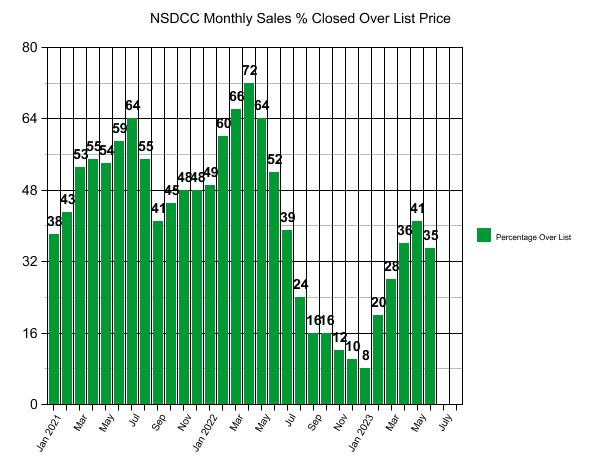

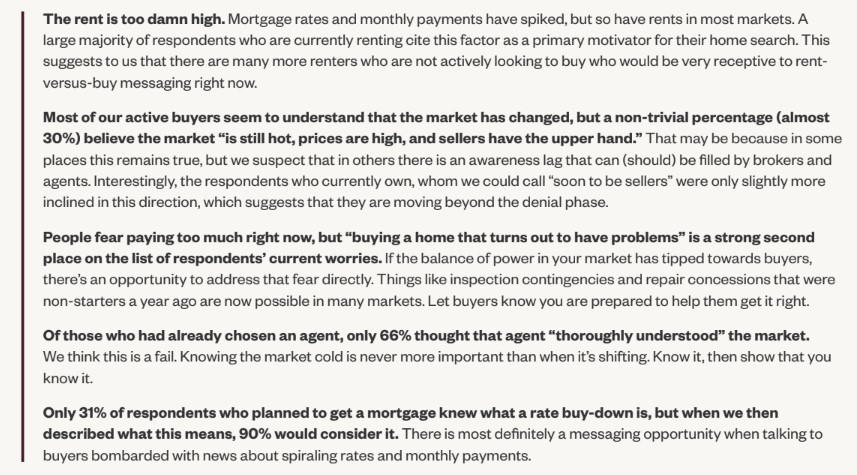

The need to pay over the list price has diminished a bit, but about a third of buyers who closed last month still felt like it was worth paying more than the sellers were asking.

Last month looked a lot like June, 2022! There were 24% fewer sales however, and that trend should continue through the rest of 2023:

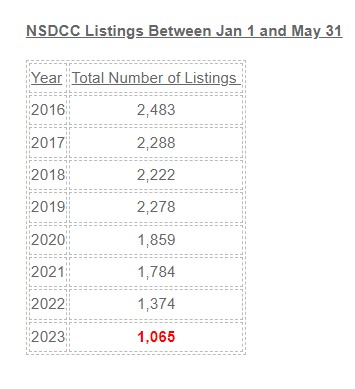

There were 20% fewer listings YoY last month, so with virtually all of the current active listings holding out on price and very little new product to consider, the fate of the 2H23 market will be back to the buyers – how bad do you need to buy a house right now, versus waiting for Spring 2024?

The local home pricing is still off the highs of early-2022, but not by much.

The smaller sample sizes (fewer sales) will make it harder to accurately identify the trends and cause more frustration/indecision for both buyers and sellers. Have we recovered, or just briefly paused the softness?

Most of all, it will expose the skill sets of realtors.

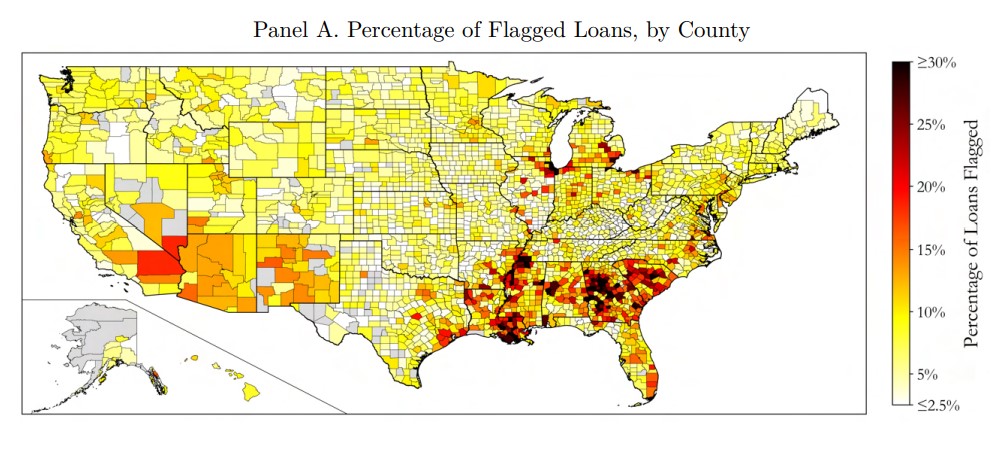

While the PPP fraud was rampant across the country, the ultra-low mortgage rates and lack of inventory were more to blame for inflating home values recently – at least around here:

