From Thanksgiving through New Year’s Day, there are 20% fewer $1 million-plus listings, and they spend an average 35% more days on the market, compared with the peak buying season in May and June, according to Realtor.com. The study looked at 10 major markets, including New York, Chicago, Washington, D.C. and San Francisco, from January 2014 through September.

But there is a jump in activity in the second week of December—a 10% rise in signed contracts from the previous week, followed by a 5% bump in closings. “It’s sort of like a second wind from the crazy summer activity,” said Javier Vivas, an economic-research analyst for the site. It is fueled by a wave of price cuts and new listings in November, and a fear of what’s to come: January through the end of February is 10% to 20% slower than December in most markets, he said.

Alternative types of credit scoring have been around for years, taking into account factors not always captured by traditional scores, such as whether borrowers pay their cellphone bills promptly. They’ve been used to assess the creditworthiness of consumers with little or no traditional credit history, including those in developing countries.

Now, a new generation of start-ups has developed scoring models that look at such things as what a borrower studied in college and how a restaurant rates on Yelp — and they’re using them on a wider audience, from businesses to individual borrowers with middling or even good credit.

The abundance of digital information, and the rapidly growing storage and computing power able to comb through it all, is changing industries including agriculture and healthcare. It should come as no surprise, then, that it’s shaking up consumer finance.

Proponents say these new methods should help borrowers gain credit, just as it has helped farmers increase their yields.

“In banking, it’s inconceivable that in the future we’ll be making financial decisions in the way we do today. We’re making decisions about people based on less than 5% of the information about them,” said Asim Khwaja, a professor of international finance and development at the Harvard Kennedy School who has studied alternative credit scoring in the developing world. “There’s a lot of excitement in this field.”

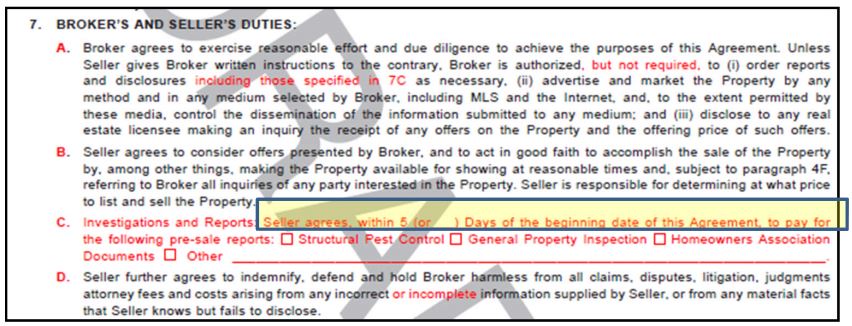

The C.A.R. legal department issues contract revisions twice a year, and they tend to be ticky-tack minor changes.

But the 2016 listing agreement will include a new paragraph that has sellers agree to pay for pre-sale reports!

When used correctly by listing agents, these reports should provide major benefits to all parties:

Enable sellers to make strategic repairs prior to going on the open market.

Provide preliminary findings for the buyers to consider when negotiating the sales price – giving them more comfort, which should mean higher price.

Alleviate any major hurdles at the repair-request stage – the second negotiation that happens about two weeks after the original deal is consummated.

I think buyers will still conduct their own home inspection with an inspector of their choice. But if all that does is confirm what they already knew, then they will be hard-pressed to convince the sellers that there are repairs to negotiate – heck, they were already baked into the price, weren’t they?

The current purchase contract already says that the property is sold ‘as-is’, and that the sellers aren’t obligated to complete any repairs.

If our standard practice shifts to providing HOA, termite, and home-inspection reports to all buyers (by simply attaching them to the MLS listing), then we should see all homes actually sold ‘as-is’, and the price paid by buyers better reflect the actual condition of the home (at least better than current practice).

It will also give listing agents a few more days to find their own buyer too, so we’ll probably see more ‘sold before processing’.

Construction workers in downtown Los Angeles are racing to finish Metropolis, the biggest mixed-use development on the West Coast.

