Immaculate Davidson-built one-story with pool/spa, owned Solar, 3-car, putting green, and upgraded interior all on a great cul-de-sac near the lagoon walking trail, Aviara golf course, and Park Hyatt Resort! New carpet and paint, high ceilings, plantation shutters throughout, travertine master bath with walk-in closet, plus roomy loft/master retreat with huge walk-in closet too! Being on the west side of the street gives you two great benefits – afternoon sun for your pool area, and your house doesn’t get hit by golf balls like those across the street.

I had another 80+ people attend my open house on Sunday, and a total of more than 200 people for the weekend. Virtually everyone who came was older, and the overwhelming message was that the buyer pool for one-story homes is large and they are hungry for product.

We have received one full-price cash offer so far, and there should be 2-3 more coming in today.

This smaller tract was built by Davidson in 1996, and sold in the $300,000s originally. Only 12 of the 82 homes are the one-story floor plan – which is typical (some newer tracts don’t have ANY one-story plans). Of the 82 homes, 57 of them, or 70% were purchased for less than $1,000,000.

I sure get the feeling that there are boomers occupying most of the newer tract homes in North San Diego County’s coastal region, and they aren’t going anywhere – unless they can buy a single-story home.

The most interesting part is that my listing will be the third sale of this floor plan in 2022, in a neighborhood where there hasn’t been a sale of this model since June, 2018. It could be another few years before the next one sells, because those who have a single-story home tend to hang onto them.

The doomers want to blame higher rates for the slowdown in sales, but unless we get a flood of one-story homes for sale, the inventory will probably keep shrinking – and be mostly made up of the two-story homes where boomers have gotten lucky and snagged one of the few single-story homes coming to market, or where they gave up and left town. It makes it tough on those buyers who are coming here to retire!

There was at least 100 open-house attendees on Saturday, all of which were 60+ years old. The one-story homes are their own market, and likely to perform much better than the two-story segment which has at least 3x as many built, historically.

There is a mystery foot in the beginning of the interior tour in this video, and it would be a good time to acknowledge the difference made by my wife Donna.

We knew on Saturday that our client’s purchase offer was accepted, contingent upon this house selling. Between Monday and Thursday night, Donna got the home carpeted, painted, and staged by her favorite vendors – people who regularly drop everything to help her out. It is a testimony to how well she has nurtured her relationships with them over the years, and when she needs a favor, she can get one!

Immaculate Davidson-built one-story with pool/spa, Owned Solar, 3-car, putting green, and upgraded interior all on a great cul-de-sac near the lagoon walking trail, Aviara golf course, and Park Hyatt Resort! New carpet and paint, high ceilings, plantation shutters throughout, travertine master bath with walk-in closet, plus roomy loft/master retreat with huge walk-in closet too! Being on the west side of the street gives you two great benefits – afternoon sun for your pool area, and your house doesn’t get hit by golf balls like the model-match across the street that just sold for $2,110,000! Other model-match sold comp (1327 Savannah) closed in June for $2,050,000 – wow!

Open house 12-3pm this Saturday and Sunday, September 17th & 18th.

Are you waiting to buy a home until you can get a sizable discount?

Is it because you know a guy who will give you a deal on any home improvements needed; you’ve got your eye on some new appliances down at the scratch-and-dent outlet; and you were thinking about going through Redfin until you heard they are cancelling their rebates? You want a deal on everything!

Well, here you go!

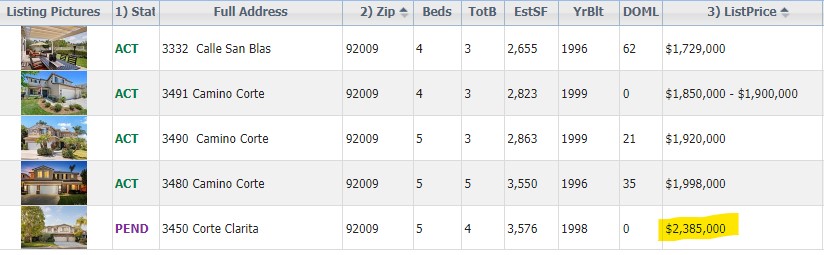

These late-1990s tract homes in SE Carlsbad and in the Encinitas school district are priced LOW. The pending listing on Corte Clarita should close at $2,300,000+ because it had already gone pending once in mid-August but came back on market – then the agent refreshed the listing once he found a second buyer a couple of weeks later. He told me there was no big discount happening there:

