Previously I said that buyer-agents are getting cut out of the action.

There are so many reasons why:

Commissions are grinding down. Buyer-agents have to sell more, to make the same $$.

Working at higher price-points requires advanced skills. Can agents improve?

Are you good enough to convince the buyer to pay your fee? It’s coming.

Fewer listings will be exposed to the buyer-agents, and to the public.

Smart sellers who offer a bounty, or reward, to agents will attract the most eyeballs, buyers, and offers. It is a system, powered by the MLS, that has worked well for decades. But it is coming to an end, sadly.

The pending lawsuits against NAR and major brokerages will likely cause the de-coupling of the commissions, and sellers won’t be able to offer a bounty (commission) to buyer-agents.

But buyer-agent commissions have already been dropping over the last two years, in part because the listing-agent teams don’t respect or care about outside buyer agents. During the frenzy, the listings sold themselves, so why not just keep most of the commission? Or all of it?

What will happen post-frenzy?

The frenzy conditions that pushed prices much higher have devastated the move-up/move-down market. Homeowners love living here, and if they have to leave town to make selling their home worth it, they aren’t as interested.

As a result, it looks like the amount of listings will keep dropping:

Detached-Home Listings between La Jolla and Carlsbad

Year

Total Number of Listings, Jan-May

Total Number of Listings, May

2017

2,287

507

2018

2,222

523

2019

2,274

502

2020

1,855

485

2021

1,780

408

2022

1,330

316

Even after mortgage rates rose dramatically, the number of new listings last month were way below previous months of May. As it gets more difficult to sell and potential home sellers get discouraged about not getting astronomical sales prices, the listing counts could dwindle further.

In the squeeze, listing agents will get more desperate and choose not to share their hot new listings with outside agents, or even within their own brokerage. Buyer-agents who are dependent upon the MLS for homes to sell just won’t have any product.

It’s already happening – the homes you see on the open market seem like the leftovers. It’s already happened with commercial listings on Loopnet, and new-home tracts don’t want to pay buyer-agents at all:

It’s inevitable that the same mindset will infiltrate the residential resales too. Buyer-agents will get squeezed out because nobody wants to pay for them, regardless of how valuable their service might be.

Speaking of infiltration, the impact of OpenDoor probably deserves its own blog post. Because NAR sold our website realtor.com (the best thing we had going for us) to a third party, other entities are now advertising their services on realtor.com that will take away business from realtors.

Input an address of a lower-valued home onto realtor.com, and you’ll see something like this:

As listing counts erode, the desperation among agents will heighten. Buyer-agents will be the first casualty, and then buyers and sellers will feel the pinch too as the MLS dissolves and private websites are used sell homes privately:

The frenzy interrupted the need for off-market sales because all sellers and listing agents wanted to go on the open market for the thrill of a bidding war. But as the market gets tougher, the off-market sales will likely resume. In the process, the buyer-agents will be the first to go, and because there are already way too many agents (at least twice as many as we need), many other agents will face an early retirement too.

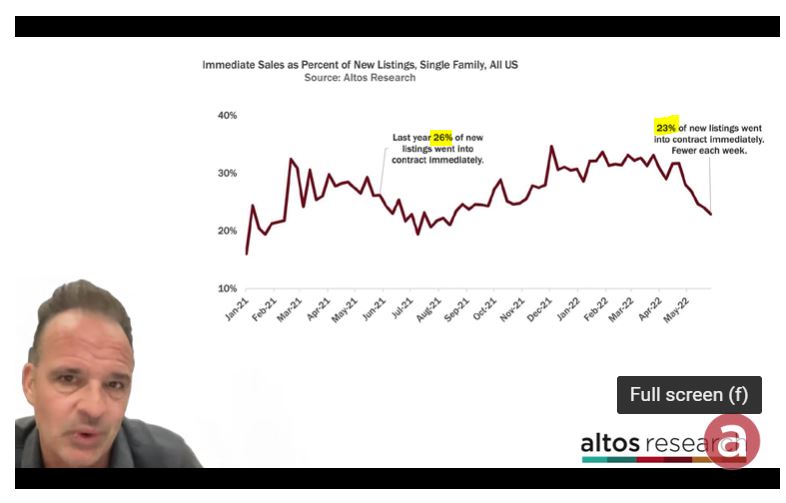

Mike is one of the more level-headed analysts, probably due to the wealth of national data he processes. There will probably be a solid undercurrent of activity as evidenced in the graph above:

