The amount of new listings is up 5% year-over-year, which isn’t alarming – in fact, it could have inspired more sales, like in 2013. Instead, there are 22 fewer sales this year, which isn’t bad because 2015 was a great year.

NSDCC Action Between Jan 1 – May 31:

Year

# of New Listings

Median LP

# of Closed Sales

Median SP

2006

2,866

$1,125,000

1,109

$989,000

2012

2,109

$975,000

1,138

$800,000

2013

2,312

$1,158,000

1,337

$900,000

2014

2,243

$1,285,000

1,108

$1,000,000

2015

2,255

$1,299,000

1,194

$1,130,000

2016

2,376

$1,450,000

1,172

$1,150,000

The median list price has really jumped this year, and today, 89% of all active listings are priced over $1,000,000.

Yet the number of active listings priced under $800,000 has grown from 26 at the end of April, to 50 today. Remember our new-pendings count of 83 two weeks ago? This week’s count was 58!

But check the first line – the 2006 stats, the high point of the last bubble. It will take a flood of new listings to cause a big problem – the course we are on is to Stagnant City!

Click on the ‘Read More’ link below for the NSDCC active-inventory data:

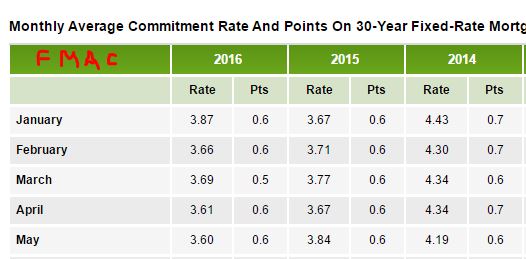

As mortgage rates dipped back into the mid-3s in February, buyers responded. The closed sales in April and May were healthy, and supported by sellers who are being reasonable about price – the cost-per-sf is about the same as last May.

Monthly Detached-Home Sales, Carlsbad to La Jolla

Year

March Sales

April Sales

May Sales

Median SP

Avg $/sf

Median $/sf

2012

238

272

289

$821,000

$380/sf

$311/sf

2013

299

303

362

$943,500

$416/sf

$366/sf

2014

219

258

269

$950,000

$465/sf

$375/sf

2015

294

278

287

$1,125,000

$497/sf

$410/sf

2016

246

300

316

$1,216,250

$497/sf

$415/sf

Flat to slightly-rising prices are the happy compromise for everyone!

When selling a custom beach house, or any house that has a smaller pool of buyers, you can’t leave anything up to chance. Great staging, mass exposure, vivid photography and video, and an agent who recognizes the positives – and can sell them:

The real estate market fluctuates often, making it tough to predict whether the market will favor buyers or sellers when it’s your turn to buy. If you’re shopping for real estate in a market that currently favors sellers, you need to know some tricks of the trade to help ensure you don’t make any mistakes.

Buyers in a seller’s market can get what they want, but they need to bring their “A” game — buying a house in a hot market isn’t for the indecisive. Here are six common mistakes many buyers make — mistakes that you can learn to avoid — when shopping in a seller’s market.

Richard and I were discussing the phenomenon of houses selling for prices that are well-above comps – and how they almost always end up being all-cash sales.

Back in the day, the cash buyers always demanded the best deals – figuring that because they were paying cash, they somehow deserved a better price. But today, cash buyers are throwing around big money to get what they want.

What do they want?

What do they need?

We know that the one-story homes have always been popular, especially with seniors. Guess who has all the money? Yep – the older set.

But there is more to it. Buyers get pickier as prices go up, and now they want everything. You can’t blame them – we are at record prices!

My rule-of-thumb has been that one-story houses sell for a 10% premium over two-story houses. But I think the gap is increasing, and for single-level houses that also have the other valued features like 3-car garage, view, and a low-maintenance but attractive yard, there is a combo premium too.

Part of the pricing pressure is due to the inventory differences. Here’s a look at South Carlsbad over the last six months:

Detached-Home Listings in 92009 and 92011

Type

ACT Listings

Avg. LP/sf

SOLDS last 6 mo.

Avg SP/sf

SP:LP

One-Story

26

$425/sf

67

$418/sf

98%

Two-Story

133

$355/sf

301

$337/sf

95%

If you prefer one-story homes, there aren’t many to consider, and the cost-per-sf premium of the solds is 24%!

When analyzing the comps, you can’t compare 1-story and 2-story homes together – they are two separate markets.

Here are two examples of one-story homes listed yesterday:

You can buy two-story homes that are 600-800sf larger nearby for the same price – or less. But because both of these have other premium features (views, lower-maintenance yards, 3-car, and no pools), and the selection of one-story houses is scant, these two stand a good chance of selling promptly!

With 10,000 baby boomers turning 65 years old every day, it’s understandable that one-story homes are fetching a premium, which today appears to be 10% to 20% above two-story homes.

