The thing I think you miss most or maybe overlook is how overleveraged the average person is. I do commercial real estate and routinely have access to small business owners financials. Equity rich in their homes but cash poor with credit card debt and car loans up the wazoo. Any bump in the road will send them into disarray. Selling the house may be the only way they can survive. I think rocky times ahead.

We can speculate about what might be or what could happen, but in the end we’re all just guessing. Blog reader ‘Another Investor’ believes the opposite – that boomers are flush and not moving until they go feet first…..so we have balance here at bubbleinfo.com!

Let’s use statistics to help guide us.

If there were trouble brewing, then more people would be trying to sell.

Not everyone would sell, because their motivation might not be strong enough to take what the market would bear. So let’s just consider the number of listings – and also consider that there are probably more re-lists now than ever:

NSDCC Total Number of Listings Between Jan-Oct:

Year

# of Listings

2014

4,278

2015

4,583

2016

4,698

2017

4,248

2018

4,389

2019

4,327

Boomers or others aren’t trying to sell any more than they used to – so no obvious surge yet.

But the number of cash-out refinances was somewhat alarming yesterday. But everyone has to qualify for those mortgages, so even if more people are tapping their equity, they must be able to afford it.

But like Eddie89 said, the rules have changed, so all previous assumptions don’t apply.

I think any distressed homeowners will wait until the very end before deciding to sell because they really don’t want to move. It will drag out the inevitable, but it might just cause a softer landing because each homeowners ability to last longer will vary.

Let’s keep an eye on the number of new listings – that’s where you’ll see it first!

I went to the annual seat shuffle at Petco Park on Tuesday. It’s the event where Padres season-ticket holders can see which seats have become available, and possibly switch to a better location.

It reminded me of our local real estate market:

The best locations are owned by seniors who have had them for a long time, and they’re not giving them up!

There were some decent seats available, but very few of the prime seats up close.

Old-timers discussing their future mirrored what I hear about their real estate too. Some have a specific succession plan where, upon their death, the kids will take over the tickets, but there were others who mentioned that their kids are out-of-town, and have no interest.

Will there be a time when a load of great tickets become available?

Just like we’ve seen in real estate, probably not.

But you don’t need every senior to bail – all you need is one old couple to give up their prime spot!

Visitor’s clubhouse

Here’s a 33-second look at how few of the good seats were available:

I was talking to Nick yesterday about the current market conditions, and how home sale have been affected by the low mortgage rates recently.

You can see in the graph above that over the last five years we’ve been accustomed to rates in the threes, so it seemed obvious that when rates almost hit 5% that a market slowdown was in order.

Likewise, wouldn’t sales pick up as rates came back down?

But interestingly, in another statistical quirk, sales this year are the same as last year:

NSDCC Detached-Home Sales, August 15th – October 15th

Year

# of Sales

Avg $$/sf

Median SP

Median DOM

Sept 30yr Rate

2016

579

$517/sf

$1,199,000

28

3.46%

2017

528

$542/sf

$1,225,000

26

3.81%

2018

484

$570/sf

$1,330,000

26

4.63%

2019

484

$604/sf

$1,387,500

27

3.61%

Last year when sales were plunging 8% (again), it was easy to blame it on the higher rates. But as rates settled down this year, the best we can say is that sales have flattened out.

Reasons:

Higher pricing is offsetting the lower rates.

Buyers expect rates in the threes. Rates would have to get into the 2s to create a surge now.

Not many homes for sale provide a compelling value to buyers (either the house or price is wrong).

The lower rates this year have provided that mythical soft landing that no one thought was possible. It is giving sellers and agents a sense of security that higher prices are supportable. But wouldn’t rates have to keep going down further for prices to go any higher?

If rates and pricing stayed about the same, the market should plateau along.

But can sellers resist adding that extra 5% on top of the last sale comp? Probably not.

We’ll need an Election Year Miracle for prices to keep rising in 2020!

When you drive around older neighborhoods, you see homes in original condition or in a state of disrepair, which are signs of senior homeowners. It makes you think, “They should sell and move – are they just waiting around to die?”

The answer is YES, and it’s because of how the IRS taxes the gain from the sale of your home. Once a property is inherited, the tax basis is stepped up to fair-market value.

The basis of property inherited from a decedent is generally one of the following.

The FMV of the property at the date of the individual’s death.

The FMV on the alternate valuation date if the personal representative for the estate chooses to use alternate valuation. For information on the alternate valuation date, see the Instructions for Form 706.

