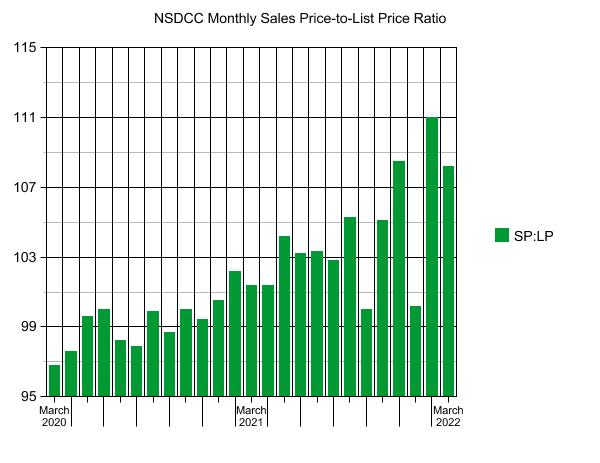

Let’s take a look at the covid history of one of our frenzy measuring sticks:

NSDCC Sales-Price-to-List-Price Ratio:

Month

# of Sales

Median List Price

Median Sales Price

SP:LP Ratio

March 2020

206

$1,492,500

$1,445,000

96.8%

Apr

156

$1,424,499

$1,390,000

97.6%

May

143

$1,399,900

$1,395,000

99.6%

Jun

274

$1,362,500

$1,363,700

100%

Jul

351

$1,450,000

$1,423,350

98.2%

Aug

350

$1,450,000

$1,419,812

97.9%

Sep

360

$1,500,000

$1,498,750

99.9%

Oct

382

$1,696,500

$1,674,100

98.7%

Nov

305

$1,599,000

$1,599,900

100%

Dec

290

$1,633,500

$1,624,391

99.4%

Jan

187

$1,716,690

$1,725,000

100.5%

Feb

224

$1,719,500

$1,758,000

102.2%

March 2021

252

$1,800,000

$1,825,000

101.4%

Apr

359

$1,799,900

$1,825,829

101.4%

May

300

$1,900,000

$1,979,500

104.2%

Jun

357

$1,900,000

$1,960,000

103.2%

Jul

312

$1,792,500

$1,852,500

103.3%

Aug

268

$1,897,000

$1,950,000

102.8%

Sep

283

$1,899,000

$2,000,000

105.3%

Oct

251

$1,899,000

$1,899,000

100%

Nov

200

$1,998,500

$2,100,000

105.1%

Dec

183

$1,995,000

$2,165,000

108.5%

Jan

140

$2,234,944

$2,240,000

100.2%

Feb

158

$2,149,500

$2,386,500

111.0%

March 2022

206

$2,425,000

$2,625,000

108.2%

The chatter increases with the lower volume, plus there are going to be months when the offerings just aren’t that tasty. But in 2022, when buyers see a home they like, they over bid substantially!

All we have to do is watch the trend over the next few months to know the direction of the market.

