We’re wrapping up the celebration of Kayla’s 25th birthday! (yesterday)

She was born on the day of the 1991 All-Star Game. I got to hold her in my arms and watch baseball on TV from Day One! The game was in Toronto, and Benito Santiago and Tony Gwynn both started for the National League!

How many people have lived in their current residence longer than any other house in their life? I’ll say most. The novelty of moving has worn off, and appreciating what you have is the new orange. Shall we say an equal impact on supply and demand – and drying up both?

Every house on the market for more than 7 days is probably a fixer – sellers should do improvements in advance. Buyers are schooled by HGTV, and want perfection. If you have a superior home in a terrific location, you’ll get offers right away as long as your price is within reason.

The Joys of Homeownership. Whether the home is owner-occupied or a rental, let’s expect to spend $1,000 per month, on average, for repairs and improvements. You can cruise for a few years, but eventually you can expect to replace the furnace, air conditioning, water-heater, dishwasher, and refrigerator every ten years. Carpet, paint, and landscaping every five years. Sure, if you or your tenants don’t mind living in squalor, it’s not a problem. But if you want to sell for top dollar, you need top-dollar improvements.

You can judge the listing agent’s experience by the MLS comments. The market isn’t hot enough that you can bluff me into thinking that your listing is so great that you’ll have multiple offers by tomorrow. Just make it easy to show, would you?

We are overdue for a media onslaught. Any disruption in the positive housing trends are sure to be exploited by national media types. Don’t listen to anybody who doesn’t have on-the-ground examples to back them up.

The ‘Sold before Processing’ listings are of great convenience. There is fantastic efficiency for a listing agent to quickly shuffle a deal into escrow and move on to the next sale, and avoid having to deal with those messy bidding wars.

It seems like Zillow is enthusiastically supporting their big-spending realtors. Zillow needs to go next-level and just openly promote their favorite agents. There will be more lines in the sand to be drawn.

The unstable current events should make you conscious of your home’s security. Do you feel secure at home? Make your home defensible, or consider moving!

Revolution is going to come, so we should take charge. Take the gun issue. Both sides should submit their solution, and a compromise hammered out. Something has to change.

If unrest continues, it is probably good for real estate. More people will buy a house to hunker down – to “cocoon”, and drive demand.

Wondering what to do? Either you can settle at today’s prices, or take your chances during the next spring selling season with the new president!

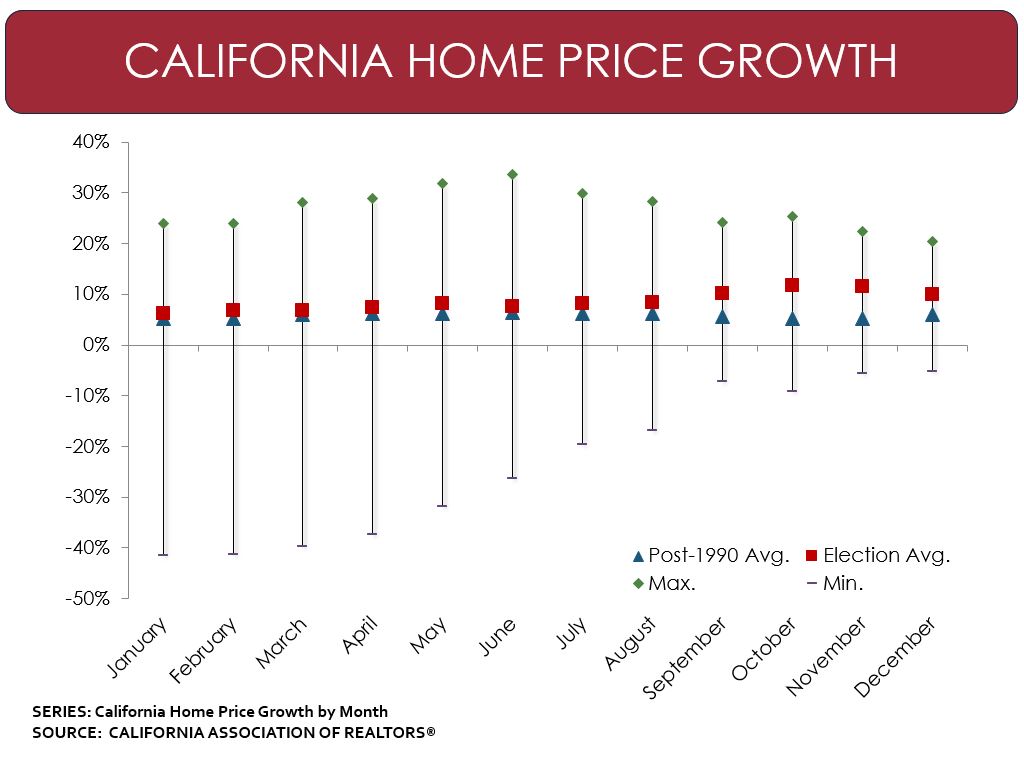

C.A.R. analysis finds presidential elections have little impact on California housing market

Prospective home buyers want current presidential candidates to address housing affordability

Presidential elections have historically had little or no negative impact on the California housing market, according to findings by the CALIFORNIA ASSOCIATION OF REALTORS® (C.A.R.).

