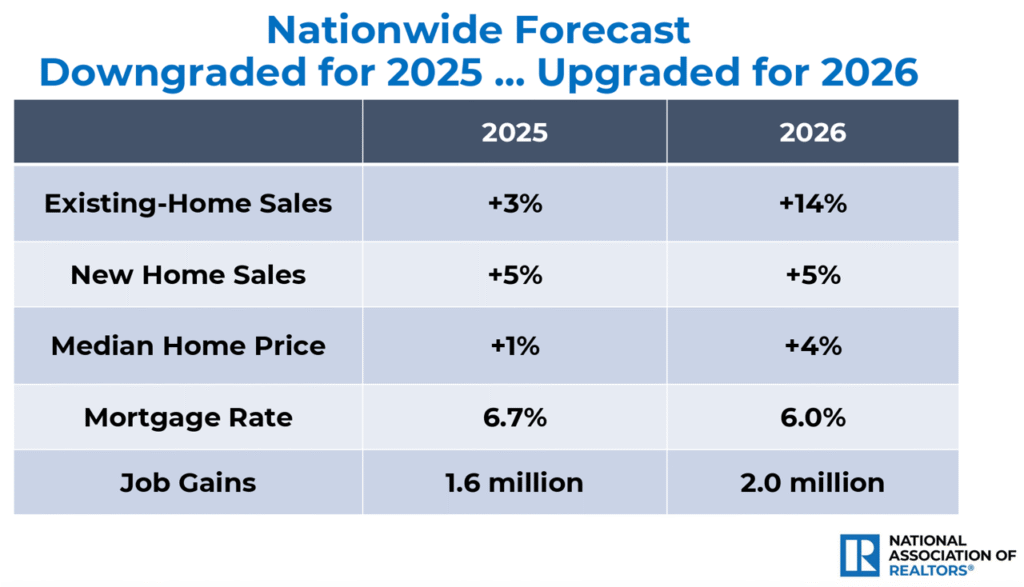

Our national real estate cheerleader at NAR, Lawrence Yun, has published his mid-year forecast. His original forecast for the 2025 Median Home Price was 2% originally, so his downgrade has cut it in half.

I don’t mind him having a revision, but doesn’t his 2026 sound wildly optimistic? He provided no substantiation or research data to back up his guesses.