When its three towers are completed sometime in 2018 – if all goes according to schedule – more than 1,500 condos will be added to Los Angeles’ scarce housing market, but some of the buyers probably won’t be spending much time living there.

Other developers have tried for decades to raise enough financing to turn the six-acre Metropolis site into something other than parking lots. The only one to pull it off has been Greenland Holding Group, a Chinese state-owned real estate behemoth. Bankers and real estate lawyers say a big reason why it has succeeded where so many others have failed is because Greenland has a big advantage: a direct line to millions of potential buyers in mainland China.

“It’s relatively easy for them to bring to their Chinese customers’ attention that they have this exciting project in Los Angeles,” said Mike Margolis, a partner at the Century City-based law firm, Blank Rome, who frequently advises Chinese companies doing business in the U.S. “That’s a ready made market for them.”

“They have been very successful at selling to Chinese buyers,” said Pin Tai, President of Cathay Bank.

Chinese buyers are attractive because about 70 percent of them pay all-cash, according to a 2015 National Association of Realtors survey.

Tai says it’s especially important to lock in those buyers first, because after the financial crisis, most banks require up to half a building to be under contract before they’ll approve a mortgage.

“It’s like building the foundation first,” said Tai. “It’s low hanging fruit.”

Architecture firm Olson Kundig, have designed Studhorse, a home for a family that loves adventures, located in Winthrop, Washington State. The house is situated in a place where the climate ranges from hot, fire-prone summers to winters that have heavy snow.

The house is composed of four buildings, centered on a central courtyard and pool. “It’s like a little campground, and you go tent to tent. The materials are tough on the outside, because of the high-desert climate, but the inside is cozy, like getting into a sleeping bag—protected, warm, and dry,” says the architect.

The impact on mortgage rates from yesterday’s Fed move was priced in already, and it’s doubtful we will see any short-term change in our local real estate market conditions.

But the Fed also indicated that they intend to ‘gradually’ raise their target range for the Fed-funds rate. At what point will buyers start to react? How will they react?

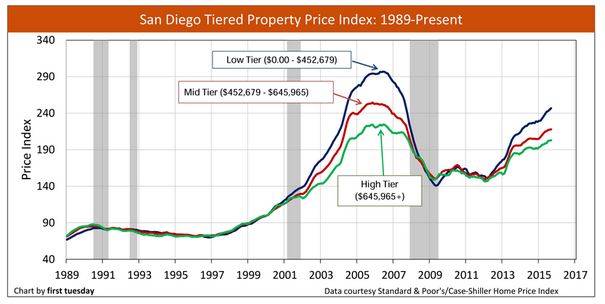

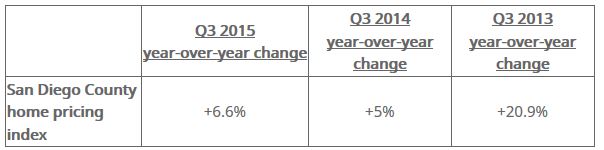

The general statistics for San Diego have been greatly enhanced by the lower-end being red hot. Look at the difference between the blue and green lines in the pricing chart above – the 2015 pricing velocity in the Low Tier has been much greater than with the High Tier, and it’s the lower end that will be more affected by rising rates.

We saw how mortgage rates in the 3s this year helped to turbo-charge the lower end, giving us the illusion that the overall market benefited – see below:

The price of low-tier housing in San Diego County skyrocketed after the latter half of 2012, peaking in Q3 2014 and leveling off after. 2015 has experienced another price increase. This is likely due to the boost given by decreased mortgage rates throughout 2015.

Lower mortgage rates free up more of a buyer’s monthly mortgage payment to put towards a bigger principal. Thus, San Diego’s high home prices continue to find fuel — not from speculators as in 2012-2014 — but from increased buyer purchasing power.

Expect home sales volume to fall off after mortgage rates begin to rise in the second half of 2016. Prices will descend 9-12 months later, by the second half of 2017.