“Transitory political events such as presidential elections don’t drive the housing market,” said C.A.R. President Pat “Ziggy” Zicarelli. “Market fundamentals such as housing inventory, affordability, interest rates, job growth, and consumer confidence are the real factors that influence the housing market.”

In an analysis of home sales dating back to 1990, the average growth in home sales during an election year is usually either slightly higher or lower each month than in non-presidential election years. Notably, sales growth is rarely negative during an election year, and there is no evidence of a systematic negative impact on home sales or prices stemming from election season. In fact, C.A.R. found that growth in home sales at the end of an election year actually outperforms non-election years by 7.1 percentage points.

On a monthly basis since 1990, California home sales contracted by roughly 2 percent during the last four months of the year.

However, during the past five election cycles, sales in the final months of the year picked up, rising by 5.3 percent on average compared with -1.8 percent during non-election years. With the exception of December 2004, every single month of the final quarter saw robust growth in home sales during election years.

The pattern for California home prices is similar. C.A.R. also found little evidence of a negative effect on home prices during an election year. In fact, home price growth in California during the past five election cycles was slightly better than the long-run average of 5.6 percent.

The effects were most pronounced during the final months of the year when demand – and therefore, upward pressure on prices – were boosted by roughly 5.6 percentage points following the elections.

and hearing that a buyer just blew out of an offer negotiation due to the seller wanting to replace the washer and dryer with an older set, it’s time for a chat.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

The lower mortgage rates are starting to clog the system with refinancings, and closings are being delayed. Additional volume probably just exposes the weaknesses in each lender’s pipeline, and there isn’t much that they can do to improve it on the fly.

Threats of delays will add to other second-half difficulties:

Can we agree that the more-motivated buyers have already bought a home this year? Those deals go down easier. In the second half – which last year was just as fruitful as the first half – prices are higher than ever. Combine with less-motivated buyers, and it’s tougher to bring deals together.

The buyers’ squeeze for better quality has exhausted the supply. What’s left are more of the inferior houses for sale – and tougher deals.

Those in the business who enjoyed a frenzy-like selling season should consider changing gears. Expect fewer bidding wars, and…gasp…lower offers.

The political circus is a distraction, and a likely reason for buyers to give up and quit looking.

If we can work together to find ways to make, and keep, sales together, the better for all. Mortgage rates in the low-3s should help!

A good way to measure the strength of the spring selling season would be to examine home sales that close in May and June. In spite of medians that have jumped 30% or more in just five years, and a low-end market that has evaporated, sales in May/June of this year were very strong:

NSDCC House Sales, for May/June

Year

# of Sales

Median SP

Median Cost-per-SF

# of Sales Under $800,000

2012

628

$850,000

$317/sf

282

2013

695

$975,000

$372/sf

231

2014

591

$1,000,000

$388/sf

167

2015

623

$1,125,000

$402/sf

138

2016

607

$1,209,000

$419/sf

98

It’s not the low-end that is carrying this market – it is the affluent. It’s why the market will likely keep going – people have more money than houses!

You can also see how difficult it is to downsize. Those who are looking to pocket a big windfall – hopefully the entire $500,000 tax-free amount – will recognize how hard it is to stay around the coast.

Of the 98 sold under $800,000, only 31 of them were single-story!

It’s not easy to downsize, especially into a decent one-story house – there aren’t enough one-story owners who want to sell!

But there are some good opportunities if you are willing to leave the coast. Sell your coastal big bombers and go inland just far enough that you can get a one-story for less, and still be close to the grandkids!

Over the weekend, I spoke with a client who purchased his home five years ago, and has a 4.0% mortgage rate now on a loan amount of $315,000. If he were to refinance, his savings would be roughly $200 per month.

Is it worth it?

It might be worth it if he took out some extra money to buy another house!

Is it worth it to refinance just to lower your payment? If you found a $200 bill on the ground, you’d pick it up, right? If the extra $200 per month would change your lifestyle, then do it.

But I pointed out that he only has 25 years left on his existing loan, and that getting a new 30-year mortgage would add five years of payments if you kept the home for the duration.

The $200 per month savings times 25 years = $60,000 savings. But adding the extra five years means an extra $120,000 in payments (the new payment is about $2,000 per month).

What if you take the new loan and save the $200 per month for 25 years, and then pay off the balance? We looked it up on an amortization schedule, and the balance on the new loan after 25 years was $77,000.

Bankers always win – you may save the $200 per month, but if you kept the home for the duration, it will cost you more in the end.

You need to do a cash-out refinance and spend the money on something worthwhile (like another house!!!), or have the savings be enough to improve your lifestyle. The last survey showed that the average ownership is now 20 years, so don’t take for granted that you will ever sell this house – no matter how much I try to convince you! 😆