Big Increase in 12 Months

The tax man will love this one. The old property-tax basis was $81,068!

The lot size of the comp across the street was 8,900sf, and this one was 9,600sf:

The tax man will love this one. The old property-tax basis was $81,068!

The lot size of the comp across the street was 8,900sf, and this one was 9,600sf:

Home buyers deserve to have their own representation.

The broker cooperation system which allows every agent to share their inventory with all other buyers via the MLS has worked well for 100+ years. But it has been under attack for years, and it may not survive the tight-inventory era where sellers and listing agents want to minimize or eliminate buyer-agents altogether.

An agent sent this in today:

Do you know that Lennar is no longer paying agents a commission or referral fee?

I have been working with a client for almost a year. She wouldn’t have known about the Lennar at Treviso community without me bringing her there. I registered her as my client and when her name got called on the list, they told her they’re no longer cooperating with agents and if she tried to include me she’d lose the house. Thank you Lennar for putting my client is a horrible position. Hey builders. Don’t ostracize the brokerage community! The market may be busy now but when the tides turn, you’re going to need us again. This is bad business.

I know for a fact that Lennar isn’t paying commissions on any of their SD communities currently.

I agree that it’s bad business to have an agent sign in their buyer as required to receive the commission, but then rescind their offer of compensation when the buyer steps up to purchase. But nobody cares about buyer-agents, and the abuse will continue. Lower or no commission being offered, no clarity on how multiple offers get handled (other than the usual “I just let the sellers decide”, which is a lie), and no easy path to show and sell.

What is the result of buyer-agents being snuffed out?

Here you go:

Buyers don’t recognize the need for getting good help.

An apprentice from a realtor team will suck them in with the promise of getting them an ‘off-market deal’, but then get sold a 1,200sf two-story house in a gang-infested area for 10% to 20% over value (true story).