Anecdotal evidence suggests that many recipients of fraudulent PPP loans used the funds they received to purchase expensive houses, cars, and luxury items.13 In this section, we examine whether recipients of PPP loans flagged as potentially fraudulent are more likely to purchase houses than non-flagged recipients. We first examine house purchases using property records from PropertyRadar for a random sample of 250,000 individual PPP borrowers.

The sample was collected in February 2023 and consists of individual borrowers who received PPP loans during all three rounds of the PPP with data on house purchases through the end of 2022. Round 3 of the PPP ended in June 2021, so we observe at least 18 months of post-PPP house purchase activity for all individuals in the sample. We match names purchasing houses in the PropertyRadar data to names of PPP borrowers, limiting the sample to names that are unique.

A nice combo pack here with two bedroom suites downstairs and private pool. It’s a little light on the premium upgrades but it had enough dazzle to attract multiple bidders. This was a standard tract house when sold new for $422,500 in 2000:

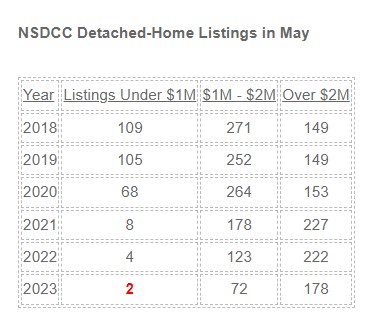

They feel like the good old days but it was only 4-5 years ago that we could count on 200-300 listings priced under $2,000,000 to hit the market every month. It caused some complacency and pickiness among buyers, but now that the choices have narrowed so quickly, there is a lingering panic in the air.

Those buyers who only qualify for $1,000,000 are forced to consider other choices further out, and for many that means out of state.

Those in the $1M to $2M market are shocked to see about a quarter of the number of monthly listings we used to see, but at least they still have a shot – though what you get for that money has been greatly diminished. It’s understandable why the frenzy conditions are still happening though.

Thankfully, a lot of affluent people want to live here!

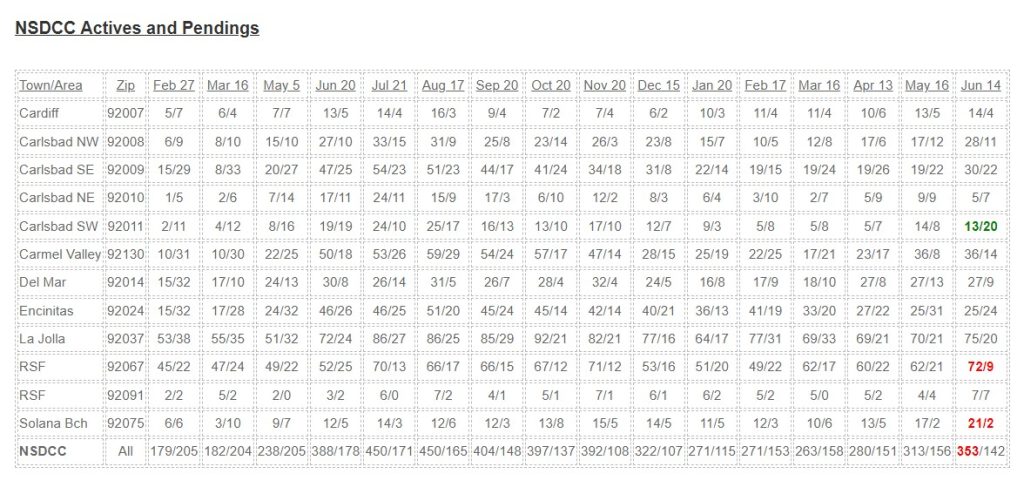

The number of active (unsold) listings has been on the rise, and is now 13% higher than it was a month ago – though I would still characterize the current market conditions as steady.

Compare your stats from this month to last June and July when higher rates had begun to take their toll. The rate-change was rather abrupt, and it was natural for buyers to wait-and-see about the impact which caused the active inventory to soar.

