Some homes are selling for less than their list price!

The original list price was $4,925,000 and this just closed for $4,226,625 for 6 br/6.5 ba, 6,031sf on a 37,026sf lot. Buyer had a license so they discounted the price instead of taking the commission:

I guessed that we’d have 5% more NSDCC sales this year because I expected a surge of delayed sellers who would finally come to market in order to cash in on the record pricing.

But it’s not happening, at least not yet.

The number of NSDCC listings for the first two months of the year is 32% BELOW last year! It means buyers are only going to have a few shots at winning a home.

Here’s what home buyers will have to endure in 2022 to succeed:

Long Waits – Days and weeks will go by without any quality new listings to review. It makes you soft and it’s difficult to keep your chops up.

Coming Soon – Listing agents will tease you by advertising a home for sale, but you can’t see it yet. It’s not always clear when you can see it, and you better not miss the date because…..

Quick Exposure – Once the listing agent is willing to show the house, they will be overcome with the demand, and will likely hit the panic button.

Many will insist that you show them a bank statement and pre-approval letter just to see the house! If you get an appointment, it will be limited to a 15-minute period that is convenient for the listing agent AND be subject to cancellation prematurely because they already took an offer before your scheduled time. Hopefully, you don’t have a job or other responsibilities that limit your scheduling. You will get the feeling it is best to quit your job so you can devote your entire life to home-buying.

No Transparency – If you want to buy it, then just make an offer and you will hear back in a few days.

Over Pay – Not only will you have to pay well over the list price to win, but there won’t be any recent sales to justify any of it. The logic and common sense you usually employ will be your enemy here.

Waiving the Appraisal – What was once an insider trick to improve an offer has turned into a standard on every deal. If you refuse, the listing agents will think you aren’t a serious buyer, and move on.

Shorten the Contingency Periods – You will have 7-10 days to sign off all contingencies. You will need to have a great home inspector on speed dial and who can schedule quickly.

60-Day Free Rentback – Listing agents demand free rentbacks whether the seller needs them or not. Those homes that provide immediate occupancy is a bonus for which buyers will pay extra.

No Repairs – Most buyers are submitting a blank repair-request form with their initial offer.

In spite of all those hurdles, there will still be stiff competition for the quality buys. Once the listing agent has collected enough offers that fit the criteria above, they will then huddle with the sellers in the back room and decide on a winner. This is where having a great agent with a good reputation in the community will pay off. Discount agents, out-of-town agents, buyers who are agents, and agents who don’t look good or don’t smell right are ignored and/or sent to the back of the line.

If you can endure that much and successfully get into escrow, you will be treated with disdain and disrespect that makes you will feel like a suspect, not a valued buyer. The contempt that listing agents have for their prey is palpable – they don’t trust that their initial mistreatment of you will be enough of a lesson, and they will keep it coming because they think that’s their job.

And get this – you will probably lose a few bidding wars before you get up to the desperation level of the other buyers. Oh, you’re not desperate? Then this market probably isn’t for you.

Give it a try and you might get lucky. But if you want a quality home in a good area, then don’t be surprised if the desperation among the competing buyers is higher than you could ever imagine.

The TinyFest comes back to the Del Mar Fairgrounds this weekend, starting at 10am. I’ll be in search of ADUs that can be fully installed at home for a reasonable cost – here was my tour from 2020:

Rising rates may discourage the regular home buyers, but they aren’t the market-makers. All that matters is how many of the desperate-buyers-full-of-cash are left, and with the new listings trickling in, we only need a few!

It’s Thursday and thus time once again for Freddie Mac’s weekly mortgage rate survey. An industry standard report dating back to the 70s, Freddie’s survey rate is standby for multiple news organizations to print their once-a-week mortgage rate color. The net effect is the appearance of a deafening consensus in financial media regarding the going 30yr fixed rate.

The problem is that all of those sources are simply reporting Freddie’s survey headline. The bigger problem is that Freddie’s survey headline often gives the wrong impression about where rates are and how they’ve been moving. This is a logical consequence of the methodology. Freddie sends the survey out on Monday, gets most of it’s responses on Mon/Tue, and then reports “this week’s mortgage rates” on Thursday.

The net effect is that the survey ends up comparing Mon/Tue rates to last week’s Mon/Tue rates. Oftentimes, that doesn’t matter. If rates aren’t moving very much from day to day, the numbers will be relatively accurate as well as the week-over-week change. It’s when volatility surges that the mixed signals show up. And volatility is surging!

Rates aren’t merely changing a lot from day to day, they’re changing multiple times per day in many recent occasions. This week’s landscape was especially troublesome for the Freddie survey because Monday’s rates were, by far, the lowest. In fact, after adjusting for the upfront points and the fact that many of Freddie’s respondents probably didn’t even look past last Friday’s rate offerings before responding, the 3.85% headline isn’t too terribly far from reality.

To be clear, rates are no longer anywhere close to that low. The average lender is now definitively up and over 4.25% for the first time since early 2019. In other words, today’s rates are the highest in almost 3 years.

The owner-occupiers are the crazy bidders, not the investors, so this will have no impact on the current frenzy:

House flippers could be taxed 25 percent of their profit under the California Speculation Act, a bill introduced by Assemblymember Chris Ward, D-San Diego. Assembly Bill 1771 aims to discourage real estate speculation that Ward said drives up home prices as equity investors outbid individual home buyers.

