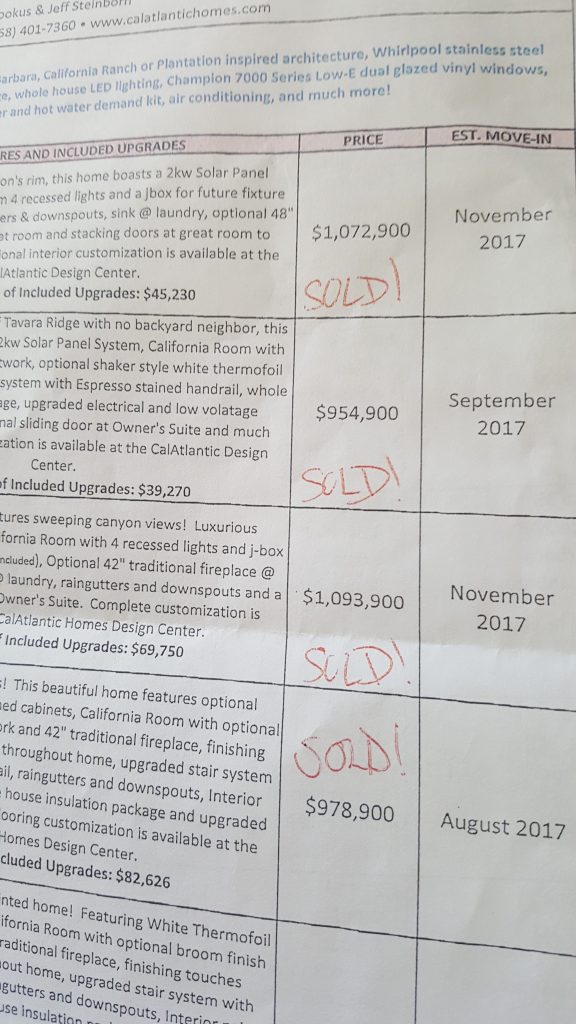

Here’s a video tour of Tom’s latest project, and discussion about his business. The master suite in back was two bedrooms that he combined, and re-configured to create a large walk-in closet and right-sized master bath.

Note how he hit all the hot buttons: curb appeal, canyon lot, cantina doors, white kitchen with marble-like counters and high ceiling, great room, and quality master suite.

This will be for sale this weekend around $750,000:

The head of Bank of America Corp, the United State’s fourth-biggest mortgage lender, said on Thursday banks would be able to supply a bigger share of funding for home purchases if the standard down payment for buyers was cut to 10 percent from 20 percent.

The vast majority of mortgages are underwritten to strict standards set by the U.S. government or quasi-government entities Fannie Mae and Freddie Mac. While down payment requirements can vary, they offer fairly little latitude to lenders that do not want to take all the risk themselves. As a result, many prospective homebuyers who cannot come up with a 20 percent down payment are unable to get a loan.

“Our goal – going back to regulatory reform – is should you move the down payment requirement from 20 percent to 10? It wouldn’t introduce that much risk but would actually help a lot of mortgages get done,” Chief Executive Officer Brian Moynihan told CNBC in an interview Thursday.

Bank of America was the top U.S. mortgage lender ahead of the 2008 mortgage crisis, causing it to face greater losses, both from defaults and litigation, than any other bank. Under Moynihan, who took the helm at the start of 2010, the bank has tightened lending standards and executives regularly use the motto “responsible growth” in public speeches.

“Real Estate Wars,” a Bravo-TV reality show pitting Orange County agents against one another as they try to woo wealthy clients and settle bitter scores against a backdrop of luxury homes, will debut on Thursday, July 6 at 10 p.m.

The show “brings the cut-throat world of real estate in Orange County to life,” Bravo said in its announcement on Thursday, May 18. “With 10 agents, eccentric clients, multi-million dollar deals, old vendettas, and one common goal of winning, all is fair in real estate and war.”

U.S. Treasury Secretary Steven Mnuchin has taken pains to stress that the Trump administration isn’t out to kill Americans’ beloved mortgage-interest tax deduction — but a side effect of the plan could turn it into a perk for only the wealthy.

President Donald Trump has proposed rewriting the tax code to raise the standard federal deduction to a level where about 25 million homeowners would no longer take advantage of the century-old break.

A married couple would need a home-loan balance of about $608,000 — almost triple the mortgage on a median-priced U.S. home — before using it would make sense, according to a new analysis by property-data provider Trulia. That would be up from about $322,000 today.

Without the incentives, along with a proposed end to local property-tax deductions, home sales may be hurt in cities where prices are rising quickly and buyers are stretching to afford their purchases, from Denver and Portland to Boston and Washington, D.C. Reduced demand would weigh on values, causing price declines nationwide, according to the National Association of Realtors, which opposes the change.

The proposal “is a backdoor way of rendering the mortgage-interest deduction close to worthless,” said Mark Zandi, chief economist for Moody’s Analytics.

