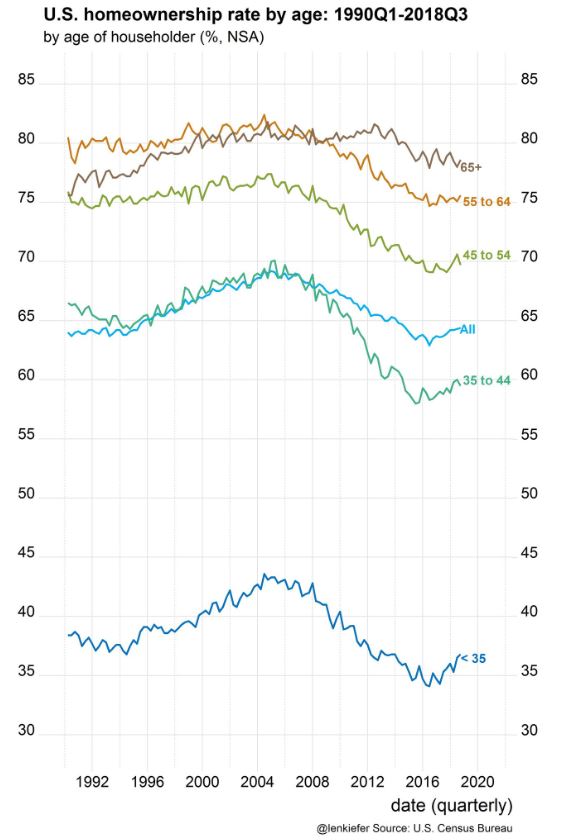

This is the Deputy Chief Economist at Freddie Mac:

It is incredible to see the trend change in every category around 2016 – as if there was a societal shift that gave permission to get back in the game.

Maybe that’s when the Bank of Mom and Dad kicked in, and their distribution of wealth made it possible to buy even though prices were soaring?

Or the resurgence from lower-end buyers enabled the move-up market?

Of all the other choices over the last 40 years, I’ll take the last four years as my favorite trend line!

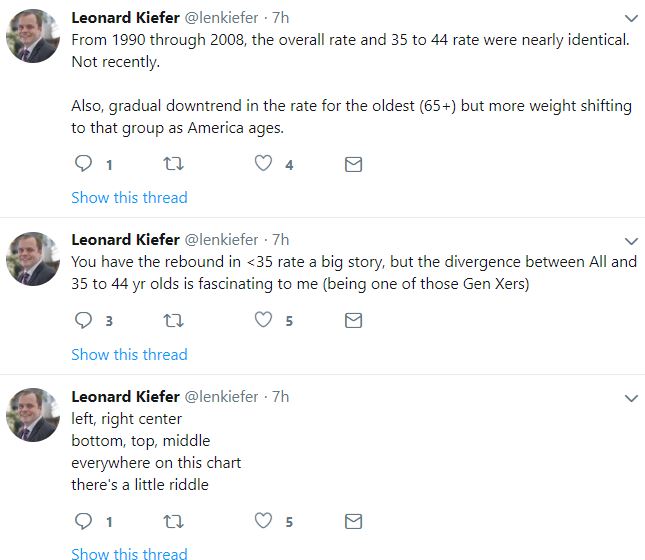

Thornberg has been the most level-headed analyst since the bust:

The annals of postwar Southern California real estate history are full of boom-and-bust cycles, with periods of sharp price appreciation that suddenly skid to a halt. Whether those ups and downs offer any guidance — or hope — for today’s homeowners is a subject for debate.

Some of those who study the housing market predict annual price increases will slow. Others think values could dip. But there is general agreement that a meltdown is not in the offing, given a healthy economy and dearth of home building. The current slowdown,saidChristopher Thornberg of Beacon Economics, “is a bump in the road.”

This time around, the risk of a crash from overborrowing is minimal, if not nonexistent, experts said. Reforms after the financial crisis dramatically tightened lending standards. Today, even though lending has eased somewhat, borrowers are more likely to be able to afford their loans.

That’s borne out in the data:

Mortgage lending is relatively restrained. Last decade, total mortgage debt consistently grew by double digits. In the second quarter, those debts rose only 3.5% from the same period a year earlier, Federal Reserve data show.

Homeowners aren’t as squeezed. Total U.S. mortgage payments in the second quarter accounted for 4.2% of total disposable personal income, the lowest level in at least 38 years. The rate was in the 6% range for most of the mid-2000s bubble, and it hit 7% just before the crash.

