Everyone complained that we had no inventory….well, we have more now! But the 286 active listings today is still well under the 349 actives that we had last year at this time, and more listings should cause more sales.

We’ll see if the slight pause in the market can be attributed to the usual graduation-season malaise, or if a full-blown buyers’ strike is underway.

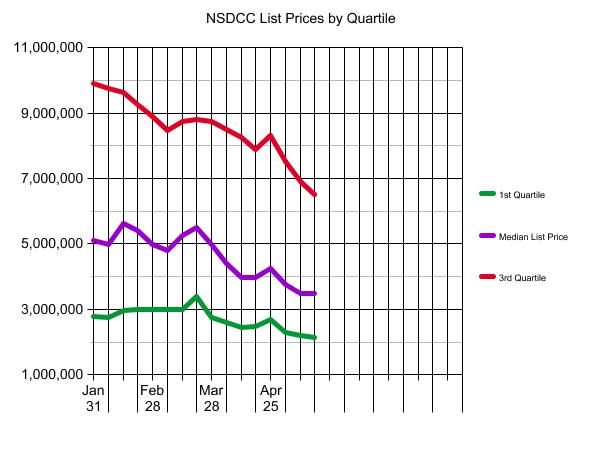

This isn’t the only measuring stick, but it appears that pricing has been settling down:

Most sellers are going to wait it out, or cancel their listing – neither of which will satisfy the buyers who are hoping for a major adjustment.

I only skimmed it and I didn’t see the one thing that could really make a difference, which is re-purposing federally-owned real estate for residential use.

Let’s start with MCAS Miramar, which is 23,116 acres in the middle of San Diego that would be ideal for residential development. It’s big enough that you could have something for everybody!

We had our chance once:

In 1954, the Navy offered NAS Miramar to San Diego for $1 and the city considered using the base to relocate its airport. But it was deemed at the time to be too far away from most residents and the offer was declined.

Let’s leave the airport where it is and redevelop Miramar!

The homes on the market today were priced according to comps from 1-4 months ago, which were the craziest-priced sales in the history of real estate.

To make matters worse, sellers are naturally drawn to the highest-priced sales – and today that means the ones that closed for hundreds of thousands above the list price. But there was probably only one buyer crazy enough to pay that price.

Then rates go up to the mid-5s, which to buyers feel like double what they were.

But the sellers have committed to their list price, and their ego is laid out bare for all to see – friends, family, neighbors – all are watching and waiting to see if another house is going to sell for an insanely high price.

What happens if it doesn’t sell right away?

The sellers have to be motivated enough about moving that they will address the results. Many have been on the market for weeks without selling – and have they even received an offer yet?

They didn’t get this far in life without being smart enough to know that something different is needed. But there are only three choices:

Cut the price.

Wait it out at this price.

Cancel the listing.

That’s it, those are the choices.

Most will add a fourth choice – it’s my agent’s fault! If my agent would only advertise more, and do more open houses, and well, heck, do whatever agents are supposed to do to sell my house for my price, then it would sell! But you can spend a million dollars on advertising, and it still won’t sell if the price isn’t right.

This is why the market won’t adjust for a long time. The gap between those crazy comps from yesteryear and what more rational buyers will pay today has never been so wide. It’s probably not 5% or 10% either.

The craziest buyers have already purchased, and left us with unattainable comps. The only question is whether there are any somewhat-crazy buyers left, or if it’s just the rational buyers.

Tip: Throw out all the sales prices of the comparable homes that have sold nearby, and just use their list prices. Those list prices were probably rooted in reality (hopefully), and then in all the commotion, one of the craziest buyers radically overpaid just to win the house. Their purchase price is unlikely to be achieved again, at least for the foreseeable future, but those list prices should be a good starting point.

The old Encina Power station site is designated for tourist uses, and open space. A seven-story hotel like this will undoubtedly be proposed – will it fly in Carlsbad? Rooms here go for $300-$2,100 per night:

A new Compass listing in South Encinitas, priced at $6,290,000:

Tucked away in seclusion, this 3606 sq. ft. 3-bedroom 3 bath New Construction Modern Hacienda masterpiece with two additional detached units exemplifies a unique combination of an ultra-modern interior and the warmth of a welcoming hacienda exterior. Nestled in the depths of Berryman Canyon, with the inviting Enclave development serving as the veritable drawbridge to the estate, this home exists as a fortress of relaxation. Upon arrival, all guests are unequivocally certain that this estate is the crown jewel of the neighborhood.

A top California lawmaker is proposing to spend $10 billion to help families buy homes in the state with some of America’s highest housing prices.

Democratic State Senate Leader Toni Atkins on Wednesday unveiled details of a proposal she’s pushing to create a revolving fund that would provide interest-free loans for up to 30% of the purchase price of a home for low- and middle-income households.