You know that my listing is going to be closing for $2,250,000 nearby, plus this one should be over $2,300,000…..so these actives are 10% to 20% under. It looks like the market is crashing….is there a catch?

Look at their locations:

The first three are on the corner of Calle Acervo, and the fourth is next door, but hey, La Costa Canyon High School is walking distance! But you have the traffic from high-school drivers too, and you know it will be a madhouse during football games. A deal is a deal though, and you can save hundreds of thousands compared to the remodeled home with larger canyon lot (in purple at bottom).

Or save millions here! This house is listed for $32,500,000, or go down the street and buy this home that was newly priced today for only $4,900,000! Both are oceanfront La Jolla!

The difference? This house is 1,167sf on a 2,982sf lot….at least for now. But it’s 85% cheaper! And the more-expensive one RAISED their price from $25,000,000.

My point? The low comps won’t suck down the expectations of future sellers of superior homes – it’s too easy for them to ignore/explain away the low comps, and will only consider pricing theirs like the other superior sales nearby – which there will be some.

Oh, what about a foreclosure? Well, they are starting to spike:

Or are you going to wait until you can rub my sizable nose in it?

Hey, I wish prices were lower, and if they crashed it would only mean more opportunity for buyers, and hopefully more volume, which is what I want. I’m not trying to coax buyers into paying too much – I’m showing you where the deals are today, if you don’t mind an inferior home or location.

I just hoping that the coming standoff only lasts a couple of years, instead of 5-10.

The final accuracy of any guess on appreciation doesn’t matter. We all know that they are just guesses.

What matters is whether home buyers and sellers will make decisions today, based on what they read.

If I keep showing data and forecasts that show pricing isn’t tanking between La Jolla and Carlsbad, would it cause you to ignore the national doom and do something different, like buy or sell now?

Or will people just take it all in, and then do what they planned to do all along – move next spring? Or deliberately wait until 2024 to ‘wait-and-see’ what happens then, hoping for something different?

Because for the market to be ‘different’ , there would need to be a change here:

Very few quality homes for sale at less-than-retail pricing.

Most everyone who bought a home in the last 13 years has tremendous incentives to NOT sell it. Will the IRS waive the capital-gains tax to help the real estate market? Will there be a load of new homes built between La Jolla and Carlsbad? Will higher rates make potential sellers panic?

The answer to those questions is ‘very unlikely’, and things are most likely going to stay the same.

Will ANY data or forecasts have an effect on your moving plans?

One of my favorite Compass agents went all out today to promote her new $15,000,000 listing – the MLS remarks:

If these walls could talk, they would speak of the fact that this estate was built by a US ambassador to Italy as a summer home for he and his family with many materials imported from Italy. They’d mention the famous houseguests, upscale fundraisers and political gatherings that have taken place here. Upon driving down the private road to the estate’s gate, you’ll be transported to Tuscany from the moment you pull in. Unlike anything else in the upscale town of Rancho Santa Fe, this home’s historic architecture is met with modern features from a head-to-toe renovation over the last two years.

Billy is a minister and he married a couple back stage right before Saturday’s show (I saw the photo), then cranked out a great set – here’s how it started for those of you who missed it:

Trustindex verifies that the original source of the review is Google.

We sold a home with Jim and Donna and from beginning to end they were consummate professionals. Their initial walk through the property resulted in a list of items to be repaired or updated. They supplied a list of vendors and job quotes to do the repairs and updates. We originally wanted to sell ‘as is’ and just get it over with. They gave us a selling price for ‘as is’ and options for doing a few updates/repairs to doing it all with the selling price for each option. We agreed to do all they suggested and we sold for the exact price they predicted. For every dollar spent we got back more than $2 back in the selling price. And they got that price in a rising interest rate environment! Donna and Jim are extremely detailed and guide you through ever aspect of the sale. There were no surprises thanks to their guidance. We couldn’t be more pleased with their representation.

