Yesterday, I had two similar occurrences take place so it must mean I should address it!

This comment was left here on the blog:

I just wanted to thank you for your bidding war info. I have followed your blog for many years. We listed our house in Ramona last week and had open house on Fri/Sat. By Monday morning we had six offers. The highest was a very good offer and well over list. The realtor encouraged us to take that one, and said she had asked everyone for highest and best. I pushed her to counter the next two lower offers with the same amount as the first offer and gave permission for her to reveal the offer amount. She was hesitant but I insisted. Both of them came back with the same amount as the highest offer, and the highest original offer then went higher through an escalation clause. I know we don’t have the same prices as NSDCC, but the same principle applies and I wanted to give you credit. MC

MC – thank you for giving me credit!

But did you recognize that his agent’s results aren’t exactly the way I do it?

There are probably blog readers who are emboldened by what they read here. Selling homes doesn’t look that hard, and in a hot market it has to be even easier, right? After listening to me talk about it for a few weeks, it’s probably natural to think you can do it yourself, or direct your agent how to do it.

Are you guessing that MC probably didn’t get top dollar?

The other occurrence was a for-sale-by-owner who suggested he was as good as me – and insinuated that he was better. He will sell his house too, and declare it as top-dollar to feed his ego. But his listing is riddled with things I’d never do, and he’s been on the market for 2-3 weeks with no sale.

ANYBODY CAN SELL THEIR HOUSE THEMSELVES!

You don’t need me – heck, just go stick a sign in the front yard and wait for the phone to ring.

But you’re not going to sell it for the same price that I can get.

Even if you read every word on this blog, it’s not enough. It’s because the most important part of my job is doing one thing really well:

Asking the right questions, the right way, at the right time.

Even if you had the questions, it’s asking them the right way, at the right time, that causes a top-dollar sale.

You can tell that MC was on the right track, but in the heat of the moment, his agent didn’t handle it like I do. But he’s happy, the agent is happy, and they sold it for more money than expected, so all is well. But it didn’t sell for top dollar – which only happens when you ask the questions the right way, at the right time.

Not only will I sell your house for more money than you can, I will sell it for more than virtually all the other realtors. I’m not your typical order-taker; I’m a professional salesman who practices his sales skills daily. Those skills really pay off in the heat of the moment, when I sense that the buyer or their agent is a contender – I know how to say the right thing, the right way, at the right time to capitalize on the moment. Who would you trust in that moment?

It looks easy, but you don’t know what you don’t know.

Wouldn’t you be better served to have Jim the Realtor in your corner?

A remarkable achievement considering that Compass has only been a nationwide company for 3-4 years.

It will matter more later too.

CoStar is going to change the search-portal landscape, and if they spend enough advertising money to get all the eyeballs, the buyer-agents will be cooked. Unlike Zillow and Redfin who encourage viewers to contact their own set of agents, CoStar will direct people back to the listing agent of each property.

You can imagine the advertising that could change everything:

“Would you rather be represented by a third-party who doesn’t know a thing about the house in question, or do you want to speak to the listing agent who knows everything about the property – including how to get you the best deal?”

CoStar got a head start when they boughthomes.com, and are rolling out their first version this summer in New York City.

Buyer-agents will be forced to join realtor teams who have the listings, or just fade away.

Who has Compass been recruiting for the last four years? That’s right, the realtor teams.

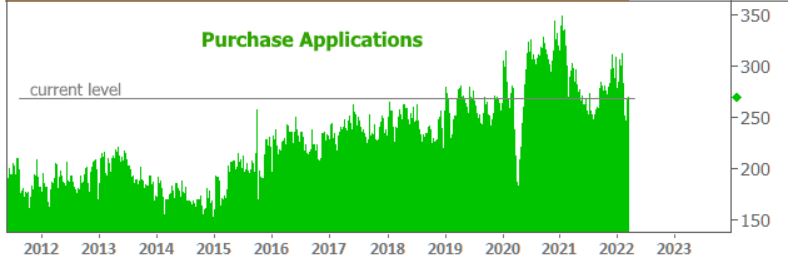

The Mortgage Bankers Association (MBA) released its latest mortgage application numbers this morning and the modest movement belies the drama unfolding in the world of mortgage rates. As usual, the MBA does a good job of capturing average rate movement week to week and they correctly identified last week’s big spike to the highest levels since the first half of 2019.

Despite the surge, mortgage applications didn’t respond in a major way. Refi applications only fell 3% from the previous week. Purchase applications actually managed a small uptick of 1% after last week’s more substantial 9% improvement. But context matters.

As seen in the following chart, refi applications have declined massively from Summertime highs and even more massively from the high levels at the beginning of 2021. MBA notes this week’s tally is 49% lower than the same week last year. The news is less dire on the purchase side. Applications are still lower than most of the past few months, but higher than most of the late summertime months from 2021:

Speaking of context mattering, a longer term chart of the same data really helps put the magnitude of this most recent rate spike into perspective. It’s not an exaggeration to say it’s now the sharpest move higher that any of us have seen in more than a decade (the overall size is about the same as 2016-2018, but this one has happened in roughly 6 short months… not only that, but 2016-2018 was really a 2-parter).

