I guessed that we’d have 5% more NSDCC sales this year because I expected a surge of delayed sellers who would finally come to market in order to cash in on the record pricing.

But it’s not happening, at least not yet.

The number of NSDCC listings for the first two months of the year is 32% BELOW last year! It means buyers are only going to have a few shots at winning a home.

Here’s what home buyers will have to endure in 2022 to succeed:

Long Waits – Days and weeks will go by without any quality new listings to review. It makes you soft and it’s difficult to keep your chops up.

Coming Soon – Listing agents will tease you by advertising a home for sale, but you can’t see it yet. It’s not always clear when you can see it, and you better not miss the date because…..

Quick Exposure – Once the listing agent is willing to show the house, they will be overcome with the demand, and will likely hit the panic button.

Many will insist that you show them a bank statement and pre-approval letter just to see the house! If you get an appointment, it will be limited to a 15-minute period that is convenient for the listing agent AND be subject to cancellation prematurely because they already took an offer before your scheduled time. Hopefully, you don’t have a job or other responsibilities that limit your scheduling. You will get the feeling it is best to quit your job so you can devote your entire life to home-buying.

No Transparency – If you want to buy it, then just make an offer and you will hear back in a few days.

Over Pay – Not only will you have to pay well over the list price to win, but there won’t be any recent sales to justify any of it. The logic and common sense you usually employ will be your enemy here.

Waiving the Appraisal – What was once an insider trick to improve an offer has turned into a standard on every deal. If you refuse, the listing agents will think you aren’t a serious buyer, and move on.

Shorten the Contingency Periods – You will have 7-10 days to sign off all contingencies. You will need to have a great home inspector on speed dial and who can schedule quickly.

60-Day Free Rentback – Listing agents demand free rentbacks whether the seller needs them or not. Those homes that provide immediate occupancy is a bonus for which buyers will pay extra.

No Repairs – Most buyers are submitting a blank repair-request form with their initial offer.

In spite of all those hurdles, there will still be stiff competition for the quality buys. Once the listing agent has collected enough offers that fit the criteria above, they will then huddle with the sellers in the back room and decide on a winner. This is where having a great agent with a good reputation in the community will pay off. Discount agents, out-of-town agents, buyers who are agents, and agents who don’t look good or don’t smell right are ignored and/or sent to the back of the line.

If you can endure that much and successfully get into escrow, you will be treated with disdain and disrespect that makes you will feel like a suspect, not a valued buyer. The contempt that listing agents have for their prey is palpable – they don’t trust that their initial mistreatment of you will be enough of a lesson, and they will keep it coming because they think that’s their job.

And get this – you will probably lose a few bidding wars before you get up to the desperation level of the other buyers. Oh, you’re not desperate? Then this market probably isn’t for you.

Give it a try and you might get lucky. But if you want a quality home in a good area, then don’t be surprised if the desperation among the competing buyers is higher than you could ever imagine.

The TinyFest comes back to the Del Mar Fairgrounds this weekend, starting at 10am. I’ll be in search of ADUs that can be fully installed at home for a reasonable cost – here was my tour from 2020:

Rising rates may discourage the regular home buyers, but they aren’t the market-makers. All that matters is how many of the desperate-buyers-full-of-cash are left, and with the new listings trickling in, we only need a few!

It’s Thursday and thus time once again for Freddie Mac’s weekly mortgage rate survey. An industry standard report dating back to the 70s, Freddie’s survey rate is standby for multiple news organizations to print their once-a-week mortgage rate color. The net effect is the appearance of a deafening consensus in financial media regarding the going 30yr fixed rate.

The problem is that all of those sources are simply reporting Freddie’s survey headline. The bigger problem is that Freddie’s survey headline often gives the wrong impression about where rates are and how they’ve been moving. This is a logical consequence of the methodology. Freddie sends the survey out on Monday, gets most of it’s responses on Mon/Tue, and then reports “this week’s mortgage rates” on Thursday.

The net effect is that the survey ends up comparing Mon/Tue rates to last week’s Mon/Tue rates. Oftentimes, that doesn’t matter. If rates aren’t moving very much from day to day, the numbers will be relatively accurate as well as the week-over-week change. It’s when volatility surges that the mixed signals show up. And volatility is surging!

