Like most real estate talk, half of this is horsepucky:

Don’t Let FOMO Drive You

Just because everyone is buying a house, doesn’t mean you should be too, said Donald Olhausen Jr., owner of We Buy Houses in San Diego. “I have seen many people force bad decisions because they have fear of missing out (FOMO). Forcing a bad deal will not rectify itself because there were no other options or because you felt stuck. Being patient in this market is hard, but overpaying for a faulty property will ultimately lead to more regret.”

There Are Markets Within Markets

There is not one universal housing market, but rather “many smaller micro-markets,” said Michael Shapot, Esq., licensed associate real estate broker. “Some of those submarkets are ‘hot, less hot or more hot’ and they may change week by week, or month by month.”

Elisa Uribe, a realtor with Wells and Bennett Realtors added that “real estate is hyper-local,” so consider the source. “You can withstand any market changes if you don’t have to move in a specific time frame.”

2022 Is a Slightly Better Time To Buy

Real estate experts like Marina Vaamonde, the founder of PropertyCashin, said that 2022 would be a better time to buy because, “The demand for residential real estate is still vastly overshadowing the inventory.”

Indeed, now that 2022 has arrived, experts still agree that is the case, even with decreasing inventory. According to Time, home prices will not increase as rapidly and home values will also likely increase at a less vigorous rate than the peak of 2021, which bodes well for buyers.

However, the Fed Just Raised Interest Rates

What made 2021 unique was extremely low interest rates, according to David Friedman, CEO of investment property platform Knox Financial. “There have been very few times in history when we’ve seen 30-year fixed mortgage rates hovering around 3.3% and 15-year mortgage rates slightly above 2.6%,” he said.

However, on March 16, 2022, The Federal Reserve raised rates for the first time in years by 0.25%. What this likely means, according to NerdWallet, is that mortgage rates will follow suit by increasing, meaning homebuyers will pay more in interest.

No One Can Predict the Next Drop

Despite these slight increases in interest rates, and decreases in inventory, this doesn’t necessarily mean the market is going down.

Khari Washington, a broker and owner of 1st United Realty & Mortgage, added, “No one knows if the housing market will drop and when it will drop. Most reports talk about the market slowing in 2023 but not falling. Builders have not built enough housing and interest rates remain low.”

“The right time to buy is when a person is ready,” adds Washington.

Don’t Wait for a Better Price

Waiting can be a gamble, said Jeff Shipwash, CEO of Shipwash Properties LLC. “You could be waiting to purchase with the thought of prices coming down, but…even if home prices do pull back some, if rates increase it will all be for nothing. You may be able to afford a $300,000 house at current rates. But if those rates increase by 1% while you wait, that same payment may be on a $250,000 house.”

Rents Are Sky High

If not buying means renting, consider that “the current rental market is on fire with rents skyrocketing and landlord incentives eliminated,” said Shapot. Renting will not be a cheaper option in the long run.

This Market Is Stable

Unlike the unstable market leading up to the economic crash of 2008, this market is stable, said Jennifer Shannon, a broker associate with Keller Williams Realty. “This market run-up hasn’t been driven by investors, flippers and bad mortgages. It’s been driven by legitimate buyers who are more free to determine where they live than ever.” While demand will start to slow eventually, she says there are no indicators of prices going down anytime soon.

You’re Ready When You’re Ready

“You’re ready to buy a home when you’re ready, not when there’s a frenzy,” said Tabitha Mazzara, director of operations at mortgage lender MBANC. “The frenzy is a seller’s market, so missing out on a frenzy is a good thing for buyers.”

Chase Michels, owner of Compass, The Michels Group, added, “If a client is fully committed to buying and is in the appropriate financial position to do so, then they should be looking. You may buy at a little lower or higher price at different times of year but that is typically unpredictable in a smaller market.”