What is the combo premium for the one-story houses with the extras? It has to be another 10% minimum, and for those that have it all, there is no ceiling.

It means that the method of selling will determine the outcome.

If the seller hires a regular realtor who compares the super-duper one-story to other two-story homes nearby, there will be money left on the table.

This is where the auction format could really pay off. Bidders are uncertain about calculating the value of the extra features, and getting them into a competitive environment will cause them to pay whatever it takes to win.

Get good help – hire a realtor who can evaluate the premiums, and create an auction-like format to ensure top dollar!

Those in the business who know the mortgage underwriting guidelines might enjoy this video – here are my takeaways from today’s Caliber Home Loans talk:

‘Investors’ are banks, mutual funds, insurance cos., hedge funds, etc. who invest in steady streams of income. But they get more than the note rate – discount points and admin fees will bump up the annual returns to 5% – 8%. They are motivated to find ways to fund mortgages!

Income-qualifying the self-employed buyers according to their 24 months of bank statements is an idea that should have been implemented by now – it is a fantastic way to qualify the actual income.

Trended credit is a smart and gives benefit to those who pay off credit cards every month.

Alternative credit is here to stay, and anyone who can verify they are paying on 3 lines of credit on time every month – one being rent – can get a mortgage.

We accept that the government will want to subsidize the mortgage industry. The FHA allows for sub-580 FICO scores on FHA loans (which already accept gift money for down payments and multiple co-borrowers).

They don’t have a direct feed from our MLS, but they give themselves the highest 4-star rating for San Diego?

Median error = half the San Diego zestimates are wrong by more than 6.2%

Zillow, the leading real estate information and home-related marketplace, today launches an update to the Zestimate® algorithm, improving accuracy across the country. Today’s update will improve the national median error rate from 8 percent to 6 percenti.

Additionally, the update, which rolls out over the next 24 hours, improves accuracy in 96 of the 100 largest counties in the U.S.

Zillow publishes Zestimates on more than 100 million homes across the country based on 7.5 million statistical and machine learning models that examine hundreds of data points on each individual home.

In particular, the change includes a model specifically built to value new construction. It will also allow Zillow to process more home value data faster.

“Homes are a big investment, so if you own one, you’re probably wondering what it’s worth. That’s why we created the Zestimate – to freely give consumers as much information as possible about the housing market and homes, so that they can make smart decisions when buying or selling,” said Stan Humphries, Zillow Group chief analytics officer and creator of the Zestimate. “Since we launched the Zestimate 10 years ago, we have been continually working on making it even better. With the additional statistical models and computing power behind today’s update, we are able to provide consumers even better information about millions of homes, equipping them to make informed decisions when talking with a real estate profession about buying or selling.”

To calculate the Zestimate, Zillow uses data from county and tax assessor records, and direct feeds from hundreds of multiple listing services and brokerages. Additionally, Zillow users have updated home facts on more than 50 million homes, enhancing Zillow’s living database of U.S. homes and adding data unavailable anywhere else.

While Zestimates are a great starting point for determining the value of a home, ultimately a home is worth what someone will pay for it. Zillow encourages home buyers and sellers to work with an experienced local real estate professional to determine and fine tune a home’s best price.

i Half of all Zestimates are within 6 percent of the selling price, and half are off by more than 6 percent.

Anyone who thought that the threat of higher mortgage rates would cause buyers to rush their home-buying decision can chillax, as Kayla would say. The threat has subsided, making buyers even more comfortable and deliberate in their search for the perfect match. These guys quote rates with no points:

Mortgage rates were sideways to slightly lower today, keeping them in line with the lowest levels in more than three years.

While there are a few aggressive lenders quoting 3.5% on conventional 30yr fixed loans, 3.625% is the most prevalent quote on top tier scenarios. 3.75% had been more common until last week’s jobs report sent rates quickly lower, and all but eliminated the possibility of a Fed rate hike in June. The Fed Funds Rate does not directly dictate mortgage rates, but increasing expectations for Fed rate hikes tend to coincide with increasing mortgage rates.

When rates have been near these 3-year lows, we’ve only seen them dip lower briefly–and usually not by that much. That means locking is never a bad idea at current levels. Even so, risk-takers could also find justification to float based on the hope that European markets continue to pull US interest rates lower as the European Central Bank (ECB) begins a new bond-buying program tomorrow. As always, if you choose to float, set a limit as to how much rates would have to rise before you’d lock to avoid further losses.

“I continue to favor floating all loans right now. The benchmark European bond, the 10yr Bund, set new record lows today ahead of the ECB corporate bond buying which is set to begin tomorrow. I think it is worth the risk to float overnight to see how that impacts the Bund which will have an impact on US Treasuries. Today, the Bund helped push the 10 year to about a 1month low.” – Victor Burek, Churchill Mortgage