Mike’s tweet:

Prices, meanwhile are still strong. 5 bidders instead of 50 bidders will still support your asking price. Prices holding up stronger than I expected frankly. $449,000 for the median single family home in the US now.

We’re going to be hearing for months about how sales are dwindling.

It’s mostly due to comparing 2022 stats to last year’s numbers, which were the most frenzied-up numbers ever. But it is also due to it being a market for the affluent now.

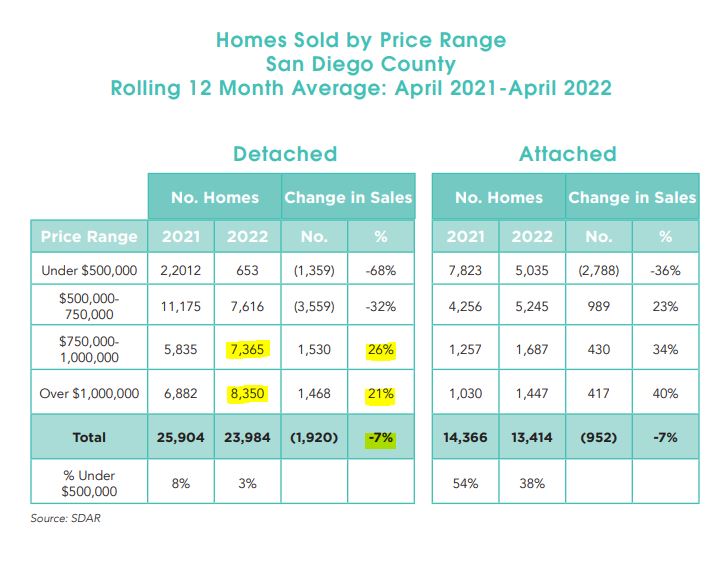

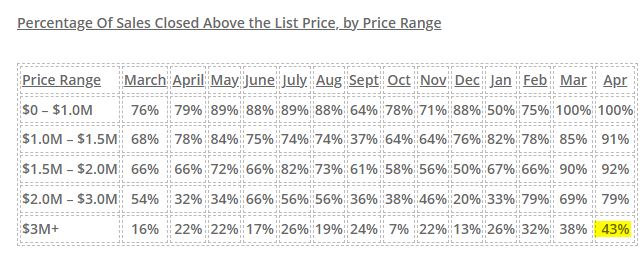

Look at the chart above. Even though sales are down 7% overall, the higher-end sales are booming:

San Diego County Detached-Home Sales, Jan 1 – May 31

Year

SD County Detached-Home Sales

Sales Over $1,000,000

2017

9,889

1,449

2018

9,154

1,570

2019

9,002

1,581

2020

7,683

1,496

2021

9,769

3,177

2022

8,267

3,786

As recently as 2019, the million-dollar sales were only 18% of the total sales count. This year, it’s 46%, and we still have a week more of sales plus late-reporters to record. It could hit 50%, just three year later!

Yet the total number of 2022 sales will only be 10% to 12% behind those in 2021, the craziest year ever.

Plus, if there were more quality homes for sale priced over $1,000,000, we’d have even more sales!

The new market conditions will bear some resemblance to the past, but to believe that real estate sales will be ‘getting back to normal’ some day would be full of false hope. Rob Dawg said it long ago – we need to abandon all previous assumptions.

Let’s start with the two things most likely to change:

Buyers are going to stop paying over the list price.