I think we will see declining sales next year as sellers try to push higher, and buyers resist. Lower-end buyers will be stymied by higher rates, and buyers on the higher end will be overwhelmed by the bulging inventory – there were 85 houses sold over $1,500,000 last month, and there are 870 for sale in San Diego County!

Prices? It will take a long stretch of stagnant before all sellers believe they need to lighten up.

If we saw price declines in the general stats by the end of next year or 2017, to what point will they be coming back? To 2015 prices? To 2014 prices? Neither would change the overall market much – houses will still be expensive.

The Fed made their move….finally! Here’s a good explanation from MND:

Mortgage rates moved just slightly lower today, despite the long-awaited Fed rate hike. Once again, that’s LOWER mortgage rates and a HIGHER Fed rate. Here’s how that works:

The rate that moved higher today is the Federal Reserve’s Target Rate. This is the rate banks charge other banks to borrow money overnight. It’s called the Fed’s Target Rate, because the Fed doesn’t actually directly enforce the rate. It merely “targets” the rate (or the range of rates, in this case) that it believes is in line with its policy goals. The Fed can then employ several tools to influence the overnight rate and bring it in line with the target range.

If you’re not already well-versed in the reasons that banks borrow from other banks overnight, don’t worry about that. All you need to know is that the Fed’s target rate is vastly important to the global financial system, and it has far-reaching effects on all manner of interest rates.

In other words, a Fed rate hike is a big deal, but bigger to some than others. Mortgage rates are less directly connected to the Fed’s Target Rate, as could be easily seen in today’s modest move lower. The Fed hiked its rate by a quarter of a point–an amount that would be unimaginably severe in the mortgage world. Such a move has only happened a few times in history on a single day.

The caveat is that mortgage rate movement is given plenty of time to roam free, day in and day out. Meanwhile, the Fed rate only moves when the Fed announces it, which is almost always at one of their meetings. Those only happen 8 times a year. In other words, mortgage rates have had time to do whatever they needed to do to get ready for today’s Fed rate hike. The bottom line is that mortgage rates do, in fact, care about the Fed rate to some extent. They’re simply not joined at the hip.

In terms of specifics, today’s mortgage rate movement was very small. Most lenders continue to quote 4.0-4.125% on top tier conventional 30yr fixed scenarios.

A story with great examples of golf courses being closed across the country, and many being turned into real estate developments.

From the nytimes.com:

BOCA RATON, Fla. — Weeds, crabgrass and fallen palm fronds cover the wildly overgrown greens of what was once the Mizner Trail Golf Club, its decrepit state emblematic of the fate of hundreds of golf courses around the country, many of them derisively known as “rabbit patches” or “goat farms.”

A short drive away, however, perspiring construction workers in yellow vests swarmed on a recent afternoon over the emerging structure of a 150,000-square-foot activities center, part of a $50 million renovation of the 44-year-old Boca West Country Club, home to some 6,000 residents, where fairways are newly planted and houses sell for as much as $5 million.

With the winter golf season beginning in Florida — the nation’s leader in golf courses with more than 1,000 — the extremes of failure and success point to a nationwide upheaval in the sport. It was booming when players like Tiger Woods reigned, but has since been roiled by changing tastes and economics, an aging population of players, and the vagaries of the millennial generation’s evolving pastimes.

There are about four million fewer players in the United States than there were a decade ago, according to the National Golf Foundation. Almost 650 18-hole golf courses have closed since 2006, the group says. In 2013 alone, 158 golf courses closed and just 14 opened, the eighth consecutive year that closures outpaced openings. Between 130 and 160 courses are closing every 12 months, a trend that the foundation predicts will continue “for the next few years.”

Dozens of private and public golf courses here in South Florida, and hundreds around the country, are in transition. Some courses have sought bankruptcy protection, while others have slipped into foreclosure. Many are under construction, with single-family homes and condominiums going up on land once dotted only with pin flags, sand traps and water hazards. Others have gone to seed as they await resolution of legal and zoning disputes.