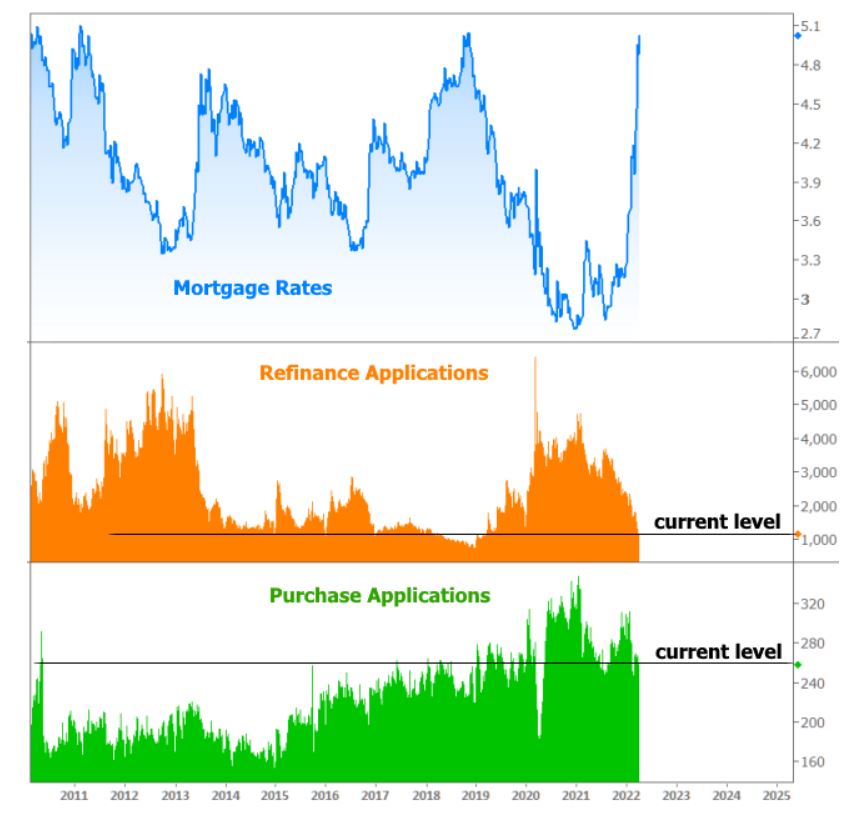

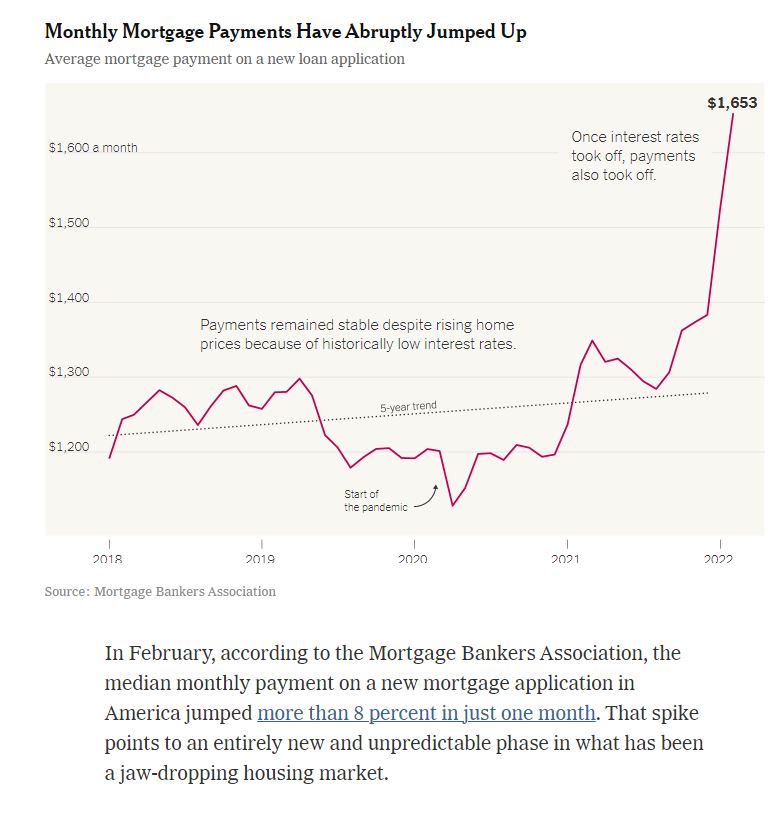

You can’t spend too much time reading/watching the news recently without being well aware of the relatively unprecedented surge in mortgage rates seen so far in 2022. In particular, the month of March was one the worst on record with one individual week in March tying a week in June 2013 as the worst in more than 25 years. All that to say, rates are much higher!

