Higher prices, higher rates, slowing sales, and now easing loan guidelines? On non-owner-occupied properties? Buying a rental property with 5% down is unheard of, and even with higher rents they are likely to negative cash flow:

Freddie Mac is consolidating its Home Possible program with its Home Possible Advantage Mortgages program. These programs offer greater flexibility and higher loan-to-value ratios (LTVs) than traditional mortgage programs.

The combined product will be called Home Possible Mortgages, and will closely align with the purpose and requirements of the previously-named Home Possible Advantage program, with some changes.

Beginning October 29, 2018, lenders will be able to offer Home Possible Mortgages to buyers with limited down payment funds. Under the consolidated program, eligible homebuyers will include:

non-occupant buyers for mortgages secured by one-unit properties with LTVs no higher than:

95% for Loan Product Advisor Mortgages; or

90% for manually underwritten mortgages (non-occupant buyers were previously excluded from the programs);

those who own other properties (buyers who own other properties were previously limited);

buyers with super conforming mortgages (mortgages with high maximum mortgage limits for homes located in high-cost areas) when the mortgage:

is submitted and receives an “Accept Risk” classification through the Loan Product Advisor; and

has an LTV no higher than 95% (super conforming mortgages were previously not permitted);

buyers with secondary financing, including home equity lines of credit (HELOCs), for most cases when the mortgage’s LTV is no higher than 97% (secondary financing was previously limited to 95% LTV);

buyers using adjustable rate mortgages (ARMs), when the LTV is no higher than 75% (ARMs were previously not permitted); and

buyers with a maximum 45% DTI for manually underwritten mortgages.

These changes are meant to both widen the pool of qualified homebuyers, and streamline programs for lenders’ ease of use.

Housing market risks broaden

By loosening the requirements for its Home Possible Mortgage programs, Freddie Mac’s hope is to encourage lenders to qualify more applicants, thereby increasing homeownership opportunities nationwide.

However, loosening requirements by allowing high LTVs, DTIs and ARMs makes lending — and by extension the housing market — riskier. For veteran real estate professionals, a growing presence of dangerous mortgage products and loose lending restrictions will sound familiar, as they all increased during the Millennium Boom and ultimately played a big part in the cause of the housing crash and 2008 recession.

Nothing wrong with distributing the estate early to help out the kids, and mortgage guidelines encourage it – the down payment can be 100% gift:

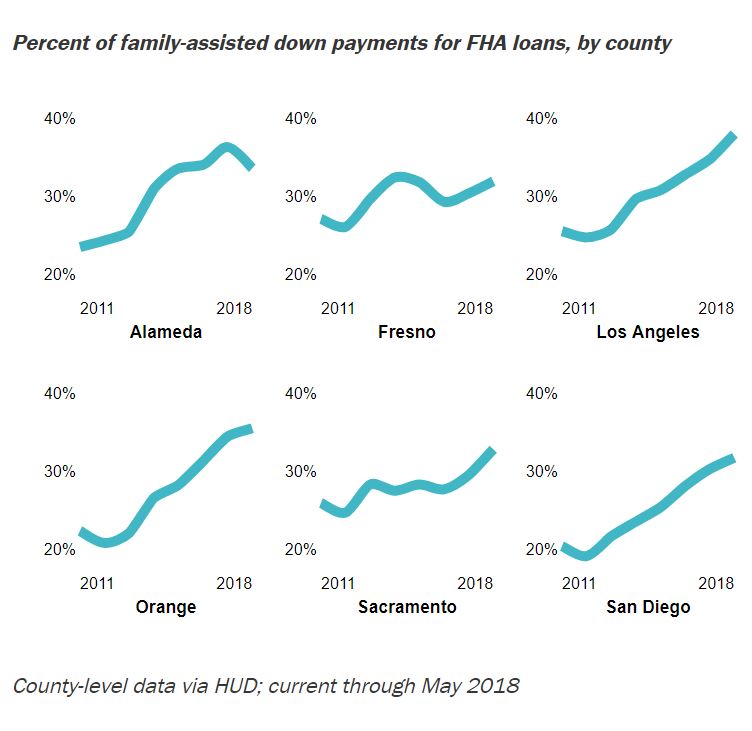

When Melanie Gerber started working as a mortgage loan officer in Riverside seven years ago, she didn’t see many first-time buyers hitting up their parents for help.

Now she sees it all the time. “I have one that just went into escrow yesterday,” Gerber said. “They’re having money gifted from the family.”

She estimates about half of her borrowers are now getting money from mom and dad. “I think the parents just want them to make it on their own and know they can’t do it,” she said.

