This is the easier part – charting the next six months.

Either the Fed will pause and delight us all, or their threat of higher rates will make buyers antsy and ready to pounce. The best-looking inventory usually happens in springtime, so all the necessary the ingredients for a selling-season surge should come together nicely.

Even though I’ve had a record amount of inquiries already, I don’t think there will be many sales early on. The inventory of quality homes is excruciatingly low, the prices are filled with early-season exuberance, the market uncertainty is off the charts, plus come on – it’s only January 8th!

Sales in the first quarter will be done by those who go out and create them while most people are standing around, waiting to see what happens. The tougher, the better for me. This should be my favorite year ever!

For those who have moved in the last three years, Texas, Florida, and Tennessee have been popular destinations – with North Carolina making a surge last year. Here are things to know about moving there!

My guess was that the NSDCC annual sales would be +5%, and pricing +15% in 2022.

It was a tough year for prognostications!

NSDCC YoY Statistics

Year

Annual Sales

Median SP

Median SF

December Sales

Median SP

Median SF

2021

3,184

$1,900,000

2,852sf

183

$2,165,000

2,804sf

2022

1,937

$2,300,000

2,722sf

100

$1,892,500

2,596sf

Diff

-39%

+21%

-5%

-45%

-13%

-7%

The smaller square footage takes a little bit of the sting out of it, but anyone who guessed right about the 2022 statistics was just plain lucky.

I was close on the annual price increase, but it doesn’t mean much after considering what the median sales price was last month – which is now back to the mid-2021 range.

I would have been way wrong on the sales prediction, even if the frenzy would have continued. The sales between January and May – when the frenzy was still raging – were down 28% YoY. It shows how insane the market was in 2021, and how unlikely it will be that we will ever seen anything like it again.

But have you seen ANY superior homes selling for a discount yet? Me neither, and one reason is because there are so few for sale. Once we wade into the spring selling season, we’re going to see how the market has divided in two segments – superior vs. inferior properties – and how the affluent buyers will pay the price for the top-quality homes.

The big question is what the realtors will do.

Any agent can sell a creampuff – the homes that are well-located, upgraded, tuned-up, easy-to-show, and priced attractively. But how many properties are in that category? Maybe 5% to 10% max? The overall market, and the changes in these dumb statistics that everyone thinks mean something, will be made in the trenches by the listing agents.

Will they game up and provide excellent salesmanship that keeps homes selling for about the same prices? Or will they be like prancing bullfighters and just get out of the way as the buyers come barreling through with their demands for discounts?

When we look at these stats next year, we will know the answer.

There will be one overwhelming factor in selling real estate this year:

Buyers Will Want To Pay Less.

They are coming into every situation with that mindset. Whether it’s online or in person, they will be looking for ANY reason to NOT buy this house. If they can’t find one, they will at least be doing the mental math on how much money they will have to pay to customize it to their tastes……and they will want someone else to pay for it.

It’s a 180-degree change from the frenzy era when buyers just wanted to win a house. Nothing mattered during the frenzy – bad floor plans, bad locations, bad improvements, bad agents, and bad prices didn’t stop buyers from paying insane amounts OVER the asking price. And what’s worse – those are now the comps!

Will sellers adjust?

Will listing agents adjust?

Here’s the first thought to go through their mind:

Let’s add a little extra to the list price to compensate. We can always come down later!

Oh, great.

