How did your area do last month, and for the first eight months of the year? It would be sufficient to just keep close to 2017, which was a good year for sales:

Town or Area

Zip Code

Aug17

Aug18

Jan-Aug17

Jan-Aug18

Cardiff

92007

7

8

49

39

NW Carlsbad

92008

23

20

147

143

SE Carlsbad

92009

45

47

390

324

NE Carlsbad

92010

10

14

109

117

SW Carlsbad

92011

28

24

189

142

Carmel Vly

92130

28

48

342

335

Del Mar

92014

20

4

105

108

Encinitas

92024

54

36

317

282

La Jolla

92037

18

24

207

227

RSF

92067

22

30

170

159

RSF

92091

11

5

28

21

Solana Bch

92075

13

13

73

63

NSDCC

All Above

279

273

2,126

1,960

Coronado

92118

22

11

124

115

Total NSDCC sales for the first eight months are down 8%, which isn’t the end of the world. The median sales price is up, and the average cost-per-sf is down:

NSDCC median sales price, August, 2017: $1,245,000

NSDCC median sales price, August, 2018: $1,325,000

NSDCC average $$/sf, August, 2017: $549/sf

NSDCC average $$/sf, August, 2018: $534/sf

You would think that the high-dollar areas might be showing some struggle, but in August, both La Jolla and Rancho Santa Fe had great months.

This is how the industry enforces the rules – run an article like this every once in a while that gives tips how to CYA. We do have a form that absolves agents from wrong-doing, which just begs agents to ignore the rules:

From N.A.R.

If you or your client is interested in proceeding with an off-market listing, be aware of the potential peril of compromising your fiduciary and ethical responsibilities. Here are five scenarios to avoid, along with ways to reduce your risk.

The real estate agent or broker, not the seller, is the one pushing for an off-MLS listing. Ensure the decision is made voluntarily, solely by an informed seller. Have a signed listing agreement that spells out to clients the limitations of not listing on the MLS (such as that it may reduce their chances of getting the highest and best price for their home by reducing its exposure more widely to the public).

“Coming soon” marketing that limits the listing’s availability to a specified group of brokers during the premarketing period. Be certain all brokers and buyers have equal access to the listing.

An agent fails to notify their member MLS when a client opts to keep the listing private. Most MLSs require that after a listing agreement is signed, the agent must file a certification—signed by the seller—noting the listing is not to be disseminated to other brokers using MLS. Typically the notification must be filed within two to three business days after a listing agreement is signed. Agents can be fined for failing to do so.

An agent faces accusations of breaching fiduciary duty in order to earn a double commission. Off-market listings can lead to more dual agency transactions, as the agent may actively advertise the property only to his or her clients. While not illegal, the practice can be problematic if the prospect of a double commission is the reason an agent suggested an off-MLS listing. Agents risk being sued by a buyer client, for example, who might believe you didn’t seek the best price since you also represented the seller.

Agents are accused of antitrust or fair housing violations by limiting listing exposure to a narrow buyer segment. Be sure you are fulfilling your duty to “cooperate with other brokers except when cooperation is not in the client’s best interest,” as stated in Article 3 of the REALTORS® Code of Ethics.

We’ve been exploring other towns around the West as alternatives for San Diegans who want to downsize. Heck, let’s pick it up a notch!

Years of doomsday talk at Silicon Valley dinner parties has turned to action.

In recent months, two 150-ton survival bunkers journeyed by land and sea from a Texas warehouse to the shores of New Zealand, where they’re buried 11 feet underground.

Seven Silicon Valley entrepreneurs have purchased bunkers from Rising S Co. and planted them in New Zealand in the past two years, said Gary Lynch, the manufacturer’s general manager. At the first sign of an apocalypse — nuclear war, a killer germ, a French Revolution-style uprising targeting the 1 percent — the Californians plan to hop on a private jet and hunker down, he said.

“New Zealand is an enemy of no one,” Lynch said in an interview from his office in Murchison, Texas, southeast of Dallas. “It’s not a nuclear target. It’s not a target for war. It’s a place where people seek refuge.”