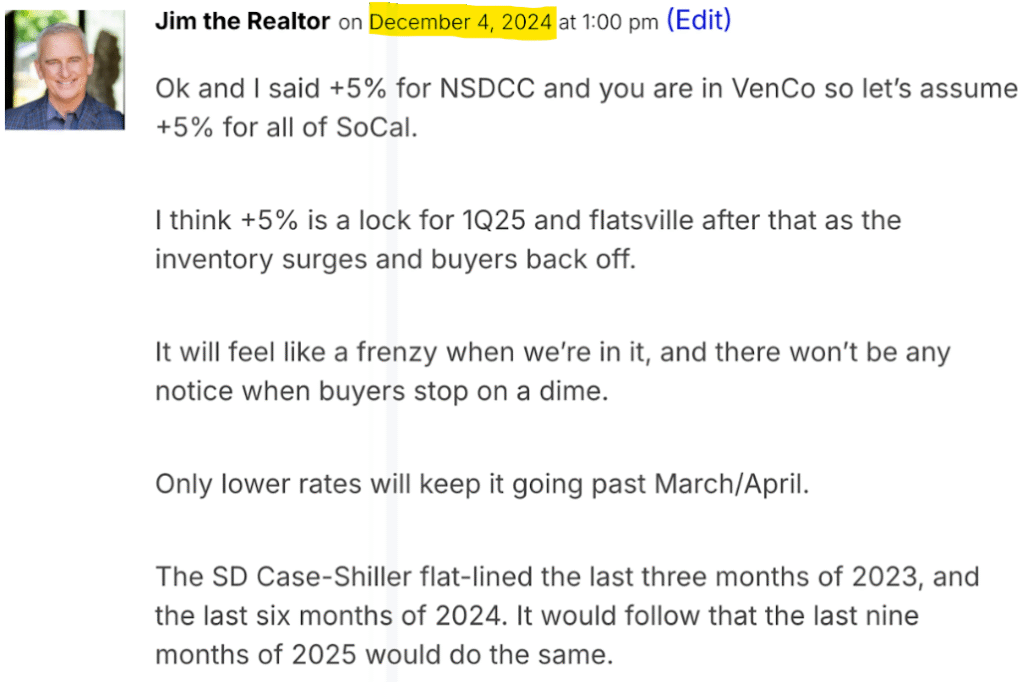

In December, I guessed +5% and there was only +3% in NSDCC appreciation in the first quarter of 2025. My ‘flatsville’ call for the rest of the year is looking pretty good though, and might be optimistic!

Check out this nicely renovated 4br home built on a large 7,600sf lot on a culdesac where three homes have sold over $2,000,000 in the last 18 months – including the house right next door that closed for $2,040,000 in March and was then gutted down to the studs! The house across the street sold for $1,710,000 in 2024 and they tore it down to build a multi-million mansion! What’s the #1 rule in real estate? Buy the least-expensive home on the street! Our listing has new flooring and paint, lighting, fencing, landscaping – and ocean view too, with peek of Catalina Island!