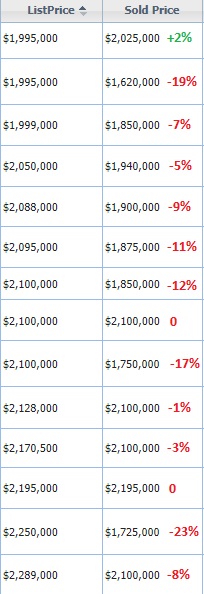

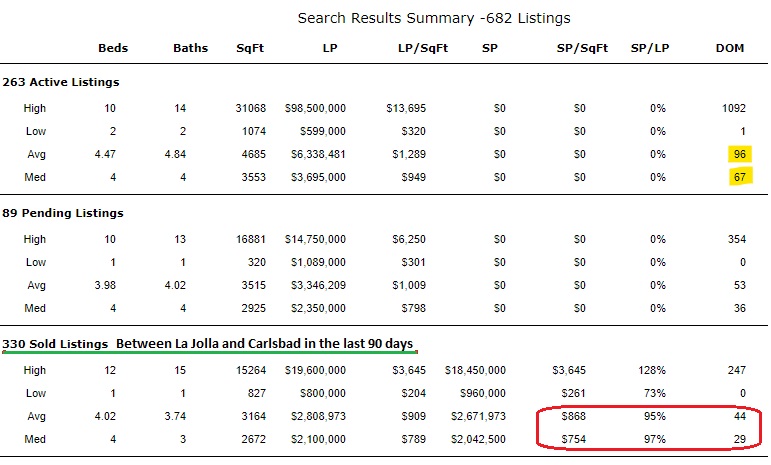

How is it playing out so far? These are NSDCC sales from the last 30 days:

These are starter homes and mid-rangers for the area – not the high-end where it’s more challenging.

It will be easy for sellers to shrug it off, and mentally prepare to sell for 2% to 4% under their list price…..because they already added it on top! But 31% of the recent sales closed for a double-digit percentage below their list price.

In the last couple of years, we’ve followed how many new listings happen in January. It’s been a good indicator of what to expect for the Spring Selling Season!

Here is some historical perspective (below). I included the stats from 2009, which was the last time the sky was falling and nobody wanted to sell their house. I would gladly take those numbers now!

For those who were thinking it’s so bad that January’s count might be single digits, there has already been seven new listings this year – though four of them were refreshed listings from last year.

Number of Listings Between La Jolla and Carlsbad

Year

Previous November

Previous December

January

1st Qtr

1st Half

2009

340

259

458

1,422

2,873

2019

292

234

418

1,280

2,716

2020

257

177

354

1,085

2,309

2021

240

181

289

986

2,171

2022

166

127

223

730

1,707

2023

141

82

7

?

?

Leave your guess in the comment section of the number of January listings, and whoever is closest to the actual count on February 15th will receive four tickets to a Padres game in 2023! This isn’t a fancy way for me to get your contact information and keep calling you until you buy or die. You don’t even have to leave your contact information – just check back on February 15th.

Reasons why January’s inventory will be LOWER than expected:

Sellers will wait until the market gets ‘better’.

Sellers will wait until somebody else goes first.

Sellers are distracted by a big playoff run by the Chargers.

Reasons why January’s inventory will be HIGHER than expected:

Panic selling – sellers who want to get out early in the season.

More boomers are getting older every year.

Realtors refreshing their listings more often.

There is no evidence that there will be a surge of hundreds of listings. Though there are more active listings today than there were at this time last year (265 vs 152), it only means the 4Q22 selling success rate was lower than in the frenzy years.

The guesses from last year’s contest:

142 The other Bob

181 Eddie89

201 Daniel Nicolas

210 Drew

215 Joe 222Majeed

230 Lifeisradincbad (he was a winner in 2021)

237 Curtis Kaiser

245 doughboy

250 Deckard Mehdy

259 Susie

260 Derek (the other winner in 2021)

270 Skip

278 Haile

286 Matt

290 Esteban del Rio

294 Tom

295 Rob Dawg

300 BWell_SoCal

312 big T

325 Mortgage Guy

373 Rob

The winner will be the closest guess, so leave some room around your number to heighten your chances.

Last January’s count was 30% lower than it was in 2021, to which I made this comment:

The 2022 inventory count was 2,832 (so far).

What it’s like watching a game from these seats? Here are 15 seconds:

A slow start is guaranteed this year because the existing inventory is so picked over – and those sellers aren’t budging on price. Instead, they are willing to wait…..and whether they realize it or not, they are waiting and hoping for new listings to hit the open market at prices that make their home/price look better.

It’s a big gamble in 2023.

Are the 2023 sellers going to list their home for a price that’s higher than those that have been languishing for the last 2-3 months? Or for less? If they are smart, they will list for less and getter done.

Either your list price is selling your house, or it’s selling the house down the street.

Optimistically, what are positive things that could happen this year?

The Fed pauses in March. They meet twice in the first quarter of 2023 – February 1 and March 16th. I’ll live through another 1/2% hike a month from now, but then a surprising Fed pause in March would give the spring market a welcome boost – and hopefully keep mortgage rates in the 5s.