The higher borrowing costs have had the same impact they always have when it comes to refinance applications. In this week’s Mortgage Application Survey from the Mortgage Bankers Association (MBA), refis dropped another 10 percent, and are now 62 percent lower than the same week last year.

The purchase market remains a different story.

While purchase applications also declined last week, they are only 9 percent below the same week last year and still higher than most of the past decade before the Covid. Keep in mind that the survey only tracks applications, so by the time all-cash demand is factored into the purchase market, housing demand has yet to show any major panic over the rising rate environment.

Now that we are grappling with 5% mortgage rates, people are wondering how it will affect the market.

The common perception is that there will be pullback.

What that means isn’t defined – it’s just a vague concept that the logical mind wants to believe. But logic flew out the window long ago, so I’m not sure how useful it is today. Prices went up 30% in 2021 and it didn’t stop, or even slow the market in the first quarter of 2022.

Does it matter what the opinion is today?

Not really, and you can refer to the chart above to see how much opinions matter.

All that matters is that we track the trends over the next few months to see what actually happens!

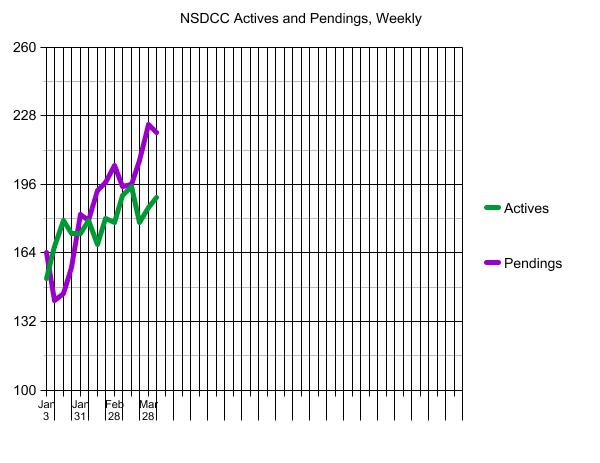

Yesterday I said all we have to do is monitor the days-on-market, and the actives vs pendings to get advance notice on how the market is behaving. Let’s add a third metric, the SP:LP ratio.