Rates aren’t merely changing a lot from day to day, they’re changing multiple times per day in many recent occasions. This week’s landscape was especially troublesome for the Freddie survey because Monday’s rates were, by far, the lowest. In fact, after adjusting for the upfront points and the fact that many of Freddie’s respondents probably didn’t even look past last Friday’s rate offerings before responding, the 3.85% headline isn’t too terribly far from reality.

To be clear, rates are no longer anywhere close to that low. The average lender is now definitively up and over 4.25% for the first time since early 2019. In other words, today’s rates are the highest in almost 3 years.

The owner-occupiers are the crazy bidders, not the investors, so this will have no impact on the current frenzy:

House flippers could be taxed 25 percent of their profit under the California Speculation Act, a bill introduced by Assemblymember Chris Ward, D-San Diego. Assembly Bill 1771 aims to discourage real estate speculation that Ward said drives up home prices as equity investors outbid individual home buyers.

“We’ve heard of people getting into their first home getting beat by cash offers” from investors, Ward said at a news conference Wednesday at the San Diego County Administration Center.

Those investors typically resell the properties soon afterward at inflated prices, stoking competition for limited housing and driving up market prices for comparable homes, he said.

The bill, introduced last week, would impose a 25 percent tax on the profits from a home resold within three years after it’s bought. After the third year, that rate would drop to 20 percent, and decline each year afterward until it is eliminated after seven years.

Most California homeowners keep their property for 10 to 16 years, Ward stated, so it would not affect most people buying a home for personal use.

Certain categories of buyers, such as first-time and military homeowners, would be exempt from the taxes.

Taxes collected from short-term sales would be distributed to cities, schools and affordable housing funds, Ward said.

The goal is to create a disincentive for equity investors, freeing up homes to people buying for personal use. “When investors fall out of the buying pool, that will give regular home buyers a chance to buy a home,” Ward said.

Housing prices rose about 20 percent statewide in 2021, Ward said.

In San Diego, they jumped 26 percent last year, earning the region the distinction as the nation’s least affordable metro area , with housing prices outpacing income.

Meanwhile, the share of homes purchased by investors instead of families has increased in recent years, the bill stated.

First-time homeowner Trisha Cortez spoke during the news conference, describing her recent experience house-hunting in the San Diego area. A health care worker with good credit, she said she was easily able to secure a loan but the home search was a grueling process until she bought a condo in Talmadge.

“I regularly offered above asking prices, but cash buyers would swoop in and take the property,” she said. “I’ve been denied 33 times before getting a home.”

Housing production is falling far behind demand, said University of San Diego economics professor Alan Gin. The region needs about 17,000 new homes per year, but over the past three years it has produced just about half that — 8,216 homes constructed in 2019; 9,472 built in 2020 and 9,358 in 2021, he said.

Other real estate experts said that’s the real issue. Despite efforts to curb real estate speculation, there will be no relief for home buyers until more housing is built, said Lori Pfeiler, CEO of the Building Industry Association of San Diego County.

“While we appreciate Chris’ objective, ultimately this is a supply issue,” Pfeiler said. “We don’t have enough homes for sale, inventory is low and anyone thinking of selling their home just won’t sell their home; they’ll figure out how to hold onto it.”

Pfeiler said lowering fees and reducing regulatory barriers to housing construction would be more effective at curbing prices.

Gin said that San Diego is such a desirable location that housing speculation would likely continue even with greater home production.

Gary London, a real estate economist and senior principal with London Moeder Advisors, warned that while the bill may ease pressure on buyers, it would limit options for sellers. He said most institutional investors target mid-price housing rather than luxury homes, so the sellers most impacted would be middle-income homeowners rather than the wealthy.

“I don’t like it, because it’s effectively an attack on the property rights of sellers,” he said.

Pfeiler also said the bill could inadvertently reduce geographic and economic mobility by restricting people from selling a home because of a job change or other economic necessity, she said.

“Chris is looking for bold ways to help us with the housing crisis, but on many, many fronts this will constrain supply and constrain people’s choices about what job they take and where they locate,” she said.