The remote island nation, clinging to the southern part of the globe 2,500 miles off Australia’s coast, has 4.8 million people and six times as many sheep. It has a reputation for natural beauty, easy networking, low-key politicians who bike to work, and rental prices half those of the San Francisco Bay Area. That makes it an increasingly popular destination not only for those fretting about impending dystopia, but for tech entrepreneurs seeking incubators for nurturing startups.

“It’s become one of the places for people in Silicon Valley, mostly because it’s not like Silicon Valley at all,” said Reggie Luedtke, an American biomedical engineer who’s moving to New Zealand in October for the Sir Edmund Hillary Fellowship, a program created to lure tech innovators.

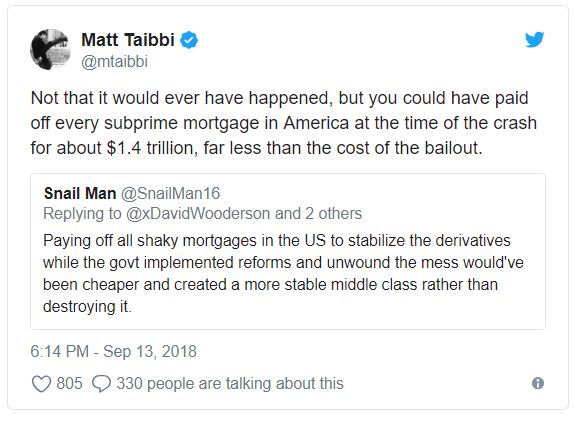

Restoring compensation levels was one of the first and most urgent priorities of the bailout. Bonuses on the street were back to normal within six months. Goldman, which needed billions in public funds, paid an astonishing $16.9 billion in compensation just a year after the crash, a company record.

Even better is the on-going discussion of particular details on twitter:

The ibuyer is the sexy new shiny object in the real estate game. While the idea of a quick and easy sale sounds great, the reality is already much different – and, as the market transitions, their quotes and repair costs should get more conservative (and home sellers be less enamored).

The only local story I’ve heard was one where the ibuyer checked out the property in person, but then didn’t offer, saying it was outside their buying range. You can’t blame them for being picky, and only take the gravy. They will probably stick to the lower-end vanilla properties that are more predictable.

Opendoor, which launched in 2014, says it’s not a house flipper. “We aim for fair market offers, making money on the fees we charge, not the profit on resale,” says Jim Sexton, head of Opendoor’s broker development. The company says it sells 800 homes a month across its 11 markets, with plans to expand to 50 markets by the end of 2020. Currently, it has nearly 3 percent market share in Las Vegas.

Opendoor eyes markets with ample volume, size, and liquidity, Sexton says, adding, “We’re looking for markets that don’t have many barriers to entry, such as hefty transfer taxes or other local or state regulations that make a transaction difficult.”

An Opendoor competitor, Offerpad, operates in eight markets with plans to expand, while Zillow, one of the newest entrants into the direct buying niche with its Instant Offer program, has been successful in Las Vegas and Phoenix, where it expects to buy and sell up to 1,000 homes by year’s end. The new Redfin Now program is available in two California test markets, and Knock, operating in Atlanta and in Charlotte and Raleigh, N.C., enables “trade-in” clients to buy a new home before their existing home is listed.

These companies all claim to speed up and simplify the real estate transaction while removing uncertainty and inconvenience for sellers and buyers. The appeal of the marketing spiel is easy to understand, but how applicable is this model for most consumers? And how likely is it that these companies will become significant players in many markets?

“The market is really driving this model,” says real estate consultant Victor Lund, founder of WAV Group. “The convenience factor, along with an alignment of circumstances are contributing to the growth of iBuyers. Consumers have built up a lot of equity in their homes since the recession, interest rates are low, days on market are low, prices are up, and there’s lots of competition, which puts cash buyers in a better position to buy.” These circumstances create the optimal environment for iBuyers to thrive. Lund believes that once prices slip and homes generally take longer to sell, consumer interest in iBuyers will fade.

Among agents who have interacted with these models, what are they finding? Despite iBuyers’ claims to revolutionize the real estate transaction, some agents are finding their transactions are neither quick nor seamless.