The value under the special-use valuation method for real property used in farming or a closely held business if chosen for estate tax purposes. This method is discussed later.

The decedent’s adjusted basis in land to the extent of the value excluded from the decedent’s taxable estate as a qualified conservation easement. For information on a qualified conservation easement, see the Instructions for Form 706.

If a federal estate tax return doesn’t have to be filed, your basis in the inherited property is its appraised value at the date of death for state inheritance or transmission taxes.

For more information, see the Instructions for Form 706.

Appreciated property.

The above rule doesn’t apply to appreciated property you receive from a decedent if you or your spouse originally gave the property to the decedent within 1 year before the decedent’s death. Your basis in this property is the same as the decedent’s adjusted basis in the property immediately before his or her death, rather than its FMV. Appreciated property is any property whose FMV on the day it was given to the decedent is more than its adjusted basis.

Community Property

In community property states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin), married individuals are each usually considered to own half the community property. When either spouse dies, the total value of the community property, even the part belonging to the surviving spouse, generally becomes the basis of the entire property. For this rule to apply, at least half the value of the community property interest must be includible in the decedent’s gross estate, whether or not the estate must file a return.

For example, you and your spouse owned community property that had a basis of $80,000. When your spouse died, half the FMV of the community interest was includible in your spouse’s estate. The FMV of the community interest was $100,000. The basis of your half of the property after the death of your spouse is $50,000 (half of the $100,000 FMV). The basis of the other half to your spouse’s heirs is also $50,000.

For more information on community property, see Pub. 555, Community Property.

