About 50 years ago, a quartet of L.A. session musicians became so synonymous with the era-defining soft-rock scene — headlined by James Taylor, Carole King, Jackson Browne, Linda Ronstadt, Crosby, Stills & Nash and Fleetwood Mac among others — that they were dubbed the Mellow Mafia.

Danny Kortchmar (guitar), Russ Kunkel (drums), Leland Sklar (bass) and Waddy Wachtel (guitar) made their way to Los Angeles through various sliding doors. By the early ’70s, they frequented the same studios, worked with the same engineers and played the same sessions. Championed by the English producer Peter Asher, the four became in-demand separately and in different configurations for their technical capabilities, inventiveness and gift for bringing live sound to the studio.

In 1971, Kortchmar and Kunkel appeared on King’s bestselling, Grammy-winning “Tapestry” and were joined by Sklar on Taylor’s “Mud Slide Slim and the Blue Horizon.” Two years later, Wachtel played on Stevie Nicks and Lindsey Buckingham’s debut, “Buckingham Nicks,” and Wachtel and Kunkel helped shape Nicks’ 1981 solo debut, “Bella Donna.” All four have joined Ronstadt, Browne and Taylor on tour. And that’s just the tip of the iceberg: Individually and together, they’ve appeared on about 5,000 albums.

A new documentary about the group, “The Immediate Family,” will premiere Tuesday at Laemmle NoHo and debut in theaters and on streaming platforms Friday. Directed by Denny Tedesco (who made “The Wrecking Crew!,” about an earlier generation of renowned session musicians), the film chronicles the foursome’s decades-long work with musical icons through original interviews and archival footage. It’s named after the group’s current band with fifth member Steve Postell, which is set to release a new album, “Skin in the Game,” in February.

“We’ve been around such amazing people for so long that we’re sort of used to the attention, observing it and being a part of it,” Sklar explains of the film. “But seeing the movie is sort of a strange reality. We realize, ‘Oh my God, this is actually just about us. Wild.’ ”

Rob Dawg noted that the year-over-year comparisons are worth a look, now that the super-frenzy days are over. Sure enough, this month looks a lot like last December!

La Jolla is going strong, Rancho Santa Fe is back to the priced-to-sit program they made famous, and the 3 mid-range areas (in purple) have total actives/pendings of 80/45 compared to 99/44 last year.

All signs are pointing to next year being similar….unless there is a surge of inventory.

I wonder how many realtors can say they have been producing 1-2 real estate YouTube videos per week since 2006? Mine don’t go viral because I try to keep them educational in nature.

It reminds me of the time when two Hollywood big-shots called me to discuss a TV show. They wanted to send writers down to fabricate some entertaining story lines. But when I told them I was only interested in keeping it educational, they said they would get back to me.

I’m still waiting for their call!

Thanks for watching – I appreciate you being here!

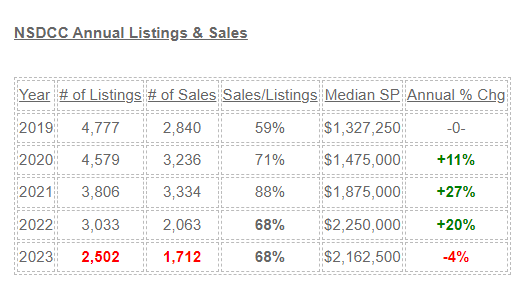

Obviously, this year isn’t over but it’s close – and we’ll be lucky to hit 1,800 sales this year (there have been 22 sales closed in December so far).

The identical Sales/Listings percentage over the last two years includes a blazing hot first half of 2022 so the demand has been steady-hot, but there just isn’t the inventory like we used to have.

Pricing?

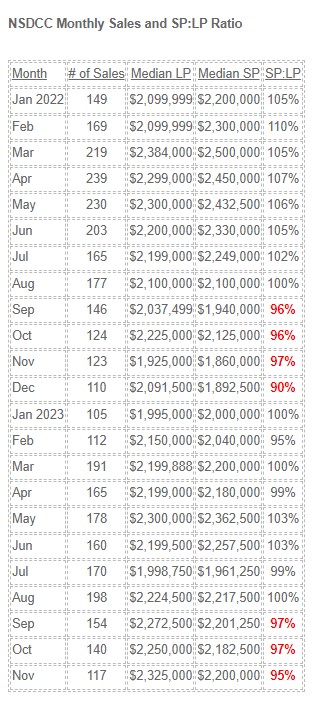

The median LIST price in 2022 and 2023 was the same $2,199,000 each year. In 2022, people preferred to pay over list, and this year…..not so much!