Prices may fall 10 percent on average nationwide, taking into account the lack of deduction for state and local property taxes, according to a preliminary estimate prepared by a consultant for the National Association of Realtors. Zandi, of Moody’s, said the proposed deduction changes would reduce prices by about 4?percent nationally, including the property-tax impact, with bigger decreases in pricier parts of the country.

Economists have been critical of the mortgage-interest deduction because it disproportionately benefits people with more expensive properties, including many who would have purchased even without the break. It also inflates home prices because buyers often overestimate their tax savings when they’re budgeting for a purchase, said Dennis Ventry, a professor at University of California, Davis, School of Law who has studied the program’s history.

Trump’s plan might boost homeownership rates over time because a drop in prices would improve affordability and the standard deduction would give buyers more money to spend on a house, Ventry said.

The real-estate industry is lining up against the proposal, including the powerful National Association of Realtors, which spent $10.2 million lobbying Congress in the first quarter, more than any other organization except the U.S. Chamber of Commerce, according to the Center for Responsive Politics.

Trump’s plan also targets tax deductions for state and local taxes paid — a provision that would hurt homeowners in states where property taxes are high.

“One of the big reasons for homeownership is the ability to deduct property taxes,” said Coldwell Banker Realtor Kevin Cascone, who’s based in Westfield, New Jersey. “If that’s eliminated, what’s the difference between renting and buying?”

The temperature on Sunday is expected to be 77 degrees in Solana Beach for the Fiesta Del Sol. Pato Banton takes the stage at 7:45pm, and the parking lot will be rocking the Jamaican reggae beat!

IRS data for 2015 shows 207,861 tax filers — a good estimate of households — from other states lived in California the year before. We may miss those old relatives or friends, but they add up to only 1.48% of 14 million California filings. Only Michigan had a lower exits-to-population ratio.

California’s departure rate is far less than the national norm, which shows movers between states account for 2.14 percent of all U.S. filers. States that did a poor job at keeping its taxpayers included Utah (losing 2.33 percent of its filers); Arizona (2.72 percent); and Nevada (3.32 percent). These Western states, frequently cited as popular places for ex-Californians, have out-migration challenges, too.

The data also shows us the incomes that move with migration patterns.

To be sure, it’s eye-catching to see what departing Californians took with them: a combined taxable income of $16 billion in 2015. When you consider total incomes of Californian filers of $1.22 trillion, though, the outflow is only 1.3 percent of dollars earned – again, the second-best rate among the states (behind Michigan) and better than the national average of 1.8 percent.

Who’s leaving the state? IRS data suggest those with less wealth: the average income of movers was $77,000 per filing in 2015 vs. $87,000 statewide. But the tax data also shows California’s ability to retain population beats the national average at all six income levels broken out by the IRS — from those with little income to those making $250,000 or more.

Please note that one bit of homebuying data also shows Californians are pretty geographically stable.

When Attom Data Solutions ranked five dozen major U.S. markets for how long recent home sellers had lived in their homes, five of the 12 markets with the greatest tenure were in California. Plus, the average length of ownership had grown by two years since 2012 to above 10 years in some cases.

In 2015, California gained 197,200 new filers with total incomes of $13.9 billion. But that’s tiny vs. the state’s huge population and economic heft. On a per-capita basis, only four states — Michigan, Ohio, Wisconsin and Illinois — fared worse in bringing in new taxpayers.

So, why have you heard tales of data showing large numbers of Californians leaving the state?

One often quoted metric is what is called the “net migration “– the difference between inbound and outbound.

Yes, population and tax data shows California with a negative net migration – more departures than arrivals. However, the seemingly large raw number of California exits is actually relatively modest when you compare it to the state’s scale as the nation’s most populous state.

IRS data shows 10,700 more departing Californian filers than arrivals, moving a “net” income of $2 billion out of state. Only three states — New York, Illinois and New Jersey — lost more “net” dollars in 2015. But when you see that net outflow in terms of California’s $1.11 trillion in taxable income, the state ranks 27th — middle of the pack – in proportional net income loss.

It was bound to happen: A homeowner has filed suit against online realty giant Zillow, claiming the company’s controversial “Zestimate” tool repeatedly undervalued her home, creating a “tremendous road block” to its sale.

The suit, which may be the first of its kind, was filed in Cook County Circuit Court by a Glenview, Illinois, real estate lawyer, Barbara Andersen. The suit alleges that despite Zillow’s denial that Zestimates constitute “appraisals,” the fact that they offer market value estimates and “are promoted as a tool for potential buyers to use in assessing [the] market value of a given property,” meets the definition of an appraisal under state law. Not only should Zillow be licensed to perform appraisals before offering such estimates, the suit argues, but it should obtain “the consent of the homeowner” before posting them online for everyone to see.