Borrowers are less risky. The median credit score for those taking out a mortgage in the second quarter was 760, compared to a bubble-era low of 707.

“I don’t think we need to worry this time around about a bursting of a credit bubble,” said Stuart Gabriel, director of the Ziman Center for Real Estate at UCLA. “We can cross that factor off the list.”

There are times when the general market is in a funk and homes aren’t selling – when it’s easy to think, “Oh this is it, we’re cooked”.

There are also times when the market erupts, and a series of homes that have been languishing for months and/or homes that appear overpriced go pending – which then triggers additional pendings nearby.

Our market is having one of those surges right now!

Not just a couple here and there – we have had dozens of NSDCC homes go pending in the last 10-14 days that have been listed for months, or priced so high you’d think they don’t have a chance.

You sure want to be on the market when that happens!

Richard and I both sold our listings featured here on Friday, and in my case, Tom’s house was the third one listed over $900,000 in South Oceanside to go pending in the last week!

We had a real fixer for sale in La Costa – a house that had undergone six months of demolition, and was left with no kitchen or baths. In a picky market, these are the types of homes that get left behind, right?

For those who want to build out a project your way, have I got a deal for you!

The architect drew up plans for a 3br/3.5ba house plus a 1br/1ba granny flat, and they just needs the finishing touches. Last sale nearby was 7503 Solano St for $975,000 in June.

Will not qualify for conventional financing – no kitchen or baths currently:

Youtube walking tour here:

After 13 cash offers and five escrow, Jim closed this at $650,000!

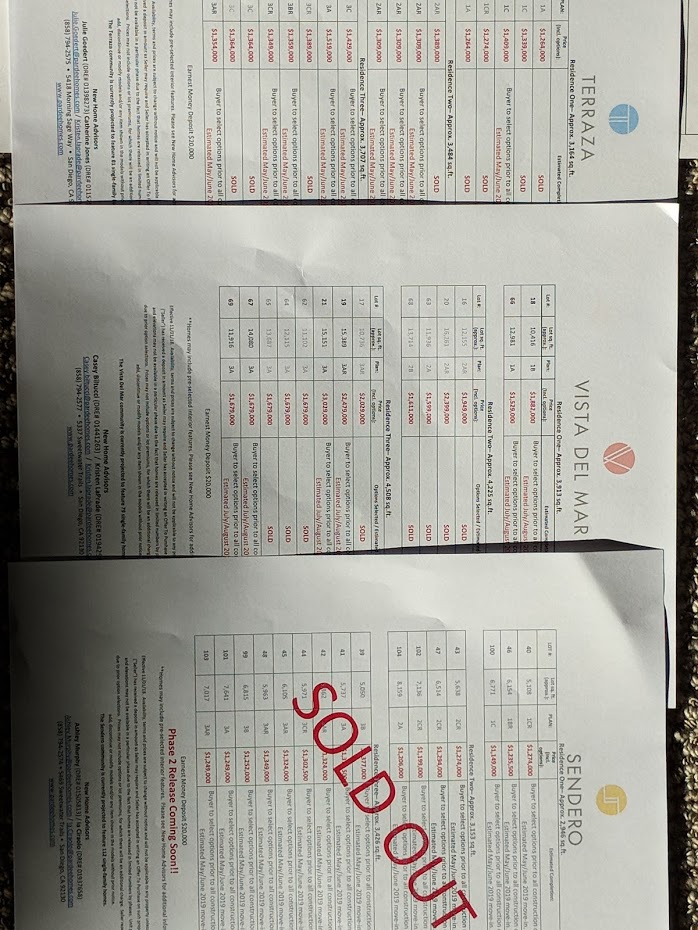

Pardee has four new tracts of homes in Carmel Valley. There will be a total of 377 houses here, plus a fifth tract (and the highest-priced), Vista Santa Fe, which is opening in January.

The grand-opening-after-the-pre-opening is this weekend and remarkably they have already sold 3/4 of the homes released for sale.