Gerber’s observations are backed up by federal data. If you want to buy a home in California, it increasingly helps to have relatives who can chip in.

KPCC crunched the numbers on more than 600,000 FHA loans, a type of government-backed mortgage that’s common with first-time buyers.

FHA borrowers can use money from relatives for their down payment. In recent years, that kind of family financial help has been on the rise in California.

Back in 2011, about one in four FHA loans in California included down payment money from relatives. Today, it’s one in three.

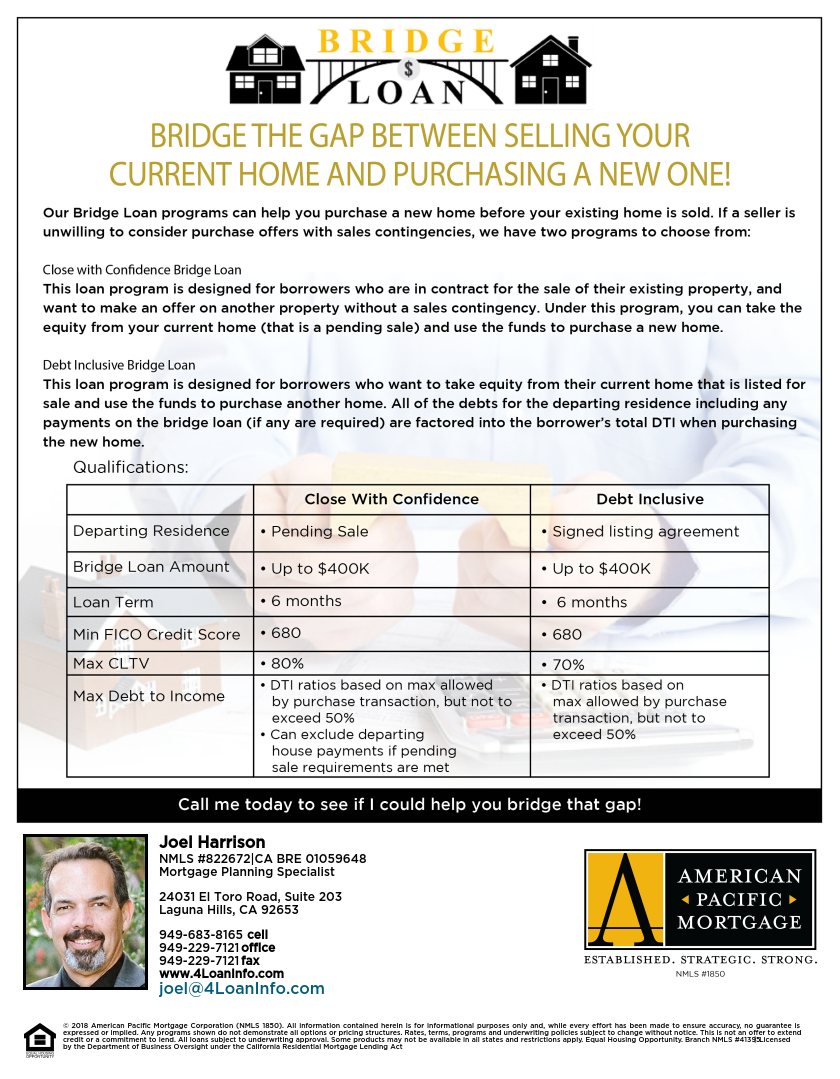

Are you turned off by the e-buyer who wants to lowball your home’s value, and then knock off another 7% to 9%? But you like the idea of having your equity available for the next purchase?

How about an old-fashioned bridge loan?

Joel arranged financing for a recent buyer of ours who changed jobs during the week of escrow closing – Joel re-verified employment and still closed on time. This was on 97% financing of a converted-apartment condo built in 1979.

Freddie Mac’s underwriting also allows self-employed buyers to submit tax returns for one year only, instead of the customary two years’ tax returns. I’m not sure if they will do that on this new program?

It’s been more than three years since Freddie Macrolled out a conventional mortgage that only required a 3% down payment for certain borrowers.

But now, Freddie Mac is about to supercharge its 3% down program and launch a widespread expansion of the offering.

Freddie Mac announced Thursday that it is rolling out a new conventional 3% down payment option for qualified first-time homebuyers. What makes this program different is that there are no geographic or income restrictions.

The new program, which is called HomeOne, puts Freddie Mac in direct competition for mortgage business with the Federal Housing Administration, which also only requires 3% down on some mortgages.

Can you do an article on the housing affordability index related to NSDCC? Just wondering what percentage of people need x amount of dollars with 20% down to afford a median priced home?

