Lilac Fire

It’s going to be a long night in Bonsall….

Day Two starts out quiet, and with no wind:

It’s going to be a long night in Bonsall….

Day Two starts out quiet, and with no wind:

Back when this property had two old houses on it, I sold it for:

$400,000 in 1999, then

$725,000 in 2000, and

$825,000 in 2003.

The current owner paid $1,575,000 in 2014, and it took this long to deliver two new condos – buy one or both! P.S. Two of my three clients became realtors!

Shiller is sticking with the irrational exuberance that plays into housing decisions – and I agree:

The co-creator of the much-watched S&P/Case-Shiller home price index doesn’t think the mortgage interest deduction really matters to the housing market.

“It’s not big,” said Yale economics professor and Nobel laureate Robert Shiller.

He also doesn’t think home prices will fall if the cap on the amount of mortgage debt (currently $1 million of debt) one can deduct interest payments on is cut in half. About 2.9 million borrowers have mortgages with an outstanding balance higher than $500,000, according to Black Knight.

“The general idea is it would push prices down if people are rational,” which Shiller says they are not when it comes to housing. He is the author of the bestselling book “Irrational Exuberance.”

He does, however, think that if homeowners can no longer deduct their property taxes, or if the amount they can deduct is limited under the new tax plan, that would be a big deal — at least to rich people.

“That is going to be a substantial hit to people who are paying a lot of property taxes, and it might be a consideration that you make before you buy a big mansion in some high property tax state,” said Shiller.

While economists, housing advocates and housing industry lobbyists argue the effects of the Republican tax plan and worry about the possibility of higher interest rates, Shiller, who has studied the economics of housing dating back to the 1800s, sees very little rhyme or reason to any of it. The human factor — the emotional aspect of most people’s single largest investment, a home — is far greater than the market stimuli that are accorded such importance.

“I tend to think it’s not as great as you imagine because people are people, and I don’t find that historically home prices have relied at all predictably to changes in things like interest rates,” said Shiller, pointing to the huge boom in housing in the last decade. Interest rates didn’t move at all during that time.

That boom, instead, was fueled by a complete crater in any type of lending standard in the mortgage market. People were offered loans at almost no cost, so they took them — and never believed that home prices could fall. In the early 80’s during a huge spike in interest rates to double digits, home prices fell slightly, but people kept buying homes.

“Things happen that have no explanation,” said Shiller.

Click to play video below:

Reader Tim sent this in:

Jim/All – do you have any thoughts on unintended consequences of the tax bills (as constituted)? You think there could be an impact from eliminating interest deduction on equity withdrawals with regard to the cash buyer market? Also wondering if increasing the time homeowners need to be in their home ultimately reduces velocity, which gums up the market further.

My initial thoughts:

What do you think?

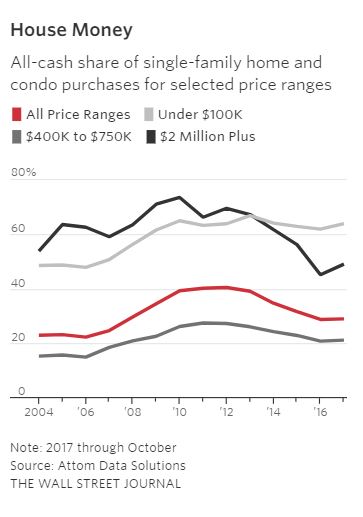

For those who might have seen this article and worried about competing with cash buyers, there hasn’t been much difference around here lately.

NSDCC Detached-Home Sales, Jan-Nov

| Year | ||

| 2013 | ||

| 2014 | ||

| 2015 | ||

| 2016 | ||

| 2017 |

An excerpt:

Meagan Freeman and her boyfriend have been looking for a midprice house in the Seattle area for six months but keep running into a hurdle: cash buyers swooping in and snatching up their properties.

It has happened three times, she said, most recently two weeks ago. The couple bid on a home in an unfashionable suburb they believed was a sure bet in the midst of a dreary Seattle November, when the market typically is slow.

Instead, the 27-year old said, a cash buyer won out yet again.

“It is definitely discouraging,” she said.

Five years after the housing market hit rock bottom, mortgage credit is finally returning to the healthy levels of the early 2000s, before the boom-bust cycle began. But all-cash deals remain well above normal levels, even as prices in many markets have pushed to record highs.

In all, 28.8% of U.S. home sales this year have been all-cash transactions, according to Attom Data Solutions, a data provider. That was down from the peak of more than 40% in 2011 and 2012, when investors were buying homes at a furious pace to turn into rentals. But the percentage of cash deals stands much higher than the 20% or so common in the early 2000s, and it has edged up from 28.6% last year, according to Attom.

Read full article here:

Another fire broke out this morning near the 405 freeway in Bel Air, and it reminded me of the Big One in 1961 when 484 homes were lost. As a result of this fire, the City of Los Angeles was able to initiate a series of fire safety policies and several laws, including the outlawing of wood shake/shingle roofs.

My Dad sold roofing materials at the time, and his company gave him a copy of this film – and I used to take it to school during fire season:

http://www.lafdmuseum.org/bel-air-fire

https://la.curbed.com/2017/12/6/16742976/bel-air-fire-history-brentwood-nixon

Events Calendar for December 2017!