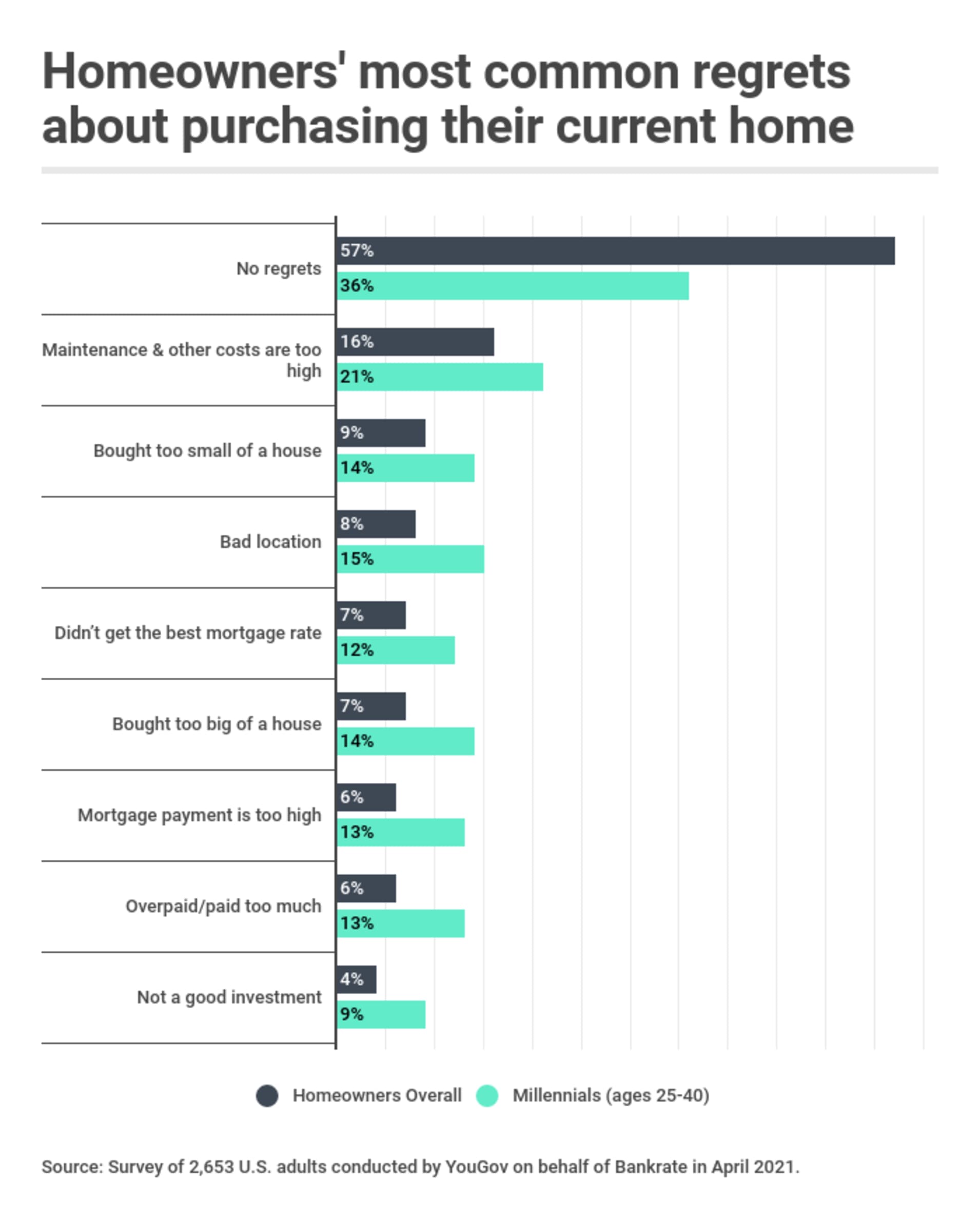

We should probably just drop the seller-paid commissions – though they should have the right to offer a bounty – and have buyers pay their own agents. Those who value good help will seek out the best agents, and those who don’t will get what they get and wind up with regrets.

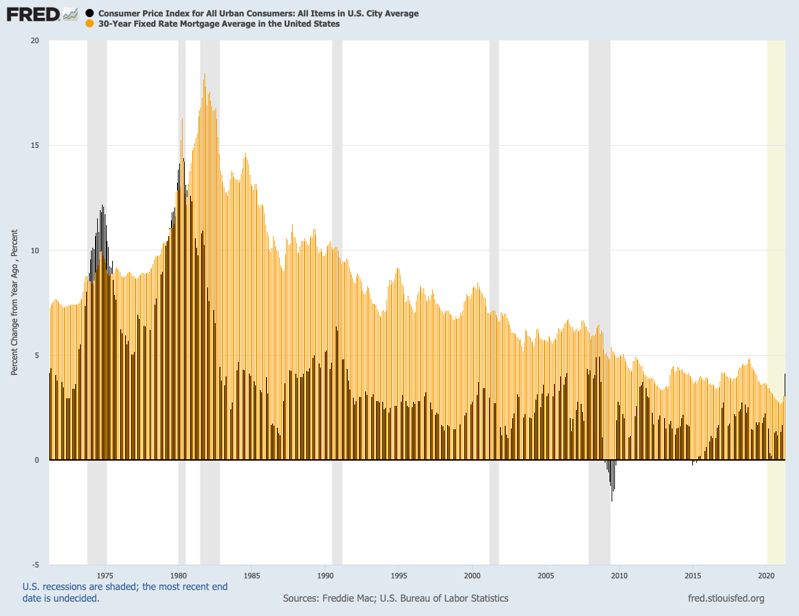

Add this to the list of reasons why demand is so hot…..

For the first time since 1980, the cost of living is rising faster than the average mortgage rate.

The Consumer Price Index for April tells us U.S. inflation is growing at a 4.2% annual pace, the largest jump since the bubble days of 2008. Meanwhile, Freddie Mac’s rate for a 30-year mortgage averaged 3.1% in the same month, a smidgen above record lows.

That puts the cost of home loans at 1.1 percentage points below inflation. Let my trusty spreadsheet tell you how topsy-turvy that really is: Over the past half-century, mortgages were an average 4 percentage points above the inflation rate — though that gap’s been halved in the past decade.

Inflation rates topping mortgage rates have happened in just 34 of the 601 months — that’s 50 years — since this loan index started in 1971. That’s just 6% of the time. The last occurrence was August 1980, when inflation was an ugly 12.9% and mortgage rates were 12.6%.

Link to Article

Here’s a demonstration of adding a bedroom/full bath over the living room with high ceiling.

This is the same house that got me into BloombergBusinessweek!

https://www.bloomberg.com/news/articles/2013-04-08/home-buying-and-selling-tips-from-a-pro

I had said previously that the frenzy will run out of gas in June.

I’m sticking with it.

There aren’t enough new listings coming to market to keep the buyers’ interest. It is the momentum of seeing hot new listings flying off the market every week that keeps the frenzy cooking.

