While there are still plenty of buyers waiting for more inventory/lower prices/lower rates, this month’s sales and pricing combination will rival those at the previous peak.

Let’s estimate this month’s sales and pricing.

Over the last three days of June, 2012, we closed 70 sales.

If we add that 70, plus 10% of total for late-reporters to the current total of 244 closings this month, it equals 345 estimated sales. It is typical that the cost-per-sf stays about the same, so if we wind up around 345 and $459/sf, we be similar to 2004 when the market had been scorching:

June Sales and Average Pricing, NSDCC Detached-Homes

Year

#Sales

Avg $/sf

Business Days in Month

2002

337

$316/sf

20

2003

360

$331/sf

21

2004

376

$455/sf

22

2005

304

$483/sf

22

2006

264

$492/sf

22

2007

267

$501/sf

21

2008

202

$441/sf

21

2009

203

$379/sf

22

2010

256

$385/sf

22

2011

251

$373/sf

22

2012

339

$368/sf

21

2013

345

$459/sf

20

To close roughly the same number of sales while the average pricing went up 25% since last June is remarkable – and similar to the last peak era when the no-doc neg-am loans were the rage and average pricing jumped +37% from June 2003 to June 2004.

In the coming years, will we see a similar trajectory as last time, or will the environment of low-fixed-rate loans and low inventory keep it steady?

An excerpt that suggests one reason why prices are going up:

In some cases banks are choosing to hold onto distressed assets longer, hoping to minimize losses on homes by artificially tamping down distressed inventory levels now. So when a home comes available in a foreclosure sale, the lender may choose to repossess it as a future REO than part with it during an auction.

In states like Arizona, that repossession is logged at the value of the mortgage — a “sales price” that may very well be higher than the actual market value of the property, according to Ingo Wizner, president of real estate research firm Local Market Monitor.

Around SD County, it appears that more borrowers have started making their payments. The number of SD filings has dropped off almost by half, Y-O-Y:

Last month had 69% fewer REOs, and 42% fewer 3rd-party sales, Y-O-Y:

Regardless whether the shortage of distressed properties is due to more borrowers now making their payments, increased legislature, or a deliberate shift in banking policy, the foreclosure spigot has slowed to a trickle.

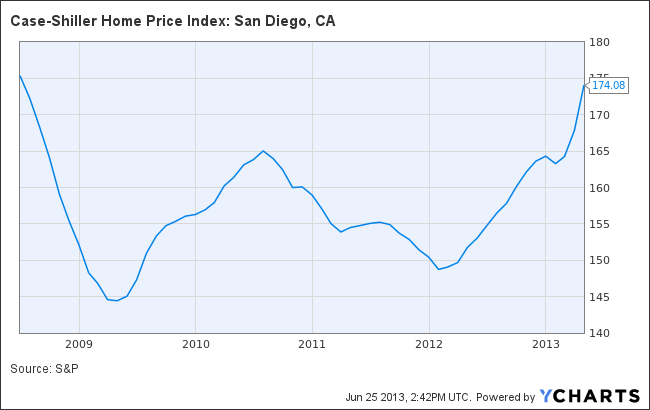

The San Diego Case-Shiller Index for April showed a higher reading, as expected. The February/March/April period was the hottest of the year, and hopefully the index will start moderating in the coming months.

San Diego Case-Shiller Index, Seasoanlly-Adjusted

Month

CSI-SD

Apr ’12

152.74

Mar ’13

170.38

Apr ’13

175.15

M-O-M = +2.8%

Y-O-Y = +14.7%

Blitzer is auditioning for Yunnie’s NAR-cheerleader job:

This latest report only tracks prices on a three-month moving average through the end of April, well before mortgage rates began their climb. Still Blitzer contends rising rates will not slow price gains.

“Home buyers have survived rising mortgage rates in the past, often by shifting from fixed rate to adjustable rate loans. In the housing boom, bust and recovery, banks’ credit quality standards were more important than the level of mortgage rates. The most recent Fed Senior Loan Officer Opinion Survey shows that some banks are easing credit restrictions. Given this, the recovery should continue,” he said in the report.

The more realistic view that applies to bubble areas:

“Today’s Case-Shiller numbers may reflect where the housing market has been in some of the frothier metros, but they are not indicative of where it’s headed. The housing market worm has turned over the past few weeks – inventory levels are beginning to show signs of easing, and mortgage interest rates are creeping up. Going forward, both of these factors will help mitigate extreme price spikes caused by very strong housing demand and very low housing supply,” said Zillow Chief Economist Dr. Stan Humphries.