The year 2017 is officially winding down! (Where did it go?!!) There are so many activities and holiday events throughout San Diego but here are some great ones to check out – once you get all of your holiday shopping done of course!

Balboa Park

How the Grinch Stole Christmas – https://www.theoldglobe.org

Carlsbad

Holidays at Legoland – Nov. 18-Jan. 1

Festival of Trees and Silent Auction – Park Hyatt Aviara – Nov. 24-Dec. 27

Coronado

Skating by the Sea – https://hoteldel.com/

Holidays at the Del – https://hoteldel.com/

Del Mar

Holiday Celebration – Dec. 6 / 5-7:30pm

Red Nose Run – Dec. 15 / 1-4pm

Downtown/Gaslamp

Holiday Pet Parade – Dec. 10 / 1-5pm

Encinitas

San Diego Botanic Garden – Dec. 2-23 and 26-30 / 5-9pm

Oceanside

Parade of Lights – Dec. 9th / 7-9pm

Pacific Beach

San Diego Santa Run 5K and 1 Mile Race – Dec. 9 / 8:30am-1pm

Mission Bay Christmas Boat Parade of Lights – Dec. 9th / 6-9pm

Point Loma

The Holiday Stroll on Canon Street – Canon and Rosecrans – Dec 9th / 1-4pm

San Diego

San Diego Bay Parade of Lights –Dec. 10&17 5pm

San Diego Holiday Half Marathon – Dec. 16 / 5am-Noon

Enjoy your holidays everyone!

The share of equity-rich properties rose to a new high—26 percent of homeowners with a mortgage in the third quarter, according to ATTOM Data Solutions’ Q3 2017 U.S. Home Equity & Underwater Report.

In the third quarter, there were more than 14 million U.S. properties considered equity rich, which is when the combined loan amount secured by the property is 50 percent or less of the estimated market value of the property. The number of equity-rich properties is up by 905,000 compared to a year ago, according to the report.

ATTOM Data Solutions found these areas (in metros with a population of 500,000 or more) had the highest share of equity-rich properties:

A few photos of the original condition, and our follow-up:

LINK to realtor.com listing.

As long as the House and Senate can agree, it appears that the tax reform bill will include the existing tax incentives for home buyers (M.I.D. and property-tax deduction up to $10,000). The N.A.R. and C.A.R. aren’t happy though, and are still fighting the fight.

Today, the C.A.R. issued this explanation:

We must reverse the decline in California’s homeownership rate. For over 100 years Congress has incentivized homeownership with the tax code; currently through the mortgage interest deduction. Any effort at reforming the tax code should maintain and prioritize this incentive. The current proposal only pays lip service to incentivizing homeownership. The proposed changes will result in only top earners itemizing their deductions. Therefore, the vast majority of people will no longer receive any tax incentive to purchase a home. So, while the proposal keeps the mortgage interest deduction, the incentive effect of the deduction for Americans to become homeowners disappears.

If you don’t earn enough money to itemize your deductions, you’re probably not buying a house around the coast. It would be nice if they included their math so we could see who they claim as the ‘vast majority’ of buyers.

The M.I.D. and the property-tax deduction are the two primary incentives for home buyers – and they should make it into the final version of the bill.

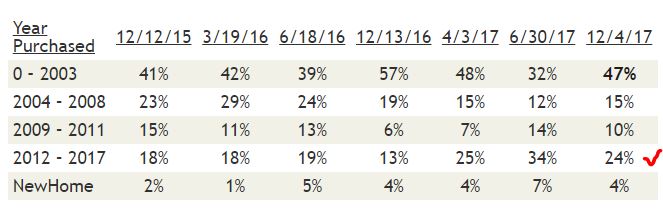

What about the five-out-of-eight years rule? It is a concern for recent purchasers only. The long-timers who make up about half of our sales already qualify for the new rule too.

As you can see in the chart above, on average about 22% of our sellers are recent purchasers. But the actual number of potential delayers is lower.

Today’s stats are from the 116 NSDCC sales we’ve had since November 15th. The 24% equals 28 sales, but five of those were flips, and five others had bought in 2012, and happened to sell right after their fifth anniversary. There were also a couple who sold in less than two years, so they paid the capital-gains tax anyway.

In summary, there were 16 sellers who sold between their two-year and five-year anniversary, or 14% of the total.

It suggests that roughly 14% of the potential sellers over the next 2-3 years might delay their plans to sell, in order to qualify for the tax-free profits. Great, even less inventory – hopefully the estate sales will increase!

The year-over-year sales were already lower in October by 5%, and November isn’t looking any better – and the tax reform hasn’t happened yet. I think we can expect 5% to 10% fewer sales in 2018!

This change to a five-out-of-eight benefit doesn’t really affect today’s buyers – most are planning to stay long-term. The average length of homeownership is already eleven years, and likely to go longer.

The homeowners who will suffer are those who have several houses and planned to move into each for two years to qualify – like Rob Dawg. But if it means you only get to take advantage of the rule once or twice instead of three or four times, at least some benefit came your way – sorry they changed the rules on you. Maybe you can run for president, and fix it? Lower the capital-gains tax while you’re at it!

Are you looking for an experienced agent to help you buy or sell a home?

Contact Jim the Realtor!

CA DRE #01527365, CA DRE #00873197