No evidence yet of a possible surge in inventory next year:

A former federal regulator who served when the 2006 housing bubble burst is concerned that today’s housing market is on an unsustainable path.

The housing market’s affordability is worse than it’s been in decades as mortgage rates toy with 8%. The median price of a U.S. home was $322,500 in the second quarter of 2019. Then the pandemic housing rush hit, and prices across the nation shot up. High mortgage rates sent sales spiraling, but home prices only experienced a minor correction before heading back up. In the second quarter of this year, the median price was $416,100, according to the Federal Reserve Bank of St. Louis.

“Talk about a bubble. That’s a classic supply-demand imbalance,” Sheila Bair recently told CNN.

Bair, who served as a federal regulator when the mid-2000s housing bubble popped, nearly taking down the entire financial system, said home prices today are “bubbly” following years of low mortgage rates.

A housing bubble can form when prices rise to unsustainable levels. This can be caused by speculative buying, as was the case during the sub-prime mortgage crisis when people who could not make the monthly payments on their mortgages were buying homes with very little money down. The bubble popped when home prices dropped and many people owed more on their home than it was worth.

A bubble can also be caused by irrational exuberance, in which a surge in prices leads to a buying frenzy.

“When rates were cheaper, a lot of people wanted to buy. You ended up with really frothy price increases. That was pretty predictable,” said Bair, who led the Federal Deposit Insurance Corp. from July 2006 until July 2011.

Although Bair said home prices need to correct downward, she’s not confident that will happen anytime soon because there’s still a shortage of homes on the market and she doesn’t expect the bubble to violently burst.

“If supply remains constrained, this could go on for some time,” said Bair,who last week released a new children’s book about bubbles called “Daisy Bubble: A Price Crash on Galapagos.”

There were just 1.1 million existing unsold homes on the market as of the end of August, down 14.1% from the year before, according to the NAR. “Letting that bubble deflate a bit would probably be a good thing,” said Bair. “People who already own their home – and I’m one of them – don’t want to hear that. But for those who want to own, I hope home prices do come down.”

Over the past year, the median home price has increased by 23.8% in Los Angeles, 18.2% in San Diego, 15% in Richmond and 14.6% in Cincinnati, according to Realtor.com.

The good news is Bair does not see a repeat of the bursting of the mid-2000s housing bubble, which set the stage for the Great Recession. That’s in part because a typical homeowner today has more equity in their homes than a homeowner during that time. Only 1.1 million homes, or 2% of all mortgaged properties, owed more on their mortgage than their home was worth in September, according to CoreLogic. That is a small number compared with the share of properties underwater during the sub-prime mortgage crisis, which topped out at 26% in the fourth quarter of 2009, according to CoreLogic’s equity analysis, which began in the third quarter of 2009.

In addition, mortgage lending standards are significantly tougher today, meaning fewer people are borrowing more than they can afford.

“I see much less speculation in the housing market today, thank goodness,” said Bair.

And unlike in the mid-2000s, homeowners today have built up a significant cushion of equity. That means they shouldn’t find themselves in a situation like during the subprime meltdown where many owed more than their homes were worth.

“Even if home prices adjust a bit, people should not be under water,” said Bair.

Legendary investor Jeremy Grantham shares Bair’s concern about a housing bubble. He has been warning of an eventual plunge in home prices around the world.

“Real estate is a global bubble,” Grantham said on The Compound and Friends podcast last month. “Home prices will come down…30% would be a pretty good guess.”

