Higher prices, higher rates, slowing sales, and now easing loan guidelines? On non-owner-occupied properties? Buying a rental property with 5% down is unheard of, and even with higher rents they are likely to negative cash flow:

Freddie Mac is consolidating its Home Possible program with its Home Possible Advantage Mortgages program. These programs offer greater flexibility and higher loan-to-value ratios (LTVs) than traditional mortgage programs.

The combined product will be called Home Possible Mortgages, and will closely align with the purpose and requirements of the previously-named Home Possible Advantage program, with some changes.

Beginning October 29, 2018, lenders will be able to offer Home Possible Mortgages to buyers with limited down payment funds. Under the consolidated program, eligible homebuyers will include:

non-occupant buyers for mortgages secured by one-unit properties with LTVs no higher than:

95% for Loan Product Advisor Mortgages; or

90% for manually underwritten mortgages (non-occupant buyers were previously excluded from the programs);

those who own other properties (buyers who own other properties were previously limited);

buyers with super conforming mortgages (mortgages with high maximum mortgage limits for homes located in high-cost areas) when the mortgage:

is submitted and receives an “Accept Risk” classification through the Loan Product Advisor; and

has an LTV no higher than 95% (super conforming mortgages were previously not permitted);

buyers with secondary financing, including home equity lines of credit (HELOCs), for most cases when the mortgage’s LTV is no higher than 97% (secondary financing was previously limited to 95% LTV);

buyers using adjustable rate mortgages (ARMs), when the LTV is no higher than 75% (ARMs were previously not permitted); and

buyers with a maximum 45% DTI for manually underwritten mortgages.

These changes are meant to both widen the pool of qualified homebuyers, and streamline programs for lenders’ ease of use.

Housing market risks broaden

By loosening the requirements for its Home Possible Mortgage programs, Freddie Mac’s hope is to encourage lenders to qualify more applicants, thereby increasing homeownership opportunities nationwide.

However, loosening requirements by allowing high LTVs, DTIs and ARMs makes lending — and by extension the housing market — riskier. For veteran real estate professionals, a growing presence of dangerous mortgage products and loose lending restrictions will sound familiar, as they all increased during the Millennium Boom and ultimately played a big part in the cause of the housing crash and 2008 recession.

Though Manhattan has been a buyers’ market for two years, let’s take these with a grain of salt – the slowdown is due to the highlighted sentence in the last paragraph. Hat tip to GW for sending this in:

New York City’s home sellers, tired of waiting for buyers, slashed prices on almost 800 listings in a single week this month, the most in at least 12 years.

In the week through Sept. 9, there were 774 homes in Manhattan, Brooklyn and Queens that got a price cut, the most for any seven-day period in data going back to 2006, according to a report Friday by listings website StreetEasy. The previous weekly record was in March 2009, during the global recession, when 713 properties were reduced.

Sellers with older listings are adjusting expectations just as a wave of newer properties hits the market — customary in New York after Labor Day. In that same September week, Manhattan got 662 additional listings, the third-highest total for any week in StreetEasy’s data.

“It’s a big gut-check for sellers,” said Grant Long, senior economist at StreetEasy. “We’re at a period in the sales market where sellers have been incredibly ambitious with the prices they’re asking. They’re having to come down and bring prices to where demand actually exists.”

Hat tip to Rob Dawg for sending in this article on the top destination cities for U-Haul users. Because it’s just one company, it isn’t the comprehensive list, but we can probably assume that these towns are where people move who are more budget-conscious, and do their own move?

Houston is the No. 1 U.S. Destination City according to the latest U-Haul migration trends report, continuing its run atop the list for the ninth consecutive year.

Houston saw a 5 percent year-over-year increase in one-way U-Haul truck arrivals in 2017 to maintain its status as the busiest locale for incoming traffic among do-it-yourself movers.

“We are an international city with a strong housing market,” stated Matt Merrill, U-Haul Company of West Houston president. “The cost of living remains relatively inexpensive. The average paycheck goes further in Houston. Many companies are relocating here and bringing jobs to our communities. With U-Haul helping move people to the next chapter of their lives, I’m not surprised Houston is the top destination city again.”

