Good to see the California crash of the early 1990s get a mention here. It was a hum-dinger for its time – but they note below that the full recovery only took eight years too.

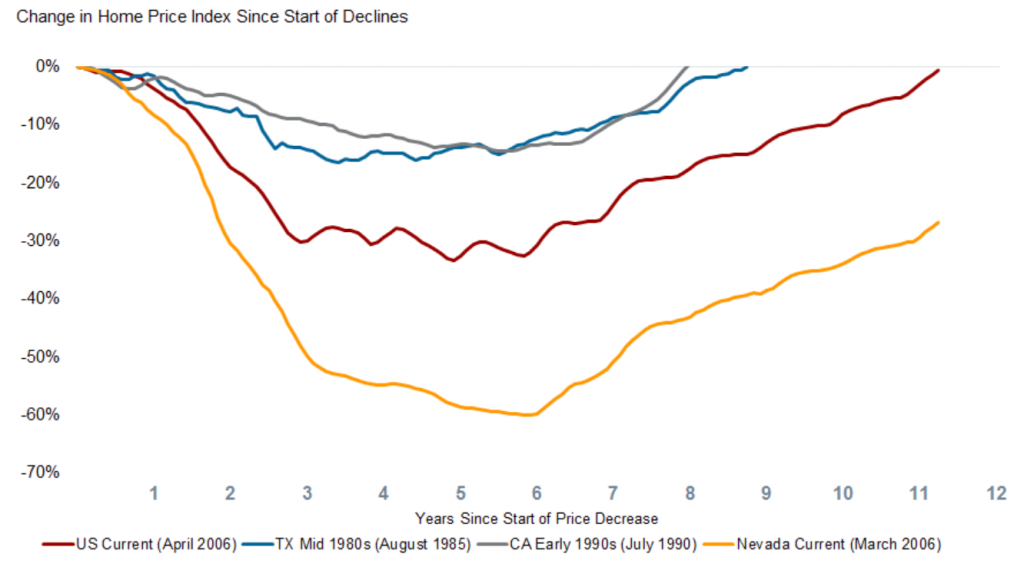

With home prices nearly back to where they were when the housing crisis began, CoreLogic’s principal economist Molly Boesel compares the duration of the recent cycle to those of other downturns. While there hasn’t been a comparable period of performance nationwide, she looks at several regional ones.

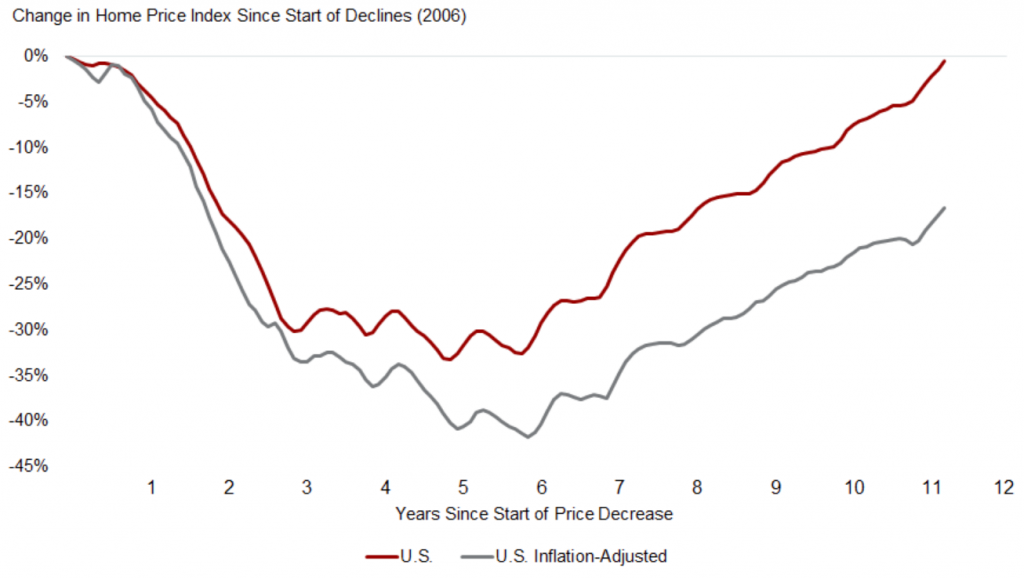

After hitting peak in 2006, the national price level fell for five years, finally reaching bottom in March 2011. Most other sources set the date for the bottom of the market to exactly a year later which may indicate they are using inflation adjusted numbers. From peak to trough, prices fell 33 percent nationally. As of July 2017, CoreLogic data shows prices were approximating the 2006 level.