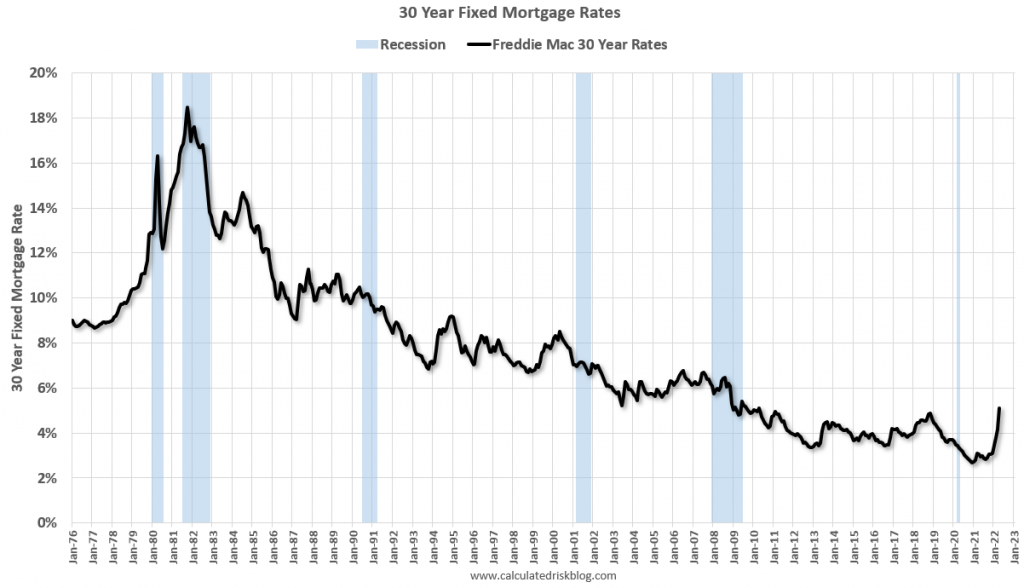

I suggested that mortgage rates should settle into the 4.75% to 5.50% range, and Bill at CR thinks the range will be 5.0% to 5.7%. Today’s rates are in the low 5s, so we have arrived and buyers should not feel the need to hurry up – but it will be bumpy over the next few months. Those with a short runway can opt for 2.375% for ten years.

Currently most forecasts are for the Fed Funds rate to rise to around 3.25%. Goldman Sach’s chief economist Jan Hatzius recently said he thinks the Fed may have to raise rates above 4%, although their baseline forecast is just about 3%.

When the Fed Funds rate peaks in this cycle, the yield curve will likely be fairly flat – meaning the 10-year treasury yield will be at about the same level as the Fed Funds rate. Based on the current estimate for the peak Fed Funds rate (3.25% to 4.0%), the 30-year fixed mortgage will likely peak at between 5.0% and 5.7%. There is some variability in the relationship, so we might see rates as high as the low 6% range. (This all depends on inflation and the Fed Funds rate – but I don’t expect rates to move much higher than the current rate – although 6% is possible).