After using Zillow for years, consumers probably start to cozy up to the zestimates, just out of familiarity and convenience.

Those who are new to the game – and believe Zillow to be an authority – are going to think the zestimate is a neutral opinion of actual value. But the zestimate is simply based on the list price, and not some fancy algorithm.

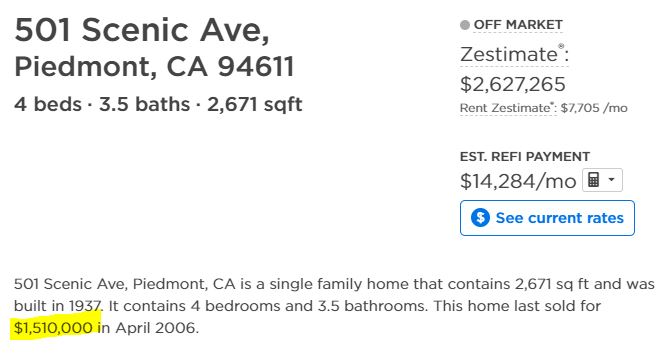

Ryan at the sacramentoappraisalblog.com ran a post that showed how a zestimate fluctuated during the time the house was on the market.

The zestimate nearly matched the list price, then went down with the first price reduction. Then once it sold, it really went nuts.

Here’s one of my all-time favorite houses in Olde Carlsbad. For those who want a non-tract custom home on a big lot with no HOA, you should check it out!

I did help the owners purchase the home, but they didn’t list with me – they listed with their sister. It happens a lot – we estimate that at least 10% of our clients have close family members become agents, or the clients themselves become realtors.