There were close to 2,000 NSDCC homes sold in 2022. We’ll probably have between 1,200 and 1,600 sales this year? A Fed boost would give the spring market a few months to transact in a more-predictable environment, and probably be the difference between 1,200 and 1,600 NSDCC sales.

Have you heard anything new about the site of the old Power Plant in Carlsbad? Or the Ponto site? I didn’t see anything in the city-council agendas from the last couple of months, but they should be in the works. The power plant site is not big enough to be a major residential site, but it would get interesting if try to turn it into a higher-end hotel (like they did at the Alila Marea and at the pier in Oceanside). Nothing on the 14-acre Ponto site either – with a current plan for a luxury resort hotel with 274 rooms and 48 timeshares that’s been for sale at $38,000,000 but they put their listing on hold last week.

If they want to do something to increase the demand for homes, they could make it easier to get a mortgage. Self-employed people still don’t have reasonable access to mortgages at market rates. If a big lender was willing to calculate the borrower’s income from bank statements instead of tax returns, more buyers would qualify. But the loans need to be at a decent rate – and a seven or 10-yr ARM would be fine (it doesn’t have to be a 30-year fixed rate).

Speaking of ways to improve the supply and demand for homes, converting the MCAS Miramar to civilian use should be considered. When the cost of housing is so ridiculous, it makes sense to develop 23,116 acres in the middle of town into a booming, multi-use development that features housing for all. We could be the national example on how to handle the future needs of the people.

The lawsuits against realtors will get addressed towards the end of 2023 and potentially dismantle buyer-agents. It would be awesome if a new auction-based brokerage would hit the scene about the same time!

Other positives about 2023 include it not being an election year, and we’ll be further beyond the pandemic. There should be more commercial and industrial-zoned properties converting to residential uses. The ADUs and aging-in-place will be priorities for many. Every month/year that goes by will push people closer to making their next move – if you know it’s coming, then let’s give it a go in 2023!

I think everyone who buys or sells a home in 2023 will consider it a major accomplishment!

Trustindex verifies that the original source of the review is Google.

A+ thank you

Lisa Tuomi

June 11, 2025

Trustindex verifies that the original source of the review is Google.

Many years ago, we purchased a home in Carlsbad, using a realtor that was recommended to us - Jim Klinge. Fast forward to 2025, we recently had the privilege of selling 2 homes in Carlsbad, CA and didn't hesitate to reach out to Jim and Donna Klinge of Klinge Realty Group to guide us through the sales. The transactions were very different, each with its own unique situation, opportunities and challenges. From start to finish, Donna and Jim helped navigate the pre-sale preparation, the listing, showing of the house, buyer negotiations, the final close and all of the paperwork and decisions in between. What stands out with both transactions is the professionalism of Jim and Donna (and their team), wonderful communication (timely, relevant, concise), their deep understanding of market dynamics (setting realistic expectations), their access to top-notch contractors, and last, their ability to guide us across the finish line successfully. We wouldn't hesitate to use Jim and Donna in the future and highly recommend them for anyone looking to buy or sell a property in North San Diego County.

Jerry Meyer

March 28, 2025

Trustindex verifies that the original source of the review is Google.

We sold a home with Jim and Donna and from beginning to end they were consummate professionals. Their initial walk through the property resulted in a list of items to be repaired or updated. They supplied a list of vendors and job quotes to do the repairs and updates. We originally wanted to sell ‘as is’ and just get it over with. They gave us a selling price for ‘as is’ and options for doing a few updates/repairs to doing it all with the selling price for each option. We agreed to do all they suggested and we sold for the exact price they predicted. For every dollar spent we got back more than $2 back in the selling price. And they got that price in a rising interest rate environment! Donna and Jim are extremely detailed and guide you through ever aspect of the sale. There were no surprises thanks to their guidance. We couldn’t be more pleased with their representation.

Thank you Donna and Jim,

Jerry and Mary

Heather Quejada

March 27, 2025

Trustindex verifies that the original source of the review is Google.

We have known Jim & Donna Klinge for over a dozen years, having met them in Carlsbad where our children went to the same school. As long time North County residents, it was a no- brainer for us to have the Klinges be our eyes and ears for San Diego real estate in general and North County in particular. As my military career caused our family to move all over the country and overseas to Asia, Europe and the Pacific, we trusted Jim and Donna to help keep our house in Carlsbad rented with reliable and respectful tenants for over 10 years.