Buyers are going to stop making offers the minute a house hits the market.

The frenzy conditions that sellers have enjoyed over the last two years will now be in question, and take some finesse to navigate. If buyers are reluctant to pay over the list price, it means that they may even want to pay less than the list price. Then for some listings, there might not be any buyers – at least none willing to pay close to list.

What’s worse is that buyers and their agents won’t be comfortable making low offers, so they just won’t offer at all. Sellers who get no offers will only know that their price is wrong – they won’t know how wrong. Plus, they might not even get any showings, let alone offers.

What variables will make the difference between selling, and not selling?

Comps aren’t going to matter much. Just because there are high sales nearby doesn’t mean that tomorrow’s sellers are going to automatically get the same money or more – especially if the new listing has a defect or unusual feature.

The differences between schools is getting fuzzy. We have become a little too reliant on the online school reviews, and there are going to be parents who spread negative stuff around – and unfortunately, there might be some truth to it. No school is perfect, and the best education is a good upbringing at home. If that’s the case, then why pay larger-than-ever premiums to be in the ‘best’ school district? Some buyers will be attracted to the better home values further out in the suburbs.

Work-From-Home is here to stay. If you WFH and already considering private schools or taking a chance on the lesser-known public schools, then the need to pay a big premium to be closer to downtown won’t be as urgent and the outskirts will benefit. Plus, there is a new car-pool lane on the I-5! The homes that have multiple spaces to accommodate the work-from-home buyers will benefit.

The easy cure for higher prices & rates is buying a smaller house. Before buyers think about sacrificing on location, they will consider buying a smaller home – and most people can find a way to live with 3,000sf to 4,000sf. As a result, the big bombers aren’t going to get the same $/sf for square footage over 4,000sf unless they have larger yards with a pool. It means we should see 4,500sf and 5,500sf homes selling for about the same price – which is different than it’s been.

Smaller yards should get penalized. While a smaller house might work, those with tiny yards won’t be as appealing post-frenzy. At these prices, buyers will be reluctant to compromise on the most-important stuff, and having a decent yard is high on the list.

The homes that have everything going for them should continue to be popular and sell for a premium.

The rest? The price gap between the dogs and the creampuffs should widen, and market times extend dramatically as sellers and agents will be slow to react.

Sellers will be smart to spruce up their home more than they had planned, make sure their price is attractive, and hire a great realtor!

I mentioned that we could be seeing a pause in the market, and for prospective home buyers, there are plenty of reasons to take a rest:

Mortgage rates starting with a 5, not a three.

The S&P 500 and Dow are down 15.9% and 11.3%, year-to-date.

The list prices of homes for sale are higher than comps.

There are very few superior homes coming to market.

It’s a good time for graduation/vacation season!

When I look at the current batch of unsold homes, I don’t see any surprises. Either they are inferior homes/locations, or the list price is too optimistic (or both). It’s natural to add a little extra mustard to a list price so the optimism isn’t a complete turnoff if the home has been upgraded nicely and is well presented.

Buyers taking their time and being more picky about what they will tolerate is a good thing for everyone. The sellers who do everything right (spruce-up, price attractively, and are easy to show and sell) will be rewarded, and those who don’t will languish.

It is a big change from the last two years when the frenzy caused buyers to jump for the inferior or overpriced homes AND pay over list for them too. Those days are gone.

If you see more than an occasional quality home not selling, then we have bigger problems. But for now, buyers could just be waiting for some quality inventory at a decent price!

Of the 109 houses that have closed escrow this month, only 22 of them sold for less than the list price. Eight percent sold have for list price or higher!

Happy to report that the new custom contemporary in Cardiff whose proceeds were going directly to the Rancho Coastal Humane Society did sell for $6,750,000 cash or $1,650,000 over it’s list price:

The homes on the market today were priced according to comps from 1-4 months ago, which were the craziest-priced sales in the history of real estate.