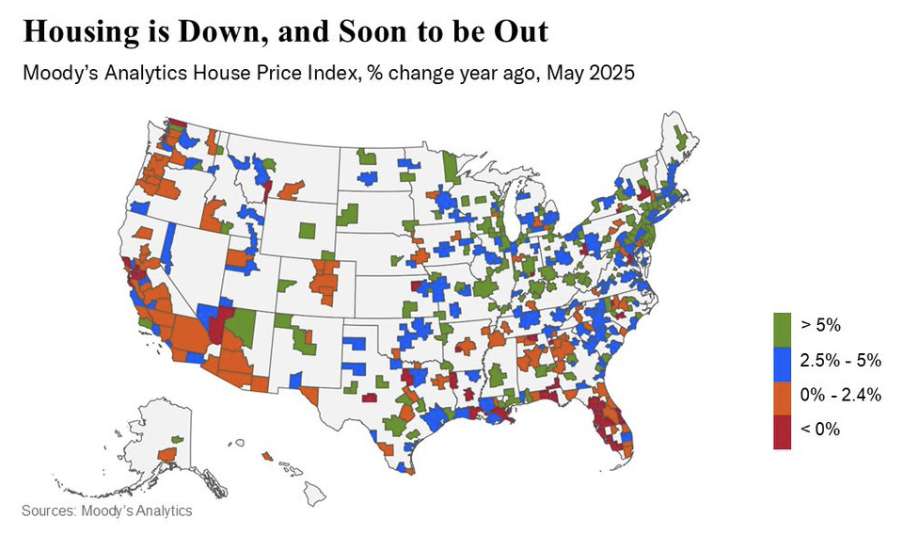

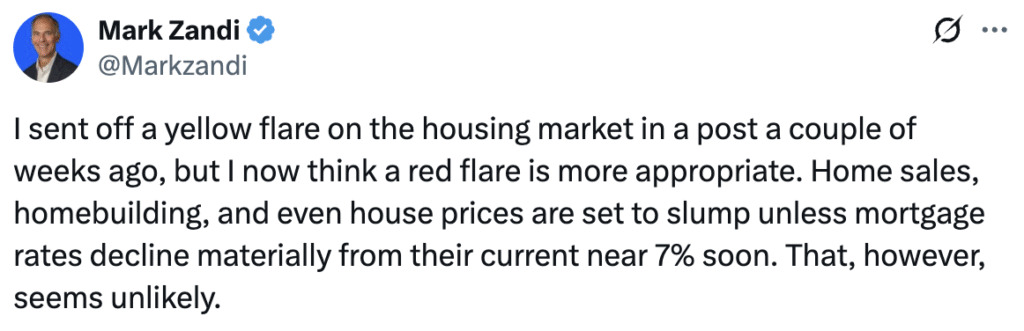

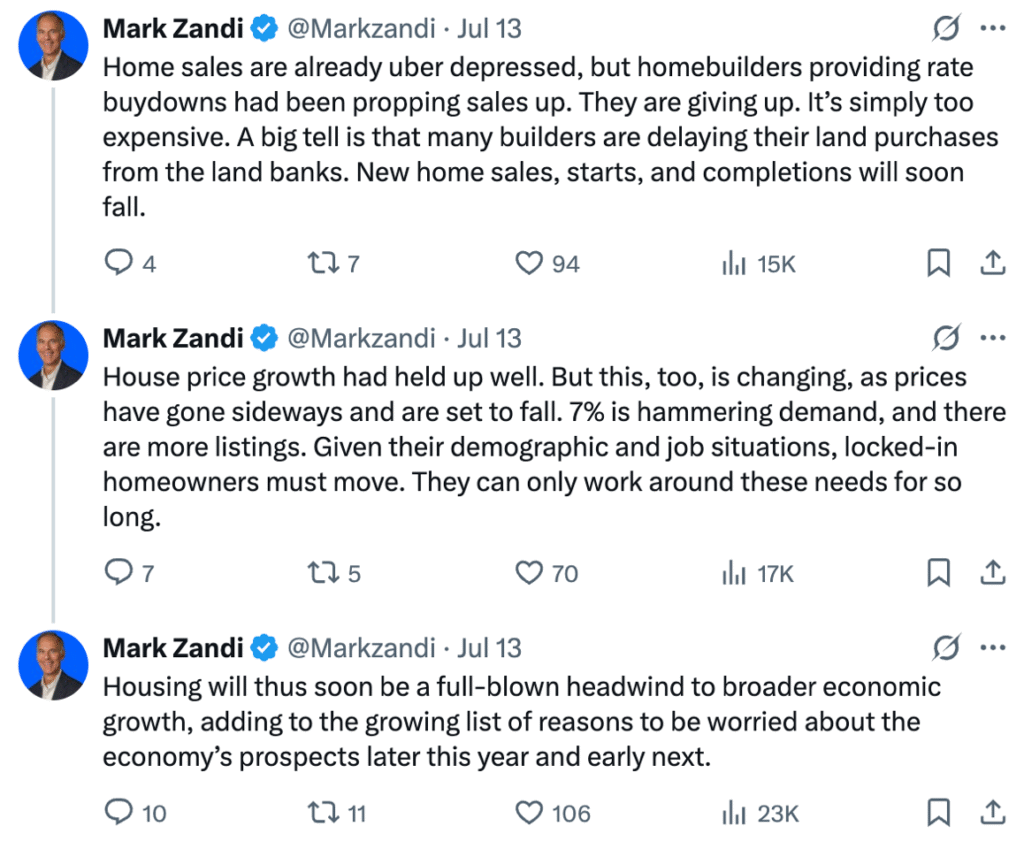

This guy is the most negative bear in real estate so the sensational-media types love him! You will probably see his views expressed elsewhere too, even though he’s been wrong (too negative) most of the time. In his map above, there aren’t many red zones.

For those who can’t get enough twitter doom, here are hundreds of comments:

I was with a handful of realtors the other day chatting it up about the current market conditions. I said, “they remind me of 2007”, which received blank stares. None of them were in the business then!

So I went back to check the statistics to verify. Because next month will be the 20th anniversary of this blog, I included the whole history to see where we’ve been:

SD County Detached-Home Annual Stats

There was a bigger drop in the number of sales between 2006 vs 2005, but the percentage of sales divided by listings was a bone-chilling 34% in 2007 – the largest failure rate ever.

Sales are much lower today, thanks to fewer homes for sale.

Halfway through 2025 and the numbers are similar to last year, but the tide appears to be turning. See my previous post!