If your area looks similar to last June/July, it’s probably not a good thing.

The activity this year is more normal and typically what happens as the selling season closes out – sellers are too enthusiastic after a couple of hot months and don’t adjust their price expectations fast enough.

There have been 57 closings between La Jolla and Carlsbad this month, which is good. The monthly sales total should finish over 100, but it probably won’t get up to the 168 sales we had in May.

There will be a few more eye-popping sales, but generally the 2023 market is fading away.

I disagreed with the expert opinions yesterday. What are they missing?

My thoughts:

We cannot apply any previous assumptions or beliefs about real estate sales to the market conditions of today – we need to clean the slate. The discussion starts with how the number of people who are willing to sell their home has dropped significantly:

The Ultra-Low Inventory Causes More Volatility

A single one-off sale in La Costa Valley where a cash buyer paid 10% above the last model-match sale has caused a similar increase in other LCV sales. Now pricing is the same or higher than the first half of 2022 which was the peak of the pandemic frenzy.

But will it continue?

Can the current LCV homeowners count on those recent gains holding? Only if they use these recent sales for comps – and they are only good for six months. Buyers in 2024 and beyond will be reluctant to rely on comps that are 1+ years old.

Here’s where the volatility comes in to play. Without having a steady stream of LCV listings to continue the hot streak, we will be starting over each year. Sure, the sellers will use the comps from the previous year, but will the buyers? Will the sellers be satsified with getting the same price as the previous year, os insist on the usual 5% bump or more? Will they improve their home to deserve a premium price? Probably not, which means the buyers will be faced with paying more, for less. Not a good bet, because….

Mortgage Rates Are Going To Remain High

Mortgage rates don’t appear to have much chance of coming down this year. The Fed could raise further and kill any likelihood of rates getting back to 6%, let alone into the 5s, which means….

Home Pricing Will Be Flat

Generally-speaking, the overall pricing will most likely go back to the +/- 3% annually, which gives buyers a reason to pause. Without runaway prices that cause buyers to worry about getting in now before they are priced out forever, they have a reason to pause. They already have to wait patiently for another house to come up for sale, and if they don’t get the feeling that prices aren’t going up – they can, and will, wait for the next one. Might as well if prices aren’t going up much.

Seasonality Is Back

The knucklehaeds who think that housing has recovered are going to get a harsh reminder that real estate is seasonal – even in San Diego. Remember at the end of last year when I documented a few sales where the sellers were lowballed by more than 10% and they took it? It will happen again this year, which leads to…..

The Biggest Fear

Home sellers have had huge gains in equity, and if they have to give some back it won’t hurt much – and some will give more than others. A few low sales in the off-season will thwart the idea that comps from the first-half of the year are sustainable.

We’ve dodged the bullet this year – so far. Each year will be different!

Here are expert opinions on the market. I disagree with all of them:

The year started out with signs showing that the Federal Reserve’s inflation-fighting tactic was effective in cooling down the hot pandemic housing market.

For the first time in 11 years, home prices dropped year-over-year in February as mortgage rates more than doubled following the Fed’s consecutive interest rate hikes, curbing affordability.

However, the median price of a home increased month-over-month for the second consecutive month in March. The median home price is projected to increase for a third month in a row in April to $393,300, which is 2% lower than the previous April’s median price of $401,700, according to data released in May by the National Association of Realtors (NAR).

One big factor behind the strengthening home prices and the decrease in sales volume — down 23% in April from a year ago — is the lack of housing inventory.

“Home sales are bouncing back and forth but remain above recent cyclical lows,” says NAR Chief Economist Lawrence Yun. “The combination of job gains, limited inventory and fluctuating mortgage rates over the last several months have created an environment of push-pull housing demand.”

Where are home prices headed?

Generally speaking, high mortgage rates should prompt house prices to trend downward.

“Yet, housing supply remains so restricted, that any uptick in demand will put upward pressure on prices,” wrote First American Chief economist Mark Fleming in a blogpost. “This is the dynamic that played out in March, as the spring home-buying season ushered in more demand for homes, while insufficient supply prompted buyers to compete and bid up prices.”

No return to typical seasonality in the market

There will be a lot of uncertainty in the economy over the next few months and prospective home buyers are going to be more opportunistic, as opposed to following traditional seasonal market trends, says Bright MLS Chief Economist, Lisa Sturtevant.

“There will continue to be volatility in mortgage rates as we wait to see what the Fed will do at its upcoming meetings and as we watch economic data roll in over the summer,” says Sturtevant. “Prospective buyers are going to be watching rates closely, and many will try to make an offer on a home when they see rates dip. As a result, we should expect less seasonality this year than we had prior to the pandemic.”