Ward said that the bill may be amended to exclude primary residences, so people buying homes for their own full-time use would not be taxed.

“We will continue to look for those buckets of people who should be exempted,” he said. “The intent of this bill is not to penalize everybody but to dissuade activity that is driving up prices for everybody.”

Of the NSDCC detached-home sales in February, 60% of them closed above their list price. The majority of buyers are doing it, and we can expect the trend to continue!

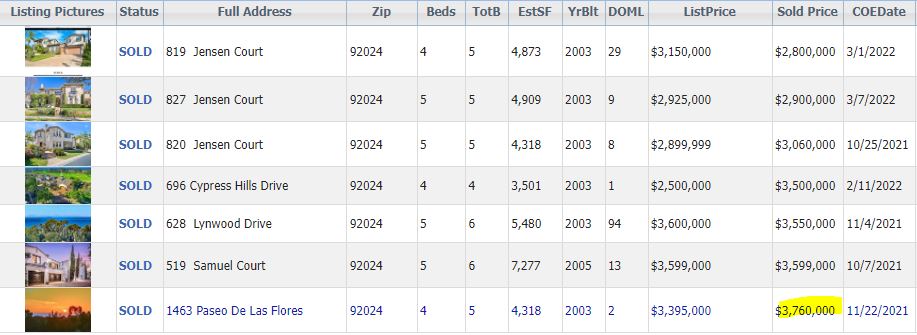

But how much over?

Here are five recent sales that demonstrate the insanity:

Instead of pushing a Code of Ethics that is 109 years old and is unenforceable, the National Association of Realtors should do the same thing and require a similar bill of rights.

Besides, once you ban blind bidding, then open auctions would evolve naturally!

This is the third sale that has closed since I set the ER sales-price record of $3,760,000 in November. This just closed for $2,900,000, which was $25,000 under list. For those who are wondering about future prices, this should be an example of the range to expect as we roll into Plateau City this summer.

Trustindex verifies that the original source of the review is Google.

Jim & Donna Klinge helped us sell our home of 30 years in Ocean Hills. We were very happy with their service and would HIGHLY recommend them to anyone looking for an Honest, Knowledgeable, Skilled, Informed Efficient realty team. Both Jim & Donna were so helpful in different ways and complemented each others skills. Please refer to a more detailed review that we wrote on YELP. Thank You Both for all your help!!!

Jesse O'Hara

June 12, 2025

Trustindex verifies that the original source of the review is Google.

A+ thank you

Lisa Tuomi

June 11, 2025

Trustindex verifies that the original source of the review is Google.

Many years ago, we purchased a home in Carlsbad, using a realtor that was recommended to us - Jim Klinge. Fast forward to 2025, we recently had the privilege of selling 2 homes in Carlsbad, CA and didn't hesitate to reach out to Jim and Donna Klinge of Klinge Realty Group to guide us through the sales. The transactions were very different, each with its own unique situation, opportunities and challenges. From start to finish, Donna and Jim helped navigate the pre-sale preparation, the listing, showing of the house, buyer negotiations, the final close and all of the paperwork and decisions in between. What stands out with both transactions is the professionalism of Jim and Donna (and their team), wonderful communication (timely, relevant, concise), their deep understanding of market dynamics (setting realistic expectations), their access to top-notch contractors, and last, their ability to guide us across the finish line successfully. We wouldn't hesitate to use Jim and Donna in the future and highly recommend them for anyone looking to buy or sell a property in North San Diego County.

Jerry Meyer

March 28, 2025

Trustindex verifies that the original source of the review is Google.

We sold a home with Jim and Donna and from beginning to end they were consummate professionals. Their initial walk through the property resulted in a list of items to be repaired or updated. They supplied a list of vendors and job quotes to do the repairs and updates. We originally wanted to sell ‘as is’ and just get it over with. They gave us a selling price for ‘as is’ and options for doing a few updates/repairs to doing it all with the selling price for each option. We agreed to do all they suggested and we sold for the exact price they predicted. For every dollar spent we got back more than $2 back in the selling price. And they got that price in a rising interest rate environment! Donna and Jim are extremely detailed and guide you through ever aspect of the sale. There were no surprises thanks to their guidance. We couldn’t be more pleased with their representation.