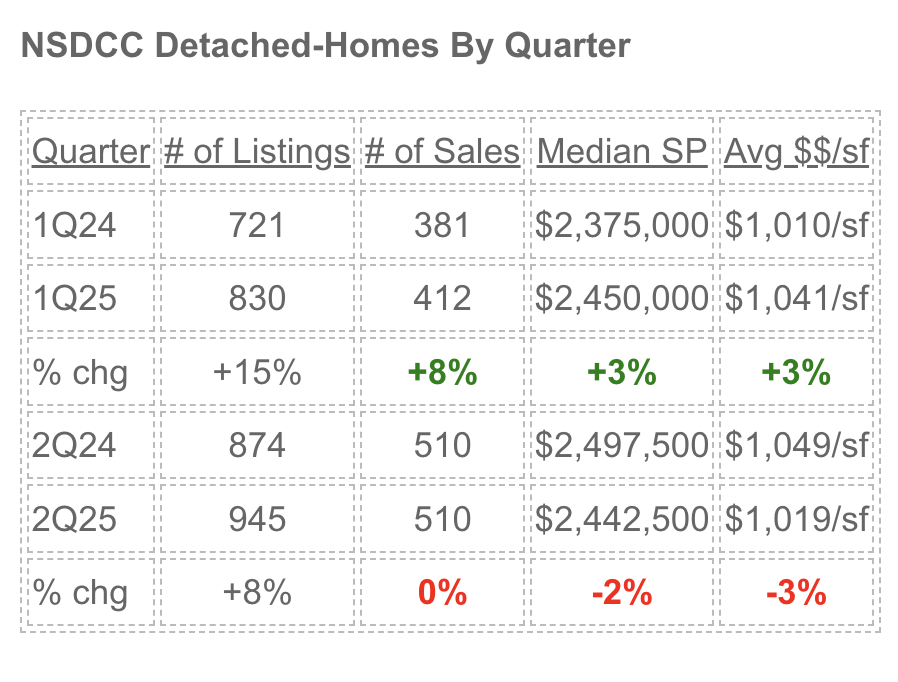

Let’s judge this year by comparing the quarters vs. 2024:

Here’s how the market did between La Jolla and Carlsbad:

Buyers enjoyed the additional listings in the first quarter as sales and pricing both grew considerably.

But as the listing count kept growing, sales slowed and pricing hit the wall.

Note: Statistics are quirky. I checked it three times – the number of 2Q sales was an identical 510 both years! There will be a few more June sales added though before it’s over.

I hope everyone is enjoying the 40th anniversary of Live Aid. The behind-the-scenes with Bob Geldof is fascinating – the first episode ran on Sunday and there are four total being aired on CNN on Sundays.

I remember watching it and loving the effort by Phil Collins who played at Wembley and then flew on the Concorde to play only two songs he knows on piano in Philadelphia:

On July 13, 1985, the world’s biggest music stars gathered for Live Aid, a massive benefit concert to raise money for famine relief in Ethiopia. In a new original series, CNN goes behind the scenes on how Boomtown Rats frontman Bob Geldof and singer-songwriter Midge Ure organized the legendary effort that brought in more than $127 million and drew in about 1.5 billion viewers around the world.

Premiering on Sunday, July 13, at 9 p.m. ET/PT, Live Aid: When Rock ‘n’ Roll Took Over the World celebrates the 40th anniversary of the multi-venue event that featured special performances by Tina Turner with Mick Jagger, Bob Dylan with the Rolling Stones’ Keith Richards and Ronnie Wood and Sting with Phil Collins and Branford Marsalis. The docuseries will feature interviews with Geldof, Bono, Lionel Richie, Patti LaBelle, Sting, Phil Collins and others, and will include archival footage of the event that took place at Wembley Stadium in London and John F. Kennedy Stadium in Philadelphia.

Premiere date: July 13 at 9 p.m. PT/ET

No. of episodes: 4

Channel: CNN

Stream online: DirecTV, Fubo, Hulu + Live TV, Sling

The Live Aid lineup also included Pretenders, Santana, Madonna, Tom Petty and the Heartbreakers, Neil Young, Eric Clapton, Phil Collins, David Bowie, Elton John, the Who, Paul McCartney, Run-D.M.C., Black Sabbath, Judas Priest, Hall & Oates and REO Speedwagon. It also brought reunions of Ozzy Osbourne with Black Sabbath, Brian Wilson with the Beach Boys and the surviving members of Led Zeppelin.