For example, after Ockey’s clients accepted the Opendoor offer, the next step was the inspection. A team of five Opendoor contractors—one for electrical, one for plumbing, one for foundations, and so on—went through the house with a magnifying glass, says Ockey. “They asked us to fix everything you could think of. They wanted bathtubs and toilets replaced if there was even the slightest blemish. They wanted showers retiled and regrouted. It wasn’t little projects; they wanted to remodel the home, and they wanted the seller to pay for it.”

The requested repairs came to about $16,000 on a $300,000 home. Ockey spent weeks negotiating that figure down, which added time and worry to the transaction. “Having representation saved my clients thousands of dollars, but in the end, they made about $10,000 less than they would have selling to a traditional buyer. It’s not horrible, but it’s a lot of money when you only have $20,000 or $30,000 in equity.”

The automated aspects of working with Offerpad didn’t faze Kellie Parten, an agent with HomeSmart Realty in Phoenix, who helped her clients buy a home from the company in May. “It was robotic, but in a positive way,” says Parten. “You can tell that they’re a little bit of a machine, but I didn’t mind because they were very responsive and organized. I never had to ask for something twice.”

Although Parten wouldn’t hesitate to bring a buyer to an iBuyer home, selling to one is a different story. “Offerpad and Opendoor offers on a couple of properties I’ve listed seemed exciting at first, but after you factor in the concessions they request and the additional credits in lieu of repairs after inspections, the net is usually too low and the deals never came together,” she says. One iBuyer recently offered $750,000 on a home that Parten later sold to a traditional buyer for $900,000.

Robert Plant and the Sensational Space Shifters are going to be at Kaaboo on Sunday! How many more times will we have a chance to see him play live in San Diego? Here is the band playing a Led Zeppelin classic that probably has something to do with so many of us choosing to live here:

Spent my days with a woman unkind

Smoked my stuff and drank all my wine.

Made up my mind to make a new start

Going To California with an aching in my heart.

Someone told me there’s a girl out there

With love in her eyes and flowers in her hair.

Took my chances on a big jet plane

Never let them tell you that they’re all the same.

The sea was red and the sky was grey

Wondered how tomorrow could ever follow today.

The mountains and the canyons started to tremble and shake

As the children of the sun began to awake.

Seems that the wrath of the Gods

Got a punch on the nose and it started to flow;

I think I might be sinking.

Throw me a line if I reach it in time

I’ll meet you up there where the path

Runs straight and high.

To find a queen without a king;

They say she plays guitar and cries and sings.

La la la la

Side a white mare in the footsteps of dawn

Tryin’ to find a woman who’s never, never, never been born.

Standing on a hill in my mountain of dreams,

Telling myself it’s not as hard, hard, hard as it seems

Songwriters: Jimmy Page / Robert Plant

A tour of a property that had been on the market since March, but because it was a good-looking 5,328sf one-story in a convenient location, the right buyer came along. This closed for $2,800,000 last month:

There is a very similar story with the risk of a housing bubble.

Real house prices nationwide are again considerably above their trend levels, although in real terms they are still 10–20 percent below their bubble peaks. However, unlike the bubble years, high house prices do not appear to be driving the economy. Residential investment is actually still below its long-term trend measured as a share of GDP. As noted with reference to the stock bubble, consumption is at moderate levels relative to disposable income, indicating a limited housing wealth effect.

Furthermore, this run-up in house prices does appear to be driven largely by the fundamentals of the market. Rents have been substantially outpacing the overall rate of inflation, especially in the markets with the most rapid increases in house prices, like Seattle and San Francisco. Also, vacancy rates have fallen sharply from the peaks reached in the recession, and are low in markets seeing rapid price rises.

There are some causes for concern in the current housing market. In particular, the bottom third of the housing market in several major cities is seeing the most rapid rate of price appreciation.

This raises the risk that many moderate-income homeowners may be buying into bubble-inflated markets, as happened in 2002–2007. That is potentially very bad news for these homeowners who may see their life’s savings disappear quickly if house prices fall 15 to 30 percent. That will not lead to a financial crisis since there is not enough money at stake in these mortgages (most of which are backed by either Fannie Mae, Freddie Mac, or the FHA), but it would be an unfortunate loss to these new homeowners.