalism, offering expert guidance on market conditions and pricing strategy, which resulted in a quick and successful sale.

Communication was prompt and we were well-informed throughout the entire process.

For anyone looking for a dedicated and knowledgeable real estate team, look no further!

---

William Sams

March 25, 2025

Trustindex verifies that the original source of the review is Google.

Donna and Jim Klinge of Klinge Realty Group have our highest possible recommendation. From Donna and Jim’s first visit to our house through closing their advice and counsel was candid and honest in all dealings. They kept us fully informed throughout the process. The house sold less than three days after listing with a two-week closing. My wife and I have sold several houses during our lives. This was by far the best experience. Klinge Reality is a premium service realtor. You can’t make a better choice for someone to sell your home fast and for top dollar.

Emily Hernandez

December 29, 2024

Trustindex verifies that the original source of the review is Google.

Donna and Jim provided exceptional support and professionalism throughout the entire process. We couldn't have been happier with their efforts. They made our house shine, and thanks to their expertise, it sold above the listing price in the very first weekend! Truly a fantastic experience from start to finish.

Jesus Adrian Sahagun

November 11, 2024

Trustindex verifies that the original source of the review is Google.

This year has been difficult on our family, mainly due to having to sell our home. Thankfully we knew God had a plan for us and working with the Klinge team was a key part of it. It was an obvious decision to work with them again after such an amazing experience when purchasing the same home we needed to sell. The challenge was, how will we do this in so little time with so much going on? Jim and Donna held our hand every step of the way. Whenever an unexpected issue arose they found and provided a solution. Never once did we feel pressured to make a decision and the Klinges were always reassuring after providing the information that the decision was ours to make. Despite the curve balls, they never panicked and exemplified the “can do” attitude, making us feel optimistic and taken care of. Their expertise and professionalism was superb. But of all the reasons to work with the Klinges, the most impactful and valuable is their compassion and genuine care for their clients. We pray that we can one day purchase our forever home and you better believe that Jim and Donna will be representing us - as long as they will have us of course. Thank you again Klinge team! Your execution, experience, and care are unmatched.

SABIHA PASHA

July 23, 2024

Trustindex verifies that the original source of the review is Google.

Jim and Donna were fantastic! Jim understanding my needs, recommending potential places, pointing out the pros and cons of each property was invaluable. Then when the offer was accepted Donna’s organized guidance through the inspections, paperwork etc made the whole process seem effortless.

So grateful that I had them on my side!

Anu Koberg

July 13, 2024

Trustindex verifies that the original source of the review is Google.

We first found Jim through his blog at bubbleinfo.com, which really showcased his knowledge of SoCal real estate. Since then we've done three transactions with Jim and Donna, and they are an incredible full service agency, with Jim's deep market insight and Donna's deft contract and project management. We trust them implicitly in their analysis and strategy, which is based on years of experience. They're always available and on top of things, and we strongly recommend them to anyone.

Bjorn Isachsen

July 10, 2024

Trustindex verifies that the original source of the review is Google.

The Good

The Klinge Realty Group operates like a finely tuned machine, with a very personal touch. We contacted them on a Sunday and they were talking to us about our family and our needs on our living room couch the following day. They carefully listened to us and worked with us to identify the best and quickest path to listing within 2 weeks to take advantage of the low inventory conditions in our South Carlsbad neighborhood. They knew our tract specifically and had many previous sales there over the years - they came prepared with a thorough analysis of comparative sales and recommended a pricing strategy that they felt confident would yield offers the first weekend on the market.

The Great

Over the next two weeks Donna coordinated a range of vendors who she knew from experience could get the preparation to list work we needed done on time and with high quality. Our light tune-up involved excellent experiences with their stagers, landscapers, contractors, electricians, and plumbers. Throughout this period Donna's daily communication was clear, concise, and responsive. Any time we had questions Donna picked up the phone or texted immediately - but almost always, she answered our questions before we even knew we had them.

The Outstanding

We had a tricky situation with a shared fence that could have delayed our escrow. Donna used superb mediation skills to negotiate the terms of replacement and was personally on site with the fence contractor to make sure everything went smoothly. The fence looks great and escrow closed on time.

The Truly Exceptional

Our house came on the market on a Wednesday and between then and Monday morning Jim was personally at all three open houses. He was in constant communication explaining potential buyer reaction and strength. As he predicted offers began to come in on Saturday and each one was incrementally higher than the last. At the end we had 5 offers, 4 of which were over list, and the final accepted offer was $100,000 over list. In addition to being over list it included rent back terms that met our needs.

The Recommendation

For all of these reasons we would strongly recommend The Klinge Team to anyone wanting to sell in North County Coastal San Diego. I had been reading Jim's bubbleinfo.com blog for 15 years and knew when the time came to sell that he would be our first call. Jim Klinge is not your standard realtor. He is keenly aware of market conditions and sales strategies. And, works his tail off - though not as hard as Donna . At this point he's gone from realtor to friend and I plan to have him over to grill and chill at our new place to talk real estate, but also just about life and raising kids in San Diego. He's more interested in relationships than his sales numbers - and that's why his sales numbers are so high. We have already recommended the Klinge's to some close friends and another successful sale is on deck right around the corner...

Chris Shea

June 21, 2024

Trustindex verifies that the original source of the review is Google.

We recently had the pleasure of working with Jim and Donna from Klinge Realty Group to sell our house, and we couldn't be more satisfied with the experience. From the initial meeting, they listened attentively to our needs and provided invaluable guidance on specific improvements to get our home market ready.

Their responsiveness throughout the entire process was truly impressive. Anytime we had questions or concerns, they were quick to address them, ensuring we felt comfortable and informed every step of the way. What stood out the most was their team and extensive network of tradespeople, which made addressing any necessary repairs or updates seamless and stress-free.

Thanks to their expertise and dedication, our house sold quickly and at a great price. We highly recommend Jim and Donna to anyone looking to buy or sell a home. They are a fantastic team who truly care about their clients and deliver exceptional results.