If implemented, it would be the largest program of its kind in the nation, according to the people who designed it. Proponents hope that it will be included in the state budget that must pass by June 15 and go into effect as soon as January. The aim is for it to eventually help about 8,000 families a year.

The proposal calls for the state government to share in any appreciation in the value of houses it helps purchase when they are sold and then invest those proceeds back into the fund.

“The purpose of this is to create a long-term endowment,” said Gene Slater, chairman of CSG Advisors, which advises public agencies on affordable housing and helped design the program. “We’re investing in the future value of the home so we can help other people.”

Under the proposal, California would spend $1 billion a year for 10 years. Participation would be limited to households making 150% of the median income in an area. There would be limits tied to a region’s median home price allowing home buyers in the most expensive markets such as the San Francisco Bay Area to benefit.

In Los Angeles County, households earning up to $120,000 a year could qualify for assistance, while in low-income areas like the agriculture-heavy Central Valley, that number would be closer to $107,000, according to data provided by the researchers who drafted the framework. Proponents want to target certain groups through outreach, including residents of largely Black and Latino neighborhoods and those with high loads of student debt.

The homeowner would repay the loan when they sell or refinance the home, along with a cut of the profit from any appreciation in value based on how much assistance the state provided. If the home price declines, Mr. Slater said, the state would be repaid if money is left over after the purchaser pays back their mortgage loan and recoups their portion of the down payment.

The program would be limited in scope to cover only about 2% of home sales volume statewide in an effort to avoid pushing prices higher.

Participants would be chosen on a first-come, first-served basis, with slots set aside for certain geographic areas and income brackets.

To become law, the proposal would have to pass both chambers of the Democratic-controlled state legislature and be approved by Democratic Gov. Gavin Newsom. A representative for Mr. Newsom declined to comment on the pending legislation. In a statement, Assembly Speaker Anthony Rendon praised Ms. Atkins’s work on the issue but didn’t say whether he supported her proposal.

Even though real estate is local, the homebuyer psychology tends to be similar across the country – mostly because people are people, and have similar reactions to every variable. When they see mortgage rates go from 3% to 5.5% in less than six months, it’s only natural to want to pause and see where this goes.

But the desperation among buyers – especially those who are out-of-towners and don’t own a home here yet – hasn’t changed, due to the low inventory. It is unsettling to see so few of the quality homes coming to market, and they want/need to stay in the game so they don’t miss out. It would take a flood of new listings to change that, which isn’t happening. At least not yet.

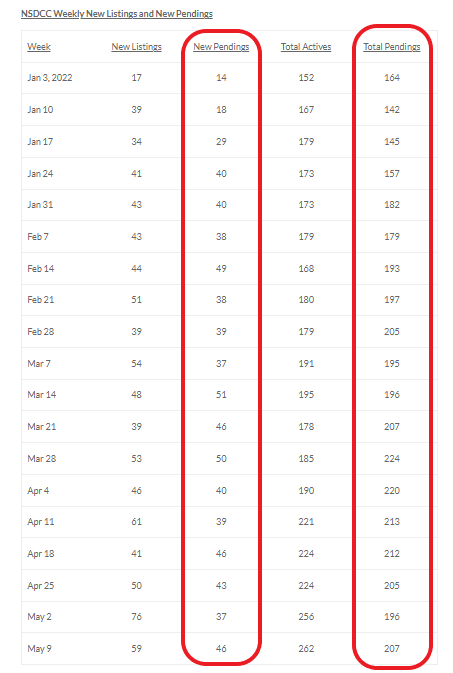

Let’s have the statistics help guide us on current market conditions.

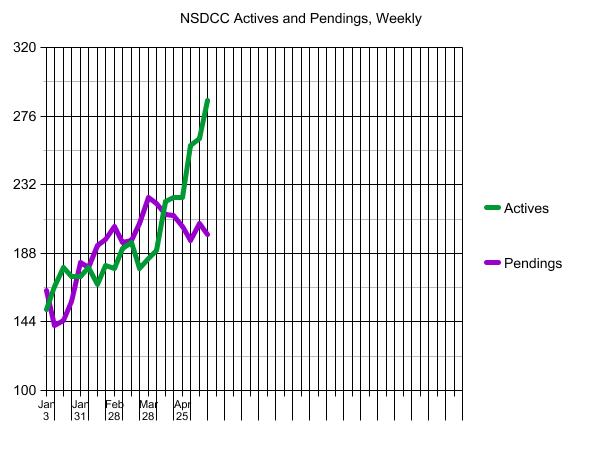

1. We have considered the local real estate market to be ‘healthy’ when the active listings to pendings has been 2:1 ratio. Here are the detached-home listings between Carlsbad and La Jolla:

Monday:

Actives: 262

Pendings: 207

Thursday (today):

Actives: 262

Pendings: 202

The current ratio is very healthy, and the actives aren’t exploding. Last year at this time there were 330 active listings, so only having 262 homes for sale in an area with a population of 300,000+ people isn’t bad. The only startling part is that there aren’t more homes for sale!