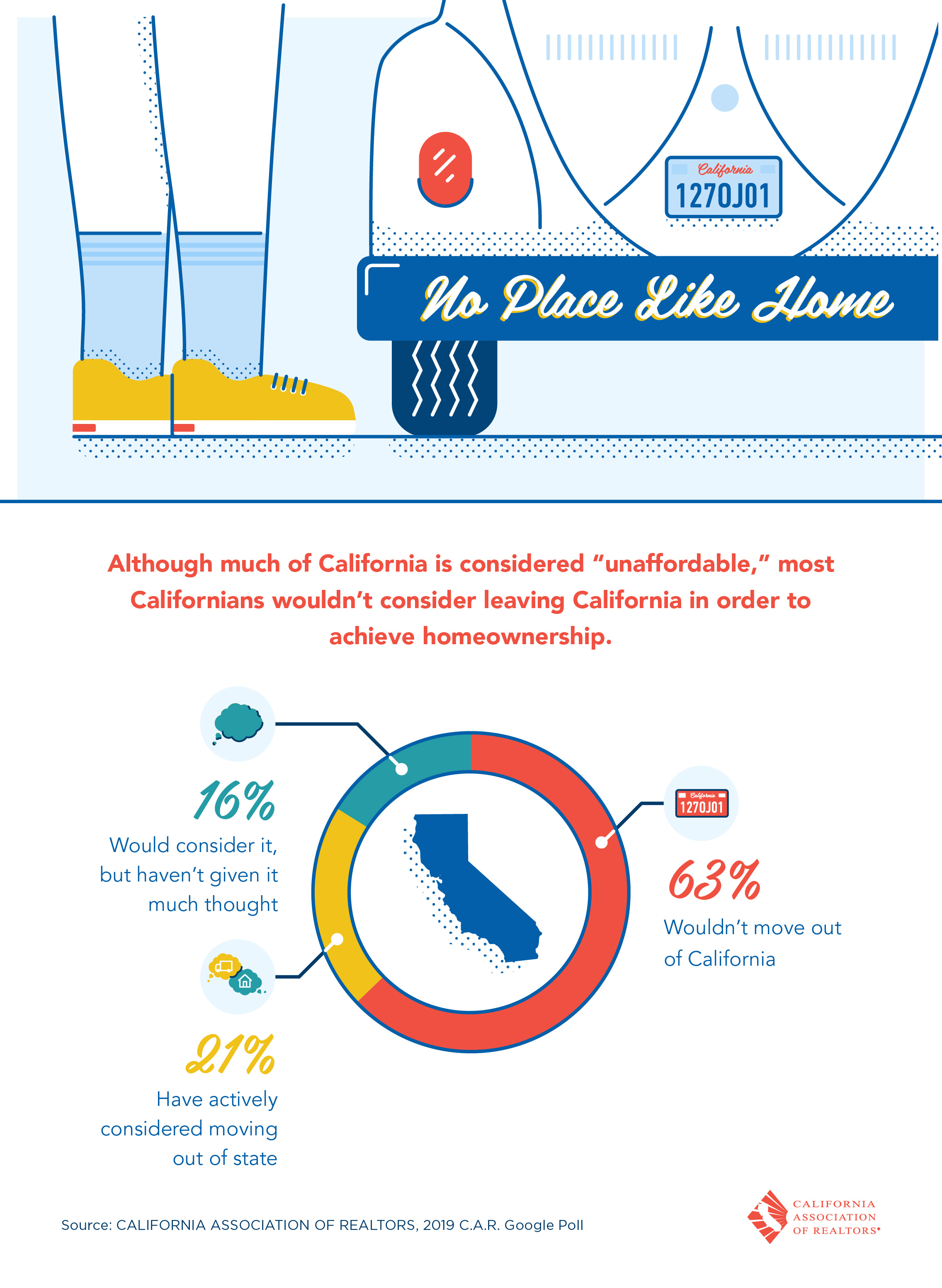

Baby boomers in full control of the market, and very few have a reason to sell. In fact, the list of reasons NOT to sell is so long that you can’t help but have a personal favorite that keeps you in limbo:

1. I don’t need the money.

2. The grandkids are here.

3. My low property taxes have me locked in.

4. My low mortgage-interest rate has me locked in.

5. Everything else is too expensive.

6. I don’t want to leave the city/state.

7. My parents might move in.

8. My kids might move in.

9. My kids need to inherit because they can’t afford a home.

10. I don’t want to pay capital-gains (on more than the $500K).

11. I got a reverse mortgage.

12. I love it here!

13. Waiting for the market to peak.

Yet we don’t have an inventory problem – heck, there are 1,005 houses for sale in North SD County’s coastal region (La Jolla to Carlsbad).

To buy one, you need to have some horsepower – the median list price is $2.25 million. But at least it looks like higher-end pricing has slowed:

First-half stats for homes priced over $2,000,000:

Year

Jan-Jun # Listings

Median LP

Jan-Jun # Sold

Median SP

2013

628

$2,998,000

203

$2,620,000

2014

646

$3,197,438

218

$2,776,000

2015

712

$3,250,000

252

$2,820,500

2016

856

$3,092,500

257

$2,754,000

2017

805

$3,100,000

293

$2,749,000

2018

862

$3,098,000

312

$2,645,000

2019

898

$2,995,000

298

$2,694,000

Has the higher-end market peaked? Compare this year to 2013.

It could be that egos are causing homes that are really worth $1.7-$1.9M to slip up into the $2M+ range, which would skew the median prices lower. But the sales have leveled off over the last three years, in spite of more choices. More listings but fewer sales keeps the pressure on pricing.

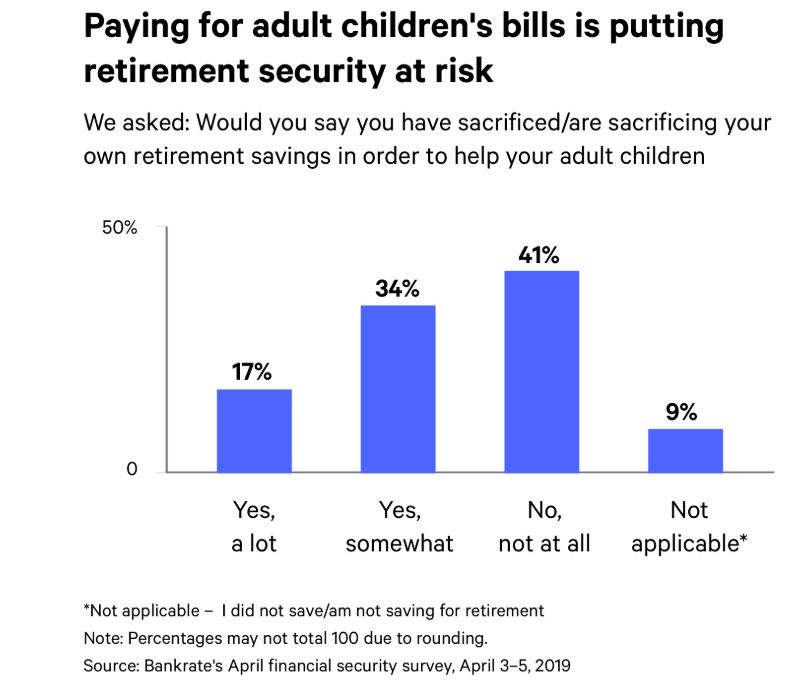

We were talking with some friends last night about how much financial support is going towards kids, and how it will affect real estate in the future.

