Fully autonomous vehicles (AVs) should become commonplace within 10–20 years, disrupting entire industries while triggering structural shifts in housing and the economy.

The path to government approval and consumer acceptance of AVs will have hiccups no doubt, so we expect ride-sharing along with semi-autonomous vehicles to kick-start the movement towards AVs.

For consumers, the tipping point for large-scale adoption will come when not owning a car makes more financial and logistical sense than traditional ownership. Car enthusiasts, the affluent, and rural households will continue to own cars as AVs evolve.

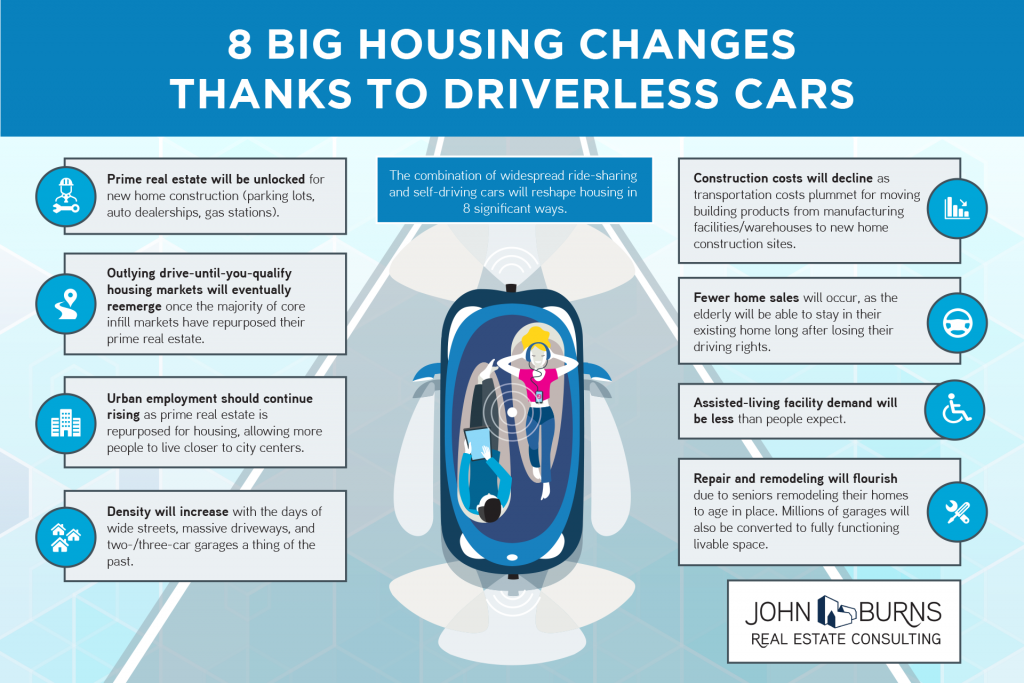

The combination of widespread ride-sharing and self-driving cars will reshape housing in 8 significant ways:

Prime real estatewill be unlocked for new home construction (parking lots, auto dealerships, gas stations).

Outlying drive-until-you-qualify housing marketswill eventually reemerge once the majority of core infill markets have repurposed their prime real estate.

Urban employmentshould continue rising as prime real estate is repurposed for housing, allowing more people to live closer to city centers.

Densitywill increase, with the days of wide streets, massive driveways, and two-/three-car garages a thing of the past.

Construction costswill decline as transportation costs plummet for moving building products from manufacturing facilities/warehouses to new home construction sites.

Fewer home sales will occur, as the elderly will be able to stay in their existing home long after losing their driving rights.

Assisted-living facility demandwill be less than most people expect.

Repair and remodelingwill flourish due to seniors remodeling their homes to age in place. Millions of garages will also be converted to fully functioning livable space.

Most of us know we own too much stuff. We feel the weight and burden of our clutter. We tire of cleaning and managing and organizing. Our toy rooms are messy, our drawers don’t close, and our closets are filled from top to bottom. The evidence of clutter is all around us.

Today, increasing data is being collected about our homes, our shopping habits, and our spending. The research is confirming our observation: we own too much stuff. And it is robbing us of life.

Here are 21 surprising statistics about our clutter that help us understand how big of a problem our accumulation has actually become.

1. There are 300,000 items in the average American home (LA Times).

2. The average size of the American home has nearly tripled in size over the past 50 years (NPR).

3. And still, 1 out of every 10 Americans rent offsite storage—the fastest growing segment of the commercial real estate industry over the past four decades.

4. While 25% of people with two-car garages don’t have room to park cars inside them and 32% only have room for one vehicle.

5. The United States has upward of 50,000 storage facilities, more than five times the number of Starbucks. Currently, there is 7.3 square feet of self storage space for every man, woman and child in the nation. Thus, it is physically possible that every American could stand—all at the same time—under the total canopy of self storage roofing.

6. British research found that the average 10-year-old owns 238 toys but plays with just 12 daily (The Telegraph).

7. We have 3.1% of the world’s children living in America, but they own 40% of the toys consumed globally (UCLA).

8. The average American woman owns 30 outfits—one for every day of the month. In 1930, that figure was nine (Forbes).

This expert says the next recession will cause home prices to come down hard, but we learned last time that people have to live somewhere, and the government will save us.