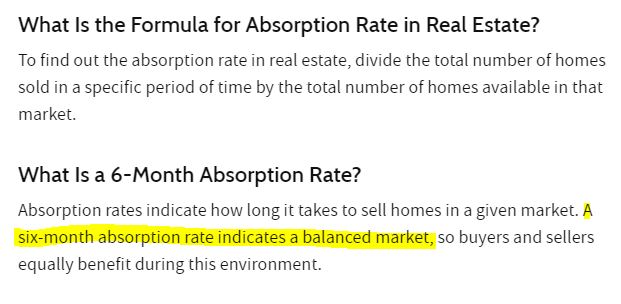

2. Let’s talk absorption rate, another measuring stick for the health of the market. The historic norm for a healthy market has been a 6-months’ supply of homes for sale. In recent years, a 3-month supply has seemed to be more realistic, just because the supply has been limited.

What is it today?

There were 225 sales in April, so the 262 active listings is only a 1.2-month supply. We would need 675 active listings to have a three-month supply, which sounds impossible in the current environment.

3. How about the market time of the current pendings? Is it taking longer to find a buyer these days? Yes. The median days-on-market for homes sold in the early months of 2022 has been nine days. The current pendings have a median days-on market of 12 days, which isn’t alarming and still extremely low.

4. Have the number of actives and pendings been consistent in 2022?

Yes, especially the pendings:

So while there is talk about a shift in the market, it may just be a pause. Statistically, the market looks steady – there isn’t a surge of unsold homes, and there are still plenty going into escrow every week.

If there aren’t as many buyers looking, and there aren’t crazy numbers of offers, then it’s just going back to a more-normal market. Not normal yet, but heading that way.

The list prices have been on a rampage, and it’s probably time for them to stop going up so much every month. It was going to happen sooner or later, and that day has probably arrived – finally!

The smoke stack and the rest of the Encina Power Station have been demolished.

What does this mean for Carlsbad?

Before agreeing to support the approval of the new plant, the city negotiated an agreement with NRG and SDG&E to help ensure the project would provide the greatest local community benefit possible.

Some of the provisions of this agreement include:

A guarantee that NRG will completely decommission, demolish and remediate the old Encina Power Station site within three years of Encina’s retirement, at no cost to taxpayers.

NRG will turn over to the city several pieces of property surrounding the lagoon and the blufftop across from the plant. NRG will work with the city and the community to create a plan for the site’s future use.

What can go on the site?

The General Plan envisions redevelopment of the Encina Power Station, as well as the adjacent SDG&E North Coast Service Center, with visitor-serving commercial and open space uses to provide residents and visitors enhanced opportunities for coastal access and services, reflecting the California Coastal Act’s goal of “maximizing public access to the coast.”

Trustindex verifies that the original source of the review is Google.

Jim & Donna Klinge helped us sell our home of 30 years in Ocean Hills. We were very happy with their service and would HIGHLY recommend them to anyone looking for an Honest, Knowledgeable, Skilled, Informed Efficient realty team. Both Jim & Donna were so helpful in different ways and complemented each others skills. Please refer to a more detailed review that we wrote on YELP. Thank You Both for all your help!!!

Jesse O'Hara

June 12, 2025

Trustindex verifies that the original source of the review is Google.

A+ thank you

Lisa Tuomi

June 11, 2025

Trustindex verifies that the original source of the review is Google.

Many years ago, we purchased a home in Carlsbad, using a realtor that was recommended to us - Jim Klinge. Fast forward to 2025, we recently had the privilege of selling 2 homes in Carlsbad, CA and didn't hesitate to reach out to Jim and Donna Klinge of Klinge Realty Group to guide us through the sales. The transactions were very different, each with its own unique situation, opportunities and challenges. From start to finish, Donna and Jim helped navigate the pre-sale preparation, the listing, showing of the house, buyer negotiations, the final close and all of the paperwork and decisions in between. What stands out with both transactions is the professionalism of Jim and Donna (and their team), wonderful communication (timely, relevant, concise), their deep understanding of market dynamics (setting realistic expectations), their access to top-notch contractors, and last, their ability to guide us across the finish line successfully. We wouldn't hesitate to use Jim and Donna in the future and highly recommend them for anyone looking to buy or sell a property in North San Diego County.

Jerry Meyer

March 28, 2025

Trustindex verifies that the original source of the review is Google.

