The doomers are hoping to drive the real estate market into hysterics, just for fun. It’s easy for buyers and sellers to get caught up in it too, and think the sky is falling.

Let’s identify the terms, what doomers want you to believe, and the truth:

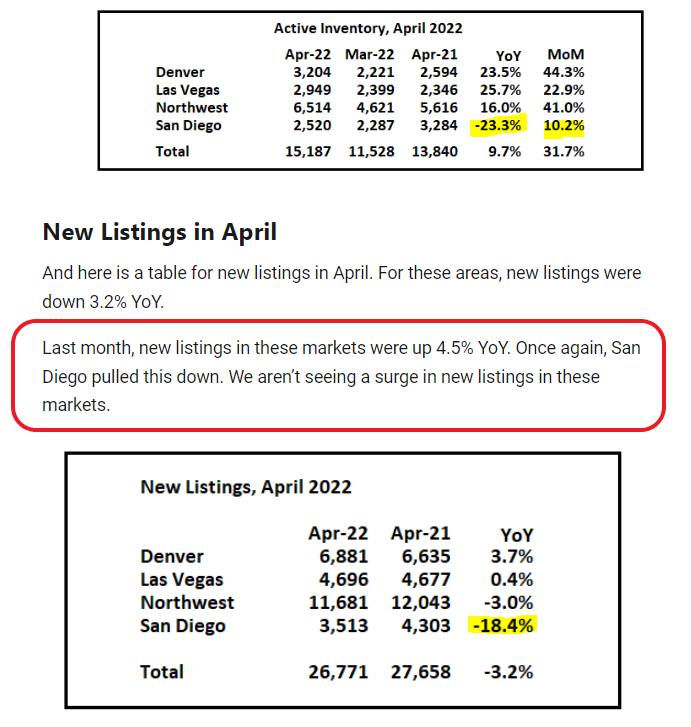

Inventory Surge

Doomers: Sellers are hitting the panic button.

Truth: If we are taking about a surge in active listings, it is because the list of aspirational sellers (those who will only move if they get their price) is growing longer. They aren’t the market makers; they are only helping those that are.

Price Reductions

Doomers – Home prices are falling.

Truth: Sellers mis-priced their home from the beginning, and now they are hoping that if they knock off a couple of bucks, it will make a difference.

Affordability/Revert to Mean

Doomers – Home prices must come down so regular people can afford to buy.

Truth – Around here, homes haven’t been affordable for the common man in years, yet home prices have accelerated. The NSDCC market is only for the affluent now.

Higher Rates Will Crush the Market

Doomers – Home prices and rates go hand in hand. When rates go up, prices must come down.

Truth – The bumps in rates are only giving the affluent a reason to pause, in hopes of a price correction.

More Open Houses

Doomers – Realtors are panicking.

Truth – More realtor trainees are trying their luck.

Home Sales Dropping

Doomers – Market is being crushed.

Truth – More sellers are holding out for their price.

Sales Crushed

Doomers – Zero

Truth – If the NSDCC monthly sales stay in the 100-200 range, we will be fine. Those are January counts, and the usual market seasons have been topsy-turvy since March 2020 so it will give the demand more time to get pent-up.

Prices Crushed

Doomers – 50% off

Truth – Sellers determine what they can live with, and their ego plays a bigger role than you might imagine. Nobody has to sell any more, so expect resistance to selling for lower than the last sale. Only the extremely-motivated sellers will sell for a big discount today – it will take years for that to become commonplace.

There are many who insist that real estate will follow its historical trend, and I like to say ‘it’s different now’ just to irritate them.

What are the things that are different?

Every buyer has had to qualify for their mortgage and use a sizable down payment, the vast majority have been buying their forever home (even if they didn’t know it at the time), and homeowners at the coast will likely be paying six figures in capital-gains taxes if they sell – which means that they need to leave San Diego to really make it worth moving. As a result, the number of people who are willing to sell has plummeted, which has kept the pressure on pricing.

The demand is different too. Back in the old days, it used to be loosely tied to incomes, but that flew out the window decades ago around here. The influx of affluent people has helped, but there is also a big difference that these researchers have explored – working from home:

It’s no secret that Americans’ newfound remote work lifestyles drove demand for larger homes with more comfortable workspaces.

What’s new: That demand may be responsible for more than half of the surge in real estate prices during the pandemic, according to a working paper published by the National Bureau of Economic Research.