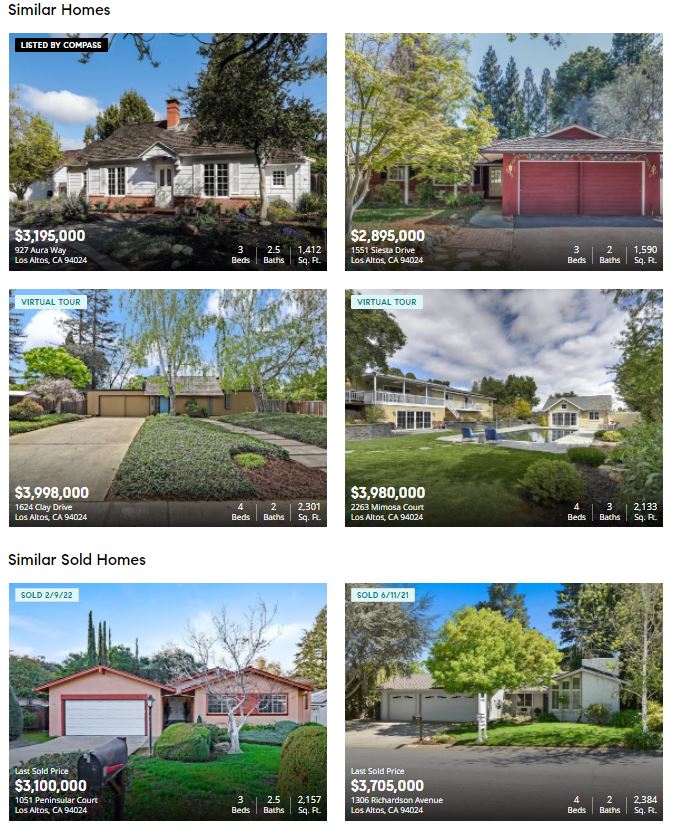

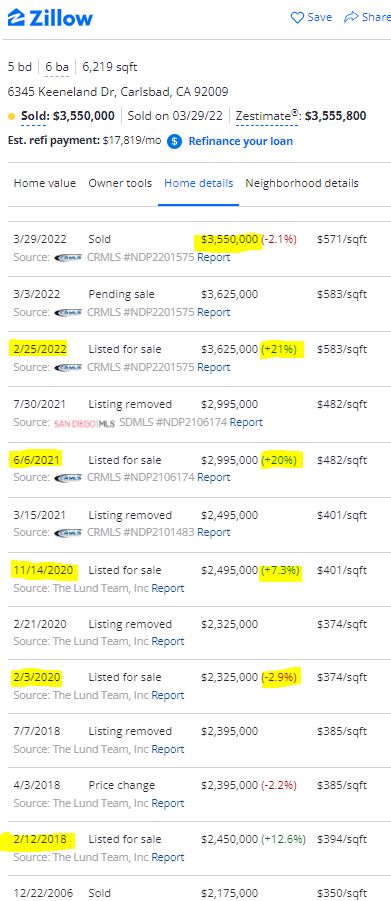

Who are the home buyers that will determine our fate? When out-of-towners from more affluent areas come here to see our prices, they think we are giving them away. There have been estimates that as many as 70% of the coastal sales here have been bought by people from the Bay Area.

We should keep an eye on their market!

I’m watching one sale in progress there. My uncle has been a lifelong resident, and my mom, brother and sister all live there so I have opportunity to check in on their real estate market from time to time.

In December, we went to pay our respects to Sally, my uncle’s long-time girlfriend. They met later in life and had separate houses, and unfortunately Sally passed away from cancer just before Christmas.

We had a brief conversation with her sisters who were from outside California, and they expected that they would sell her home in early 2022. The zestimate was in the mid-$2,000,000s, and they said they would be happy with a price in that range.

After painting and staging the relatively modest 1,763sf house built in 1953, they listed it for $3,195,000. It went pending within ten days – and since then the zestimate has zoomed to $3,800,000!

The house is five doors away from the Foothill Expressway, which isn’t a freeway but there is some road noise. The 9,975sf lot size is attractive, and the house is one-story. But low-to-mid $3,000,000s?

Even more interesting was the house at 1051 Peninsular Ct. When we were there, I saw the sign and drove by to confirm that it was literally right next to the Foothill Expressway. It closed for $3,100,000!

The pricing in the Bay Area is subject to change, just like it is here – but it should be somewhat relative, and we will likely ride the same elevator. The 1Q22 pricing spiked in Los Altos, and the sisters – who only expected a sales price in the mid-$2,000,000s – will pick up a lucky windfall.

The 2022 Lucky Windfall of the First Quarter doesn’t have to continue throughout the year for our market to thrive. If pricing “crashes” downward 10% to 20% from today’s lofty heights, it means we’re only back to November pricing, which you would think wouldn’t bother sellers much.

But it will.

Do not underestimate the home seller’s ego.

It doesn’t mean you should, or shouldn’t, go buy a house today. If you are a home buyer in the hunt, just be picky (or pickier) about what you will tolerate. The list prices will feel like TodayComps+5%, the sellers are doing less to condition them for sale, and the listing agents act like you owe them money.

There is one guarantee. The inventory later in the year will be worse than it is today. It could feel like pricing is loosening up (it’s not yet), especially in the 4th quarter of 2022, but it won’t matter if there aren’t any homes for sale that you would buy. Be in the hunt for the right house!

I will keep track of the winners and losers. Help me if you can!