On one hand, it’s the Bank of Mom and Dad, and helping to keep the market afloat when funding home purchases at these lofty prices for those kids with regular jobs.

However, for those kids who never get to the point of financial stabilization, the selling of the parents home will become the lottery ticket to solve their money issues.

I suggested that this is where the ibuyers could do the most harm by taking advantage of people who want and need a quick sale and who aren’t that familiar with the values.

When we were in Las Vegas for that one-day vacation, I saw more than one ibuyer ad on TV, and they were very enticing. The kids who have been strapped for years and then inherit their parents’ house might jump at the chance to get their hands on quick money – and likely leave some on the table.

Will anyone step up to protect the unsuspecting? A new challenge/opportunity for realtors!

“Since last year, several forces have helped increase the market potential for existing-home sales,” said Fleming. “House-buying power, driven by falling mortgage rates and rising household income, contributed to a gain of 183,000 potential home sales compared with one year ago. Compared with May 2018, rising house prices also contributed positively, increasing the market potential for home sales by 41,000.

“Additionally, loosening credit standards boosted the marketing potential for home sales by more than 60,000 sales over the last year. Some modest growth in new-home construction also added 1,000 potential home sales,” said Fleming. “Finally, the growth in household formation, as millennials continue to form households, contributed nearly 81,000 potential home sales compared with a year ago. Despite all the positives, the market potential for home sales remains nearly 80,000 units below the level of a year ago.”

Unprecedented Homebody Era is Here

“Collectively, the aforementioned market forces contributed to a positive gain of 366,000 potential home sales, but it was not enough to offset the loss of 446,000 potential sales due to the impact of rising tenure. The average tenure length, the amount of time a typical homeowner lives in their home, has increased dramatically in the last year,” said Fleming. “Since existing homeowners supply the majority of the homes for sale and increasing tenure length indicates homeowners are not selling, the housing market faces an ongoing supply shortage – you can’t buy what’s not for sale.

“Before the housing market crash in 2007, the average length of time someone lived in their home was approximately five years. Average tenure length jumped to seven years during the aftermath of the housing market crisis between 2008 and 2016,” said Fleming. “The most recent data shows that the average length of time someone lives in their home reached 11.3 years in May 2019, a 10 percent increase compared with a year ago.

“Two trends are driving the increase in tenure length. The majority of existing homeowners have mortgages with historically low rates, so there is limited incentive to sell if it will cost them more each month to borrow the same amount of money from the bank,” said Fleming. “While mortgage rates have come down compared with last year, they are still below the 3.5 percent mortgage rates of 2016.

“The second trend influencing tenure is seniors aging in place. A recent study from Freddie Mac shows that if seniors and adults born between 1931-1959 behaved like earlier generations, nearly 1.6 million housing units would have come to market by 2018,” said Fleming. “Improvements in health care and technology have made aging in place easier, which has meant fewer homes on the market.

“So far in 2019, the market potential for existing-home sales has benefited from lower mortgage rates and rising household income, all contributing to stronger house-buying power,” said Fleming. “Surging consumer house-buying power coupled with rising household formation has resulted in strong demand for homes.

“Yet, today, we are in an unprecedented homebody era as many existing homeowners continue to feel rate-locked into their homes and seniors continue to age in place. Looking ahead, more than half of all existing-homes are owned by baby boomers and the silent generation and they will eventually age out of homeownership,” said Fleming. “But right now, housing supply remains tight – you can’t buy what’s not sale — and market potential is lower because of it.”

Twenty percent of Americans is a good-sized group, and with the cost and difficulty of senior care being so high, it is natural for more people to consider multi-generational living. Home sellers who can present their home as multi-gen friendly could really benefit.

PNC is one of several banks and lenders paying more attention to “the sandwich generation,” people with dependent children and with elderly parents for whom they need to care. While not everyone in the sandwich generation has parents living with them, it is a growing phenomenon: Today, 20% of Americans live in multigenerational homes, where at least two adult generations live under one roof, accounting for 64 million people. In 1980, only 12% of Americans lived this way, according to the Pew Research Center.

