Let’s look closer at the individual neighborhoods, and compare annual sales and pricing between 2016 and 2017:

Town

Zip Code

2016 Sales

Avg $$/sf

Med SP

2017 Sales

Avg $$/sf

Med SP

Cardiff

92007

82

$711

$1,407,500

76

$711

$1,300,000

NW C-bad

92008

220

$465

$897,400

189

$429

$875,000

SE C-bad

92009

498

$343

$900,000

531

$363

$981,000

NE C-bad

92010

162

$343

$731,250

168

$367

$804,402

SW C-bad

92011

280

$393

$935,000

275

$413

$999,000

Crml Vly

92130

540

$409

$1,144,500

486

$441

$1,218,400

Del Mar

92014

162

$966

$1,787,500

163

$814

$1,800,000

Encinitas

92024

499

$530

$1,185,000

446

$568

$1,212,250

La Jolla

92037

354

$829

$1,918,250

328

$846

$2,172,500

RSF

67+91

251

$512

$2,272,500

284

$494

$2,240,000

Solana B

92075

86

$708

$1,310,000

98

$786

$1,500,000

NSDCC

All Above

3,103

$1,160,000

3,075

$1,225,000

SanMarcosSo.

92078

529

$291

$679,000

530

$316

$730,000

PB/MB

92109

226

$673

$1,082,500

225

$755

$1,195,000

West RB

92127

561

$343

$900,000

615

$366

$1,050,000

East RB

92128

533

$347

$660,000

513

$371

$725,000

RP

92129

450

$338

$720,000

374

$380

$759,500

Scripps R

92131

333

$340

$830,000

320

$367

$910,000

The velocity is slowing a bit from previous years. Of the 17 areas:

Ten had fewer sales in 2017.

Three had a lower cost-per-sf in 2017.

Three had a lower median sales price in 2017.

Rancho Santa Fe had the cost-per-sf and median sales price dip slightly, but the annual sales were up 13%. NW Carlsbad had sales, cost-per-sf, and median SP all go down.

The current market conditions are very positive, especially on the lower-end of North San Diego County’s coastal region.

Of the houses listed under $1,500,000, there are 151 actives and 167 pendings, which is fantastic. The market of houses listed over $1,500,000 is more sluggish, with 493 actives and 102 pendings.

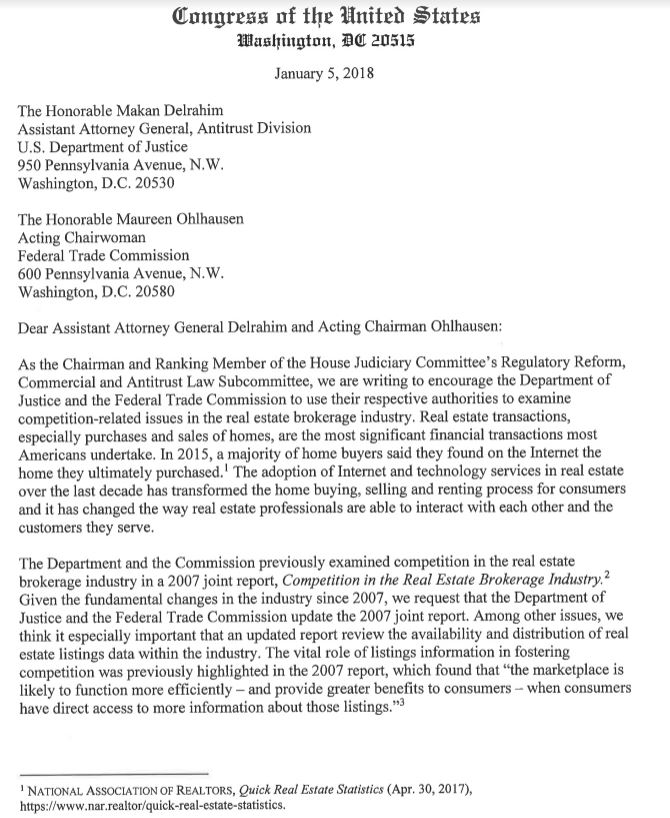

We see agents take great delight in pushing ‘off-market’ deals as a vehicle to double-end commissions, while industry bosses look the other way.

Might these two congressmen stumble upon it, and decide to do something? Seen at I-News:

NAR general counsel Katie Johnson said:

The National Association of REALTORS® is aware of plans for a workshop to be co-hosted by the Federal Trade Commission and the U.S. Department of Justice on the topic of competition in the real estate industry. NAR has contacted both agencies and looks forward to the opportunity to demonstrate the reality that the real estate market is vibrant, healthy, and vigorously competitive. REALTORS® serve the best interest of consumers and provide them with more real estate information today than has ever been available.