It’s one of the first papers that aims to quantify how remote work reshaped the housing market.

Why it matters: If the research holds up, it signals a fundamental shift in the housing market — that it wasn’t just low-interest rates and fiscal stimulus that drove up housing prices.

By the numbers: It found that remote work led to about 15 percentage points of the 24% average increase in house prices between December 2019 and November 2021.

Details: The paper’s authors are John A. Mondragon, an economist at the Federal Reserve Bank of San Francisco, and Johannes Wieland, of the University of California, San Diego’s economics department.

The researchers found that after controlling for COVID migration, regions with the highest rates of remote work experienced much higher home price growth during the period.

They also observed a similar effect on residential rents — along with declines in commercial rents — in these areas.

What they’re saying: This implies a shift in demand, as many pandemic homebuyers and renters sought to upgrade to larger, and more expensive homes to support their telework lifestyles, said Mondragon.

The bottom line: Policymakers like those at the Fed would be wise to pay close attention to the evolution of remote work because it will help determine the future of home prices — and of overall inflation, the economists wrote.

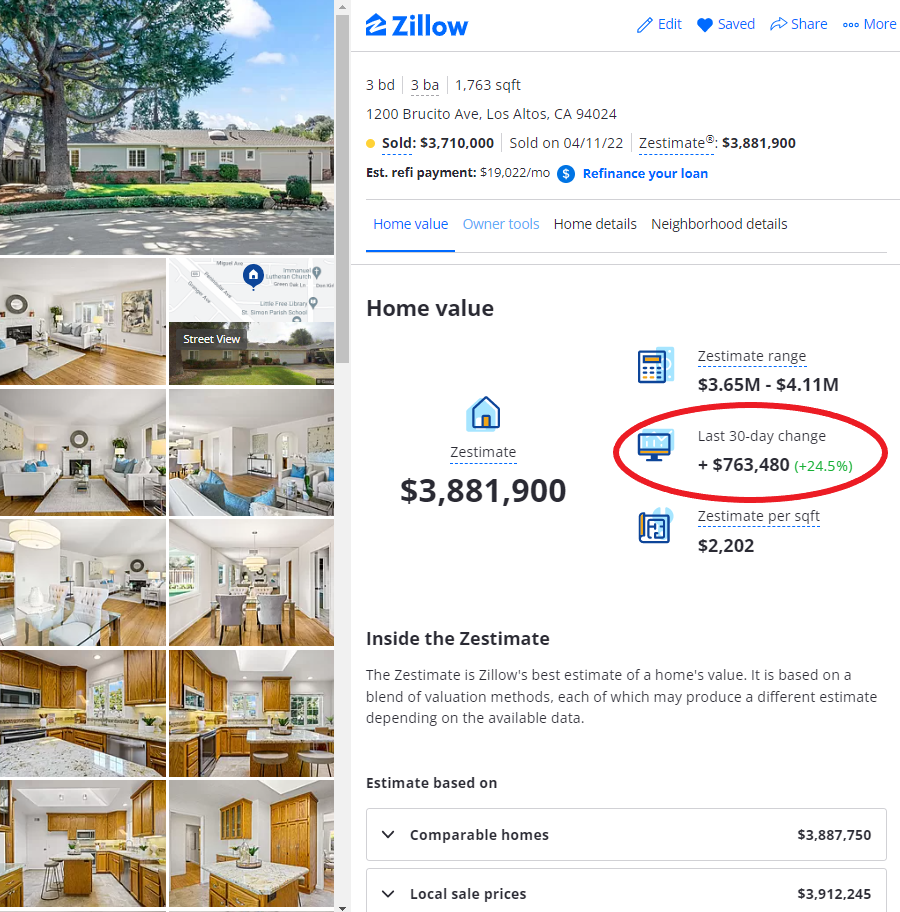

The bump over the list price is so customary in the local area that the zestimate was raised by $763,480 about the time it was marked pending – the algorithms already had the expected increase baked in!

They are enjoying The 2022 Lucky Windfall of the First Quarter, and we’ll see how well it holds up. But as long as home sales in the Bay Area keep selling for much-higher pricing than in San Diego, one of our main feeder areas will keep sending happy buyers our way!

