We took four listings in a row and I was going to document the whole experience but it was turning into a feature-length movie. Here is the segment where we discuss the bidding war in Rancho Penasquitos, its failure, and how we handled the aftermath:

I comment because you might see a dance version of this video later by yours truly.

I was exposed to this album and The Pretenders debut on the same day, and they probably had everything to do with me moving back to California from Arizona and leaving the metalheads behind.

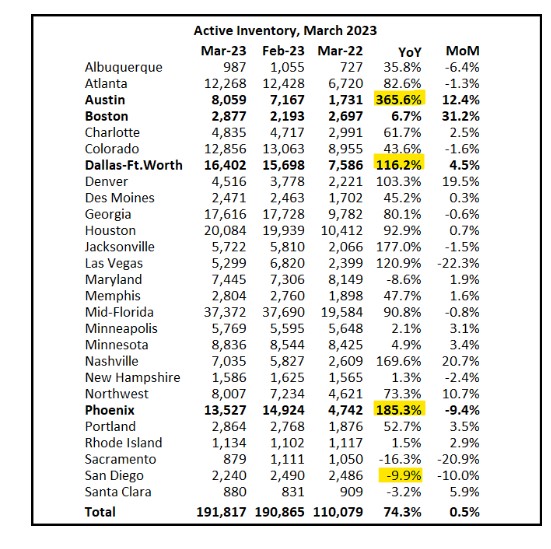

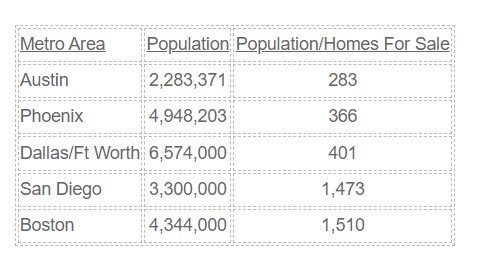

It looks like the San Diego market is surviving the current conditions quite well, while the rest of the country is being crushed by soaring inventory. The Californians must be staying home, and those feeder towns are suffering!

Any town that has a +50% increase year-over-year would be feeling it – which includes virtually every area that people relocating from here would consider.

These are ideal conditions for those who are willing to sell here, and move out-of-state. Sell here, and go rent there for a year or two? Might as well 1031 your house here, and defer those capital-gain taxes!

Hopefully, it will be more predictable than it has been lately!

The Fed’s insistence on raising rates just to see if they can tank the economy should keep a ceiling in place. The buyer pool is already limited to only those who can qualify and have big money, and the generational wealth transfer should be very active between now and 2026 when the estate-tax/gift rules go backwards.

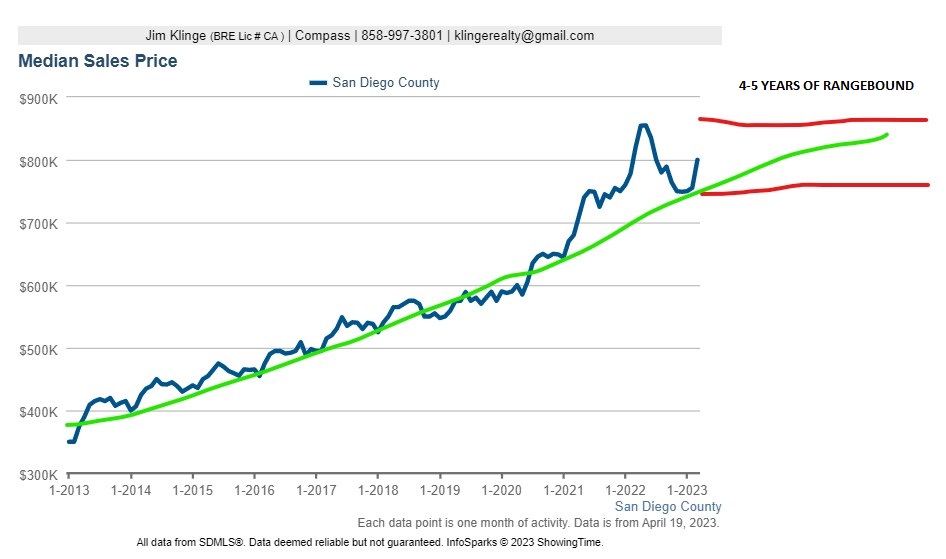

But there isn’t much hope for more inventory, and the limited number of homes for sale should keep a pricing floor in place. It should mean that the overall pricing trend stays rangebound for the next few years – which will be BORING!

But it will be best thing that could ever happen.

If the frenzy conditions settle down and buyers and sellers can make sound financial decisions based on facts and logic, it wouldn’t be a bad thing!

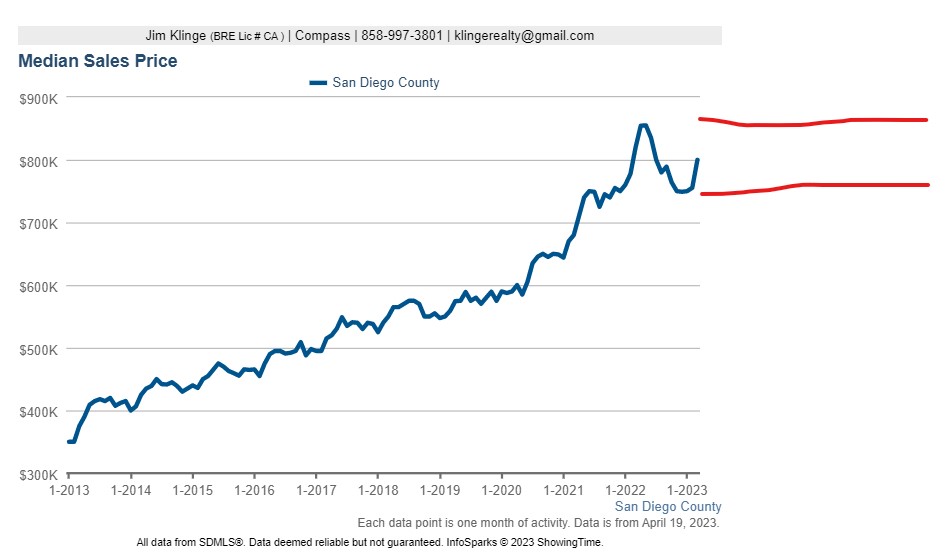

The return of seasonality will keep pricing in check too. The graph shows how the median price usually peaks in the middle of each year, and then is flat or glides downward to the next selling season.