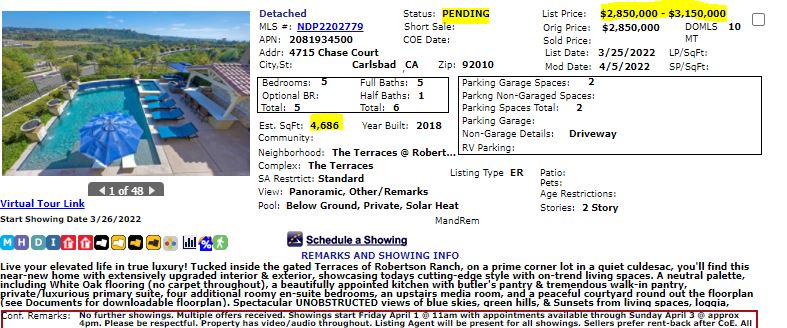

Here is today’s winner, who had 11 showings and three offers. Tanya raised the list price to a range, which makes it look like it probably went over $3,000,000:

It may seem crazy to you, but those coming from Los Altos will think it looks like a steal!

We joke about how sellers are reluctant about lowering their price, but it has been a solid strategy over the last 10-12 years. Here is a prime example (see above).

P.S. They had no showings last year, and decided the timing wasn’t right. Boy, howdy!

From yesterday’s article, which also ran in the SDUT today:

“There are so many strange things going on right now,” said Edward Seiler, the associate vice president for housing economics at the Mortgage Bankers Association.

It has been 40 years since rates have risen like this alongside similar home price growth and high inflation. This time around, the United States also has a severe housing shortage. And then there’s a new and uncertain dynamic — the sudden rise of working from home, which has the potential to change what home buyers want and where they live.

“Nobody really knows what’s going to happen over the next year,” Mr. Seiler said. That makes it hard to predict when rates might start to act as a brake on rising prices.

Nobody?

I have to take a swing at that one!

There are many variables that could slow the increases in home prices, and higher rates are just the latest excuse. Prognosticators said that last year’s velocity was the reason the home prices would cool in 2022 – no one could imagine that they could go up as fast as they did in 2021 – yet NSDCC the median sales price has INCREASED 21% BETWEEN DECEMBER AND MARCH!

But will rising rates be the final blow, and home prices start to decelerate?

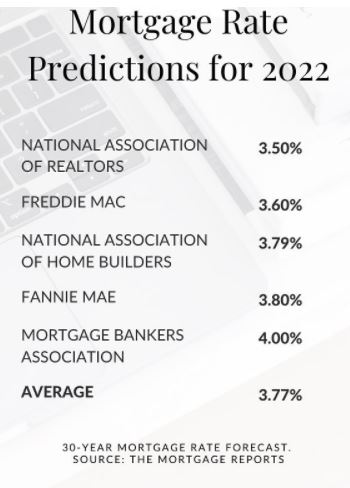

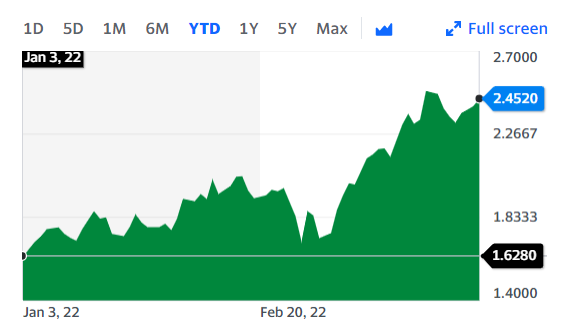

Let’s try to predict the path of mortgage rates in 2022. How much worse could it get?

Mortgage rates are loosely tied to the 10-year T-bill, which has risen 0.824% this year:

The Fed is expected to raise their benchmark rate 1.5% this year (6 x 0.25%), so the 10-year yield has another 0.676% to go to reflect the anticipated 1.5% increase in 2022.

Mortgage rates have mirrored the 10-year, plus 1.75%, for decades.