To make matters worse, sellers are naturally drawn to the highest-priced sales – and today that means the ones that closed for hundreds of thousands above the list price. But there was probably only one buyer crazy enough to pay that price.

Then rates go up to the mid-5s, which to buyers feel like double what they were.

But the sellers have committed to their list price, and their ego is laid out bare for all to see – friends, family, neighbors – all are watching and waiting to see if another house is going to sell for an insanely high price.

What happens if it doesn’t sell right away?

The sellers have to be motivated enough about moving that they will address the results. Many have been on the market for weeks without selling – and have they even received an offer yet?

They didn’t get this far in life without being smart enough to know that something different is needed. But there are only three choices:

Cut the price.

Wait it out at this price.

Cancel the listing.

That’s it, those are the choices.

Most will add a fourth choice – it’s my agent’s fault! If my agent would only advertise more, and do more open houses, and well, heck, do whatever agents are supposed to do to sell my house for my price, then it would sell! But you can spend a million dollars on advertising, and it still won’t sell if the price isn’t right.

This is why the market won’t adjust for a long time. The gap between those crazy comps from yesteryear and what more rational buyers will pay today has never been so wide. It’s probably not 5% or 10% either.

The craziest buyers have already purchased, and left us with unattainable comps. The only question is whether there are any somewhat-crazy buyers left, or if it’s just the rational buyers.

Tip: Throw out all the sales prices of the comparable homes that have sold nearby, and just use their list prices. Those list prices were probably rooted in reality (hopefully), and then in all the commotion, one of the craziest buyers radically overpaid just to win the house. Their purchase price is unlikely to be achieved again, at least for the foreseeable future, but those list prices should be a good starting point.

Even though real estate is local, the homebuyer psychology tends to be similar across the country – mostly because people are people, and have similar reactions to every variable. When they see mortgage rates go from 3% to 5.5% in less than six months, it’s only natural to want to pause and see where this goes.

But the desperation among buyers – especially those who are out-of-towners and don’t own a home here yet – hasn’t changed, due to the low inventory. It is unsettling to see so few of the quality homes coming to market, and they want/need to stay in the game so they don’t miss out. It would take a flood of new listings to change that, which isn’t happening. At least not yet.

Let’s have the statistics help guide us on current market conditions.

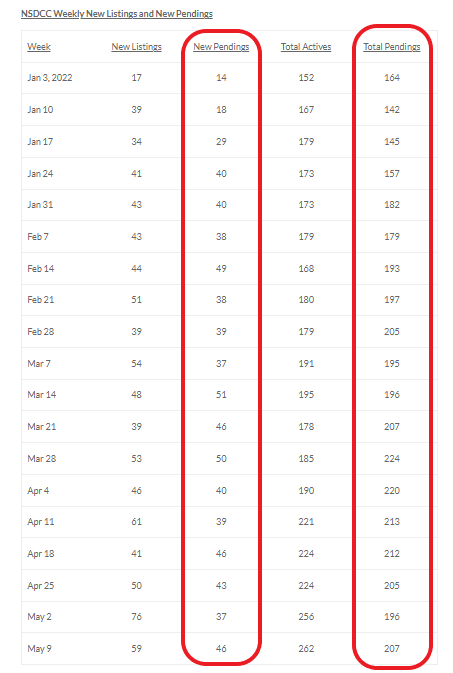

1. We have considered the local real estate market to be ‘healthy’ when the active listings to pendings has been 2:1 ratio. Here are the detached-home listings between Carlsbad and La Jolla:

Monday:

Actives: 262

Pendings: 207

Thursday (today):

Actives: 262

Pendings: 202

The current ratio is very healthy, and the actives aren’t exploding. Last year at this time there were 330 active listings, so only having 262 homes for sale in an area with a population of 300,000+ people isn’t bad. The only startling part is that there aren’t more homes for sale!

2. Let’s talk absorption rate, another measuring stick for the health of the market. The historic norm for a healthy market has been a 6-months’ supply of homes for sale. In recent years, a 3-month supply has seemed to be more realistic, just because the supply has been limited.