Prices are $1.6M to $2.4M in Vista Del Mar. Here’s a tour of the Plan 2 model:

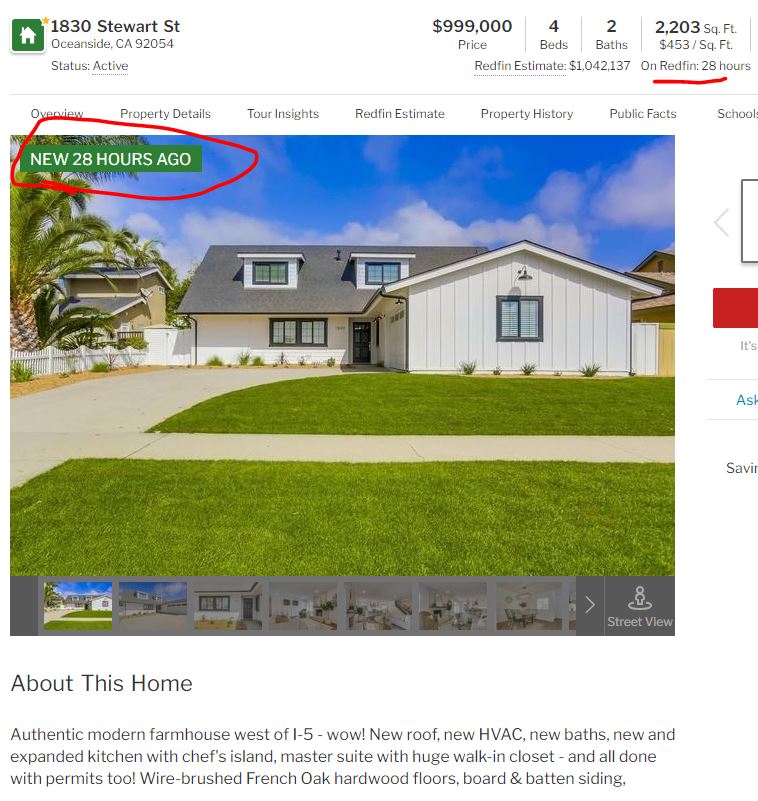

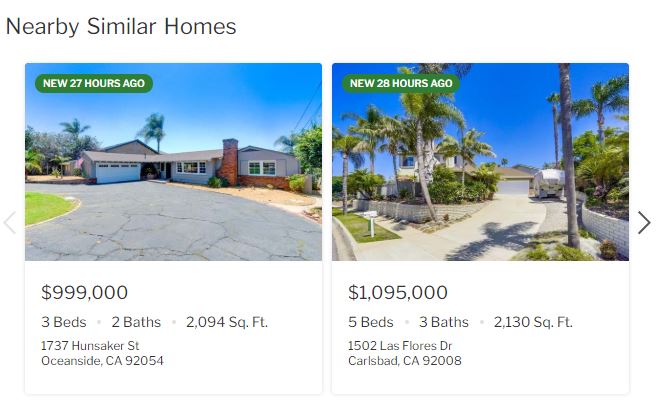

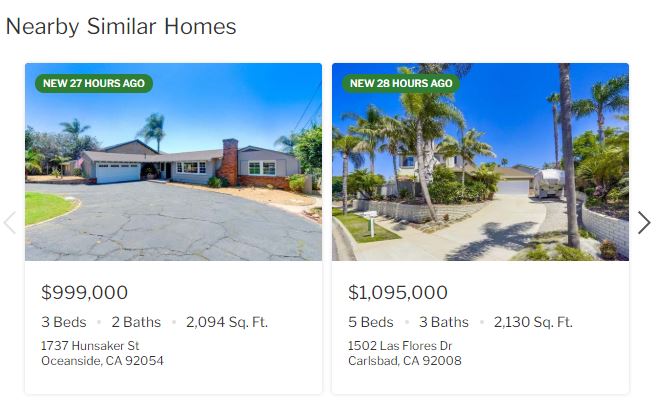

Tom saw that Stewart had a new banner on Redfin, and he wondered if I refreshed the listing on the MLS. I didn’t, and when I checked, the other listings nearby that have been active for months had the same look:

Buyers are probably smart enough to figure it out. But in case it brings more eyeballs, we lowered the price to $989,000 and we’ll have open house 12-3 on Sunday! Three other listings within a couple of blocks of us went pending in the last week, so it’s been hopping in South O!