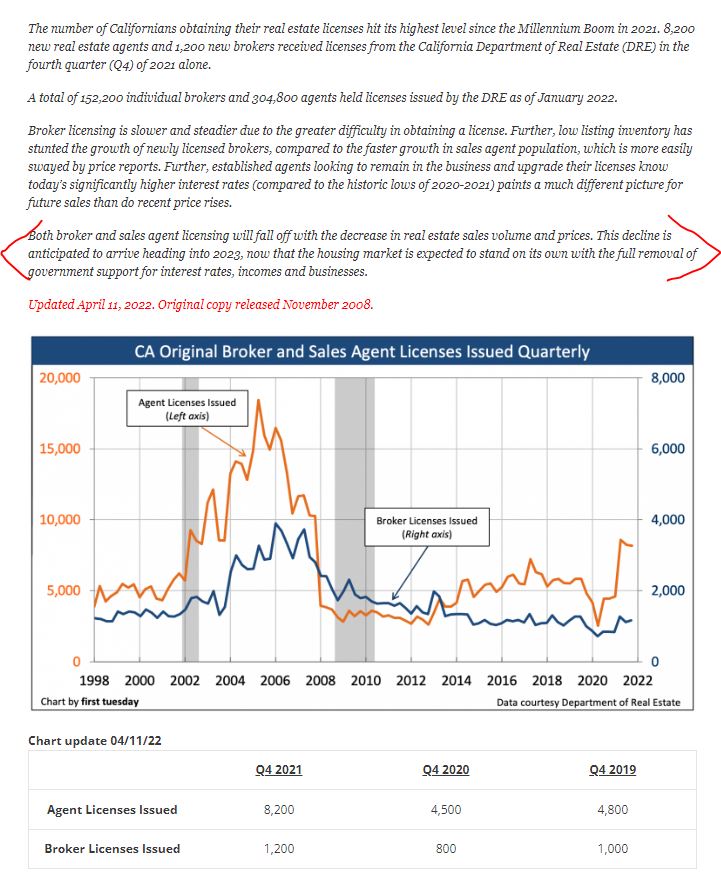

More people continue to get their real estate license.

It looks like there have been around 8,000 new licensees in each of the last 2-3 quarters! There are somewhere between 15,000 and 20,000 dues-paying realtors already in San Diego County, and last month there were 3,198 residential sales on the MLS…..for the whole county!

I think that their doomy author has been misreading the market for years, but if you are thinking about becoming a realtor, believe their nonsense and don’t bother – there is not enough business to go around.