What is it today?

There were 225 sales in April, so the 262 active listings is only a 1.2-month supply. We would need 675 active listings to have a three-month supply, which sounds impossible in the current environment.

3. How about the market time of the current pendings? Is it taking longer to find a buyer these days? Yes. The median days-on-market for homes sold in the early months of 2022 has been nine days. The current pendings have a median days-on market of 12 days, which isn’t alarming and still extremely low.

4. Have the number of actives and pendings been consistent in 2022?

Yes, especially the pendings:

So while there is talk about a shift in the market, it may just be a pause. Statistically, the market looks steady – there isn’t a surge of unsold homes, and there are still plenty going into escrow every week.

If there aren’t as many buyers looking, and there aren’t crazy numbers of offers, then it’s just going back to a more-normal market. Not normal yet, but heading that way.

The list prices have been on a rampage, and it’s probably time for them to stop going up so much every month. It was going to happen sooner or later, and that day has probably arrived – finally!

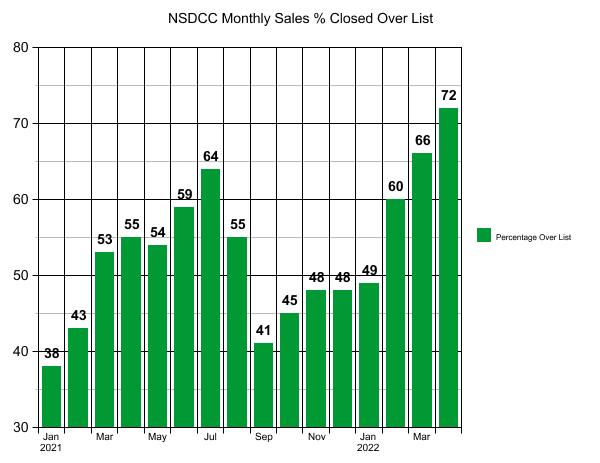

Will April be the peak month of buyers paying over the list price?

NSDCC Detached-Home Sales, % Closed Over List Price

Hard to imagine that there will ever be another month where nearly three-quarters of the home buyers end up paying over the list price!

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

How about those $3,000,000+ home buyers!

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

NSDCC Average and Median Prices

Month

# of Sales

Avg. LP

Avg. SP

Median LP

Median SP

Feb

224

$2,298,797

$2,257,334

$1,719,500

$1,758,000

March

252

$2,295,629

$2,260,524

$1,800,000

$1,825,000

April

357

$2,396,667

$2,403,962

$1,799,900

$1,828,000

May

300

$2,596,992

$2,581,715

$1,900,000

$1,994,500

June

348

$2,509,175

$2,537,953

$1,900,000

$1,967,500

July

311

$2,421,326

$2,442,738

$1,795,000

$1,855,000

Aug

268

$2,415,075

$2,438,934

$1,897,000

$1,950,000

Sept

278

$2,479,440

$2,445,817

$1,899,000

$1,987,500

Oct

248

$2,754,470

$2,705,071

$1,899,000

$1,899,500

Nov

199

$2,713,693

$2,707,359

$1,999,000

$2,100,000

Dec

189

$2,686,126

$2,664,391

$1,985,000

$2,157,500

Jan

140

$2,828,988

$2,855,213

$2,234,944

$2,240,000

Feb

156

$3,058,406

$3,104,854

$2,149,500

$2,386,500

Mar

206

$3,254,033

$3,342,384

$2,425,000

$2,625,000

Apr

224

$3,205,239

$3,267,447

$2,372,500

$2,575,000

Whoops – after the average sales price went up 7% MoM in January, 9% in February, and 8% in March, it dropped by 2% in April.

Same here – after the median sales price went up 4% MoM in January, 7% in February, and 10% in March, it dropped 2% in April too!

The median sales price could drop another 15% this year and still be in positive territory for 2022. Yet it would feel like a complete meltdown of epic proportions!