Congrats to Mike for coming on board. With him generating market data regularly, we have as much to gain as anyone at Compass – look for more data from Mike here!

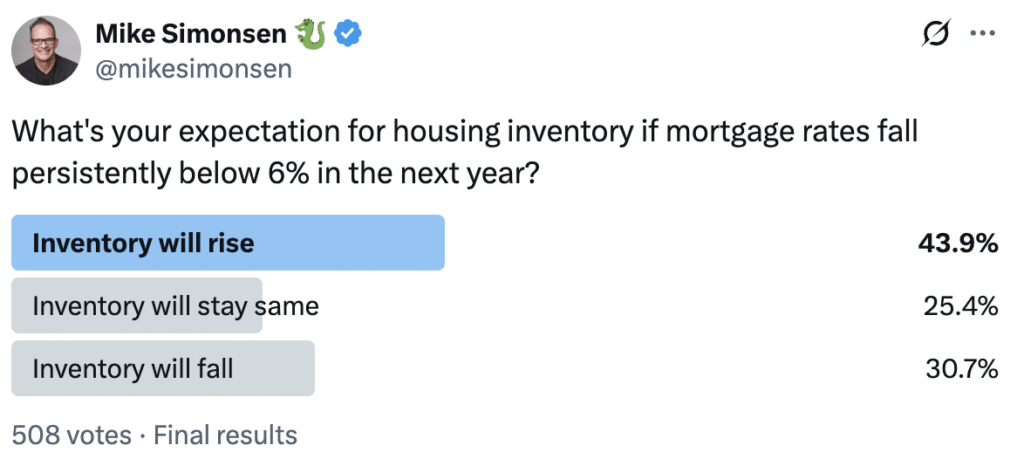

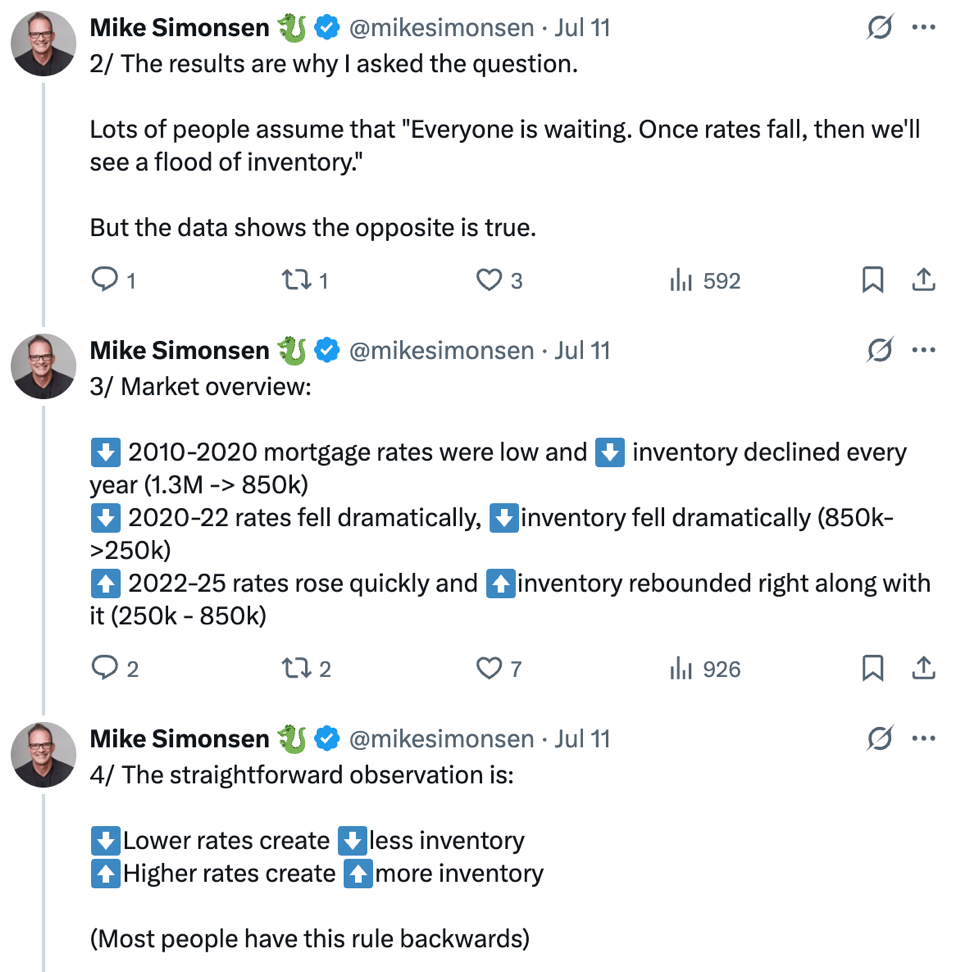

Because there is recent history (the last 15 years) when lower rates coincided with lower inventory, he believes it will happen again. He says that lower mortgage rates motivates all buyers, which causes the demand to move faster than the supply.

In other words, when rates go down, the frenzy conditions will re-appear.

I said the same thing last week – that the current market lull will be over as soon as Trump can get rid of Powell and install a new Fed chief next May who will dump on rates.

But I’ve been thinking about it ever since.

Here’s why I don’t think it’s going to happen and why Mike could be wrong this time. We’ve never had market conditions like this before, so we should throw out all previous assumptions (hat tip Rob Dawg/Giving Cat):

The unsold listings from this year will be coming back to market faster in 2026. Frustrated sellers who dinked around this year will come back firing!

I think Mike is mixing ‘inventory’ and ‘active inventory’. He thinks the additional demand will gobble up the inventory, leaving fewer actives, which makes sense. But I guarantee there will be more listings overall.

The seller’s market has been broken. Buyers didn’t know if it would ever happen, or what it would look like – but this is it. Not sure it’s a full-blown buyer’s market yet, but the sellers have lost considerable negotiating ground.

More sellers combined with cautious buyers means more of what we have now. Low activity with everyone wondering about pricing, now and in the future.

Realtors have jumped the shark.