Boesel compares these numbers to those of the Texas oil bust in the mid-1980’s which resulted in a 16 percent decline over 3.5 years. The peak to recovery cycle in that downturn took nearly nine years. In the early 1990s in California, defense and manufacturing job losses led to home price declines in that state. After falling by 15 percent over five and a half years, home prices in California fully recovered after eight years. The U.S. home price decreases that started in 2006 were twice as severe as these two regional declines.

While national home price numbers are nearly back to their peak, the recovery is far from even. Nevada, where prices dropped the farthest of any state, 60 percent, the 11-year period that has elapsed has left the state 27 percent short of its March 2006 peak.

In Colorado, on the other hand, prices fell 14 percent from an August 2007 peak but have now surpassed that peak by 42 percent. Boesel calls Colorado “an extreme case” of rapidly rising prices, but says 34 states are now above their pre-crisis home price levels.

Boesel says inflation should also be factored into the pace of recovery. From the peak in housing prices through this past July, the inflation has totaled just under 18 percent. When home prices are adjusted for that, the trough was deeper, down 40 percent from the beginning of the cycle, and the recovery shallower; prices remain 17 percent off the peak.

The 2018 forecast from the California Association of Realtors is out, and they are towing the company line as usual. They expect the statewide sales to increase 1% and the California median sales price to rise 4.2% next year.

How is San Diego County doing this year?

Here are the detached-home sales and median price for the first nine months of the year in San Diego County:

SD County Detached-Home Sales, January through September

Year

Number of Sales

YoY Change

Median SP

YoY Change

2012

18,648

–

$375,000

–

2013

19,385

+4%

$450,804

+20%

2014

16,858

-13%

$497,250

+10%

2015

18,389

+9%

$527,000

+6%

2016

18,192

-1%

$555,000

+5%

2017

18,068

-1%

$600,000

+8%

My guess is for the San Diego County detached-home sales to drop 5% next year, and the median sales price to rise 5%. The drop in sales to be on the high-end.

Jeff Swaney is worried about selling his 5,600-square-foot home one day.

In his neighborhood south of Atlanta, demand and prices for large ranch houses like his have declined over the last decade, as more young professionals move to smaller abodes in hipper areas. He doesn’t expect that to change anytime soon.

The 51-year-old real estate investor and owner of Swaney Consulting Group has personal reasons to hold on, at least for now. He may eventually move to a condo at the beach, but wants his future grandchildren to enjoy his pool, yard and basement. For these amenities, he spends about $18,000 annually in lawn maintenance, taxes, insurance and utilities alone.

The housing market, on the rebound since the Great Recession, is increasingly being driven by millennials and first-time homebuyers who “are hungry for starter homes and efficient layouts,” said Javier Vivas, manager of economic research for realtor.com.

The trend may leave some older homeowners in a lurch if they want to retire, downsize and cash in their nest egg.

Large single family homes — defined as the largest 25 percent of all listings on realtor.com and about 2,900 square feet to 4,000 square feet — receive 12 percent to 45 percent less views on realtor.com than the typical home in each market.

This year so far, large, single family homes are selling up to 73 percent (or 50 days) slower on average than the typical home in each market.

The often hefty price tags for bigger homes contribute to their lengthier sale times because there is a smaller pool of buyers who can afford them, said Artur Miller, founder and CEO of Miami-based AMLUXE Realty.

Even Swaney, whose 1994 home appraised for $350,000, thinks he may have a tough time selling.

“The McMansions that soon-to-retire people purchased in the 80s and 90s are a very difficult sell right now,” said Melissa Rubenstein, a former real estate attorney who now sells luxury properties with Re/Max HomeTowne Realty in Bergen County, New Jersey. Many are outdated and may not include a first floor bedroom and bath suite for aging in place or in-laws.

Listings of large homes are also up two percent from last year, suggesting owners are dumping them faster, while listings of all homes are down 10 percent from last year, according to the realtor.com data.

“We’re finding these homes are an albatross for clients,” said Michael E. Chadwick, a financial planner and owner of Chadwick Financial Advisors in Unionville, Connecticut.

“We’ve got several right now who have been trying to sell them and move south, and they’ve cut the asking price by over 30 percent each and they’re still not going anywhere fast,” he said.

Add house-flippers to Goldman Sachs’ ever-expanding roster of potential clients as the Wall Street firm hunts for new ways to make money.

Lending has taken an increasingly higher profile at Goldman, where once-prominent trading desks have had their wings clipped by automation and regulation. The bank started out last year with small loans up to $30,000 for regular people with good credit through an online business it calls Marcus.

This summer it opened its doors to investors by giving financial advisors a way to arrange loans of up to $25 million for clients backed by their investment portfolios.

Goldman is even trying to find a way to occupy its traders’ time, exploring possibilities in the realm of bitcoin and other digital currencies after picking up on client interest in the area.