The other takeaways from the chart include the notion that the purchase market is still firing on all cylinders relative to most of the past decade (even then, we can responsibly conclude it would be even higher if not for the low inventory situation) and that refi demand doesn’t have much farther to fall before hitting the historical bottom. In fact, due to the immense equity build-up of the past 2 years, the doldrums of 2017-2018 may not be a relevant baseline this time around.

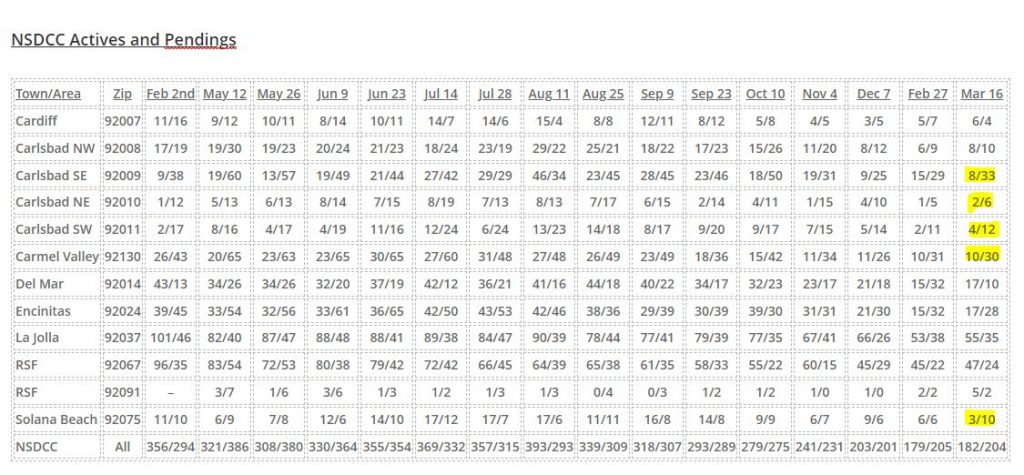

Let’s see which areas are picking up steam early in the selling season:

We used to think that a normal and healthy market has a ratio of 2:1 actives to pendings, so it’s stunning to see five areas that have 3x the number of pendings as actives! And SE Carlsbad has more than 4x!

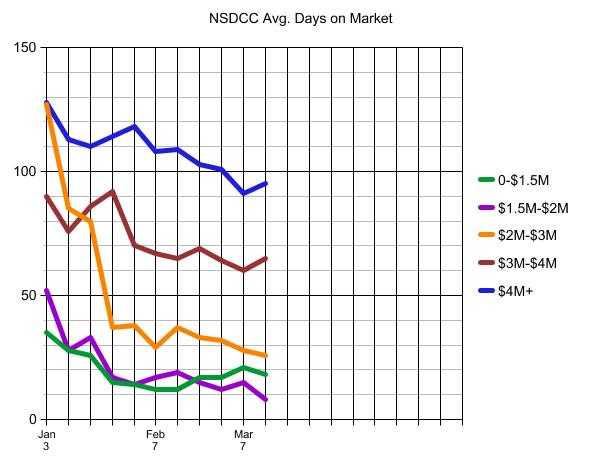

The trend of the average days-on-market can give us a feel for the market direction too:

In 2020, we had 400+ pendings from June 22nd to November 30th – with a peak of 491 pendings on September 7, 2020.

Last year, the high pending count was 386 on May 12th – and this year’s peak will likely be in May too.

It looks like I made an error on the Del Mar A/P counts in the last reading.

I spoke with Jordan at the San Diego County Tax Assessor’s office about their Prop 19 processing. He said they have received about 1,000 requests since Prop 19 went into effect last April 1st, and have completed about half of them. He said there is a backlog of 6-9 months because they are appraising/analyzing every property in question to ensure compliance.

There were 36,936 sales of attached and detached homes in San Diego County since April 1, 2021, so the 1,000 requests (3%) gives us a feel for how effective Prop 19 has been in getting seniors to move (not very).

From Liam at the LAT:

Rose Liebermann opened her property tax bill and did a double take.

The $15,584 she owes on her new West Hills home was almost four times as much as the taxes on her previous house in Granada Hills where she had lived for more than 30 years.

“This bill, when I saw it, I said, ‘This can’t be real,’ ” said Liebermann, 71, a clinical social worker.

It wasn’t supposed to be that way. Proposition 19, narrowly approved by California voters in 2020, gives older homeowners a property tax break when they move. Specifically, it allows those 55 and older to blend the taxable value of their previous home with the value of a new, more expensive home they purchase, resulting in significant tax savings.

But processing delays at the Los Angeles County assessor’s office have left property owners like Liebermann facing hefty tax bills that must be paid while they wait for their applications to be approved.