Thank you Donna and Jim,

Jerry and Mary

Heather Quejada

March 27, 2025

Trustindex verifies that the original source of the review is Google.

We have known Jim & Donna Klinge for over a dozen years, having met them in Carlsbad where our children went to the same school. As long time North County residents, it was a no- brainer for us to have the Klinges be our eyes and ears for San Diego real estate in general and North County in particular. As my military career caused our family to move all over the country and overseas to Asia, Europe and the Pacific, we trusted Jim and Donna to help keep our house in Carlsbad rented with reliable and respectful tenants for over 10 years.

Naturally, when the time came to sell our beloved Carlsbad home to pursue a rural lifestyle in retirement out of California, we could think of no better team to represent us than Jim and Donna. They immediately went to work to update our house built in 2004 to current-day standards and trends — in 2 short months they transformed it into a literal modern-day masterpiece. We trusted their judgement implicitly and followed 100% of their recommended changes. When our house finally came on the market, there was a blizzard of serious interest, we had multiple offers by the third day and it sold in just 5 days after a frenzied bidding war for 20% above our asking price! The investment we made in upgrades recommended by Jim and Donna yielded a 4-fold return, in the process setting a new high water mark for a house sold in our community.

In our view, there are no better real estate professionals in all of San Diego than Jim and Donna Klinge. Buying or selling, you must run and beg Jim and Donna Klinge to represent you! Our family will never forget Jim, Donna, and their whole team at Compass — we are forever grateful to them.

Lou F

March 27, 2025

Trustindex verifies that the original source of the review is Google.

WeI had the pleasure of working with Klinge Realty Group to sell our home in Carmel Valley, and I cannot recommend them highly enough!

Jim and Donna demonstrated exceptional professionalism, offering expert guidance on market conditions and pricing strategy, which resulted in a quick and successful sale.

Communication was prompt and we were well-informed throughout the entire process.

For anyone looking for a dedicated and knowledgeable real estate team, look no further!

---

William Sams

March 25, 2025

Trustindex verifies that the original source of the review is Google.

Donna and Jim Klinge of Klinge Realty Group have our highest possible recommendation. From Donna and Jim’s first visit to our house through closing their advice and counsel was candid and honest in all dealings. They kept us fully informed throughout the process. The house sold less than three days after listing with a two-week closing. My wife and I have sold several houses during our lives. This was by far the best experience. Klinge Reality is a premium service realtor. You can’t make a better choice for someone to sell your home fast and for top dollar.

Emily Hernandez

December 29, 2024

Trustindex verifies that the original source of the review is Google.

Donna and Jim provided exceptional support and professionalism throughout the entire process. We couldn't have been happier with their efforts. They made our house shine, and thanks to their expertise, it sold above the listing price in the very first weekend! Truly a fantastic experience from start to finish.

Jesus Adrian Sahagun

November 11, 2024

Trustindex verifies that the original source of the review is Google.

This year has been difficult on our family, mainly due to having to sell our home. Thankfully we knew God had a plan for us and working with the Klinge team was a key part of it. It was an obvious decision to work with them again after such an amazing experience when purchasing the same home we needed to sell. The challenge was, how will we do this in so little time with so much going on? Jim and Donna held our hand every step of the way. Whenever an unexpected issue arose they found and provided a solution. Never once did we feel pressured to make a decision and the Klinges were always reassuring after providing the information that the decision was ours to make. Despite the curve balls, they never panicked and exemplified the “can do” attitude, making us feel optimistic and taken care of. Their expertise and professionalism was superb. But of all the reasons to work with the Klinges, the most impactful and valuable is their compassion and genuine care for their clients. We pray that we can one day purchase our forever home and you better believe that Jim and Donna will be representing us - as long as they will have us of course. Thank you again Klinge team! Your execution, experience, and care are unmatched.