“This has been on our radar for the last couple of years,” said Todd Johnson, Wells Fargo Home Lending’s Division Sales Manager, Pricing and Products Lead. In January, Wells Fargo lowered the down payment requirement for duplex buyers to 5% from 15% to 20%. This program is only available for loans that conform to Fannie Mae and Freddie Mac guidelines, but Mr. Johnson noted that loan limits for duplexes in costly areas can be relatively high.

For example, in San Diego a conforming duplex loan can reach $883,300, and in San Francisco, $930,300, Mr. Johnson said. Such loans can have as many as four borrowers, so a couple plus a set of elderly parents can all take out the loan together, Mr. Johnson said.

The program, however, comes with homework: It requires borrowers to take a four- to six-hour online course about being a landlord. What if your own mom and dad are going to be your tenants? You’ve still got to take the class, Mr. Johnson said. It covers issues such as getting insurance and landlord deductions and depreciation.

A common approach is for the older couple to sell their own home and use the equity to help make the down payment on the multigenerational home.

If a loan doesn’t allow gift funds to be used as a down payment, Ms. Graziano said, “the older couple may need to become a co-borrower on the mortgage loan as well as an owner named on the title to the property.”

When those older parent co-owners pass away, it can get complicated, especially if the parents have other heirs, says Ms. Graziano. “It may require refinancing the property to cash out the [parents’] equity, or selling the property.” For loans that PNC Bank treated as a single-family home at origination, the borrowers can rent out their extra unit to someone else without penalty if renting parents die or move, Mr. Boomer said.

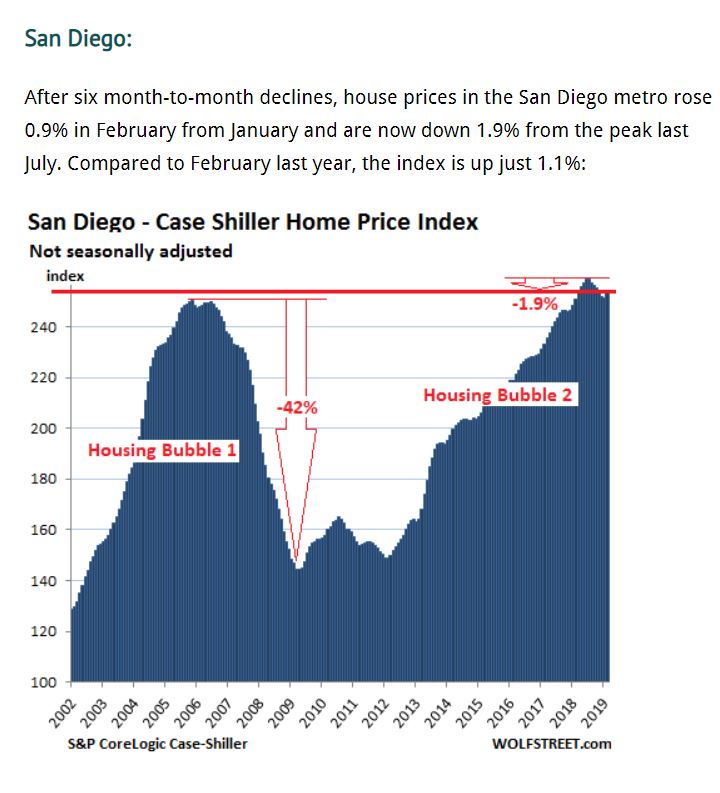

More doomer talk at Wolfie’s, though he doesn’t say much other than some slight skittishness in the Case-Shiller Index equates to home prices going down – click here for 131 comments:

He should consider the dearth of home sellers who would sell for any price. Other bubbles have popped by banks giving away properties, but now that foreclosures got phased out and mortgage delinquencies are at all-time lows, who is going to cause a crash?

It’s much more likely that our market will stall/plateau, with the worst-case being a gradual decline over several years/decades. I think other factors besides price will play an increasing role in the decision-making too, where well-located newer one-story homes continue to be very popular.

It will fracture the market further, where dumpy old two-story tract houses will need flippers to revive them while trendy new homes sell for a premium. Newer condos closer to work are more desirable to many buyers than the older SFRs way out in the burbs.

Market statistics will become less reliable than ever.

Interesting to note that of all the metro areas he features in his article, San Diego had the lowest increase over the previous peak. Others like Dallas and Denver are 50% above their previous peak!