In September, the bank’s president, Harvey Schwartz, said lending activities are projected to shake out $2 billion in additional revenue. Now Goldman is getting into lending for real estate pros through its acquisition of Genesis Capital.

The deal, for undisclosed terms, gives Goldman a business that makes loans of $100,000 to $10 million at rates of 7 percent to 12 percent. It won’t lend to occupants, so that leaves real estate professionals who are renovating and looking to sell fairly quickly. Genesis made $1 billion of loans last year.

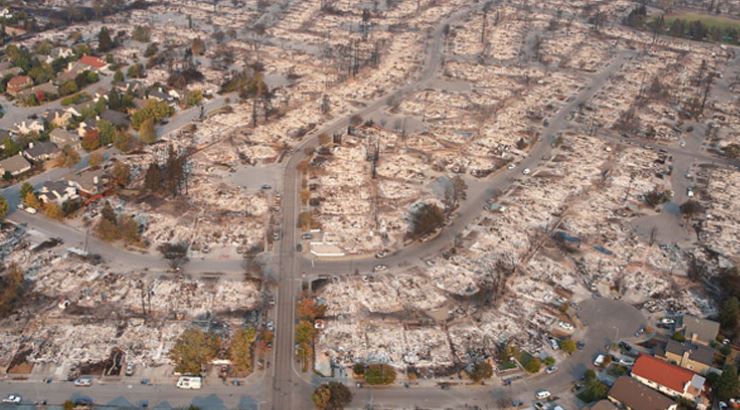

An article that details some of the impact from the fires. The area had a 1% vacancy rate, so for people who got burned out, there is no place to go. If only half of the residents rebuild, then there will be ample opportunities for new people to get in, but at what price?

The median home price in Napa County was a whopping $876,200 on Sept. 1, according to realtor.com® data. In neighboring Sonoma County, the median home price was $750,000. But that was before the fires.

More than 172,000 homes are now at risk of going up in flames in the Napa and Santa Rosa metropolitan areas, which are usually not prone to wildfires, according to an analysis from CoreLogic. (Napa is the name of a town as well as of the surrounding county.) It will cost an estimated $65 billion or more to rebuild them.

Californians are just beginning to come to grips with the scope of the disaster.

“Multiple neighborhoods are burnt out,” says Randall Bell, CEO of the national real estate appraisal firm Landmark Research Group, based in Laguna Beach, CA, which has assessed areas damaged by wildfires. “It’s street upon street of just charred-to-the-ground moonscape. All you see are chimneys and foundations. It’s a sad sight—and you see hundreds of them.”

Only about a quarter to half of the original residents whose homes were reduced to ash are likely to return and rebuild, Bell predicts.

“Emotionally they’re overwhelmed. Financially, they’re overwhelmed,” he says. “When these fires come through, they don’t just burn houses. They burn stores, restaurants, the churches, the schools. They burn everything. You may rebuild a house, but where’s your infrastructure?”

Lee, the real estate agent whose Santa Rosa home burned down, doesn’t plan to rebuild. He and his wife plan to move to Kentucky, TN, or North Carolina, where they have friends who might be able to find him work.

“I’ve started an insurance claim and hopefully I’ll do well. … [But] I’m a real estate agent and there’s nothing to sell anymore,” he says. “I’m starting over from scratch at 63 with achy joints and an achy back.”

Even homeowners with insurance premiums may not get enough money to rebuild their entire homes to what they were before, Bell says. That’s because the price of construction is likely to skyrocket with the extra demand for construction workers, for which there is currently a national shortage compounded by Hurricanes Harvey and Irma, and building materials. Some will get loans, others will tap into their savings.

Those who do rebuild are in for the long haul. The area is expected to recover only about 10% to 15% each year, according to Bell. That means it’s likely to take five to 10 years before homes, businesses (including employment and tourism), and the local infrastructure is back to normal.

Plus, they’ll have to find a place to live while they rebuild—which won’t be an easy feat.

“We had a housing crisis before the fire,” says Santa Rosa–based Realtor® Daphne Peterson, of Keller Williams Realty. “We’re in a very high-cost area. Our vacancy rate was about 1%. Now we’ve lost about 1,500 to 2,000 homes. We have no place for people to stay.”

Homeowners who decide to sell won’t have it easy, either. Those whose homes survived should expect the properties to sell at a 10% to 35% discount. That’s because it’s not as desirable to live near burnt-out houses or with fewer services and businesses nearby.

“People don’t buy a house,” Bell says. “They buy a neighborhood.”

Meanwhile, properties whose homes were charred or destroyed altogether could see discounts as high as 60%, he says. Sellers should expect an army of investors, a combination of home flippers and landlords, to swoop in.

But the price breaks won’t last forever. These will likely dissipate after about five years, he says.