“Runaway appreciation in many of the large, coastal metros that form the backbone of the Case-Shiller indices will begin to moderate. Home value appreciation in some of these areas will have to slow down, or potentially fall, as higher bottom-line prices are no longer masked by rock-bottom mortgage rates. In general, the national housing recovery is strong and sustainable, but pockets of volatility will emerge as local fundamentals shift. Buyers expecting home values to continue rising at this pace indefinitely may be in for a shock.”

Mortgage rates finally lost less ground than they have over the past few business days. The problem is that this still left room for rates to go higher at a much faster pace than normal.

Some borrowers will have seen their quoted rate move up another eighth to a quarter, depending on the lender. After rising to 4.625% on Friday, Conventional 30yr Fixed best-execution is currently between there and 4.75%. Lenders continue to offer lower rates in exchange for increased upfront costs, but those rates have deteriorated (meaning costs have increased) significantly faster than rates in the best-execution zone.

As we often say, “volatility” is unkind to mortgage rate sheets. The wider the range of potential outcomes lenders are forced to defend against, the less aggressive they can afford to be with rates, regardlessof whether or not today’s rates improved. In other words, an awesome day for mortgage rates is made less awesome by volatility, and a bad day is made extra bad.

In that sense, current rate levels are a product of a double whammy between current trading levels and the need to account for volatility. As of now, volatility should be assumed to be expanding or steady at high levels until we have clear reason to believe it’s receding, and we’re not there yet.

This continues to be one of, if not THE most significant move in the modern history of mortgage rates (in terms of the pace of change).

“The volatility in mortgage rates has been unprecedented. Daily swings cause changes intraday and unfortunately that creates distortion for consumers.

The recent volatility will not subside until the free market determines where the real bid/ask is minus the FED. Until that point expect the swings to continue. 30-45 days should be locking. Longer term may be able to float, however we do not recommend it with the current environment.

We went from low 3’s to high 4’s in a couple of weeks, and this morning we were possibly talking 5’s. The day is not over and the week just begun. ” –Constantine Floropoulos, Quontic Bank

The last period had 73 new listings, and 66 new pendings.

In the last week we had a 100:69 mix of new and pending listings, which should begin a trend that’s closer to the more-normal 2:1 ratio, as more sellers sense the opportunity:

The UNDER-$1,200,000 Market:

Date

NSDCC Active Listings

Avg. LP/sf

DOM

Avg SF

April 29

201

$384/sf

36

2,599sf

May 5

195

$381/sf

36

2,633sf

May 9

207

$387/sf

35

2,624sf

May 18

241

$397/sf

33

2,566sf

May 23

236

$397/sf

34

2,529sf

May 30

230

$391/sf

35

2,591sf

June 5

229

$393/sf

35

2,577sf

June 11

239

$390/sf

34

2,569sf

June 17

246

$389/sf

36

2,577sf

June 24

255

$397/sf

36

2,535sf

The OVER-$1,200,000 Market:

Date

NSDCC Active Listings

Avg. LP/sf

DOM

Avg SF

April 29

620

$806/sf

94

5,183sf

May 5

606

$806/sf

93

5,223sf

May 9

628

$808/sf

93

5,150sf

May 18

653

$807/sf

92

5,161sf

May 23

661

$814/sf

92

5,141sf

May 30

659

$805/sf

95

5,222sf

June 5

663

$794/sf

96

5,185sf

June 11

672

$779/sf

96

5,163sf

June 17

661

$787/sf

99

5,164sf

June 24

679

$791/sf

98

5097sf

Mortgage rates should find some equilibrium in the mid-4%s, and if they do we should see a less-frenzied environment the rest of summer.

The bidding will start with the minimum bid as indicated in the brochure. The Minimum bid may be less than 90% of the appraised value. This is determined by reviewing the current appraisal and selecting the (NOPA) legal process.

The procedure to confirm a sale in court will ALWAYS be an option and at the discretion of the Public Administrator at anytime.