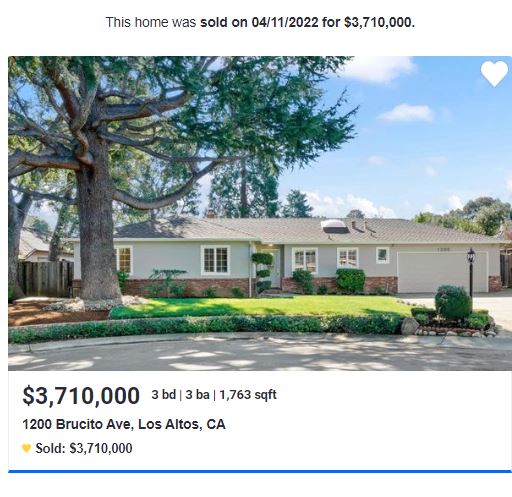

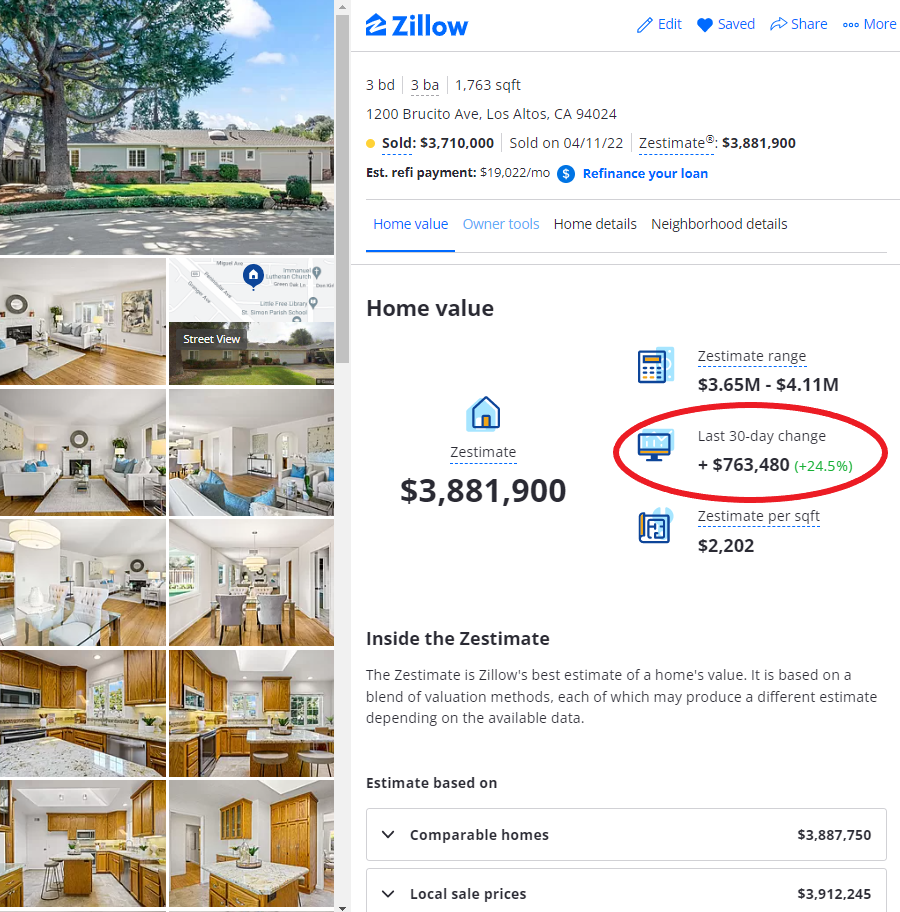

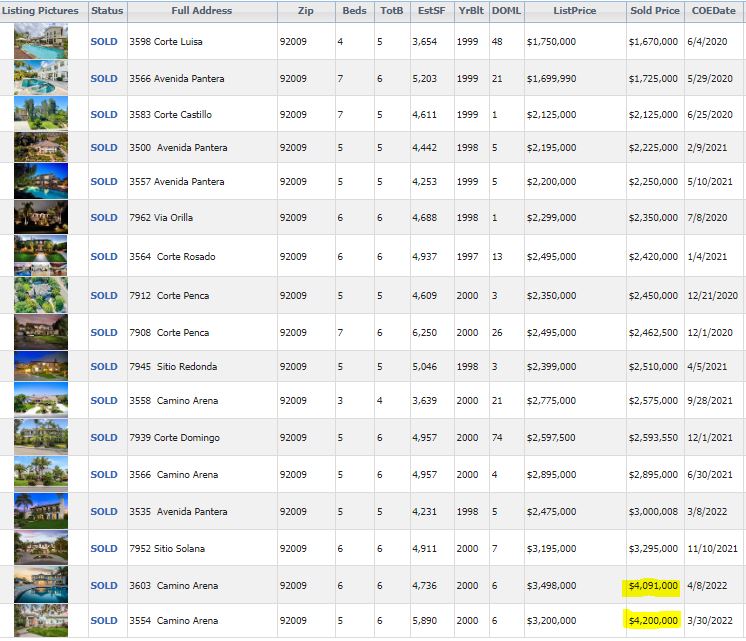

The bump over the list price is so customary in the local area that the zestimate was raised by $763,480 about the time it was marked pending – the algorithms already had the expected increase baked in!

They are enjoying The 2022 Lucky Windfall of the First Quarter, and we’ll see how well it holds up. But as long as home sales in the Bay Area keep selling for much-higher pricing than in San Diego, one of our main feeder areas will keep sending happy buyers our way!