We sold a home with Jim and Donna and from beginning to end they were consummate professionals. Their initial walk through the property resulted in a list of items to be repaired or updated. They supplied a list of vendors and job quotes to do the repairs and updates. We originally wanted to sell ‘as is’ and just get it over with. They gave us a selling price for ‘as is’ and options for doing a few updates/repairs to doing it all with the selling price for each option. We agreed to do all they suggested and we sold for the exact price they predicted. For every dollar spent we got back more than $2 back in the selling price. And they got that price in a rising interest rate environment! Donna and Jim are extremely detailed and guide you through ever aspect of the sale. There were no surprises thanks to their guidance. We couldn’t be more pleased with their representation.

Thank you Donna and Jim,

Jerry and Mary

Heather Quejada

March 27, 2025

Trustindex verifies that the original source of the review is Google.

We have known Jim & Donna Klinge for over a dozen years, having met them in Carlsbad where our children went to the same school. As long time North County residents, it was a no- brainer for us to have the Klinges be our eyes and ears for San Diego real estate in general and North County in particular. As my military career caused our family to move all over the country and overseas to Asia, Europe and the Pacific, we trusted Jim and Donna to help keep our house in Carlsbad rented with reliable and respectful tenants for over 10 years.

Naturally, when the time came to sell our beloved Carlsbad home to pursue a rural lifestyle in retirement out of California, we could think of no better team to represent us than Jim and Donna. They immediately went to work to update our house built in 2004 to current-day standards and trends — in 2 short months they transformed it into a literal modern-day masterpiece. We trusted their judgement implicitly and followed 100% of their recommended changes. When our house finally came on the market, there was a blizzard of serious interest, we had multiple offers by the third day and it sold in just 5 days after a frenzied bidding war for 20% above our asking price! The investment we made in upgrades recommended by Jim and Donna yielded a 4-fold return, in the process setting a new high water mark for a house sold in our community.

In our view, there are no better real estate professionals in all of San Diego than Jim and Donna Klinge. Buying or selling, you must run and beg Jim and Donna Klinge to represent you! Our family will never forget Jim, Donna, and their whole team at Compass — we are forever grateful to them.

Lou F

March 27, 2025

Trustindex verifies that the original source of the review is Google.

WeI had the pleasure of working with Klinge Realty Group to sell our home in Carmel Valley, and I cannot recommend them highly enough!

Jim and Donna demonstrated exceptional professionalism, offering expert guidance on market conditions and pricing strategy, which resulted in a quick and successful sale.

Communication was prompt and we were well-informed throughout the entire process.

For anyone looking for a dedicated and knowledgeable real estate team, look no further!

---

William Sams

March 25, 2025

Trustindex verifies that the original source of the review is Google.

Donna and Jim Klinge of Klinge Realty Group have our highest possible recommendation. From Donna and Jim’s first visit to our house through closing their advice and counsel was candid and honest in all dealings. They kept us fully informed throughout the process. The house sold less than three days after listing with a two-week closing. My wife and I have sold several houses during our lives. This was by far the best experience. Klinge Reality is a premium service realtor. You can’t make a better choice for someone to sell your home fast and for top dollar.

Emily Hernandez

December 29, 2024

Trustindex verifies that the original source of the review is Google.

Donna and Jim provided exceptional support and professionalism throughout the entire process. We couldn't have been happier with their efforts. They made our house shine, and thanks to their expertise, it sold above the listing price in the very first weekend! Truly a fantastic experience from start to finish.

Jesus Adrian Sahagun

November 11, 2024

Trustindex verifies that the original source of the review is Google.

This year has been difficult on our family, mainly due to having to sell our home. Thankfully we knew God had a plan for us and working with the Klinge team was a key part of it. It was an obvious decision to work with them again after such an amazing experience when purchasing the same home we needed to sell. The challenge was, how will we do this in so little time with so much going on? Jim and Donna held our hand every step of the way. Whenever an unexpected issue arose they found and provided a solution. Never once did we feel pressured to make a decision and the Klinges were always reassuring after providing the information that the decision was ours to make. Despite the curve balls, they never panicked and exemplified the “can do” attitude, making us feel optimistic and taken care of. Their expertise and professionalism was superb. But of all the reasons to work with the Klinges, the most impactful and valuable is their compassion and genuine care for their clients. We pray that we can one day purchase our forever home and you better believe that Jim and Donna will be representing us - as long as they will have us of course. Thank you again Klinge team! Your execution, experience, and care are unmatched.

SABIHA PASHA

July 23, 2024

Trustindex verifies that the original source of the review is Google.

Jim and Donna were fantastic! Jim understanding my needs, recommending potential places, pointing out the pros and cons of each property was invaluable. Then when the offer was accepted Donna’s organized guidance through the inspections, paperwork etc made the whole process seem effortless.

So grateful that I had them on my side!