SABIHA PASHA

July 23, 2024

Trustindex verifies that the original source of the review is Google.

Jim and Donna were fantastic! Jim understanding my needs, recommending potential places, pointing out the pros and cons of each property was invaluable. Then when the offer was accepted Donna’s organized guidance through the inspections, paperwork etc made the whole process seem effortless.

So grateful that I had them on my side!

Anu Koberg

July 13, 2024

Trustindex verifies that the original source of the review is Google.

We first found Jim through his blog at bubbleinfo.com, which really showcased his knowledge of SoCal real estate. Since then we've done three transactions with Jim and Donna, and they are an incredible full service agency, with Jim's deep market insight and Donna's deft contract and project management. We trust them implicitly in their analysis and strategy, which is based on years of experience. They're always available and on top of things, and we strongly recommend them to anyone.

Bjorn Isachsen

July 10, 2024

Trustindex verifies that the original source of the review is Google.

The Good

The Klinge Realty Group operates like a finely tuned machine, with a very personal touch. We contacted them on a Sunday and they were talking to us about our family and our needs on our living room couch the following day. They carefully listened to us and worked with us to identify the best and quickest path to listing within 2 weeks to take advantage of the low inventory conditions in our South Carlsbad neighborhood. They knew our tract specifically and had many previous sales there over the years - they came prepared with a thorough analysis of comparative sales and recommended a pricing strategy that they felt confident would yield offers the first weekend on the market.

The Great

Over the next two weeks Donna coordinated a range of vendors who she knew from experience could get the preparation to list work we needed done on time and with high quality. Our light tune-up involved excellent experiences with their stagers, landscapers, contractors, electricians, and plumbers. Throughout this period Donna's daily communication was clear, concise, and responsive. Any time we had questions Donna picked up the phone or texted immediately - but almost always, she answered our questions before we even knew we had them.

The Outstanding

We had a tricky situation with a shared fence that could have delayed our escrow. Donna used superb mediation skills to negotiate the terms of replacement and was personally on site with the fence contractor to make sure everything went smoothly. The fence looks great and escrow closed on time.

The Truly Exceptional

Our house came on the market on a Wednesday and between then and Monday morning Jim was personally at all three open houses. He was in constant communication explaining potential buyer reaction and strength. As he predicted offers began to come in on Saturday and each one was incrementally higher than the last. At the end we had 5 offers, 4 of which were over list, and the final accepted offer was $100,000 over list. In addition to being over list it included rent back terms that met our needs.

The Recommendation

For all of these reasons we would strongly recommend The Klinge Team to anyone wanting to sell in North County Coastal San Diego. I had been reading Jim's bubbleinfo.com blog for 15 years and knew when the time came to sell that he would be our first call. Jim Klinge is not your standard realtor. He is keenly aware of market conditions and sales strategies. And, works his tail off - though not as hard as Donna . At this point he's gone from realtor to friend and I plan to have him over to grill and chill at our new place to talk real estate, but also just about life and raising kids in San Diego. He's more interested in relationships than his sales numbers - and that's why his sales numbers are so high. We have already recommended the Klinge's to some close friends and another successful sale is on deck right around the corner...

Chris Shea

June 21, 2024

Trustindex verifies that the original source of the review is Google.

We recently had the pleasure of working with Jim and Donna from Klinge Realty Group to sell our house, and we couldn't be more satisfied with the experience. From the initial meeting, they listened attentively to our needs and provided invaluable guidance on specific improvements to get our home market ready.

Their responsiveness throughout the entire process was truly impressive. Anytime we had questions or concerns, they were quick to address them, ensuring we felt comfortable and informed every step of the way. What stood out the most was their team and extensive network of tradespeople, which made addressing any necessary repairs or updates seamless and stress-free.

Thanks to their expertise and dedication, our house sold quickly and at a great price. We highly recommend Jim and Donna to anyone looking to buy or sell a home. They are a fantastic team who truly care about their clients and deliver exceptional results.