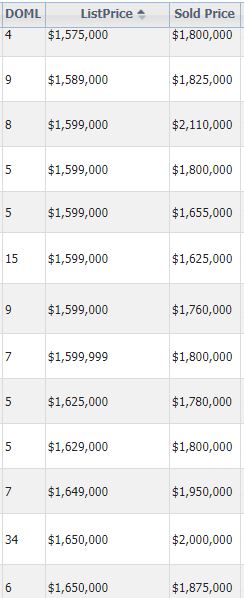

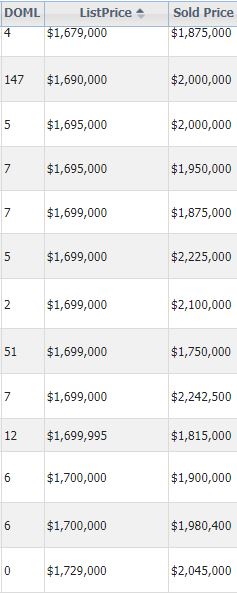

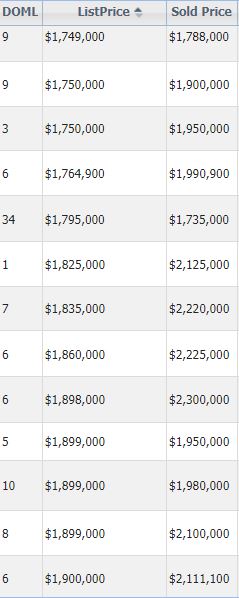

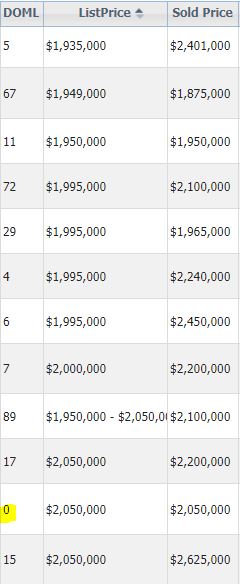

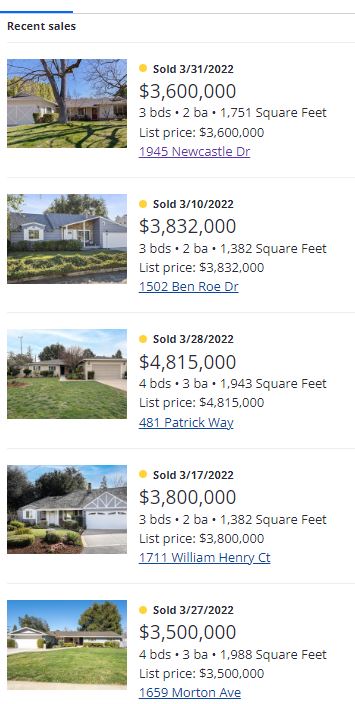

The list prices mentioned here all say that they sold for 100% of the LP, but it’s a typo – they all sold for well over. For example, Patrick Way sold for $1.1 million over, and William Henry sold for $800,000 over list:

Paying ~$2,000/sf for modest homes in Los Altos has been fairly routine lately!

Hopefully, those sellers keep coming our way. Even if their market were to dip 10% to 20% from these dizzy heights, they will still love what they can buy here for the money.

In the last 24 months, there were two sales of $1,670,000 and $1,725,000 in the Ranch of Carlsbad. In the last 12 months, there have been three sales in the $2,500,000s.

I think we can say that the statistics are starting to reflect the current environment, which is being muddled by a few factors:

There are so few listings that sellers (and listing agents) are pushing the list prices….but buyers have had enough, and the inferior properties aren’t selling like they used to.

Sellers and agents are skipping the spruce up/staging extras, and buyers are being picky.

The wait-and-see strategy is addictive, and once buyers adopt it, it’s hard to get off the fence.

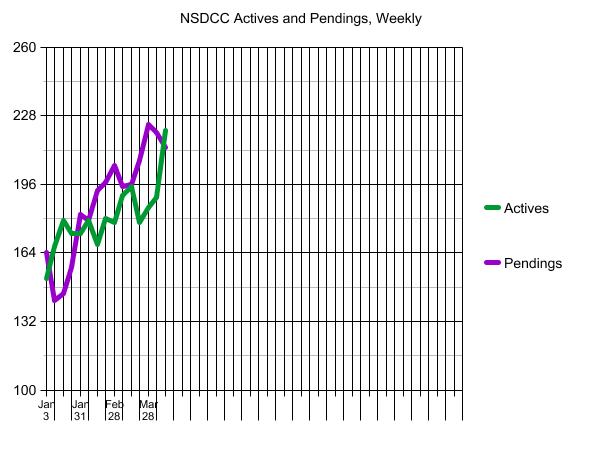

This is the first time during the selling season that there are more actives than pendings (221 vs 213). If it ever gets back to the normal 2:1 ratio, it’s going to feel like the sky is falling!

It is rare that a seller decides to sell and then lists their home for sale the same day. Usually, it’s a plan that has been in the works for months, and any last-minute adjustments – especially on price – are also rare. Don’t be surprised if the pricing over the next two months reflects the pricing of the last two months.