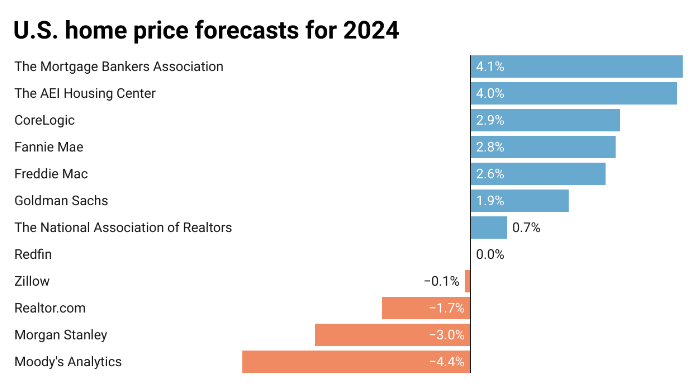

Yet others on Wall Street are confident home prices will continue rising.

Despite high mortgage rates, Goldman Sachs expects US home prices will increase by 1.8% this year and then accelerate to 3.5% growth in 2024. Similarly, CoreLogic forecasts that home prices will increase by 4.3% from June 2023 to June 2024.

Although UBS acknowledges home prices have spiked to “dizzying heights” in recent years, the bank only sees two cities around the world at risk of being in a bubble: Zurich and Tokyo. That’s down from nine cities a year ago. Miami, Los Angeles, Toronto and Vancouver are among the cities that UBS says are in “overvalued” territory.

Fannie Mae CEO Priscilla Almodovar said it’s “unusual” that home prices have not taken more of a hit from high mortgage rates. “What has surprised us the most is the stickiness of home prices,” Almodovar told CNN in a recent interview. “Supply is the issue. There is no place to go. There is a lack of inventory.”

That’s the main reason Lawrence Yun, chief economist at the National Association of Realtors, says homebuyers shouldn’t hold their breath waiting for a drop in home prices.

“There is not going to be a home price crash,” Yun told CNN. “When you have a housing shortage, home prices simply cannot decline in any measurable way.”

While a temporary dip in prices is possible, Yun said a “prolonged” drop of 10% to 15% “cannot happen in this tight supply market.”

Yun noted that many assumed London was in the midst of a housing bubble years ago – only to see prices continue to rise, albeit with fewer people participating.

“It became only a playground for the wealthy. I hope America doesn’t go in that direction,” he said.

In many ways, today’s housing market is the polar opposite of the one that preceded the Great Recession.

Back then, reckless mortgage lending helped create a situation where demand became artificially strong. Eventually, it collapsed and the market was left with way too many homes.

“Today, we have an imbalance the other way. Too much demand, not enough supply,” said Yun.

The NAR has estimated the supply of homes needs to basically double to moderate home prices.

“It’s creating social inequity. The only way out of this situation is we have to induce more supply,” said Yun.