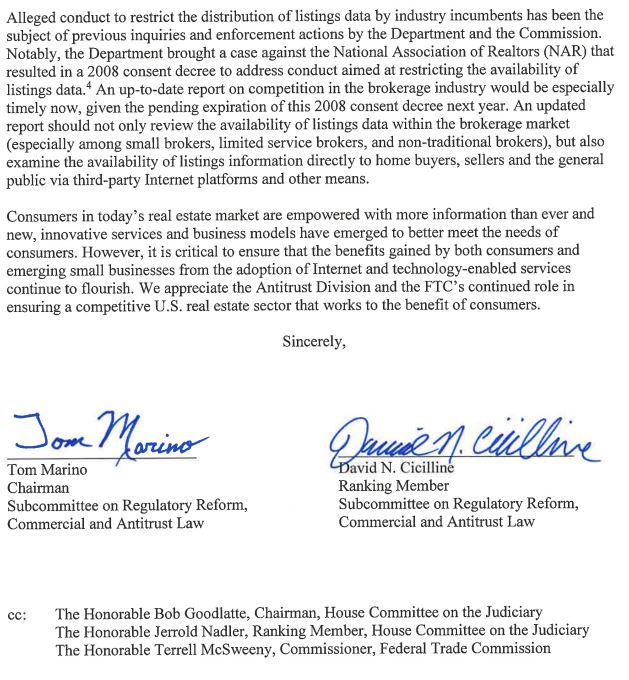

Mortgage rates have risen almost one-half percent this year, and are around 4.50% with no points today (conforming and jumbo). Because rates haven’t moved much in recent years, the half-point increase sounds dramatic, and could cause a few people to reach for the panic button.

But there’s no need to panic.

During the Frenzy of 2013, rates went up higher in less than half the time of the current increase:

But home prices didn’t back off – instead, our NSDCC median sales price has risen 40% since July, 2013!

But aren’t we closer to a new market peak now, and higher rates will just be the beginning of the end? After all, the last two readings of the SD Case-Shiller have declined month-over-month, and those are calculating county-wide sales that are generally lower priced than NSDCC.

While the higher-rates/higher-prices/tax reform/insert-your-favorite-doom will likely cause nervous buyers to pause, the market has always been made by the buyers with less caution and more horsepower.

They might be more selective going forward, which means only the cream-puffs will be selling for retail, or retail-plus – the inventory of those is too tight, and the competition will drive the sales price.

It’s the sellers of homes that are lingering unsold who might want to sharpen their pencil on their list price. Once you’ve been on the market and not selling for 2-3 months, do you really need to keep pressing for that extra 5% to 10% on top of what the last guy got – and risk not selling at all?

If higher rates do become an issue, it is a problem that is easy to fix, unlike tax reform or higher prices.

Buyers can either opt for a 5-year or 7-year fixed rate to stay under 4%, or ask the seller to buy down the rate. Sellers who are getting a 5% premium over last year’s prices shouldn’t mind paying 1% or 2% to make the deal.

The number of NSDCC houses being listed in January has been remarkably consistent, but the $197,100 increase in the median list price since last year will be a lot to swallow:

Year

Number of January Listings

Median List Price

2013

410

$1,137,500

2014

413

$1,295,000

2015

401

$1,300,000

2016

470

$1,465,000

2017

393

$1,499,900

2018

398

$1,697,000

We did pick up 18 more pendings this week, and the usual start of our selling season, the Super Bowl, is now complete. It’s go time!