In an interview, Andersen told me she is considering bringing the issue to the Illinois state attorney general because it affects all owners in the state. She has also been approached about turning the matter into a class action, which could touch millions of owners across the country.

In the suit, Andersen said that she has been trying to sell her townhouse, which overlooks a golf course and is in a prime location, for $626,000 — roughly what she paid for it in 2009. Homes directly across the street, but with greater square footage, sell for $100,000 more, according to her court filing. But Zillow’s automated valuation system has apparently used sales of newly constructed houses from a different and less costly part of town as comparables in valuing her townhouse, she says. The most recent Zestimate is for $562,000.

Andersen is seeking an injunction against Zillow and wants the company to either remove her Zestimate or amend it. For the time being she is not seeking monetary damages.

Emily Heffter, a spokeswoman for Zillow, dismissed Andersen’s litigation as “without merit.”

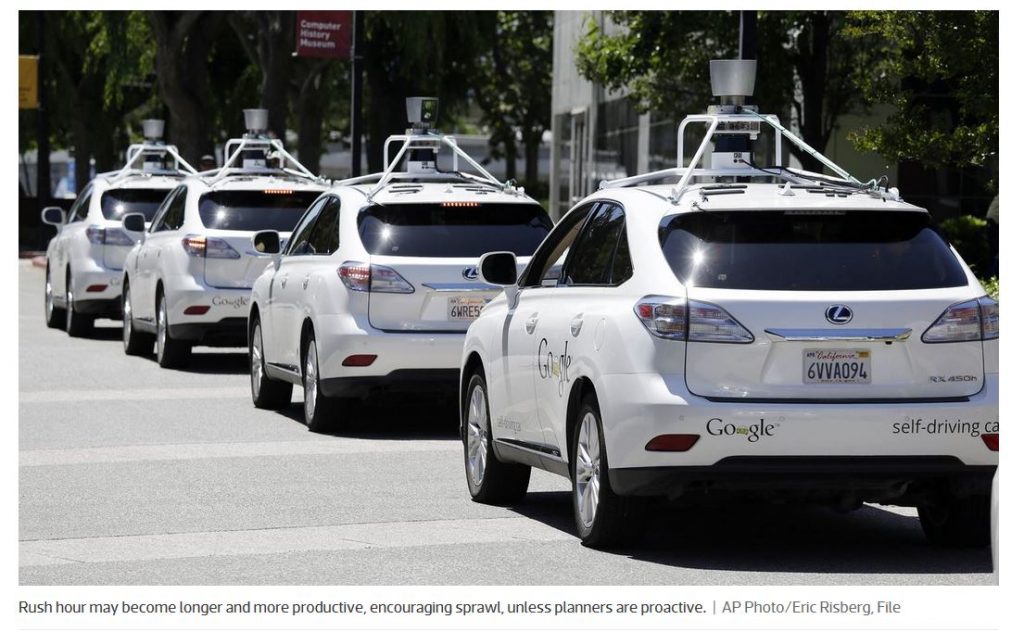

The futuristic vision offered by automated vehicles—the freedom to be active during your commute instead of wasting away behind the wheel while stuck in traffic—isn’t quite as utopian a scenario when you run it past cautious and concerned city planners.

The convergence of three new technologies—automation, electrification, and shared mobility—has the potential to create a whole new wave of automation-induced sprawl without proper planning and regulation.

“This will completely change us as a society,” says Shannon McDonald, an architect, assistant professor at Southern Illinois University-Carbondale, and an expert in future mobility planning. “I think it’ll have the same transformational change as the introduction of the automobile.”

Real estate firms will negotiate for fewer parking spaces, perhaps even setting up their own agreements with autonomous bus or transportation-network companies, such as Uber or Lyft, to provide tenants with transportation access in exchange for gaining more usable, high-value urban space. Though banks and financial institutions will need to get on board with the concept, this would offer a new way to add density, and could help spur more mixed-use, walkable cities.

The question marks around AVs cut both ways; some believe AVs could also be tools for sprawl, since commutes will suddenly be more enjoyable and “not everyone can live in funky lofts.”

Just as driverless car technology will speed up a change in the way cities think about parking allowances, it’ll also accelerate a shift in how we design roadways, specifically pick-up and drop-off zones for vehicles. The growth in services such as Lyft and Uber are beginning to make this issue clear, but as autonomous vehicles eventually hit the streets, the way buildings and developments welcome and adapt to traffic flow will become increasingly important.

“Our streets aren’t designed for door-to-door service,” says McDonald.

New land-use rules and traffic codes will need to be designed to properly funnel AV traffic and prevent what could be a series of bottlenecks on the road, especially during rush hours, as people get to and from work and school.

Redesigning parking lots and entrances to be less about static parking and more about increasing the flow of dropoffs and pickups, as well as serving as staging areas for driverless cars not in use, will both free up space and ideally protect roadways from potential congestion.