Naturally, when the time came to sell our beloved Carlsbad home to pursue a rural lifestyle in retirement out of California, we could think of no better team to represent us than Jim and Donna. They immediately went to work to update our house built in 2004 to current-day standards and trends — in 2 short months they transformed it into a literal modern-day masterpiece. We trusted their judgement implicitly and followed 100% of their recommended changes. When our house finally came on the market, there was a blizzard of serious interest, we had multiple offers by the third day and it sold in just 5 days after a frenzied bidding war for 20% above our asking price! The investment we made in upgrades recommended by Jim and Donna yielded a 4-fold return, in the process setting a new high water mark for a house sold in our community.

In our view, there are no better real estate professionals in all of San Diego than Jim and Donna Klinge. Buying or selling, you must run and beg Jim and Donna Klinge to represent you! Our family will never forget Jim, Donna, and their whole team at Compass — we are forever grateful to them.

Lou F

March 27, 2025

Trustindex verifies that the original source of the review is Google.

WeI had the pleasure of working with Klinge Realty Group to sell our home in Carmel Valley, and I cannot recommend them highly enough!

Jim and Donna demonstrated exceptional professionalism, offering expert guidance on market conditions and pricing strategy, which resulted in a quick and successful sale.

Communication was prompt and we were well-informed throughout the entire process.

For anyone looking for a dedicated and knowledgeable real estate team, look no further!

---

William Sams

March 25, 2025

Trustindex verifies that the original source of the review is Google.

Donna and Jim Klinge of Klinge Realty Group have our highest possible recommendation. From Donna and Jim’s first visit to our house through closing their advice and counsel was candid and honest in all dealings. They kept us fully informed throughout the process. The house sold less than three days after listing with a two-week closing. My wife and I have sold several houses during our lives. This was by far the best experience. Klinge Reality is a premium service realtor. You can’t make a better choice for someone to sell your home fast and for top dollar.

Emily Hernandez

December 29, 2024

Trustindex verifies that the original source of the review is Google.

Donna and Jim provided exceptional support and professionalism throughout the entire process. We couldn't have been happier with their efforts. They made our house shine, and thanks to their expertise, it sold above the listing price in the very first weekend! Truly a fantastic experience from start to finish.

Jesus Adrian Sahagun

November 11, 2024

Trustindex verifies that the original source of the review is Google.

This year has been difficult on our family, mainly due to having to sell our home. Thankfully we knew God had a plan for us and working with the Klinge team was a key part of it. It was an obvious decision to work with them again after such an amazing experience when purchasing the same home we needed to sell. The challenge was, how will we do this in so little time with so much going on? Jim and Donna held our hand every step of the way. Whenever an unexpected issue arose they found and provided a solution. Never once did we feel pressured to make a decision and the Klinges were always reassuring after providing the information that the decision was ours to make. Despite the curve balls, they never panicked and exemplified the “can do” attitude, making us feel optimistic and taken care of. Their expertise and professionalism was superb. But of all the reasons to work with the Klinges, the most impactful and valuable is their compassion and genuine care for their clients. We pray that we can one day purchase our forever home and you better believe that Jim and Donna will be representing us - as long as they will have us of course. Thank you again Klinge team! Your execution, experience, and care are unmatched.

SABIHA PASHA

July 23, 2024

Trustindex verifies that the original source of the review is Google.

Jim and Donna were fantastic! Jim understanding my needs, recommending potential places, pointing out the pros and cons of each property was invaluable. Then when the offer was accepted Donna’s organized guidance through the inspections, paperwork etc made the whole process seem effortless.

So grateful that I had them on my side!

Anu Koberg

July 13, 2024

Trustindex verifies that the original source of the review is Google.

We first found Jim through his blog at bubbleinfo.com, which really showcased his knowledge of SoCal real estate. Since then we've done three transactions with Jim and Donna, and they are an incredible full service agency, with Jim's deep market insight and Donna's deft contract and project management. We trust them implicitly in their analysis and strategy, which is based on years of experience. They're always available and on top of things, and we strongly recommend them to anyone.