Nearly a year after the law took effect, the assessor’s office has not completed any of the 1,271 applications it has received to recalculate the property taxes for older and disabled homeowners under the law, according to the agency. And it hasn’t finished any of the nearly 3,700 applications for parent-to-child and grandparent-to-grandchild inheritances, the other major piece of the tax measure.

Liebermann moved last summer because she wanted to help her daughter, Natasha Gershon, who is divorced and raising two young children, including a 10-year-old son with autism. Believing the tax measure would make it possible for her to afford a nicer place, Liebermann decided to buy the larger single-family home in West Hills where they all could live.

Liebermann has since borrowed money through a refinance loan to help pay the property tax and to build an accessory dwelling unit for herself.

Currently, the entry level for Carlsbad houses is around $1,200,000, so when this one first hit the market at $1,119,000 you can bet it stirred up the frenzy!

They raised the list price to $1,199,000, but it didn’t slow anyone down. The agent received 28 offers, and they countered the best five. It closed for $1,525,000!

We gave credit to the ultra-low rates when they were in the 2%-range for helping to create the frenzy. Likewise, higher rates will have something to do with the way the market turns out in 2022.

It’s not because the payment are so much different. When the rate changes from 3.0% to 3.85% on a $1,000,000 loan, the payment only changes $472 per month.

The change will be because of the effect that higher rates have on market psychology.

We’re not going to get a memo on the day when buyers decide that they have had enough.

We know what signs to look for – higher market times, declining SP:LP ratios, and a growing amount of active (unsold) listings – to recognize when the market conditions are adjusting, and it’s been quiet so far.

Harder to measure is how quickly the demand could subside.

With the quality homes fetching an average of five offers each (roughly), then for every sale there is probably 2-3 losers that are literally priced out or voluntarily quit the race. At that rate, the demand could be cut in half or less within a couple of months.

Add the war in the Ukraine, rates well into the 4s, and list prices starting at 10% above the comps, and you have all the ingredients needed for a slowdown. Because the market is so hyped up, there will be ample overshoot and the frenzy should last into summer. But everyone knows it won’t last forever.

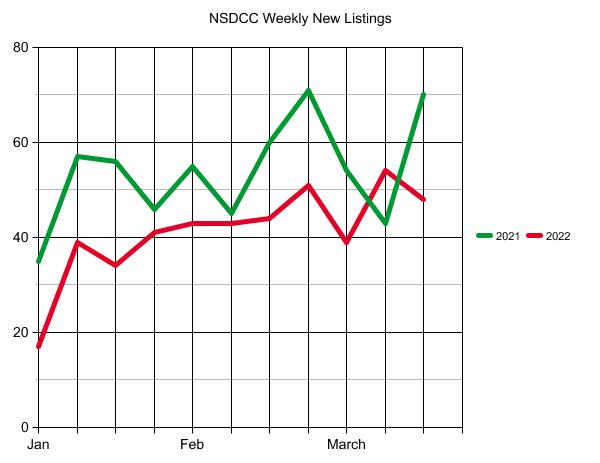

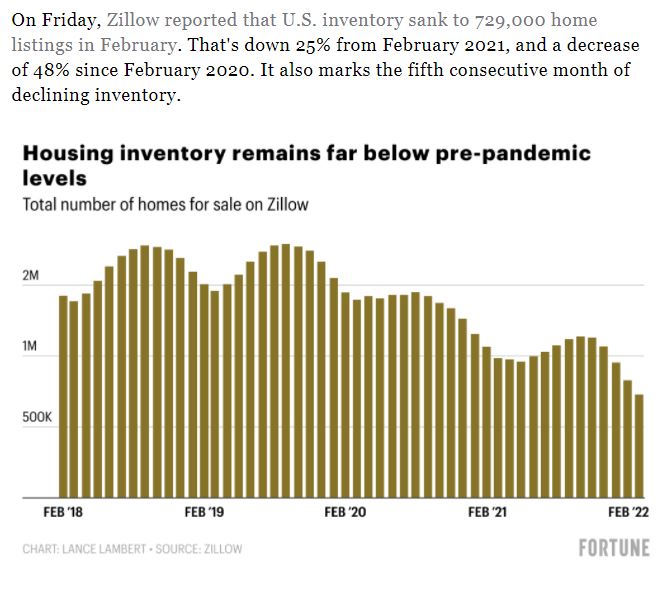

Bill is reporting a 3.1% increase in inventory nationally, which sounds hopeful and we can only pray that it happens here. But we were really far behind after the holidays and we’re still struggling to catch up:

NSDCC Inventory:

March 15, 2021 – 332 Actives, 333 Pendings

March 14, 2022 – 195 Actives, 196 Pendings

The number of houses for sale between La Jolla and Carlsbad is 41% lower than last year!

There wasn’t an obvious winner at the TinyFest – everyone is asking full retail for their product, and it makes you think that going custom is a better choice. And they all do custom!