The 2020-2022 Covid-Frenzy price trend was just about straight up!

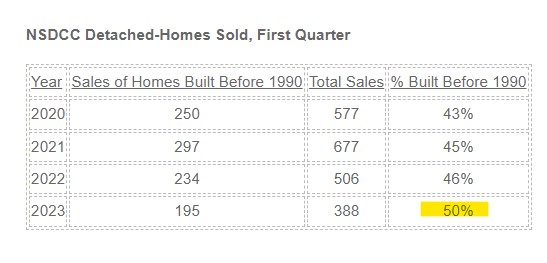

My one post-frenzy prediction was that there wouldn’t be any more sales under $2,000,000 in the Davidson-built Starboard tract in La Costa Oaks (the last was $2,150,000 in October).

We’ve finally had a closing here in the middle of April. They had to knock off $4,000 to make the deal:

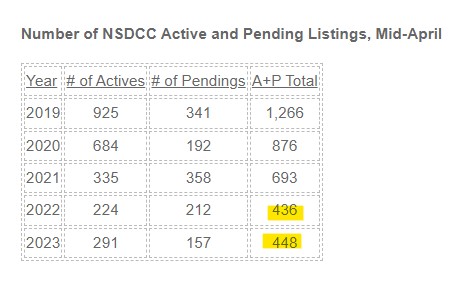

The main cause of the ultra-low inventory is from homebuyers purchasing their forever home – whether they knew it at the time, or not. Between today’s higher rates and the difficulty of buying a better home, just about everybody is stuck in their current house.

How can today’s buyers get a leg up?

Just about everyone wants a newer house vs. older house.

But look at the data.

La Costa Valley, a 25-year old master-planned community of 1,073 houses has ZERO homes for sale today. La Costa Oaks South? That’s right – another zero!

More empty-nesters are staying put, and as a result, the market for newer homes will likely be frozen up for decades due to the lack of inventory.

Predictably, the percentage of older-home sales is on the rise:

The number of estate sales should stay fairly constant, and probably increase in the coming years – and they tend to be the older homes. I know you want to buy a newer home……but those who can get comfortable with fixing up an older home will open up possibilities that other buyers will be ignoring.

Hat tip to the readers who sent in this article found in the tabloid newspaper NY Post. It mentions the Fannie/Freddie fee increase for those with higher credit scores, and fee discount for those with lower credit scores. All the revised policy does is reduce the gap – those with lower credit scores are still paying more.

LLPAs are upfront fees based on factors such as a borrower’s credit score and the size of their down payment. The fees are typically converted into percentage points that alter the buyer’s mortgage rate.

Under the revised LLPA pricing structure, a home buyer with a 740 FICO credit score and a 15% to 20% down payment will face a 1% surcharge – an increase of 0.750% compared to the old fee of just 0.250%.

When absorbed into a long-term mortgage rate, the increase is the equivalent of slightly less than a quarter percentage point in mortgage rate. On a $400,000 loan with a 6% mortgage rate, that buyer could expect their monthly payment to rise by about $40, according to calculations by Stevens.

Meanwhile, buyers with credit scores of 679 or lower will have their fees slashed, resulting in more favorable mortgage rates. For example, a buyer with a 620 FICO credit score with a down payment of 5% or less gets a 1.75% fee discount – a decrease from the old fee rate of 3.50% for that bracket.

When absorbed into the long-term mortgage rate, that equates to a 0.4% to 0.5% discount.

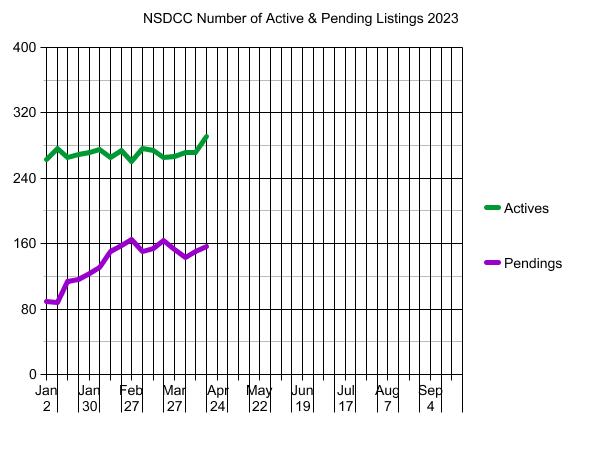

The number of active listings broke out of its range!

But the flow is still a trickle:

It’s hard to tell whether we are starved for inventory or it’s just enough.

We’ll know over the next four weeks as the spring selling season wraps up. Will there be a spurt of new pendings before graduation season/Memorial Day/summer vacations? Or are potential home buyers already getting bored?

Long-time friend Peter gave me a classic Padres jacket that I wore to the game last night, and everyone was asking about it! Hat tip to Gary for getting me on the Silver Slugger wall!