If the tax-free-home-sale bill gets passed, look out. Will any Republican would oppose it? Paying the extra tax has been the #1 reason long-time homeowners tell me why they don’t want to move. For those still spry enough to pack it up and go (probably move out-of-state), here’s your chance. It will be especially attractive to those who have lived elsewhere and can move back home.

I don’t think mortgage rates can dump, even if Trump gets his way. If they decline slowly, it gives more fuel to the buyers to wait longer.

In summary, I think the 2026 listings will come faster than buyers will/can gobble.

Buyers are enjoying this new-found freedom of being patient and aren’t feeling pressured to pay crazy amounts over the list price. Buyers prefer this feeling!

Sellers have been thinking they would have a line of buyers who would pay their price, and they would get to pick the winner. But now, nobody is looking at their home, let alone making an offer.

Advantage: Buyer.

Buyers dig this new feeling, and they aren’t going to get suckered into paying some crazy price. Especially if the flow of listings keeps them thinking there will be others.

By next year, there will be enough unsuccessful sellers from 2024-2025 that a few will feel some panic. Not the type of panic like before when sellers only had 10% equity and if hired the wrong realtor they walked away with just enough dough for a steak dinner.

It will be a nervousness from not knowing how low they might need to go on price. They will act tough and tell everyone that they’re not going to give it away, but inside it will feel out of control.

Most sellers are flush, and they will gladly wait until ‘the market gets better’, rather than give it away. They will join the hundreds of households on the market now, just waiting.

But the market is made by those who are transacting.

Sales will likely suffer, and the comps will scatter all over the board as some lucky sales are interspersed with the giveaways. Sellers will gravitate to the former, and buyers will believe the giveaways are more indicative of the current market. They will want a deal too!