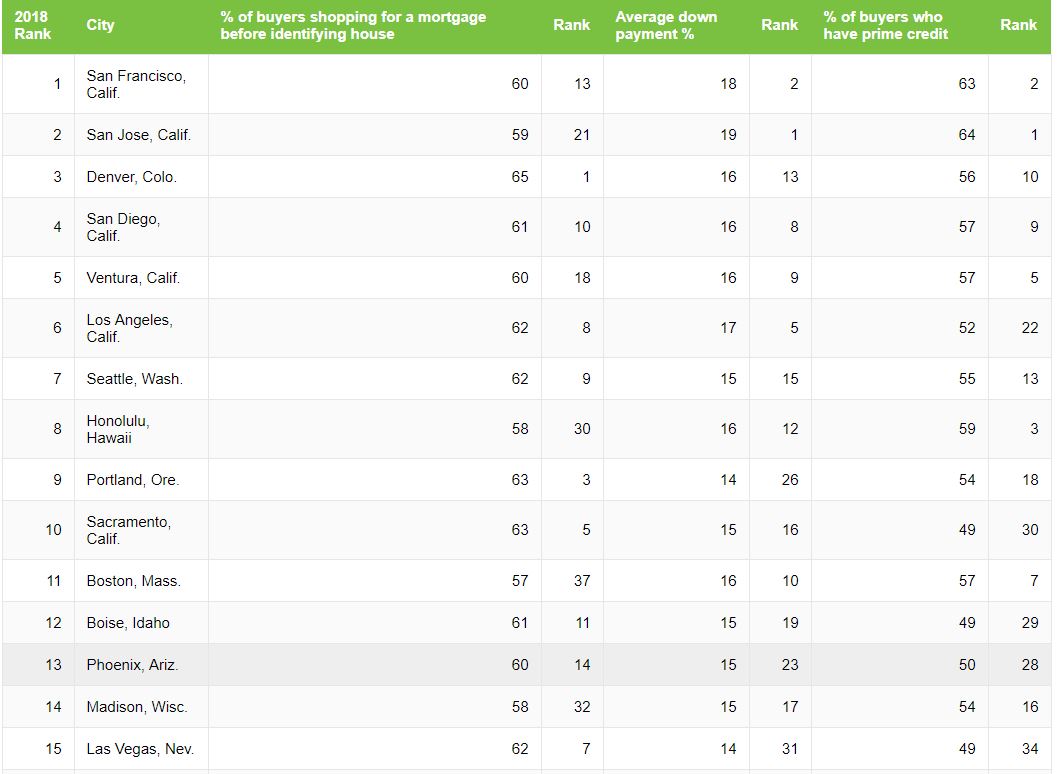

A better competitive gauge would be the number of bidding wars per city, but hard to get a count. Hat tip to Jarrell for sending this in:

In a new study, LendingTree ranked the top 100 Most Competitive Housing Markets based on the factors that truly create a competitive market for homebuyers — how many house hunters are putting more money down, have high credit scores and start loan shopping before home shopping.

We looked at 1.5 million purchase mortgage loan requests that came through the LendingTree marketplace in the 100 largest cities in 2017. Then, we ranked each city based on three criteria:

The share of buyers shopping for a mortgage before identifying the house they want. Buyers with financing in place are more appealing to sellers and can compete with cash buyers. Average down payment percentage. Having a higher amount of money saved for a down payment can enable you borrow more money or be offered a lower interest rate, allowing you to make a stringer offer. Percentage of buyers who have prime credit (above 680). Borrowers with higher scores have more financing options to make more competitive offers.

I sent yesterday’s post to Lawrence – and this was his reply:

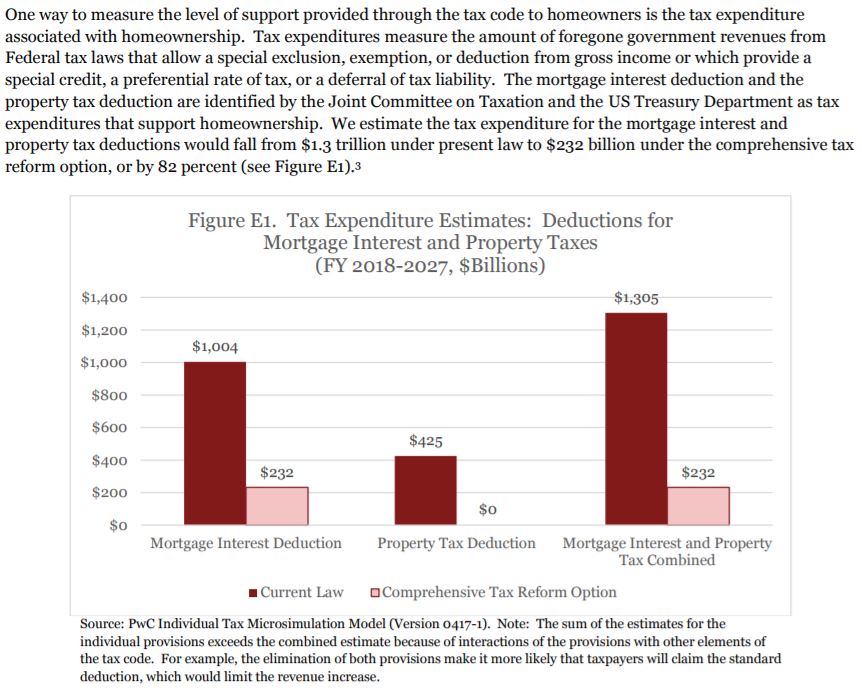

Home values falling 8% to 12% were based on taking away all of the deductions- no MID and no property tax deductions.