A 10% deposit will be required with the successful bid. The 10% deposit required at the time of the auction must be in the form of cash, cashier’s check, or certified check payable to the “Public Administrator”. Please be prepared to bring 10% of the appraised price listed in the brochure. Should the property be sold for more than the appraisal price, then the difference will need to be made up in the form of a personal check at the time of the successful bid. If a petition to the court is filed for a hearing to confirm sale (Court Confirmation), an overbid procedure will be followed as part of this legal process. Higher bids may be accepted by the court if they are made in court and they are in the amount of at least 10% more on the first $10,000.00 and 5% more on the amount of the bid in excess of $10,000.00 of the original bid submitted for confirmation. Our acceptance of an offer is contingent on the estate’s being able to furnish the buyer a Policy of Title Insurance showing the property to be free of any encumbrances of record, subject to restrictions and easements of record. No termite clearance is given.

Please be advised that you are basing your purchase of an offered property solely on your findings and research, that you have satisfied yourself as to the zoning, usage’s, physical condition inside and out, size and other information that might affect your decision to purchase this property. You understand that you are buying this property in “AS IS” condition with no warranties, usage’s or conditions, (physical or otherwise), written, implied or expressed by the San Diego County Public Administrator’s Office and its agents or employees.

All properties have access through the use of Multiple Listing Service (MLS) lock boxes. Please contact a broker of your choice to view each property.

A real estate broker who registers a client with the Public Administrator and who attends and remains with his client during the auction, will generally receive a commission of 2.5% of the purchase price, awarded by the court. In the event this client becomes the successful bidder, the commission will be paid at the close of escrow. A real estate licensee who buys as a principal will not be entitled to share in the commission if he or she is buying as a principal or intends to share the commission with the principal.

The San Diego County Probate Referees appraise all properties at this auction. Referees are assigned to each estate by the Superior Court of California, and are not affiliated with the Public Administrators office.

All descriptions and information are derived from reliable sources, but no guarantee is expressed or implied. Announcements made on the day of sale will take precedence.

The writer called these ‘pocket listings’ but this activity should be called something else – and the buyer should paying the commission – because a “listing” implies a contract with a seller. If any agent has a written listing agreement with the seller, they have a fiduciary duty to put the listing on the open market – it is what’s best for the seller.

Prof Hoff is selling her inland digs, and what a house!

She and Tom have created an incredible modern contemporary with epic views of the mountains and hills – and centrally located less than an hour from Laguna Beach, Newport Beach, South Coast Plaza, John Wayne Airport, and Staples Center. Only 90 minutes to Sea World or Big Bear!

Diana said, “I’m not so sure that interest rates are worse than rising home prices. We have seen a spike in home prices because of low inventories and that’s a far bigger deal than rising mortgage rates going up a lot.”

If you purchase a home today, there is effect from both higher prices and rates. Let’s compare the difference in costs.

Here are two homes on the same side of the street in Carmel Valley for comparison. The first closed for $714,500 in April, and the second is the same model, asking $757,000-$777,000:

The jumbo-mortgage rates didn’t jump as dramatically this week as the conforming-loan rates. Let’s use a 0.50% increase for the example, and a 20% down payment:

House #1 – Sales price $714,500

$142,900 down payment

$8,574 closing costs (1.5% of loan amount)

$151,474 cash needed

$3,570/mo. PITIHOA at 3.875%

House #2 – Sales price $777,000

$155,400 down payment

$9,324 closing costs

$164,724 cash needed

$4,046/mo. PITIHOA at 4.375%

Today, you need $13,250 more cash, and be willing and able to pay an additional $476 per month to buy the same house than three months ago.

There were also four of this model that sold in the $600,000s last year.

Last June, there was a $680,000 sale, which with 20% down would have dropped you under the high-balance conforming loan limit. The difference? Cash needed was $22,895 less, and difference between the PITI payments was $661/month.

Real estate agent Mickey Knickerbocker was as surprised as anybody when her client closed on a $905,000 Manhattan Beach town house using “piggyback” financing: a two-mortgage deal designed to minimize the down payment.

Popular during the housing boom, piggybacks all but disappeared after the mortgage meltdown taught banks and regulators a big lesson: Borrowers needed to have skin in the game. So the loans seemed like a throwback to the days of carefree lending, especially on such a pricey property.

“I don’t think, a year ago, I could have gotten loans that would have served this purpose,” Knickerbocker said. “I didn’t even know … that this was going to be possible.”

With home prices rising, risk is creeping back into mortgage lending. In addition to creative down-payment arrangements, mortgages on high-end properties — so-called jumbo loans — have also gotten plentiful and cheap. Meanwhile, banks are accepting borrowers with lower credit scores and allowing them to take on more debt relative to their incomes, experts and industry professionals say.