Let’s include data on the median price of detached-home active listings, and those sold in the last 90 days. I used an interest rate of 4.50%, 20% down payment (25% down payment on $2,395,000 price), and qualifying ratio of 35%:

Category

# in Category

Median Price

Cash to Close

Annual Income

SDCo Actives

3,912

$824,823

$170,000

$115,000

SDCo Solds

4,744

$624,700

$130,000

$87,000

NSDCC Actives

822

$2,395,000

$605,000

$312,000

NSDCC Solds

608

$1,327,500

$270,000

$185,000

The fixer market feels the impact. When it takes both spouses holding down good jobs to qualify, they don’t have the time or patience to fix up a house – they want and need a house in good shape. Maybe this is where Zillow and others can provide more renovated homes to fit the needs of today’s buyers.

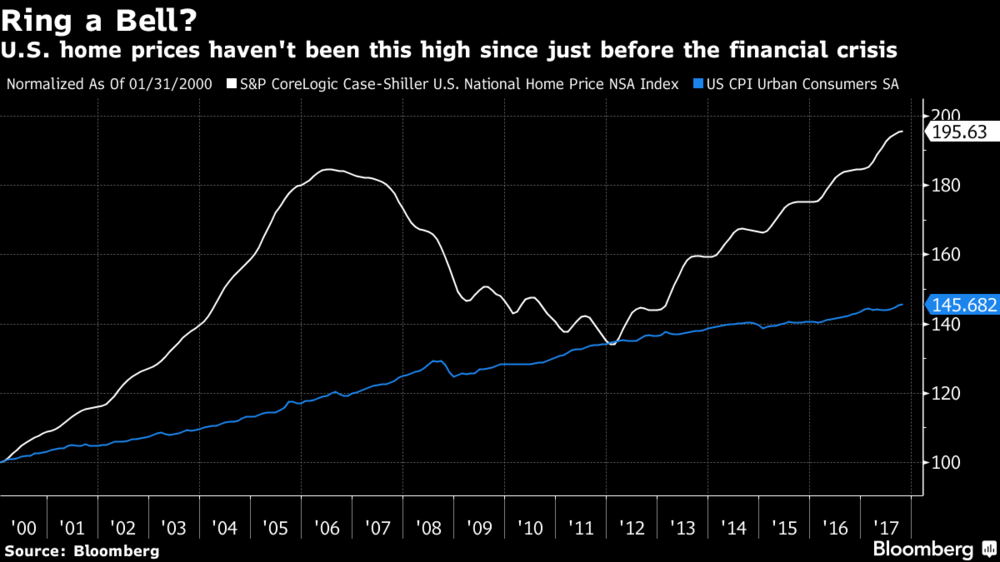

When real estate investors get this confident, money manager James Stack gets nervous. U.S. home prices are surging to new records. Homebuilder stocks last year outperformed all other groups. And bears? They’re now an endangered species.

Stack, 66, who manages $1.3 billion for people with a high net worth, predicted the housing crash in 2005, just before prices reached their peak. Now, from his perch in Whitefish, Montana, he says his “Housing Bubble Bellwether Barometer” of homebuilder and mortgage company stocks, which jumped 80 percent in the past year, once again is flashing red.

“It is 2005 all over again in terms of the valuation extreme, the psychological excess and the denial,” said Stack, whose fireproof files of newspaper articles on bear markets date back to 1929. “People don’t believe housing is in a bubble and don’t want to hear talk about prices being a little bit bubblish.”

As the housing market approaches its key spring selling season, Stack is practically alone in his wariness. While price gains may slow, most analysts see no end in sight for the six-year-old recovery.

There are plenty of reasons to be optimistic. The housing needs of two massive generations — millennials aging into homeownership and baby boomers getting ready for retirement — are expected to fuel demand for years to come if employment remains strong. Sales in master-planned communities, many of which target buyers who are at least 55, reached a record last year, according to John Burns Real Estate Consulting. Last month, a gauge of confidence from the National Association of Home Builders/Wells Fargo rose to the highest level in 18 years, and starts of single-family homes in November were the strongest in a decade.

“As soon as homes are finished, they’re flying off the shelf,” said Matthew Pointon, Capital Economics Ltd.’s U.S. property economist.

Stack has a different perspective. While the market might gradually correct itself, history shows that it’s more likely to “come down hard” with the next recession, he said. He described the pattern as a steep run-up in housing prices spurred by low interest rates. The last downturn came about when economic growth slowed after a series of rate increases, exposing the “rot in the woodwork” and prompting loan defaults, Stack said.