Fortunately, MID is set at $750,000 and $10,000 for state and local tax deductions. With these in place in the final tax bill, we have not said of those price declines. Our forecast is for a 2% price gain nationwide. You, nonetheless, bring a good point that there are still many consumers thinking of what we had said earlier. We’ll work in getting the updated info out more aggressively.

I thanked him for his response.

Are potential home buyers going to bother with calculating the specific impact of tax reform, and then not buy a house if they don’t like the result? Or would they spend less on a house?

Californians are used to heavy taxation. I’m guessing they will shrug off a few thousand more in taxes if it means getting the right home.

For those who want to estimate their taxes, and are WSJ subscribers, here’s a basic calculator:

Yesterday I sent a note to the C.E.O. of the National Association of Realtors to counter the idea that home values will be going down 8% to 12% this year. I’ve been asking for two months – show us your math.

Here it is – see link below. They commissioned a study by Price Waterhouse, who used their microsimulation model to determine that demand will drop so severely that home values would tank by 8% to 12%. The study is dated May, 2017, so it’s not based on the final tax reform legislation – they used samples of what they thought it could be.

Here they note that the mortgage-interest deduction would drop by almost $800 billion when the law that was passed had NO IMPACT on the ability of existing homeowners to deduct the same mortgage-interest as they’ve been deducting all along.

They also drop the Property Tax Deduction to zero – which is wrong too.

So Lawrence and the N.A.R. are publicizing the negativity based on an old report from six to twelve months ago that used faulty assumptions.

Great.

The data point I included in my email was the bidding war in Carmel Valley this week on a tract-house listed for $1.2 million that garnered 16 offers. Apparently, the tax reform didn’t impact those buyers the way the microsimulation model expected.

Here’s the email from Lawrence:

Hello Mr. Klinge,

Our CEO shared your note with me, as it mentions my name.

Thanks for sending us the market info on the ground from San Diego. We always appreciate member feedback. We have also heard similar condition of multiple bidding and the lack of inventory in CA coastal cities and in many parts of the country. I will use your comments in my presentations about variations in the country: with upper-end market needing to cut prices in CT and IL and still multiple bidding in San Diego.

We regularly conduct a survey of Realtors® for that exact reason of gauging what is happening on the ground. The latest monthly Realtor® feedback, which we call the Realtor® Confidence Index, is attached. Getting a feel for the market from these 3,000 Realtors® greatly helps me and my staff. I am asking my staff to contact you subsequently to be part of this survey. There is an open-ended question at the end where we delve into issue not mentioned in the questionnaire and comments like yours will be helpful for us to understand what is happening on the ground and to identify “turning points” in the market.

I’m very glad to hear that the tax deductions limit on mortgage interest and property tax appear not to be impacting your market. The strong job market in San Diego is no doubt helping boost home buying confidence. That is not what we are hearing in other markets, however. Here’s a couple news interview of academics. I am attaching a link of Dr. Robert Shiller’s interview with CNBC at a recent NAR event, when he gave talk about the market condition. He, unlike most other economists, does not believe that consumers are always rational. In fact, people are more irrational then rational, in his view. Always interesting to hear his perspective and it’s here:

Most economists would be like Mark Zandi, believing consumers are mostly rational in their behavior, and has called for negative home price impact from limit real estate tax preferences. Here’s Dr. Zandi’s interview with CBS

After taking into account of current market momentum, the job market, local housing starts, interest rate forecast, we have CA home prices rising by only 1% in 2018. It would be presumptuous to imply this NAR forecast will be the reality for 2018. Indeed, CA may experience for the remainder of the year what you are seeing currently. Given that many members have asked for our views for outlook in 2018, and the below forecast is our attempt at that.

One big issue we have been working on is to boost inventory and housing supply. As such we have been working with University of California Berkeley … to boost housing supply and homeownership in a sustainable way. Here’s the paper and my presentation at the University is attached.

Based on Realtor® feedbacks, we know how critical it is to have more inventory. Therefore, my presentations have focused on this issue. I am attaching 2 powerpoint presentations that talks to the great undersupply in CA.

Housing Conference at University of California at Berkeley

Homeownership Conference at HUD, with Dr. Ben Carson presiding.

For day-to-day update on the ever changing market conditions, follow us on social media, along with other 100,000 + fellow realtors®. I am sure you will not agree on all things shown, but it is my hope, some of the info can be used in your business.

Finally, if not already, please consider becoming a major RPAC donor. Many very successful Realtors® like to give their time back to the organization by volunteering and by investing in RPAC to help protect private property rights.