A fantastic spin on higher mortgage rates by two economists – an excerpt:

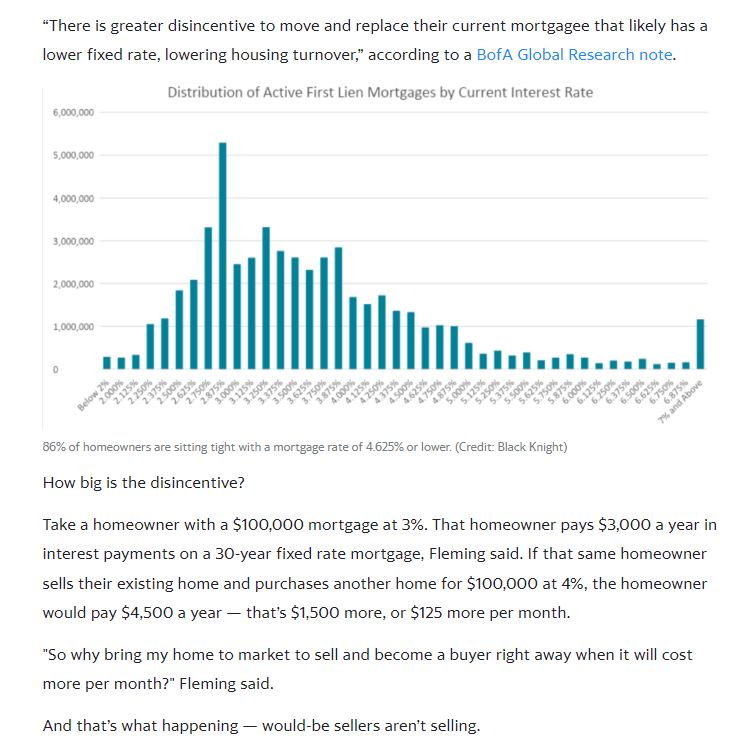

Mark Fleming – That’s a great question, Odeta. And when we subtract the core CPI inflation rate from the 30-year, fixed mortgage rate, we find that, with air quotes here, mortgage rates are actually negative.

Odeta Kushi – Say what now? Here we’re talking about rates as high as 5%. And now you’re telling me rates are negative?

Mark Fleming – Yep, over the last half century, there have only been two other times when core inflation was higher than the 30-year, fixed mortgage rate. Both of those were in the 1970s.

Today, we’re experiencing the extremely rare phenomenon of real, negative mortgage rates. So, while we may expect rising mortgage rates to cool the market, real estate still looks cheap, given the high inflation, not to mention the appreciation benefits that people get from the stellar asset returns that we’ve experienced recently.

Okay, thinking like a finance guy for a hot minute here. If the price of everything is rising faster than the price of borrowing at a fixed rate, aka the negative real rate of mortgages, to own an asset that’s appreciating in value. Hmmm.

Odeta Kushi – Yeah, so a significant slowdown in purchase demand due to rising mortgage rates is not necessarily a foregone conclusion, not to mention that house prices, and even sales to a lesser extent, have shown to be pretty resilient in the face of rising mortgage rates. You can refer to our podcast episode 15, if you want to know more about this.

But the SparkNotes version is in four of the last six rising mortgage rate eras, the existing-home sales increased or only declined after prolonged resistance. Home prices show even more resiliency.

Apart from the 1994 rising-rate period when house prices declined slightly and briefly, house prices have always continued to rise, albeit more slowly, when rates have increased. That’s because home sellers would rather withdraw from the market, rather than sell at lower prices, a phenomenon we refer to as ‘downside sticky.’

Of course, relative rates matter and mortgage rates have been in the 2-to-3% range during most of the pandemic. So, rising to about 4% may have a larger impact than in the earlier periods. So, it’s unclear how much rising rates will cool the purchase market. But, how would rising rates cool the housing market anyway? By reducing affordability, of course, and causing buyers to pull back from the market. In other words, by cooling demand.

JtR: Let’s note that the highly-financed buyers don’t get much of a vote because in the bidding wars over quality properties, they are sent to the back of the line. The ‘cooling demand’ from financed buyers pulling back only means fewer offers. The market’s direction will be determined by the cash buyers, and/or the big-down-payment buyers who will shrug off higher payments when they hear a catchy buzz word like ‘negative mortgage rates’. The location/condition of the home will matter more to the sales price than rates.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~