He noted that the Fed has projected three rate increases for this year, and said that “raises the risk that today’s highly inflated housing market will again end badly.” He’s watching homebuilder stocks closely because they’re a leading indicator, peaking in 2005, the year he called the crash — and the year before home prices themselves hit a top.

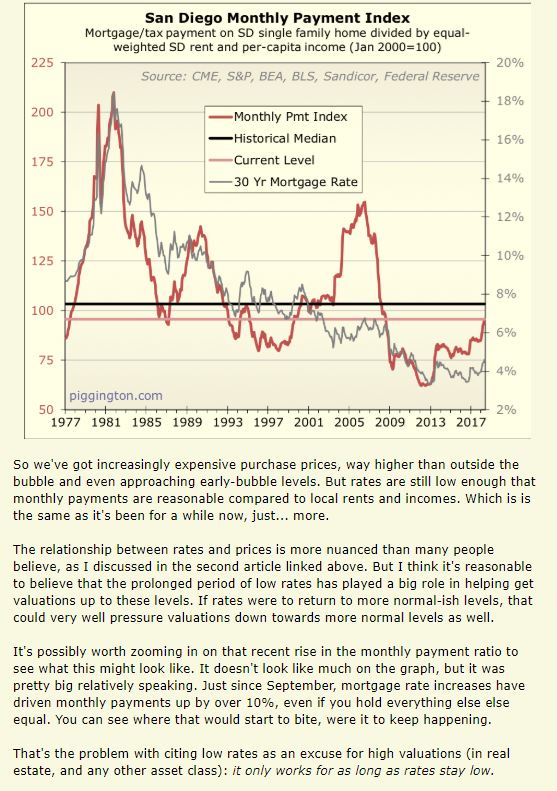

Jim: Of course today’s environment feels irrationally exuberant – it’s hard to believe how well we have done since our pricing recovery began in 2009!

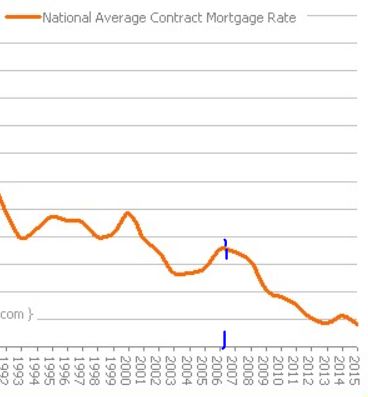

But his reasoning that higher mortgage rates would “Raise the risk that today’s highly inflated housing market will again end badly” is off-base. Rates were coming down during the mortgage crisis – it was the fury over the neg-am loans that caused borrowers to think their payment was going to go through the roof, burn the house down, and kill their family. Borrowers who could only afford their initial minimum payment on the ARM then panicked at the first adjustment and hit the eject button.

Neg-am loans are now illegal, and I haven’t seen or heard of any ez-qual loans available at conforming rates – everybody who bought a house in the last nine years had to prove they could afford it, and their payment is fixed. Besides, we learned last time that just because their home value went down, people don’t panic and sell their house as long as they can afford it. People have to live somewhere, and we like it here. If a full-blown depression happened and we had another run of defaults, the government will provide another safety net and just tell banks not to foreclose.

If rates go up to 5% or 6%, it will probably stall the market, causing prices to bounce around. But there won’t be enough sellers who will dump on price that it would cause a major event. There could be a skirmish here and there caused by boomer liquidations occasionally. But that’s it.

Most business crowdfunding platforms offer returns on the investment, but this has none — it is simply a gift. George said the individual gifts will be small, in the $50 to $250 range. The platform can be linked to wedding and baby registries.

“You’re going to spend $250 on a coffee making machine? If that $250 goes to a down payment of your home, at the very least, I improve your quality of life and the second thing I do is I give you some, today, some tax deductibility,” George added.

As an incentive for encouraging prospective homeowners to attend credit education courses and counseling, borrowers can also receive grants of up to $2,500 once they’ve completed the free classes. After that, the platform will match donations at $2 for every $1 raised, up to $2,500.

“Folks that go to counseling tend to be more informed, and they also tend to be better borrowers,” George said. “We’ve looked at this as advertising dollars and have said, listen we think this promotes homeownership, we think it’s something that we would otherwise spend either through the internet or through social media. We’ve put our money here where we think it has its best use.”

On the other side, contributors are also assured that the money will in fact go to fund the home purchase and can make their gift conditional on that.

The idea is not just to raise money for the down payment but to add to the borrower’s existing funds. This can help eliminate the need for mortgage insurance, which is required on very low down payment loans. Fannie Mae is calling it a “pilot project,” and will be watching the results closely.