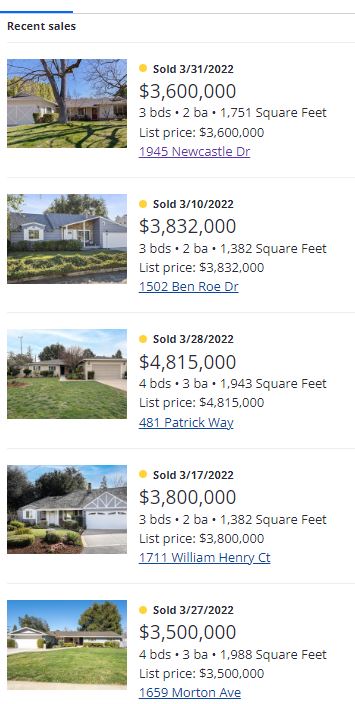

The list prices mentioned here all say that they sold for 100% of the LP, but it’s a typo – they all sold for well over. For example, Patrick Way sold for $1.1 million over, and William Henry sold for $800,000 over list:

Paying ~$2,000/sf for modest homes in Los Altos has been fairly routine lately!

Hopefully, those sellers keep coming our way. Even if their market were to dip 10% to 20% from these dizzy heights, they will still love what they can buy here for the money.

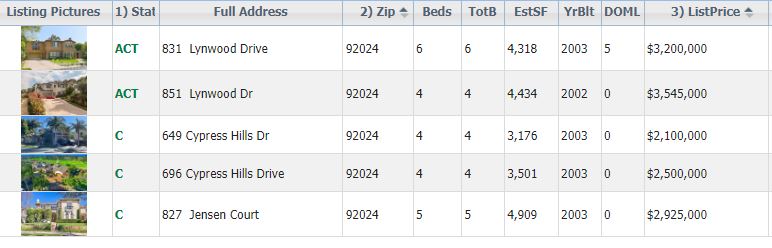

The new listings of 2022 are only trickling out, but we know that there can be spurts.

We’re seeing one underway in Encinitas Ranch, where five listings are hitting the market this week! The three Coming-Soons will all change to active listings on Saturday.

Buyers – there is hope!

Whenever there are two or more homes for sale in a neighborhood, there is one fact of life:

Either yours is selling mine, or mine is selling yours.

The chances of EVERY house being perfectly priced to reflect their condition AND compare favorably to all other choices is about the same as the Padres chances of winning the World Series. It’s possible every year, but come on.

There are times when NONE are perfectly priced, causing a stalemate and no sales.

The market is hot enough that at least one of these listings will compare more favorably than the rest, and will sell this weekend. With few or no other choices for sale currently, the ultra-hot frenzy conditions could pick up two of more of these listings.

Let’s see how many go pending in the next seven days!

During the inspection of the fixer in Olde Carlsbad, it was determined that further investigation was warranted due to the slope in the floor.

A geologic engineer came out with his fancy altimeter and found that there was a 5-inch difference between the foundation height from one side of the house to the other.

Here’s how it looked. When you have seen me do this, I have set the ball down and let it go where it goes. In this case, the buyer rolled the ball in one direction, only to have it make a U-turn and go the other way…..and it picked up speed:

In the course of the discussion, I asked, “What is the worst you have seen?”

The engineer said, “A nine-inch differential.”

I said, “Ok, so this is kinda in the middle”.

To which I added a solution. Install the popular wood-tile, and have the installer add some extra mortar to help make up the difference. It doesn’t have to get to zero – if it was down to 2-3 inches it wouldn’t be as noticeable.

The buyers asked for a $50,000 reduction in price, and the seller agreed. It could have been worse – cancelling this sale and finding a new buyer who would pay more than $1,050,000 seemed unlikely.

Our sale closed on Tuesday, a couple of days after this closed nearby:

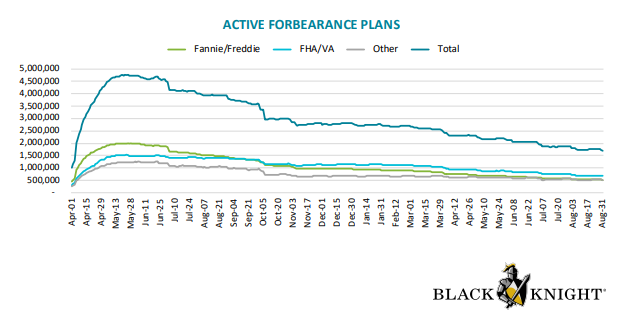

Another update on the forbearance exits. Nobody is going to get foreclosed in North San Diego County’s coastal region, mostly because of the ample equity position every homeowner has in place – but those positions could cause them to sell. Won’t the homeowners be spoiled from the 12+ months of free rent, and, once they recognize the alternatives (renting for ridiculous rates here or moving out of state), be more likely to work out a payment plan with their lender? Yes! But this would be a good time for a surge, if it happens!