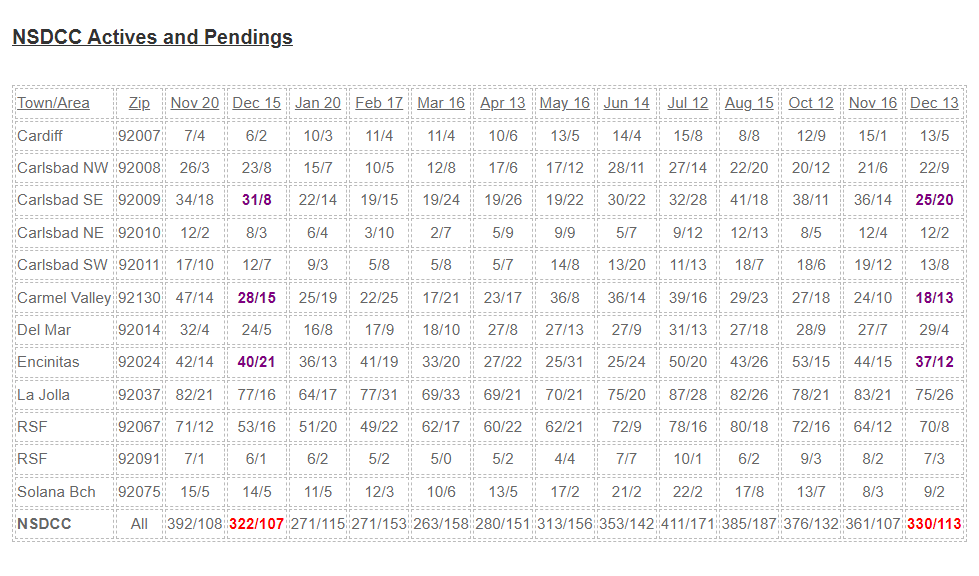

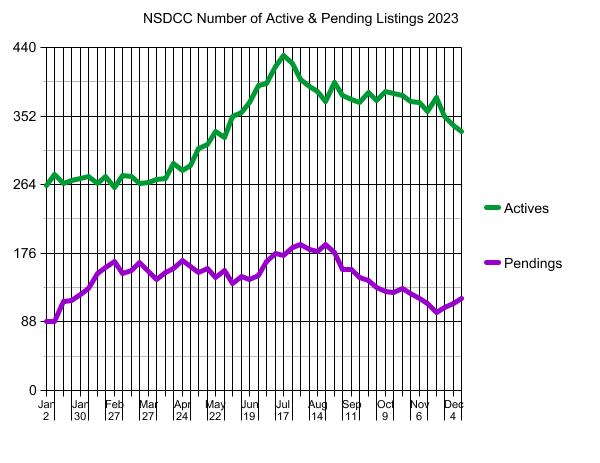

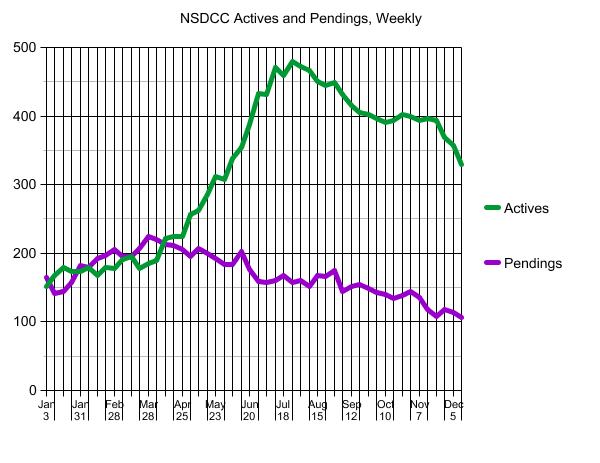

Today we wrap up the 50-week look at the number of NSDCC active and pending listings for 2023 (above). Last year’s market was the only one that was somewhat comparable to this year, so here’s how 2022 looked for the same 50 weeks:

Second week of December, 2022: 329 actives. 107 pendings

Second week of December, 2023: 332 actives, 118 pendings

Those who are betting that 2024 inventory will look a lot like the last two years probably won’t be disappointed!

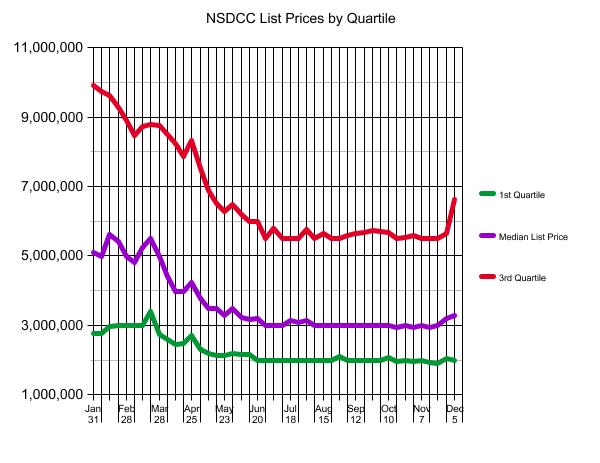

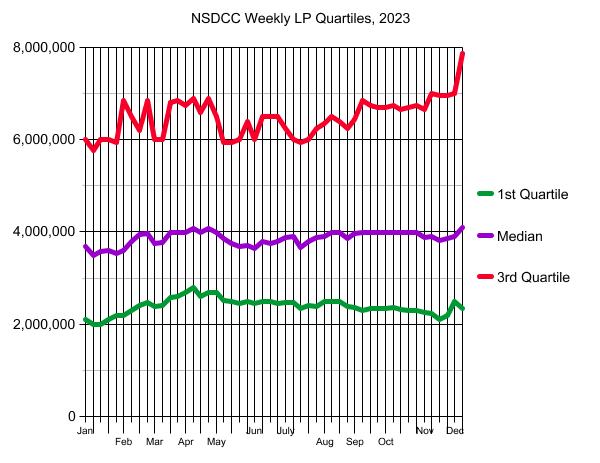

Here is how the last two years looked for their pricing quartiles:

2022

2023

Whoa….a much-different look! Once the higher mortgage rates took the fluff out of the list prices last summer, the market has been fairly steady. How about the sales prices?