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

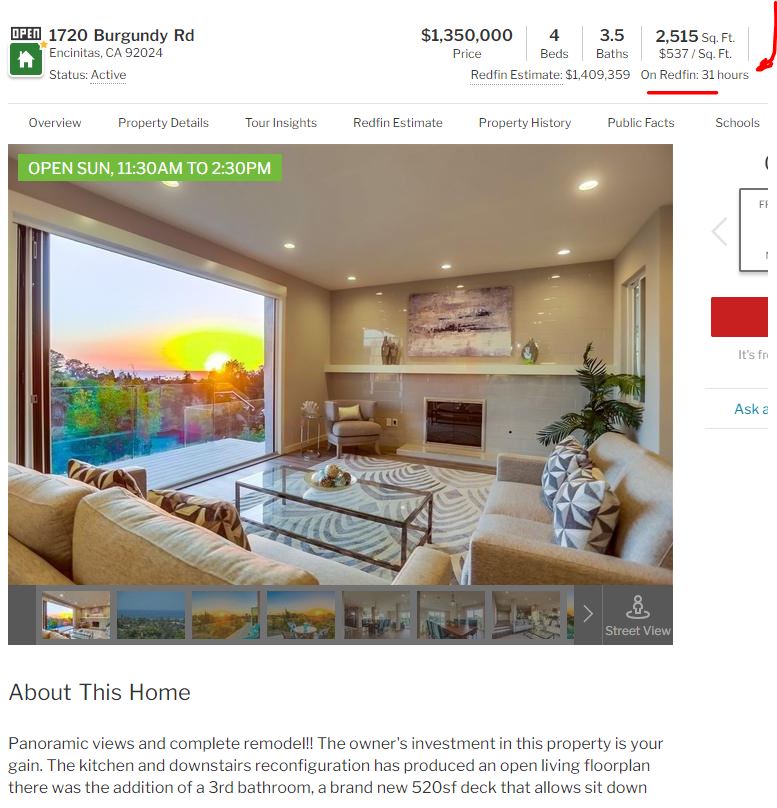

The same thing happened to Richard, so maybe it is system wide?

He also dropped the price, ($1,299,000) and NO OPEN HOUSE – PENDING!:

We have a fundamental problem in the housing market – how it works today.

New listings are distributed within minutes these days, and waiting buyers are on the edge of their seat. Those who were already frustrated with high prices, higher rates, and coming soons want to get it over with and buy now – and they either jump immediately on the good ones, or they swipe to the next offering.

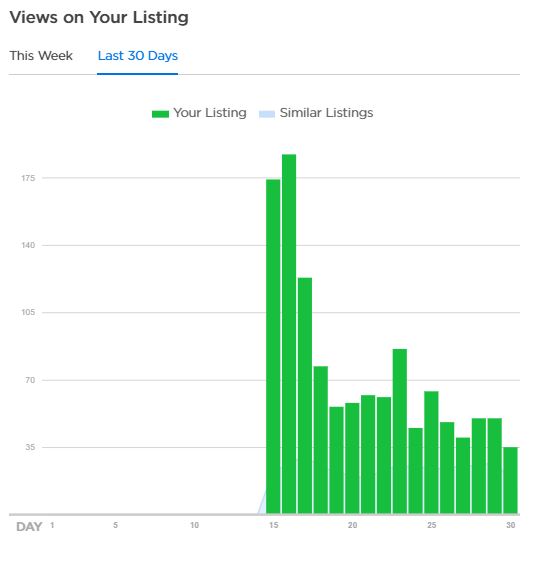

The graph above show the Zillow views of my one-story listing in La Costa Ridge. Look how quickly the interest fell off. The bump on Day 9 was when we lowered the price $100,000, and literally by the next day it was old news.

What’s the problem?

Sellers are unaware.

Once they figure it out, it is natural to resist, and the real estate industry makes no attempt to educate sellers on this dilemma. Maybe agents aren’t aware either, or are uncertain what to make of it?

It doesn’t matter when prices are rising – sellers can just wait until the market catches up with their price, which has been the preferred method forever. But in a stalled/stagnant/soft market, prices aren’t coming to meet you – and they might be going to other way. It could be years before they do catch up.

We expect selling a house to be like every other job – put in a good effort for weeks or months, and at the end we will have success.

But selling a house in this environment gets more-frustrating/less-rewarding with the longer it goes on.

Will sellers resist the temptation to add a little extra to their list price, and instead employ sharp pricing to sell early and for a higher amount?

They should, because buyers are dying to beat down the prices of the stale old listings, and their pricing expectations will be dropping far faster than sellers. It will get harder and harder to put deals together on the older listings.

It’s simply an educational thing for the new market conditions – if you price your home to sit, not sell, you will be sitting much longer than before!