The inferior homes won’t be attracting the crowds – and multiple offers – like they were at peak frenzy (which will probably end up being the August-March time period). We will see an occasional hot new listing that will get frenzied up and sell for 10% to 20% over list, but the regular listings should feel more normal.

I’ll offer one example from this weekend. There was a new listing of a larger one-story house that had three nearby sales that had closed for higher prices in the last 90 days. But as of last night, the agent had not received any offers.

It’s not the end of the world. It’s probably more of a sign that sellers are selecting a list price that includes all of the covid-frenzy premium that buyers are willing to take.

A more-normal, balanced market is good for everyone. Sellers will still be able to sell for these prices, and buyers who decided to wait it out will slowly re-enter the buyer pool, keeping the demand in place. All we need to do is figure out the prices!

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

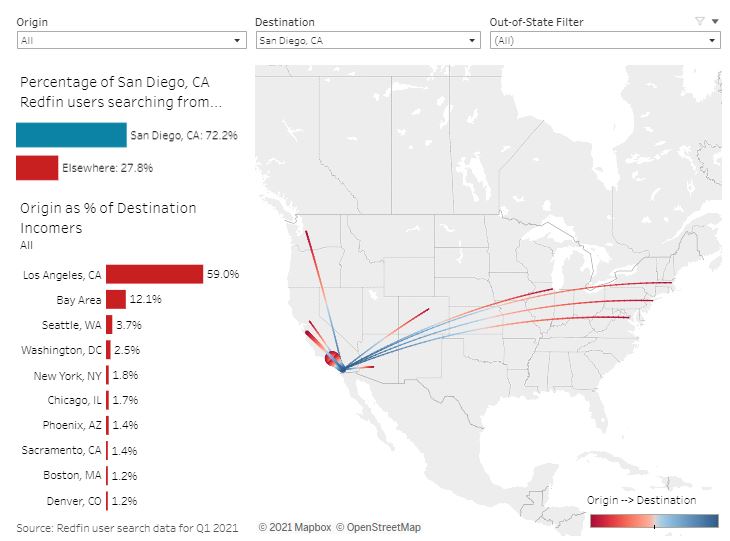

People are curious about where today’s buyers are coming from, and while results may vary for each individual neighborhood, we might be able to get a general sense from data like this.

Not everyone who is looking is an actual home buyer, and not everyone uses this search portal.

But this data backs up the latest idea that people tend to want to stay close to home. Almost three-quarters of those looking at San Diego real estate are local folks, and more than half of the rest are from L.A.

San Diegans are looking at these destinations also – this is interactive is you’d like to explore further:

A gravel road for access and home is on septic, not sewer. Still sold for $86k over list!

In last Saturday’s blog post, I mentioned three reasons why San Diego real estate was undervalued, and pondered that there are new market forces in play that we haven’t seen before.

While people will scoff at the idea that it could be different this time and insist that the market will always revert to the mean, there are new factors to consider that will have impact on the eventual outcome:

LESS SUPPLY

No foreclosures

Ultra-low rates locking in homeowners to their forever home.

Boomers are older than ever, and are aging-in-place (too old to move).

Holding real estate has never been so sexy.

Longest expected length of ownership ever.

MORE DEMAND

Population is more affluent than ever (SD County has 100,000+ millionaires, fifth in USA).

Work From Home has expanded the choices for buyers, increasing the demand in desirable areas.

Hoarding real estate is cool (high rents, kids to inherit).

Current homeowners have more equity than ever to use when buying again.

There are more people than ever in the homebuying ages.

We probably only needed supply OR demand to change by 5% or 10% to make a difference. But it seems like BOTH have changed more than that….in opposite directions, which has really stirred it up.

It used to be that when home prices were hitting new highs, sellers would come out of the woodwork to take advantage. But not this time – which is different!

One caveat to having open houses is actually having homes for sale!

The frenzy conditions have been building for years – see this old blog post from 2017 (above).

We were discussing it all through the second half of last year that the 2021 Frenzy was going to be huge, and the signs were so obvious that even Ray Charles could see them!

But the foundation of people buying their forever home with a low-rate mortgage has been on-going since the last crisis bottomed out in 2009.

San Diego really should enjoy frenzy conditions longer than most areas – maybe longer than any area!

Interestingly, a check of our buyers, and buyers of our listings over the last 18 months shows that about 80% of them were local residents. We’ve had people move here from the Bay Area, Chicago, and NYC, but for the most part it has been move-uppers and move-downers. Results may vary!