Black Knight estimates that nearly 630,000 forbearance plans, more than one-third of those currently active, are slated for review this month. Of those, 400,000 will have reached the end of their 18 months of forbearance eligibility unless the maximum term is extended again.

The end of August saw a significant decline in forbearance numbers as servicers worked through the month’s crop of three-month reviews. Plans declined by 53,000 over the week ended August 31 with more than 23,000 from FHA or VA portfolios. The number of GSE (Fannie Mae and Freddie Mac) loans dropped by 20,000 and loans serviced for bank portfolios or private label securities (PLS) saw a 10,000 unit decline. The number of plans is down by 9 percent since the end of July.

Black Knight estimates that approximately 1.71 million borrowers remain in forbearance, 3.2 percent of the 53 million outstanding mortgages. Those loans have an unpaid balance of $331 billion. The total includes 514,000 GSE loans, 676,000 FHA and VA loans, and 520,000 portfolio/PLS loans. The loans remaining in forbearance represent 1.8 percent of the GSEs’ totals and 5.6 percent and 4.0 percent of FHA/VA and portfolio/PLS loans, respectively.

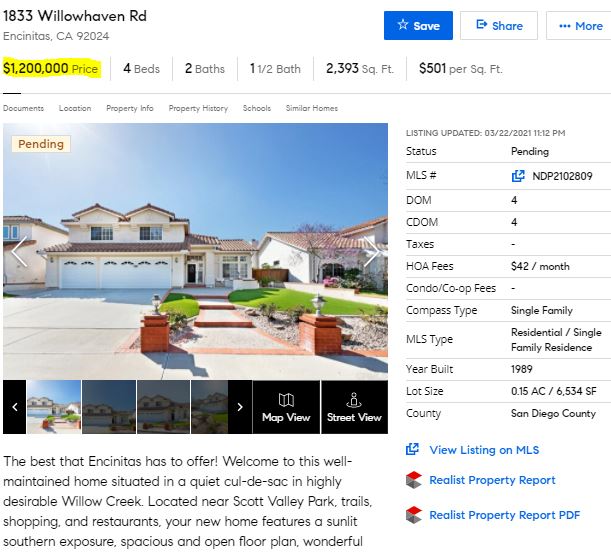

To provide some transparency on the deal-making on the street, here’s a review of properties that have gone pending this week. I didn’t intend to make a blog post out of it, but I had inquired about the availability of these listings, and for my own knowledge I like to ask how many offers the listings agents have received.

They had FIVE OFFERS on 1833 Willowhaven, and another similar home that listed on the same side of the street for $1,299,000 also had multiple offers. A good example of how a few more listings in the lower price ranges should all get picked up.

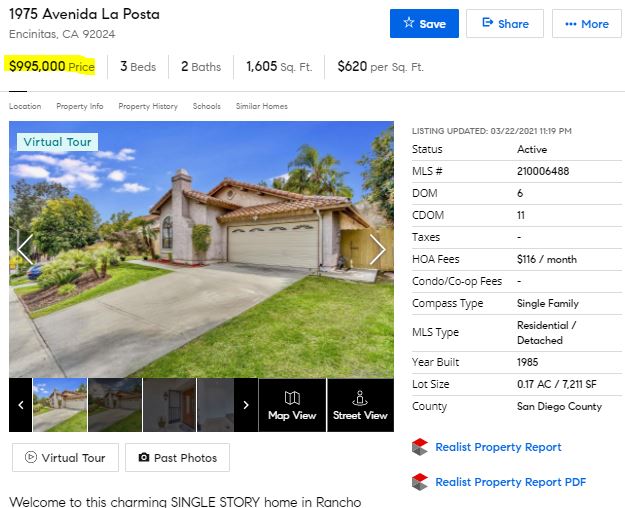

They had EIGHTEEN OFFERS on this one, because it checks most of the boxes. Well-priced single-level with nice private yard that’s been tastefully renovated. The 17 other buyers will be battling it out for months on these! I commend the listing agents for providing enough access to accommodate that many people and offers.