More sellers returning to the market

While inventory will remain low this year, we should expect to see more sellers who had been on the sidelines list their home for sale this summer and into the fall, says Sturtevant.

Many existing homeowners have been “locked in” with super low mortgage rates, which has discouraged discretionary moves.

“However, some people have to move, and others will decide to move for a bigger or smaller home, or to change jobs or neighborhoods, despite rates remaining elevated,” says Sturtevant.

The uptick in new home construction has provided more opportunities for move-up buyers who may have been staying in place because they did not have anywhere to move to.

“One thing that could shut down new listings is if we see a sharp spike in mortgage rates to 8 or 9%, a situation that is still unlikely but not out of the realm of possibilities,” she says.

New home construction

Instability of regional banks is a concern for builder and land developer financing going forward, says Robert Dietz, chief economist for the National Association of Home Builders.

Lending conditions for builders have tightened, and the interest rate for development and construction loans is now well above 10%, which threatens housing supply.

Single-family spec home building loans had an effective rate of 13% in the first quarter of 2023 compared to 9% in the first quarter of 2018.

“Our expectation is that the rate of these loans will move lower as the Fed cuts the federal funds rate, but our forecast is that will not happen until later in 2024,” Dietz told USA TODAY. “As a result, land development would be suppressed, and we risk loaning low on lots during a home building rebound in 2024. Lot development can take three years in a typical market.”

The experts are saying that real estate has recovered and everything will be fine now, in spite of high rates. They are quick to add that nobody can predict the future!

Well, it looks fairly predictable to me.

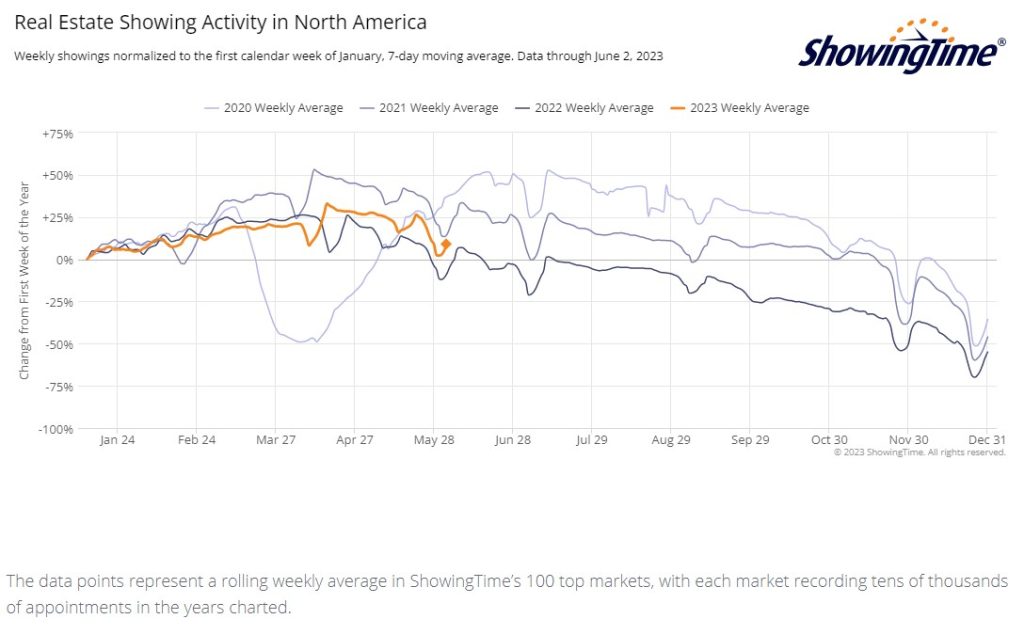

The previous three years plotted above were the hottest frenzy markets of all-time, so we’re lucky just to be having a similar run of showings. But today those showings will be less fruitful, and even if the 2023 trend can stay close, we probably won’t be having as many actual sales.

If the rest of this year goes about the same as recently, we should have a couple of strong weeks in June, take off July 4th, and then a couple of decent weeks in July before drifting off for the rest of the year.

Mortgage rates would have to get into the 5s for it to go any better.

These charts and graphs get updated on the first of the month, so let’s take in the latest data. Everyone laments the general lack of inventory, but can we break it down further?

Yes indeed – and let’s note that the higher-end inventory was bustling during the pandemic which helped fuel the insane frenzy conditions. But look how the number of higher-end listings has cooled off now.

The affluent buyers have never been so frustrated!