Stack’s prescience makes his latest warning particularly ominous. He has dusted off the same Housing Bellwether Barometer that raised red flags more than a decade ago and is watching it to see when — not if — the nation’s booming housing market will turn down.

That barometer, Stack explained, is an index of “the most sensitive stocks in the housing industry” — including homebuilders and mortgage companies. It recovered nicely after the 2008-2009 crash and has been flat for the past few years. But over the past 12 months, Stack said in an interview, it “started to go up like a rocket ship again, similar to what it did back in 2004-2005.

That tracks the anecdotal evidence he’s seen of frantic bidding wars in some of the nation’s hottest markets. “It’s that kind of nuttiness that defines the psychology of a bubble,” he said.

Some key statistics also point to a new housing bubble:

The Case-Shiller national index hit all-time highs last December and continues to rise.

Case-Shiller indexes show prices in Boston, San Francisco, and Charlotte, N.C. about 10% above their previous peaks; Portland and Seattle, around 20% higher, and Denver and Dallas, 40% higher. These are the new boom towns, replacing Las Vegas, Phoenix, and Miami the last time around.

The SPDR S&P Homebuilders ETF has quintupled (up 400%) from its March 2009 lows, vastly outperforming the broad S&P 500 , which has gained around 270%.

Stack says the best way to measure housing’s true value is to compare it with long-term inflation, and that measure is also raising a warning flag.

“Median family home prices are 32% above the long-term inflationary trend — in other words it has to fall 32% to get down to where it was,” Stack explained. “That’s not as bad as the 35% in 2005, but it does kind of wake you up and say, this isn’t normal, this is going to end badly.” To me, there isn’t much difference between being 32% and 35% overvalued.

Stack acknowledges there are big differences between 2005 and now. “You’re not seeing the esoteric mortgages, the so-called liars’ loans…,people buying multiple homes, thinking that they can rent it and make money on it,” he said.

Back then there was rampant mortgage fraud, huge demand from Wall Street for subprime mortgage securities and rating agencies giving them black checks, with no regulatory oversight whatsoever. Also, says Stack, there was an inventory glut then and a shortage now that is causing prices to soar.

On the other hand, “you are seeing lending institutions loan 95% or more of the value of the home,” he said. “That is a problem, because when home prices come down, it makes it very easy for the home buyer to walk away from that mortgage.”

One key similarity: “We still have a lot of easy money out there for mortgages,” he said. “We have a Federal Reserve policy today that’s unfortunately like the early 2000s,…, and it’s conducive to bubbles.” The federal funds rate now is very close to the 1% low where Greenspan pushed it, and that triggered the final, disastrous stages of the last bubble.

The big danger, of course, is the next recession, which Stack views as inevitable. “At some point we’re going to have another economic downturn, another economic recession,” he said. “When we see that downturn…you’re going to see [housing] prices come down quite hard over a period of 12- to 24 months.” He added that he doesn’t foresee a recession until at least 2018.

Stack’s record isn’t perfect — in early 2016 he called a bear market that never happened — but it’s been excellent over the long run, and going back to the 1987 stock market crash, he’s had a knack for spotting bubbles.

The realtor industry has given a huge head start to Zillow and the others, so it would take a herculean effort to build a new/better portal to squash them.

Here is what Greg has said about the features to expect on his realtor portal:

* A “secret sauce” differentiator that attracts homebuyers away from Zillow and other websites.

* Only listing agents will appear next to their listings.

*No online valuations – you can’t value a home without seeing it.

* No FSBOs – only listed homes by licensed agents.

* No days-on-market disclosure – it hurts value perception.

* No price reduction disclosure – it hurts value perception.

* Managed by an elected committee of agents/brokers.

* Optimized to maximize lead flow for listing agents.

* Designed as the perfect website to sell homes faster.

To build a better portal than Zillow would require more transparency, not less. He wants to hide the days-on-market and price histories? Buyers would be slow to give up that information, and instead, click back over to Zillow.

I doubt his secret sauce will make up for the lack of transparency, and if the new portal doesn’t have active and sold comps readily available, he might as well pack it up right now.

They are supposed to send out an email today regarding the pre-launch:

Tomorrow we begin the pre-launch phase of our crowdfunding campaign. This will provide the seed money we need to build an industry unification website designed to sell our listings instead of using our listings to take advantage of us. It will be the first ever nationally marketed home search portal owned and managed by America’s real estate agents, a refreshing alternative to websites like Zillow that don’t care about our industry or our clients (beyond how they can profit from us).

This crowdfunding prelaunch is only being shared with a select few. It is being provided to you because you have volunteered to help as part of our leadership team. The main launch to the public will not take place until September 19th.

The guy who started the StopZillow campaign wants to build a new real estate portal which would be controlled by realtors – he discusses the details here:

An excerpt from the leadership team’s email announcing that the pre-launch of the crowdfunding campaign starts today:

We will use contributions from this crowdfunding campaign to build the best home search portal ever in real estate. This will bea website designed to sell our listings rather than using our listings to take advantage of us. Crowdfunding will also be used to create the national TV, print and Internet advertising we will need to market this website.