Thank you Donna and Jim,

Jerry and Mary

Heather Quejada

March 27, 2025

Trustindex verifies that the original source of the review is Google.

We have known Jim & Donna Klinge for over a dozen years, having met them in Carlsbad where our children went to the same school. As long time North County residents, it was a no- brainer for us to have the Klinges be our eyes and ears for San Diego real estate in general and North County in particular. As my military career caused our family to move all over the country and overseas to Asia, Europe and the Pacific, we trusted Jim and Donna to help keep our house in Carlsbad rented with reliable and respectful tenants for over 10 years.

Naturally, when the time came to sell our beloved Carlsbad home to pursue a rural lifestyle in retirement out of California, we could think of no better team to represent us than Jim and Donna. They immediately went to work to update our house built in 2004 to current-day standards and trends — in 2 short months they transformed it into a literal modern-day masterpiece. We trusted their judgement implicitly and followed 100% of their recommended changes. When our house finally came on the market, there was a blizzard of serious interest, we had multiple offers by the third day and it sold in just 5 days after a frenzied bidding war for 20% above our asking price! The investment we made in upgrades recommended by Jim and Donna yielded a 4-fold return, in the process setting a new high water mark for a house sold in our community.

In our view, there are no better real estate professionals in all of San Diego than Jim and Donna Klinge. Buying or selling, you must run and beg Jim and Donna Klinge to represent you! Our family will never forget Jim, Donna, and their whole team at Compass — we are forever grateful to them.

Lou F

March 27, 2025

Trustindex verifies that the original source of the review is Google.

WeI had the pleasure of working with Klinge Realty Group to sell our home in Carmel Valley, and I cannot recommend them highly enough!

Jim and Donna demonstrated exceptional professionalism, offering expert guidance on market conditions and pricing strategy, which resulted in a quick and successful sale.

Communication was prompt and we were well-informed throughout the entire process.

For anyone looking for a dedicated and knowledgeable real estate team, look no further!

---

William Sams

March 25, 2025

Trustindex verifies that the original source of the review is Google.

Donna and Jim Klinge of Klinge Realty Group have our highest possible recommendation. From Donna and Jim’s first visit to our house through closing their advice and counsel was candid and honest in all dealings. They kept us fully informed throughout the process. The house sold less than three days after listing with a two-week closing. My wife and I have sold several houses during our lives. This was by far the best experience. Klinge Reality is a premium service realtor. You can’t make a better choice for someone to sell your home fast and for top dollar.

Emily Hernandez

December 29, 2024

Trustindex verifies that the original source of the review is Google.

Donna and Jim provided exceptional support and professionalism throughout the entire process. We couldn't have been happier with their efforts. They made our house shine, and thanks to their expertise, it sold above the listing price in the very first weekend! Truly a fantastic experience from start to finish.

Jesus Adrian Sahagun

November 11, 2024

Trustindex verifies that the original source of the review is Google.

This year has been difficult on our family, mainly due to having to sell our home. Thankfully we knew God had a plan for us and working with the Klinge team was a key part of it. It was an obvious decision to work with them again after such an amazing experience when purchasing the same home we needed to sell. The challenge was, how will we do this in so little time with so much going on? Jim and Donna held our hand every step of the way. Whenever an unexpected issue arose they found and provided a solution. Never once did we feel pressured to make a decision and the Klinges were always reassuring after providing the information that the decision was ours to make. Despite the curve balls, they never panicked and exemplified the “can do” attitude, making us feel optimistic and taken care of. Their expertise and professionalism was superb. But of all the reasons to work with the Klinges, the most impactful and valuable is their compassion and genuine care for their clients. We pray that we can one day purchase our forever home and you better believe that Jim and Donna will be representing us - as long as they will have us of course. Thank you again Klinge team! Your execution, experience, and care are unmatched.

SABIHA PASHA

July 23, 2024

Trustindex verifies that the original source of the review is Google.

Jim and Donna were fantastic! Jim understanding my needs, recommending potential places, pointing out the pros and cons of each property was invaluable. Then when the offer was accepted Donna’s organized guidance through the inspections, paperwork etc made the whole process seem effortless.

So grateful that I had them on my side!