“What we’re doing today is we’re trying to test and learn a variety of solutions because the preferences for today’s homebuyers have changed significantly, and there is no silver bullet to solving a problem that’s as hard as how do you find a down payment,” said Jonathan Lawless at Fannie Mae. “What we prefer to do is source ideas from all sorts of different places. Our customers are a major one, lenders who are dealing every day with people trying to buy homes, and instead of trying to take those ideas and spend three years trying to roll out a major change, we’d rather test and learn.”

In what has to be one of the most bizarre developments in real estate this year, the ivory-tower folks at the Fed, of all people, dreamed up a creative new loan that would not require a down payment. Then they used the dreaded COFI term from neg-am mortgage days! No word on when these might be available, if ever:

Abstract: The 30-year fixed-rate fully amortizing mortgage (or “traditional fixed-rate mortgage”) was a substantial innovation when first developed during the Great Depression. However, it has three major flaws. First, because homeowner equity accumulates slowly during the first decade, homeowners are essentially renting their homes from lenders. With so little equity accumulation, many lenders require large down payments. Second, in each monthly mortgage payment, homeowners substantially compensate capital markets investors for the ability to prepay. The homeowner might have better uses for this money. Third, refinancing mortgages is often very costly.

We propose a new fixed-rate mortgage, called the Fixed-Payment-COFI mortgage (or “Fixed-COFI mortgage”), that resolves these three flaws.

This mortgage has fixed monthly payments equal to payments for traditional fixed-rate mortgages and no down payment. Also, unlike traditional fixed-rate mortgages, Fixed-COFI mortgages do not bundle mortgage financing with compensation paid to capital markets investors for bearing prepayment risks; instead, this money is directed toward purchasing the home. The Fixed-COFI mortgage exploits the often-present prepayment-risk wedge between the fixed-rate mortgage rate and the estimated cost of funds index (COFI) mortgage rate.

Committing to a savings program based on the difference between fixed-rate mortgage payments and payments based on COFI plus a margin, the homeowner uses this wedge to accumulate home equity quickly. In addition, the Fixed-COFI mortgage is a highly profitable asset for many mortgage lenders. Fixed-COFI mortgages may help some renters gain access to homeownership. These renters may be, for example, paying rents as high as comparable mortgage payments in high-cost metropolitan areas but do not have enough savings for a down payment. The Fixed-COFI mortgage may help such renters, among others, purchase homes.

Keywords: COFI, Cost of funds, Financial institutions, Fixed-rate mortgage, Homeownership, Interest rates, Mortgages and credit

JtR: This sounds like the reverse of a neg-am mortgage, or a positive-amortizing loan where borrowers have a fixed payment as a ceiling, and then when rates float down, the difference is applied to the principal. But how much potential is there for your rate to drop when we’re at all-time lows? Maybe they are preparing a loan option for the day that rates rise substantially?

Freddie Mac announced Friday it is making buying a home a better experience for lender and homebuyers – by cutting the appraiser out of the process.

The company is now offering a new product which will cut the appraisal process out of qualified home purchases and refinances. This could save borrowers an estimated $500 in fees and could reduce closing times by as much as 10 days.

The new Automated Collateral Evaluation assesses the need for a traditional appraisal by using proprietary models and utilizing data from multiple listing services and public records as well as the historical home values in order to determine collateral risks.

“By leveraging big data and advanced analytics, as well as 40+ years of historical data, we’re cutting costs and speeding up the closing process for borrowers,” said David Lowman, Freddie Mac executive vice president of single-family business.

“At the same time, we’re providing immediate collateral representation and warranty relief to lenders,” Lowman said. “This is just one example of how we are reimagining the mortgage process to create a better experience for consumers and lenders.”

Lenders can determine if a property is eligible for ACE by submitting the data through Freddie’s loan product advisor. This will then assess credit, capacity and collateral to determine the quality of the loan. Lenders will receive the risk assessment feedback in real time.

ACE will be available for home purchases beginning on September 1, 2017.

Earlier this summer, the company announced it began using this product on qualified refis beginning June 19, 2017.

“When we launched loan advisor suite in July 2016, we set out to give our customers certainty, usability, reliability and efficiency,” said Andy Higginbotham, senior vice president of strategic delivery and operations for Freddie Mac’s single-family business. “ACE is our most recent capability to deliver on that vision.”

Fannie Mae also updated its policy on appraisals this year, and clarified its “existing policy that allows an unlicensed or uncertified appraiser, or an appraiser trainee to complete the property inspection. When the unlicensed or uncertified appraiser or appraiser trainee completes the property inspection, the supervisory appraiser is not required to also inspect the property.”