Today’s 30-year fixed mortgage rate is 4.84% so let’s add the additional 0.676% = 5.516%. Because mortgage lenders are like gas stations – quick to overshoot rates on the way up, and sluggish on the way down – we will probably see 6% mortgages this summer as lenders continue to get out in front.

Let’s note that today’s 10-yr yield is 2.452% plus 1.75% = 4.202% which means today’s mortgage rate is about 0.6% overshot too high.

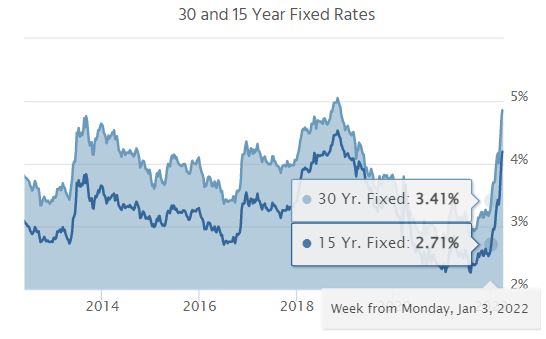

To further demonstrate the current mortgage-rate overshoot, here was the rate on January 3rd:

The 10-year has gone up 0.824% YTD, and mortgage rates have risen 1.43% YTD.

We are due for pullback, but the mortgage lenders will more likely just let it ride, knowing that more Fed increases are coming. They will panic (again) and mortgage rates will probably be touching 6% in a couple of months, but we should settle into a range of 4.75% to 5.5% by the end of the year – which isn’t much different than it is today. It coincides with the January’s 3.41% plus 1.5% = 4.91%.

Will higher rates than today affect home prices? It depends on the sellers – they get a vote.

If relatively nobody wants to sell at these prices, they sure won’t want to sell at lower prices! Rather than lowering the price, they will blame their realtor for their home not selling, and try again next year.

They’re not going to give it away!

There isn’t going to be a surge on inventory, because it would have happened by now. But I’m sure there are buyers running to the sidelines in droves, wanting to believe it’s going to be different, later. There will be fewer offers on homes for sale, and some may not get any! All we have to do is monitor the two metrics, the days-on-market, and the actives vs pendings, to know the trend.

But there are additional variables that will keep prices in this range:

The affluent buyers who aren’t as affected by rates. As long as we don’t run out of them, home prices will stay right where they are, or keep trending upward.

All buyers, affluent or otherwise, will buy the dips. There will be an occasional home priced under the comps (usually the dated estate sales) and buyers will jump to pay less. But they will get bid up to within 5% of retail and create the floor.

Buyers who are affected by higher rates can get a 2.375% ARM, fixed for ten years.

Realtors will keep pumping the seller’s market because it’s all they know.

We are pulling into Plateau City.

Even if the buyer psychology crashes, and only the desperate buyers stay in the game for the next few months, we can easily predict what will happen in the second half of 2022. Because both sellers and buyers who didn’t transact in the first half of 2022 will pack it in for the rest of the year, sales will plummet in the last half of 2022. It’s what happens in the early stage of a market shift, because sellers can’t believe they missed the peak and would rather wait, then lower. It will takes several failures before sellers re-consider their price accuracy – and some never will.

The NSDCC median sales price in December was $2,165,000. In March, it was $2,625,000.

I expect that the December, 2022 median sales price will be within 5% of $2,625,000 (plus or minus).

Then in 2023, the market will be flooded with lookers, who will be hoping for lower prices than what they remember from summer. But sellers will be packing a little extra on their price, just in case.

What do you think?

Before commenting, spend 15 seconds to watch this response to a ~$3 million off-market listing:

It is natural to have more closings during the last week of the month, and the dip in the pendings count wasn’t as bad this month as it was last month. This is where you will see the first signs of any concern on behalf of buyers about interest rates, etc.

Everyone was talking about them at open house over the weekend. But we’re still going to sell my listing for well over the list price today!