Once the website is completed (projected January 2018) you as a campaign leader will have the first opportunity to demo it. You will also be given an insiders preview of the national TV commercials and blitz marketing campaign we develop to attract buyers to the website. After you have approved the website and marketing, it will then be made available to crowdfunding contributors, followed by other agents throughout the country.

Then we will launch a $50,000,000 Regulation A+ securities offering to enable every licensed agent and broker the opportunity to become an owner. This $50,000,000 shouldn’t be difficult to raise… it’s an average of less than $50 per Realtor. I plan to buy at least $100,000 in stock myself. That money will be used for a national blitz marketing campaign to make every buyer aware of our website.

Once we have our buyers back, we will be able to retain our sellers and ensure our future. Recapturing control of our buyers and regaining control of our industry is the #1 goal of this project. Sellers need buyers. If we have the buyers, sellers will need us.

It seems far-fetched that he could get enough realtors on-board and get them to cough up money to build a new portal. But realtors need to do something to save our jobs, and having our own portal would solve everything.

This stretch of Carlsbad oceanfront is high enough off the water and has substantial riprap to keep the storms away – yet has easy access to the beach!

This Friday night at Kaaboo, Michael McDonald will take the Trestles stage around 7:00 pm. While, at first take, it wouldn’t seem like he might fit in with today’s crowd, Michael is hip once again:

We’re featuring Jeff ‘Skunk’ Baxter on lead guitar two weeks in a row! This on a song from the album Takin It To The Streets – Skunk was the guy who brought Michael into the band:

By late 1974, touring was beginning to take its toll on the band, especially leader Tom Johnston. Things became worse during touring in support of Stampede when he was diagnosed with stomach ulcers. His condition worsened and several shows had to be canceled. With Johnston forced to reduce his involvement with the band, the other members considered just calling it quits but while in Baton Rouge, Louisiana, member Jeff Baxter suggested calling up friend and fellow Steely Dan graduate Michael McDonald who at the time was between gigs and living in a garage apartment. McDonald was reluctant at first, feeling he was not what they wanted, according to him, “…they were looking for someone who could play Hammond B-3 organ and a lot of keyboards, and I was just a songwriter/piano hacker. But more than anything, I think they were looking for a singer to fill Tommy’s shoes.” He agreed to join them and met them at the Le Pavillon Hotel in New Orleans where they moved on to a warehouse to rehearse for the next two days. Expecting to be finished once touring was completed, McDonald was surprised when the band invited him to the studio to work on their next album.

Hat tip to Richard for sending this in…..how much more can buyers take?

A house in Sunnyvale just sold for close to $800,000 over its listing price.

Your eyes do not deceive you: The four-bed, two-bath house — less than 2,000 square feet — listed for $1,688,000 and sold for $2,470,000.

“I think it’s the most anything has ever gone for over asking in Sunnyvale — a record for Sunnyvale,” said Dave Clark, the Keller Williams agent who represented the sellers in the deal. “We anticipated it would go for $2 million, or over $2 million. But we had no idea it would ever go for what it went for.”

This kind of over-bidding is known to happen farther north in cities including Palo Alto, Los Altos and Mountain View. But as those places have grown far too expensive for most buyers, future homeowners have migrated south to Sunnyvale, a once modest community that now finds itself among the Bay Area’s real estate hot spots.

Close to tech employment centers, it makes for a convenient commute — and prices there, too, are now pushing the limits of middle-class buyers. The house that sold for $782,000 over asking in Sunnyvale — it’s on Prunelle Court — is about a mile from Apple’s new spaceship campus.

The buyers, who work in tech, had been hunting for a home for a while — but kept getting out-bid, said Mini Kalkat, the Intero agent who represented them: “They lost two before they bid on this one, so we kind of knew what the numbers would be. It’s a crazy market, but there’s a way to maneuver the market.”

The property is one of more than 50 South Bay homes that sold in the last month for at least $200,000 above the listing price. More than half of those deals were made in Sunnyvale. Others were made in Cupertino, Saratoga and West San Jose, according to Alain Pinel agent Mark Wong. He compiles a monthly list of such “over-asking” transactions.

Over-asking sales are at least partly the result of agents’ sleight of hand. It’s become common strategy to list homes under their market value in order to entice Silicon Valley buyers; they are all too willing to fight over the few houses available in this chronically tight market.

One of my most favorite books of all time is The Great Gatsby. When it turned into a motion picture with another one of my favorites, Leonardo DiCaprio, I became even more in love!

In 2015, the mansion that inspired Gatsby’s home became for sale! I thought…YES! But then I saw the price tag of $100 million and was a little discouraged – I need to sell more houses!

This mansion boasts 18 bedrooms, 2 separate guest homes, indoor pool, a bowling alley, a shooting range, and a casino! Unfortunately at the end of the dock you will not see Daisy Buchanan’s green light, but the New York City skyline instead! Not bad!

Here’s a link with photos to see more! The house is now down to $85 million!