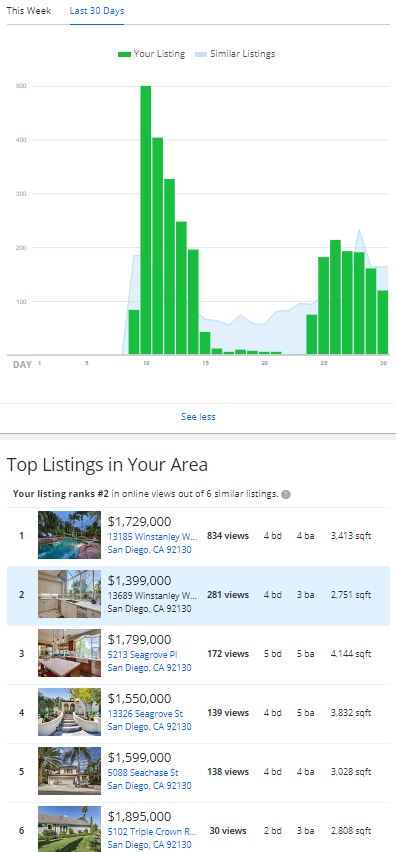

Our listing in Carmel Valley is still getting hundreds of views – the chart above are two-day totals. I love when a new listing hits the market nearby, because it gives buyers some perspective, and in this case we are almost identical in cost per square foot ($507 vs $509) so the analytical buyers will be pleased.

The graph at the top shows the importance of the first few days on the market.

It’s virtually impossible to re-ignite the same buzz later, even with a price reduction, so we try our best to make the first deal stick. In this case, our first buyer was doing a 1031 exchange with tight timelines, but then the IRS extended everyone to July 15th, so like most buyers he figured he could get a better deal later, and cancelled on us.

The talk about how opening up the country will affect the real estate market seems simple enough to me. The more-motivated buyers will be the first ones to venture out, and that’s who drives the market anyway.

I’ve been convinced for years that we can sell homes by video, and the coronavirus will present that challenge to us now. If agents can be handy with their phone, a decent representation can be made that should be enough to get buyers to make offers – and we’ll figure out the rest:

Value buy in Santa Fe Summit, where the last four sales were $1.75M to $2.0M! Located at the far-north end of Winstanley near miles of walking trails yet close to TPHS. Hardwood floors, new carpet, new paint, three fireplaces, and kitchen has new quartzite counters/newer stainless appliances to go with a walk-in pantry! Downstairs bedroom with attached full bath too. The Mello-Roos ends in April, 2027, which means big savings over PHR!

4 br/3 ba, 2,751sf

YB: 1994

LP = $1,380,000 Jim represented both the buyers and sellers.

The 10,022 sf space station above Carmel Valley has a $4,000,000 mortgage out on it when Union Bank foreclosed on it in 2010. They sold it for $2,475,000:

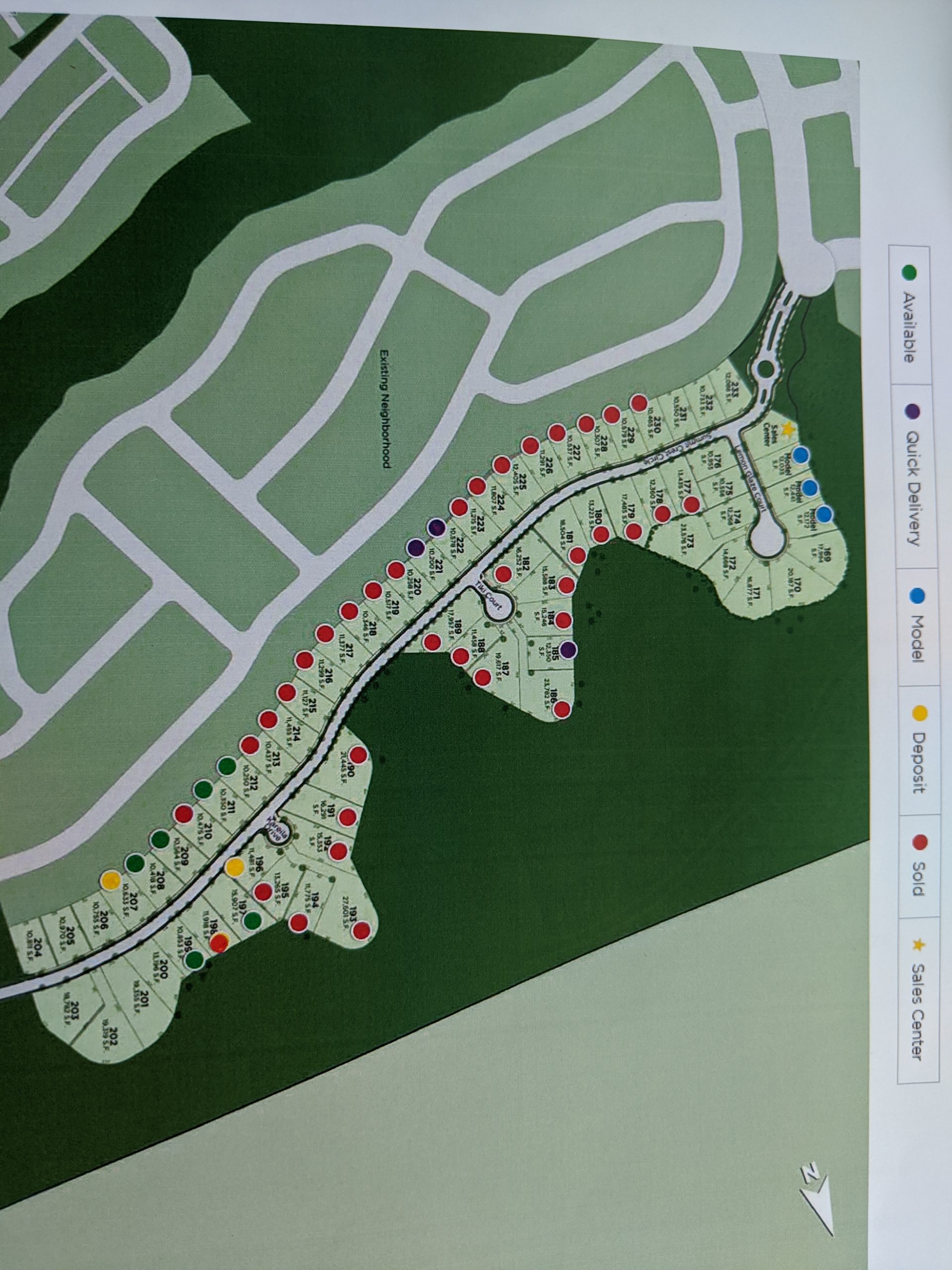

What will it be like when there are no more new homes to buy in Carmel Valley? Pardee has been building houses steadily for 30+ years, and they will be down to their last 103 lots, once they are done here – and they’ve sold 33 of 44 so far. These are priced from $1.8 to $2.5M.

Toll hopes to sell two per month at Palomar (the image above), and they sold five in October! Altogether they’ve sold 36, which puts them ahead of schedule. They are priced from $2.5 to $3.8M.

This just closed for full price, $1,925,000, which is the highest sale in the history of the Santa Barbara tract. But no surprise – there hasn’t been a sale on this side of the street in 2+ years, and these compete very well with the new homes down the hill. Plus you could have moved in for the holidays!

Are you looking for a quiet and private culdesac home with white kitchen and new master bath?

Then check out my new listing in RP! This 4br/3ba, 2,394sf house is 900ft above sea level and gets gentle breezes daily! Open floor plan, 3 full bathrooms, low-maintenance yard, central air conditioning and whole-house fans. The house and yard are great…..but wait until you see the dazzling new master bath! Great curb appeal too – with putting green in front yard!

We featured this bank-owned property earlier as an online auction (which didn’t work out).

They did find a cash buyer – I hope they got in the house to take a look around!