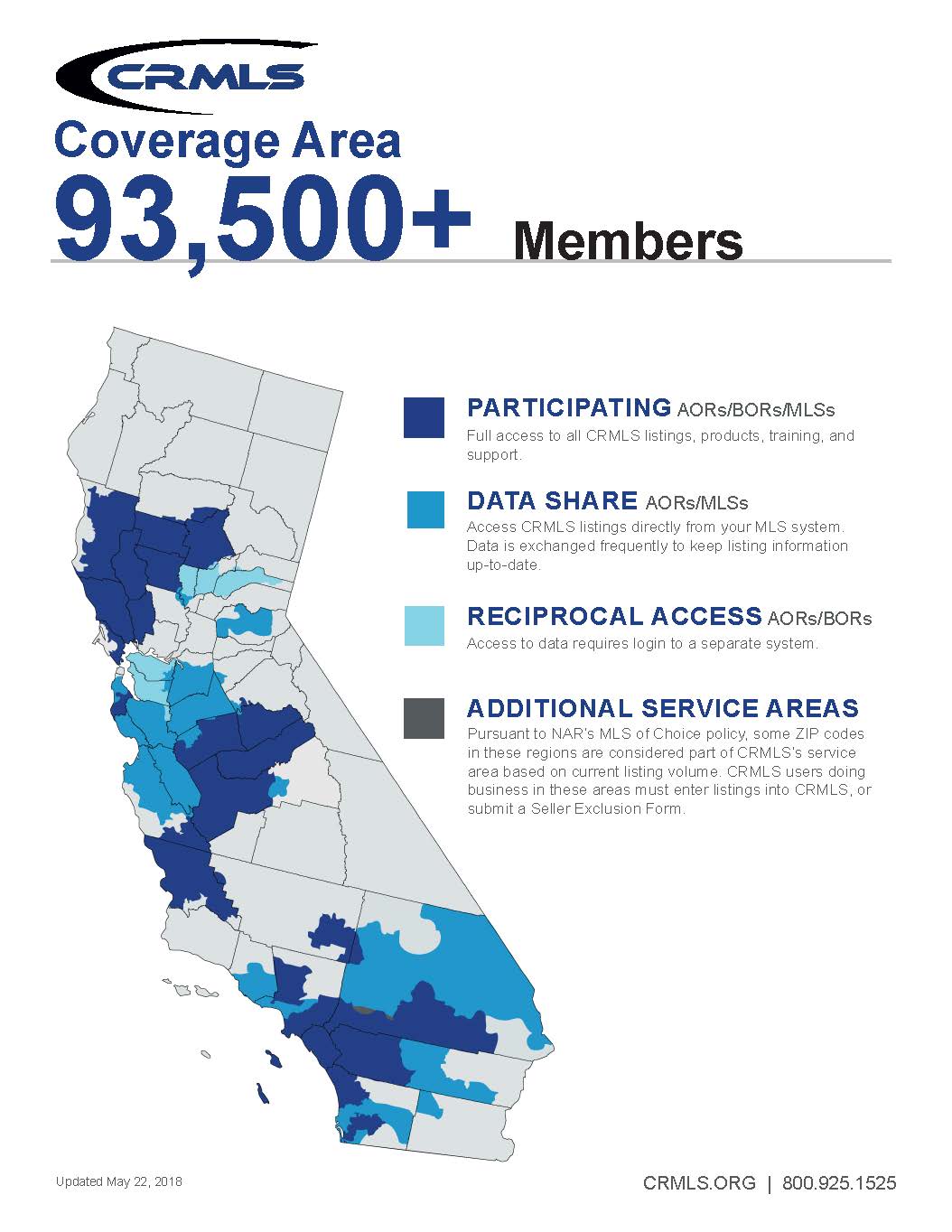

Our local associations of realtors are done suing each other, and as of today, those of us in the NSDCAR are officially using the nearly-statewide CRMLS. We are going to share the other local option, SDMLS, for the next two years so consumers probably won’t notice any difference on the portals.

What does it mean?

It means Jim the Realtor is going state-wide!

Well, almost – the map above shows the areas of coverage. While Temecula and the OC would be obvious markets that are closer to home, it’s not out of the question that I can sell homes anywhere.

When my Dad died in 2010, I sold my parents’ home in Concord for top dollar, and the long-timers here might remember my grandparents’ house.

My sister had just become a realtor in the Bay Area when it came time to sell the family homestead. It was a custom home my grandparents had bought in the 1940s, and there had not been much upkeep or improvements:

Plus, like with many families, there was an overload of sentimental value. It’s where we had most of the holiday gatherings, and there’s even a photo somewhere of me as a toddler sitting on Earl Warren’s lap in the living room!

My Mom and sister were convinced that it would sell for over $2,000,000.

I told them to send me the comps, and once reviewed, I said it was going to sell for $1,500,000. They were outraged and hurt, and accused me of knowing nothing about the local market – how could I possibly offer any assistance?

Here’s how it turned out:

I don’t think it’s feasible to be able to help homebuyers in other areas, but I can offer my full compliment of sales skills to sellers – contact me and we can discuss. I already have a listing coming in Murrieta, and another possible one in the OC so we’ll see how it goes. Tract houses and condos are a little easier to evaluate, but as you saw with my grandparents’ house, I can get pretty close on the custom estates too.

One other change with the CRMLS:

They have the same policy as Sandicor did about requiring that listings are inputted onto the system within 48 hours – but CRMLS only counts business days, not calendar days. So listings taken on Thursday don’t have to be inputted until Monday. Of course, agents are still welcome to use the SELM form to exclude the listing for days or weeks if they so desire.