“We’ve heard of people getting into their first home getting beat by cash offers” from investors, Ward said at a news conference Wednesday at the San Diego County Administration Center.

Those investors typically resell the properties soon afterward at inflated prices, stoking competition for limited housing and driving up market prices for comparable homes, he said.

The bill, introduced last week, would impose a 25 percent tax on the profits from a home resold within three years after it’s bought. After the third year, that rate would drop to 20 percent, and decline each year afterward until it is eliminated after seven years.

Most California homeowners keep their property for 10 to 16 years, Ward stated, so it would not affect most people buying a home for personal use.

Certain categories of buyers, such as first-time and military homeowners, would be exempt from the taxes.

Taxes collected from short-term sales would be distributed to cities, schools and affordable housing funds, Ward said.

The goal is to create a disincentive for equity investors, freeing up homes to people buying for personal use. “When investors fall out of the buying pool, that will give regular home buyers a chance to buy a home,” Ward said.

Housing prices rose about 20 percent statewide in 2021, Ward said.

In San Diego, they jumped 26 percent last year, earning the region the distinction as the nation’s least affordable metro area , with housing prices outpacing income.

Meanwhile, the share of homes purchased by investors instead of families has increased in recent years, the bill stated.

First-time homeowner Trisha Cortez spoke during the news conference, describing her recent experience house-hunting in the San Diego area. A health care worker with good credit, she said she was easily able to secure a loan but the home search was a grueling process until she bought a condo in Talmadge.

“I regularly offered above asking prices, but cash buyers would swoop in and take the property,” she said. “I’ve been denied 33 times before getting a home.”

Housing production is falling far behind demand, said University of San Diego economics professor Alan Gin. The region needs about 17,000 new homes per year, but over the past three years it has produced just about half that — 8,216 homes constructed in 2019; 9,472 built in 2020 and 9,358 in 2021, he said.

Other real estate experts said that’s the real issue. Despite efforts to curb real estate speculation, there will be no relief for home buyers until more housing is built, said Lori Pfeiler, CEO of the Building Industry Association of San Diego County.

“While we appreciate Chris’ objective, ultimately this is a supply issue,” Pfeiler said. “We don’t have enough homes for sale, inventory is low and anyone thinking of selling their home just won’t sell their home; they’ll figure out how to hold onto it.”

Pfeiler said lowering fees and reducing regulatory barriers to housing construction would be more effective at curbing prices.

Gin said that San Diego is such a desirable location that housing speculation would likely continue even with greater home production.

Gary London, a real estate economist and senior principal with London Moeder Advisors, warned that while the bill may ease pressure on buyers, it would limit options for sellers. He said most institutional investors target mid-price housing rather than luxury homes, so the sellers most impacted would be middle-income homeowners rather than the wealthy.

“I don’t like it, because it’s effectively an attack on the property rights of sellers,” he said.

Pfeiler also said the bill could inadvertently reduce geographic and economic mobility by restricting people from selling a home because of a job change or other economic necessity, she said.

“Chris is looking for bold ways to help us with the housing crisis, but on many, many fronts this will constrain supply and constrain people’s choices about what job they take and where they locate,” she said.

Ward said that the bill may be amended to exclude primary residences, so people buying homes for their own full-time use would not be taxed.

“We will continue to look for those buckets of people who should be exempted,” he said. “The intent of this bill is not to penalize everybody but to dissuade activity that is driving up prices for everybody.”

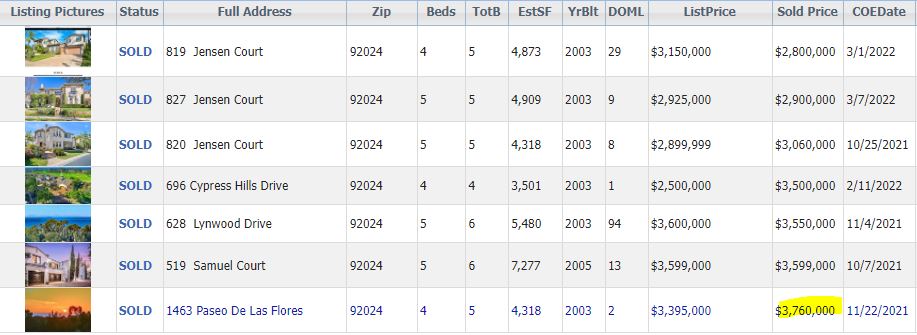

Of the NSDCC detached-home sales in February, 60% of them closed above their list price. The majority of buyers are doing it, and we can expect the trend to continue!

But how much over?

Here are five recent sales that demonstrate the insanity:

Instead of pushing a Code of Ethics that is 109 years old and is unenforceable, the National Association of Realtors should do the same thing and require a similar bill of rights.

Besides, once you ban blind bidding, then open auctions would evolve naturally!

This is the third sale that has closed since I set the ER sales-price record of $3,760,000 in November. This just closed for $2,900,000, which was $25,000 under list. For those who are wondering about future prices, this should be an example of the range to expect as we roll into Plateau City this summer.