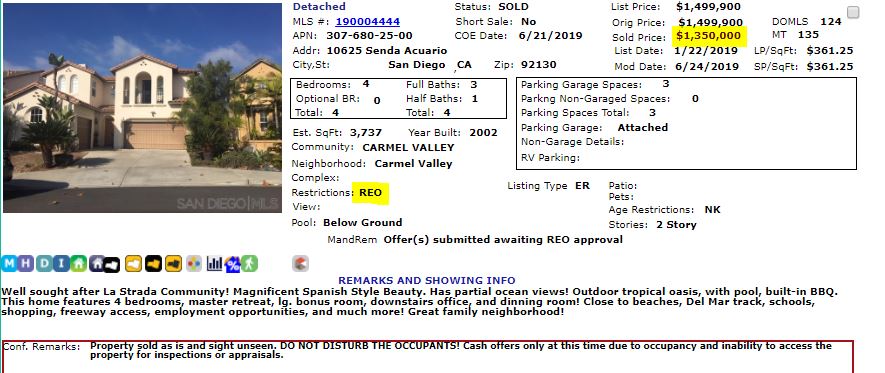

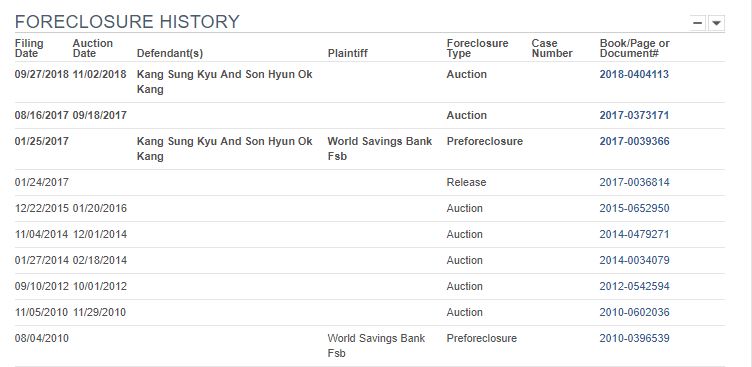

This is a typical example of an REO sale these days. The former owners paid $1,650,000 in 2007, and used a 31% down payment. The original $1,137,500 mortgage was funded by World Savings, and undoubtedly it was a neg-am loan.

It looks like the buyers stopped paying in 2010, but instead of foreclosing and losing a truckload, the bank (Wells Fargo, who bought World Savings) just waited until they knew market value was high enough that they wouldn’t lose money:

The price at the trustee’s sale in November was $1,365,016, and they sold it traditionally for $1,350,000. It means that after paying closing costs, the bank received 100% of the principal back, plus around $150,000 of the neg-am interest that accrued.

These days, banks are only foreclosing once they can make money on them!

Because they are building such large houses, the one-story plans barely fit on these interior lots that have slopes. Toll has literally redesigned smaller versions so they can get a bigger backyard.

Wells Fargo foreclosed on this Carmel Valley home in November. It had been listed on the MLS for the previous 12 months, and it looked like the agent had been trying to process a short sale (it was marked ‘contingent’).

She had it listed for $1,500,000.

Her clients paid $1,650,000 in 2007, and financed $1,137,500 with World Savings. Times were tough for many, and these folks got their notice of default filed in August, 2010. It doesn’t look like they made any payments since.

Wells Fargo’s amount at the trustee’s sale was $1,365,016, which is typically the amount owed. So the former owners got a couple of hundred thousand dollars in relief, but waved bye-bye to their down payment of $512,500.

Wells Fargo then listed the house for sale in January for $1,499,000, and has now sent it to an online auction. The bidding started yesterday, and will remain open until Tuesday:

The interesting twist is that the house is occupied – probably by the former owners – and no one is allowed to see the house. They also have only one photo of the exterior.

I’ll help them out by providing a link to the previous listing with photos here:

The auction website also notes that it needs to be a cash purchase, though it’s not mentioned in the MLS listing. The buyer has to pay a 5% buyer’s premium on top of the purchase price, and I assume they want you to close escrow with the occupants inside?

What will somebody pay for the home, under those conditions?

The current bid is $1,199,920, though note sure if that is actually a real offer or just the minimum bid.