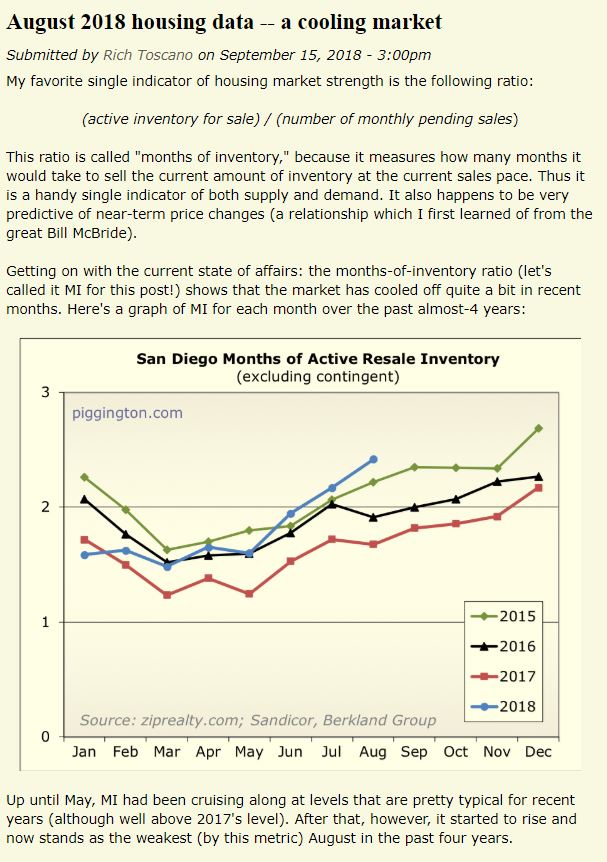

Rich didn’t sound any alarms in his most-recent post, and he is among the most neutral observers – he’s not in a real-estate-related profession. He said:

So, there’s nothing extraordinary or panic-worthy here… the market is a good amount weaker than it was in recent times, but that’s coming from a very hot market, so things are still very much in the realm of normalcy at this time.

You can see why. The inventory remains relatively low, and it wouldn’t take much for it to plunge again. Rich made the point that with both rates and prices higher, we may have reached the tipping point, but if one or both were to relax a bit, the current inventory would thin out.

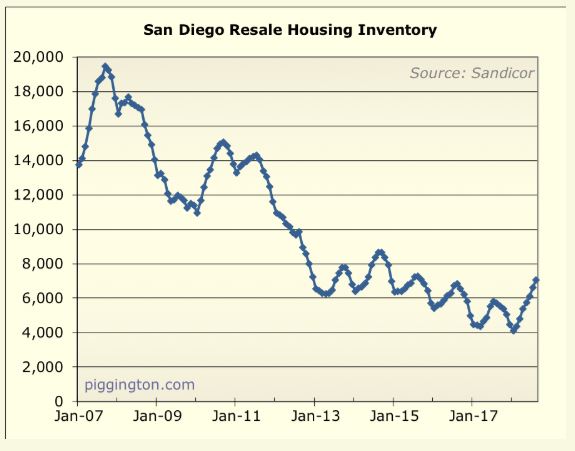

You can see in the graph above that the inventory peaked in the middle of the year previously, when in 2018 it’s kept growing. We may just have more sellers waiting longer into the year before cancelling their listing for the holidays.

This graph doesn’t trigger any alarms either:

More factors that will create more Stagnant City, instead of a downturn:

The county population has grown by roughly 300,000 people already this decade, and is expected to grow by another 600,000 people by 2050. Home building is so anemic that we will be short 150,000 homes by then!

The move-up market is comatose. Prices have gone up so fast that it is miracle work trying to make sense of moving up – you really have to have a good reason, and loads of money. My rule-of-thumb is still in effect – you need to spend 50% more than the price of your old home to have it work (if you sell your a million, you can’t stay in the same area and spend $1.1 million – there isn’t enough additional benefit – maybe an extra bedroom?). There is too big of a delta between the purchase prices for someone who bought at $800,000 and can sell now for $1,000,000 who then needs to spend $1,500,000 to get enough benefit.

Virtually nobody knows different market conditions than what we’ve had this decade. Anybody who got into this in the last nine years has only known a seller’s market, and the rest of us are too old to remember!

Buyers don’t lowball, instead, they just walk away – which doesn’t give overly-optimistic sellers any feedback on price. They just keep waiting for that magical nuclear family with 2.2 kids to show up tomorrow.

The trend for agents to be on salary or lower commissions means they aren’t going to work too hard – and won’t employ the expertise to create solutions.

There are just enough sales to keep everybody optimistic!

The total number of NSDCC listings are steady, in spite of more ‘re-freshing’ than ever:

Year

Number of Listings between Jan 1 and Sept 15

2013

3,899

2014

3,755

2015

4,018

2016

4,150

2017

3,728

2018

3,763

As long as fewer people want to sell, expect more of the same.

Initially this had a lot of promise being the HGTV winner and being oceanfront for only $15 million, but as the film rolls on, you realize the high density – it is practically like a condo. It might be better enjoyed with the volume down: