We are trying to reach audiences in different places – this will end up on Instagram – but I like playing them here too for those who prefer videos even though we acknowledged last week that the Fed cut is a nothing-burger for now. Every message has it’s own personality though.

Hat tip to Jorge who sent in this interview with Jeffrey Gundlach, the prominent bond trader who speculates with confidence on the Fed’s half-point cut and what it means for the markets. He speaks quite knowledgeably about everything except the future of the housing market, which he called the ‘wild card’ for the economy.

This video starts where he says that he expects another 3/4% Fed cut this year, and then housing:

He said that none of us really know what’s going to happen……but let’s use math to predict the future.

My Theory:

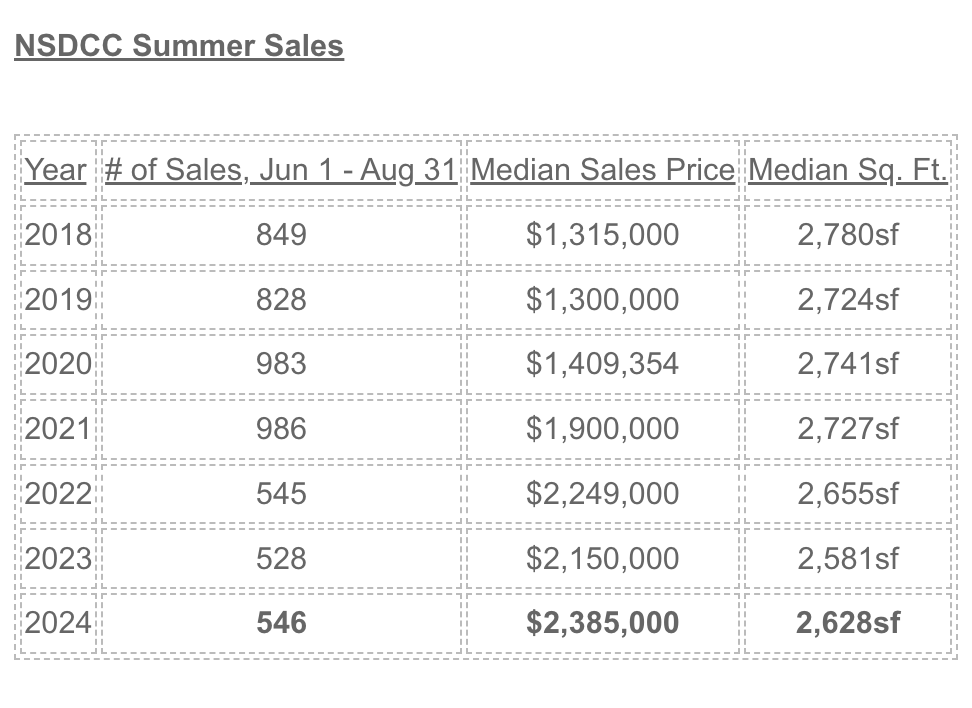

It’s the HIGHER HOME PRICES that are locking in the current homeowners, not mortgage rates.

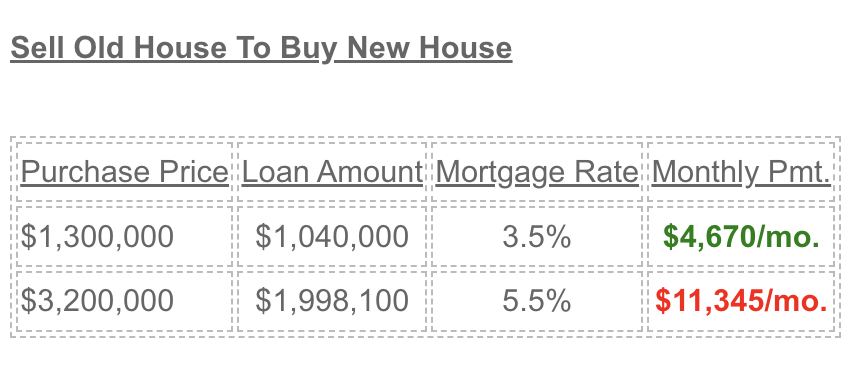

Everyone who bought a home before 2022 is enjoying a bonanza of new-found equity. Let’s use the 2019 buyer for an example. They hit the jackpot to buy a regular home for $1,300,000 back then, and now it’s worth around $2,385,000 – wow, an extra million dollars of equity, just like that!

Some may have a good reason to move, and they are DREAMING about using their same equity, and same mortgage amount to buy up and live with a slightly-higher rate.

But they can’t buy a much-better house for $2,385,000 – they already own a similar-sized house! The old house that was worth $1,300,000 is now $2,385,000. So they have to spend more to make it worth moving.

My rule-of-thumb is 50% more, or $3,577,500.

But let’s say that they work with a really sharp, experienced realtor and find a home that makes it worth moving for $3,200,000 and use ALL of their equity from the old house after closing costs:

Let’s also point out that in California the property taxes would go up an additional $1,742 per month, so the $11,345 + $1,741 = $13,086 MORE PER MONTH to move to a better home in the same area. Even if rates were to drop to 3.5%, the combined P&I+T = $10,713 per month.

“You’re killing me, Jim – aren’t there any other alternatives?” Yes, there are two:

Buy a smaller, crappier house in the same area.

Move out of town.

That’s it, or throw down another $1,000,000 in cash to keep the loan amount down where it was.

What does it mean for the 2025 market?

Mortgage rates should be lower than they are today, and probably in the mid-5%s. There will be a new president, and all the wait-and-see buyers who were determined to see the Fed cut rates before venturing out again will be storming the streets en masse. Those first-time buyers and out-of-towners are used to these prices now and will succumb.

What about the supply? We will have a similar number of deaths, divorces, and job-transfers (The Big Three) who always sell every year. Will those who bought a home since 2022 who made a mistake and bought the wrong house be motivated to sell? Not unless they can buy something at least equal or better – the ego can’t take a step down, so they may just refi to a lower rate instead.

But those who already own a house here will appreciate it even more, because once they look around, they will realize that their existing home will have to last them forever – they’re not moving!

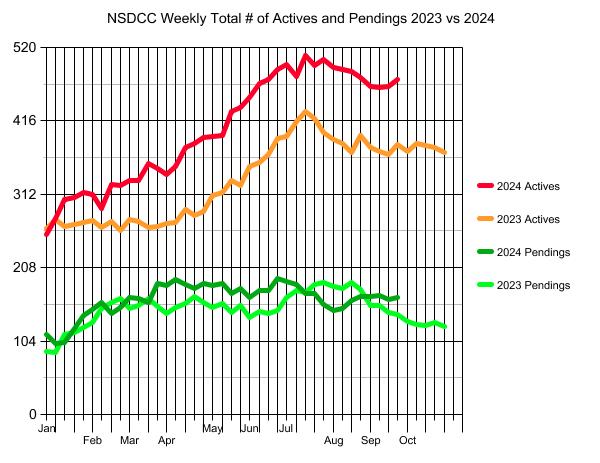

Statistics are quirky – there are always things that happen that defy explanation. Look at the uptick in inventory in today’s reading, and note that the same thing happened last year!

The number of pending listings has been riding above last year’s pendings count, which is interesting.

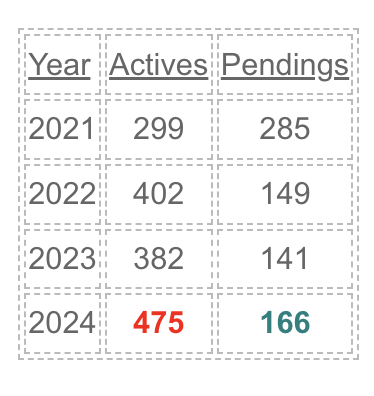

Having more actives could trigger a wait-and-see feeling in buyers, but there should be some tolerance because the inventory has been so much lower than ever before. It appears that having 24% more active listings still falls into the tolerable category because the number of pendings is higher today:

NSDCC Actives and Pendings, Last Week Of September

The 475 actives sounds like a boatload compared to the last three years, but instead of being scared off, buyers are just ignoring the 174 that have been on the market for more than 60 days.

The entry-level homes have kept, or exceeded their value from the frenzy. Generally speaking, it takes $2,000,000 or more to buy a decent house between La Jolla and Carlsbad today.

What about higher up?

It was at the peak of the frenzy in early 2022 that three homes sold in ‘The Ranch’ in Carlsbad, a tract of large homes on half-acre lots next to Olivenhain built by Centex in the early 2000s.

This one got the party started when it closed for $4,200,000, which was $1,000,000 over its list price:

Here’s what has happened since (and the active listing was refreshed after 186 days):

It looks like $4,000,000 is still a stretch in today’s market.

While the July closing of $3,500,000 made it look like the comps were approaching $4 million again, then the same-sized house closes for $3,225,000 last week, thwarting the momentum.

Here’s how it looked:

At Encinitas Ranch, my record sale of $3,760,000 in November, 2021 is still holding up as the highest-priced sale of the tract homes. There was another sale of a home for the same price in 2022 that was 1,000sf larger than mine, but none higher since – this pending probably won’t get there either.

Lower rates may infuse more curiosity into the real estate market, but buyers will still be cautious now.

In what might be the biggest news of the year for us, daughter Kayla has joined the Compass family in New York City! Because she still has her California real estate license, she has also joined us at the Klinge Realty Group, making KRG bi-coastal!

A few other agents from her previous brokerage also went to Compass, making the transition a little easier, plus Robert Reffkin called her personally to welcome her and spent 3-4 minutes discussing her future!

The succession plan is for Kayla to run the NYC operation, and for Natalie to take over here.

We are thrilled to have Kayla back working with us!

If you or someone you know is thinking about buying or selling in Manhattan, let Kayla know!

Ringo at Humphrey’s with Steve Lukather (Toto) on guitar on stage right, and Hamish Stuart (Average White Band) and Colin Hay (Men at Work). Incredible show – they played all the hits, and it would be worth it to see any one of these guys play with their former band. Average White Band and Men at Work have future dates scheduled!

This is the only venue in San Diego that Ringo is willing to play, in spite of those who float up in their boats and kayaks to see a Beatle perform for free. I told Donna that Ringo will have something to say to the freeloaders, and sure enough, he did.

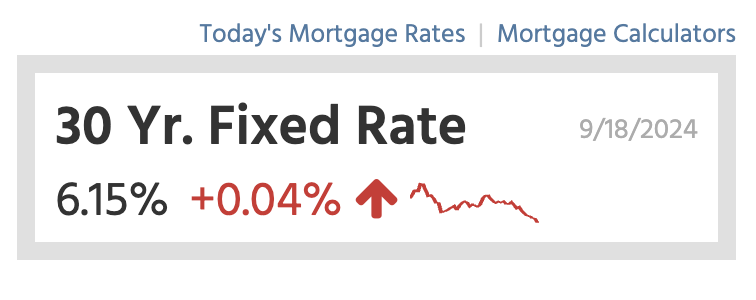

We publish daily coverage of mortgage rate movement and have done so for nearly 20 years now. It’s a great place to quickly check in on rate trends and to get a sense of what’s true and what matters.

If you’d been checking in at any point in the past few days/weeks, you likely saw one of several attempts to remind readers that today’s Fed rate cut not only had absolutely no implication for lower mortgage rates, but indeed that mortgage rates have often moved higher on the same day that the Fed cuts.

That’s what happened today.

Interestingly enough, mortgage rates were already slightly higher than yesterday BEFORE the Fed announcement came out. The bonds that dictate mortgage rates are actually pointing to even higher rates tomorrow unless there’s a decent improvement overnight.

It is smart for realtors to tell their buyers that lower rates in the future are unpredictable, and buying the right house at the right price is much more important. Also, any future rate improvement will be noticed by home sellers too, and they will want to push pricing – offsetting any benefit to buyers.

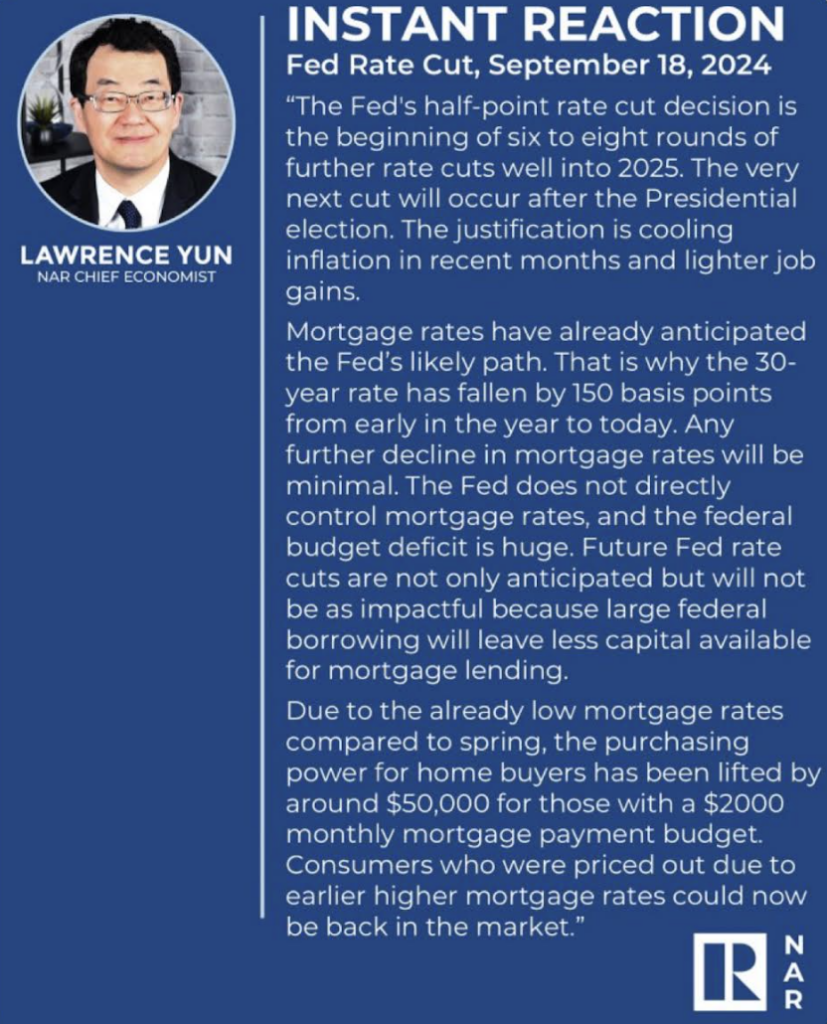

So the realtor industry should unite in our message to buyers about not waiting for…………..oh crap, here’s our head cheerleader telling buyers there will be six to eight rounds of further rate cuts!

Larry, Larry, Larry you’re supposed to be on our side!

The new rules don’t allow the MLS to publish on active listings how much buyer-agent commission is being offered by the seller and listing agent. But in a strange quirk, the CRMLS – the biggest MLS in California covering about half of the state – now requires that when marking a listing sold, the listing agents have to publish how much compensation was paid to the buyer-agent.

Since August 17th, there have been 173 NSDCC closed sales, and 54 of them published the buyer-agent compensation paid (CRMLS and SDAR are the competing associations/MLS companies in the county, and SDAR doesn’t require these stats from listing agents).

Of the 54 sales who published the amount paid, here is the breakdown:

2.5%: 25(46%)

2.25%: 4(7%)

2.0%: 20(37%)

1.5%: 2(4%)

1.0%: 1(2%)

Zero: 1(2%)

This is roughly the same mix that we’ve seen since April when I first started logging the commission rates being offered by the listing agents. We will follow this trend because buyers deserve to know the chances of them having to pay some or all of the commission to their buyer-agent.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

I have every intention of persuading the seller and listing agent to pay my buyer-agent fee.

In the event that we get stuck with an unreasonable seller/listing agent who insists on paying little or nothing – and the buyer doesn’t want to pay either – then I’m not going to hold you to it. I’m going to turn you over to the listing agent and bow out gracefully, if you don’t mind, because Donna doesn’t work for free (she plugs in once we have an accepted offer).

Why would I be willing to work for free for weeks or months? Because that risk has always been part of the buyer-agent environment – historically, we have always risked spending our time without any promise of getting paid. It’s the main reason why we deserve good compensation – it is risky. I will take my chances that I can get the seller and listing agent to come around, and/or have the buyer recognize and appreciate our services enough that I’ll get paid. If not, then fine.

Trustindex verifies that the original source of the review is Google.

We sold a home with Jim and Donna and from beginning to end they were consummate professionals. Their initial walk through the property resulted in a list of items to be repaired or updated. They supplied a list of vendors and job quotes to do the repairs and updates. We originally wanted to sell ‘as is’ and just get it over with. They gave us a selling price for ‘as is’ and options for doing a few updates/repairs to doing it all with the selling price for each option. We agreed to do all they suggested and we sold for the exact price they predicted. For every dollar spent we got back more than $2 back in the selling price. And they got that price in a rising interest rate environment! Donna and Jim are extremely detailed and guide you through ever aspect of the sale. There were no surprises thanks to their guidance. We couldn’t be more pleased with their representation.

Thank you Donna and Jim,

Jerry and Mary

Heather Quejada

March 27, 2025

Trustindex verifies that the original source of the review is Google.

We have known Jim & Donna Klinge for over a dozen years, having met them in Carlsbad where our children went to the same school. As long time North County residents, it was a no- brainer for us to have the Klinges be our eyes and ears for San Diego real estate in general and North County in particular. As my military career caused our family to move all over the country and overseas to Asia, Europe and the Pacific, we trusted Jim and Donna to help keep our house in Carlsbad rented with reliable and respectful tenants for over 10 years.

Naturally, when the time came to sell our beloved Carlsbad home to pursue a rural lifestyle in retirement out of California, we could think of no better team to represent us than Jim and Donna. They immediately went to work to update our house built in 2004 to current-day standards and trends — in 2 short months they transformed it into a literal modern-day masterpiece. We trusted their judgement implicitly and followed 100% of their recommended changes. When our house finally came on the market, there was a blizzard of serious interest, we had multiple offers by the third day and it sold in just 5 days after a frenzied bidding war for 20% above our asking price! The investment we made in upgrades recommended by Jim and Donna yielded a 4-fold return, in the process setting a new high water mark for a house sold in our community.

In our view, there are no better real estate professionals in all of San Diego than Jim and Donna Klinge. Buying or selling, you must run and beg Jim and Donna Klinge to represent you! Our family will never forget Jim, Donna, and their whole team at Compass — we are forever grateful to them.

Lou F

March 27, 2025

Trustindex verifies that the original source of the review is Google.

WeI had the pleasure of working with Klinge Realty Group to sell our home in Carmel Valley, and I cannot recommend them highly enough!

Jim and Donna demonstrated exceptional professionalism, offering expert guidance on market conditions and pricing strategy, which resulted in a quick and successful sale.

Communication was prompt and we were well-informed throughout the entire process.

For anyone looking for a dedicated and knowledgeable real estate team, look no further!

---

William Sams

March 25, 2025

Trustindex verifies that the original source of the review is Google.

Donna and Jim Klinge of Klinge Realty Group have our highest possible recommendation. From Donna and Jim’s first visit to our house through closing their advice and counsel was candid and honest in all dealings. They kept us fully informed throughout the process. The house sold less than three days after listing with a two-week closing. My wife and I have sold several houses during our lives. This was by far the best experience. Klinge Reality is a premium service realtor. You can’t make a better choice for someone to sell your home fast and for top dollar.

Emily Hernandez

December 29, 2024

Trustindex verifies that the original source of the review is Google.

Donna and Jim provided exceptional support and professionalism throughout the entire process. We couldn't have been happier with their efforts. They made our house shine, and thanks to their expertise, it sold above the listing price in the very first weekend! Truly a fantastic experience from start to finish.

Jesus Adrian Sahagun

November 11, 2024

Trustindex verifies that the original source of the review is Google.

This year has been difficult on our family, mainly due to having to sell our home. Thankfully we knew God had a plan for us and working with the Klinge team was a key part of it. It was an obvious decision to work with them again after such an amazing experience when purchasing the same home we needed to sell. The challenge was, how will we do this in so little time with so much going on? Jim and Donna held our hand every step of the way. Whenever an unexpected issue arose they found and provided a solution. Never once did we feel pressured to make a decision and the Klinges were always reassuring after providing the information that the decision was ours to make. Despite the curve balls, they never panicked and exemplified the “can do” attitude, making us feel optimistic and taken care of. Their expertise and professionalism was superb. But of all the reasons to work with the Klinges, the most impactful and valuable is their compassion and genuine care for their clients. We pray that we can one day purchase our forever home and you better believe that Jim and Donna will be representing us - as long as they will have us of course. Thank you again Klinge team! Your execution, experience, and care are unmatched.

SABIHA PASHA

July 23, 2024

Trustindex verifies that the original source of the review is Google.

Jim and Donna were fantastic! Jim understanding my needs, recommending potential places, pointing out the pros and cons of each property was invaluable. Then when the offer was accepted Donna’s organized guidance through the inspections, paperwork etc made the whole process seem effortless.

So grateful that I had them on my side!

Anu Koberg

July 13, 2024

Trustindex verifies that the original source of the review is Google.

We first found Jim through his blog at bubbleinfo.com, which really showcased his knowledge of SoCal real estate. Since then we've done three transactions with Jim and Donna, and they are an incredible full service agency, with Jim's deep market insight and Donna's deft contract and project management. We trust them implicitly in their analysis and strategy, which is based on years of experience. They're always available and on top of things, and we strongly recommend them to anyone.

Bjorn Isachsen

July 10, 2024

Trustindex verifies that the original source of the review is Google.

The Good

The Klinge Realty Group operates like a finely tuned machine, with a very personal touch. We contacted them on a Sunday and they were talking to us about our family and our needs on our living room couch the following day. They carefully listened to us and worked with us to identify the best and quickest path to listing within 2 weeks to take advantage of the low inventory conditions in our South Carlsbad neighborhood. They knew our tract specifically and had many previous sales there over the years - they came prepared with a thorough analysis of comparative sales and recommended a pricing strategy that they felt confident would yield offers the first weekend on the market.

The Great

Over the next two weeks Donna coordinated a range of vendors who she knew from experience could get the preparation to list work we needed done on time and with high quality. Our light tune-up involved excellent experiences with their stagers, landscapers, contractors, electricians, and plumbers. Throughout this period Donna's daily communication was clear, concise, and responsive. Any time we had questions Donna picked up the phone or texted immediately - but almost always, she answered our questions before we even knew we had them.

The Outstanding

We had a tricky situation with a shared fence that could have delayed our escrow. Donna used superb mediation skills to negotiate the terms of replacement and was personally on site with the fence contractor to make sure everything went smoothly. The fence looks great and escrow closed on time.

The Truly Exceptional

Our house came on the market on a Wednesday and between then and Monday morning Jim was personally at all three open houses. He was in constant communication explaining potential buyer reaction and strength. As he predicted offers began to come in on Saturday and each one was incrementally higher than the last. At the end we had 5 offers, 4 of which were over list, and the final accepted offer was $100,000 over list. In addition to being over list it included rent back terms that met our needs.

The Recommendation

For all of these reasons we would strongly recommend The Klinge Team to anyone wanting to sell in North County Coastal San Diego. I had been reading Jim's bubbleinfo.com blog for 15 years and knew when the time came to sell that he would be our first call. Jim Klinge is not your standard realtor. He is keenly aware of market conditions and sales strategies. And, works his tail off - though not as hard as Donna . At this point he's gone from realtor to friend and I plan to have him over to grill and chill at our new place to talk real estate, but also just about life and raising kids in San Diego. He's more interested in relationships than his sales numbers - and that's why his sales numbers are so high. We have already recommended the Klinge's to some close friends and another successful sale is on deck right around the corner...

Chris Shea

June 21, 2024

Trustindex verifies that the original source of the review is Google.

We recently had the pleasure of working with Jim and Donna from Klinge Realty Group to sell our house, and we couldn't be more satisfied with the experience. From the initial meeting, they listened attentively to our needs and provided invaluable guidance on specific improvements to get our home market ready.

Their responsiveness throughout the entire process was truly impressive. Anytime we had questions or concerns, they were quick to address them, ensuring we felt comfortable and informed every step of the way. What stood out the most was their team and extensive network of tradespeople, which made addressing any necessary repairs or updates seamless and stress-free.

Thanks to their expertise and dedication, our house sold quickly and at a great price. We highly recommend Jim and Donna to anyone looking to buy or sell a home. They are a fantastic team who truly care about their clients and deliver exceptional results.