First Quarter, 2022: 537 sales, median sales price $2,350,000

First Quarter, 2023: 408 sales, median sales price $2,100,000

Third Quarter, 2023: 522 sales, median sales price $2,150,000

Jay Powell can say he crashed the market – and this is how it looks today between La Jolla and Carlsbad.

Mortgage rates have come down 1% in the last few weeks, and the casual observers are hoping it means that the Big Turnaround will commence in the Spring of 2024.

But for a full-fledged frenzy to break out, home prices would have to drop too.

We’ll never learn much from the median sales prices by themselves. But the SP:LP ratios demonstrate the off-season trend of buyers driving harder bargains, which is the solution for lower prices too.

We’re probably not going to see the whole market drop in price (i.e., big dips in the median sales prices) because the superior properties should hold their value better with the impatient buyers.

But those who don’t need the perfect house will likely have better luck next year with getting a deal. We only flirted with an over-list frenzy briefly this year, and in 2024 we not see many, if any, 100% months.

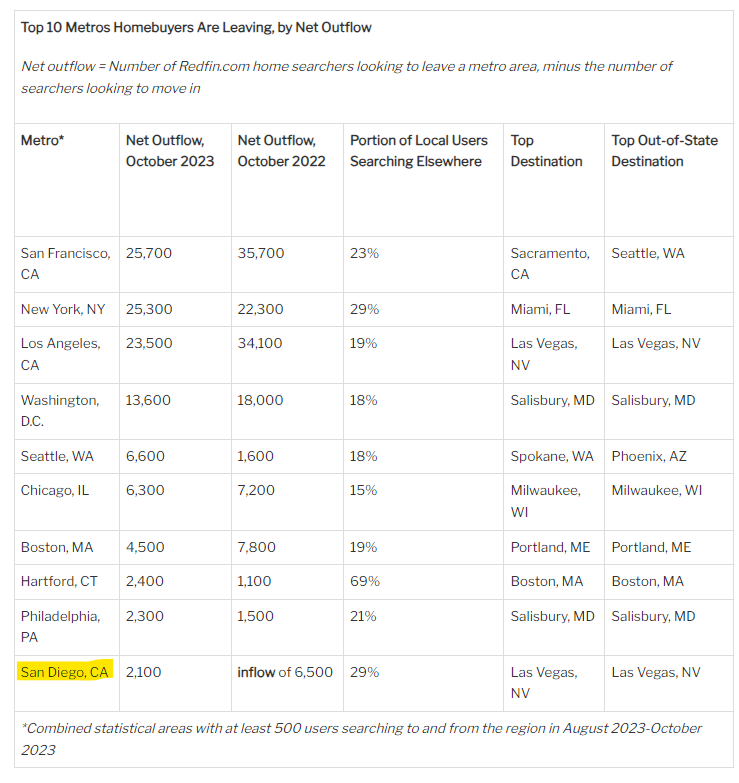

It looks like 29% of you, or almost one out of three, are looking to move elsewhere? Or are you just confirming that there’s nothing better than San Diego?

San Diegans are looking elsewhere to live, according to a Redfin report that placed America’s Finest City as the No. 10 metropolitan area where homebuyers are leaving.

The real estate company analyzed about two million of its users who viewed for-sale home online across more than 100 metro areas from August to October.

Las Vegas was the top destination and top out-of-state destination in San Diego home searches. In October, the median sales price in San Diego was $914,000, compared to $412,000 in Las Vegas.

Sacramento is also on the minds of locals as San Diego ranked No. 3 on the number of homebuyers searching to move into California’s capital city, the study shows. The median price of a house in Sacramento was $500,000 in October, per Redfin.