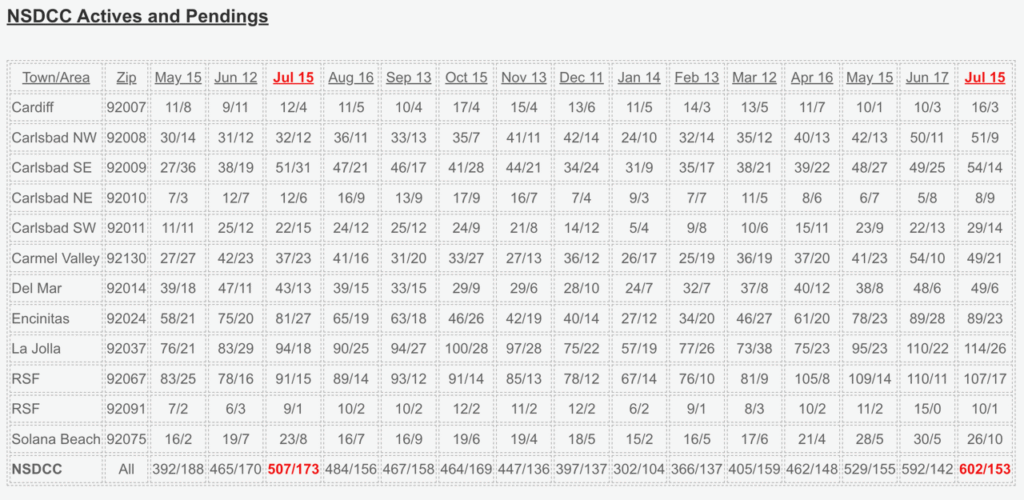

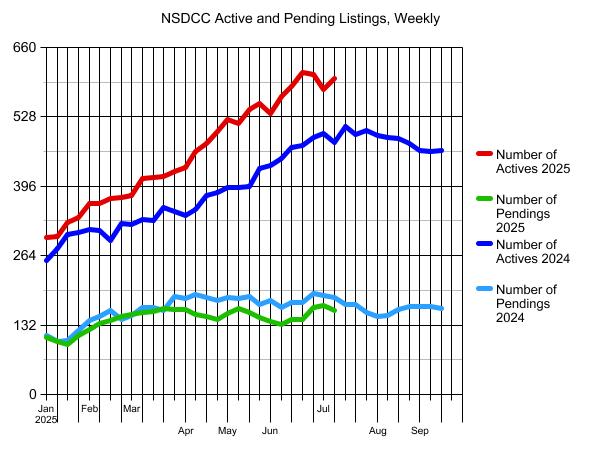

The number of NSDCC active listings is 19% higher than it was at this time last year, and the pendings are -12%……although the total number of pendings is a little higher than it was last month.

Over the last three months, the number of pendings are running 20-30 fewer YoY. If that continues, it means we’ll get down to 100-130 pendings for the rest of the year. My guess of the 3rd quarter sales being 25% lower than last year is looking pretty good right now!

The sellers aren’t done yet! Look at the bump in actives about the same time last year!

It may feel like we’re due for an end-of-summer sale, but the pendings dropped in 2024. In the last week, there were 24 listings that were marked pending – do you think there will be a surge of 40-60 this week? Yeah, probably not, unless a group of sellers do something drastic about their price.

There have been 1,883 NSDCC listings in 2025. Of those, 878 have sold or gone pending (47%) and 406 have expired, cancelled, or withdrawn (22%).

Trustindex verifies that the original source of the review is Google.

Jim & Donna Klinge helped us sell our home of 30 years in Ocean Hills. We were very happy with their service and would HIGHLY recommend them to anyone looking for an Honest, Knowledgeable, Skilled, Informed Efficient realty team. Both Jim & Donna were so helpful in different ways and complemented each others skills. Please refer to a more detailed review that we wrote on YELP. Thank You Both for all your help!!!

Jesse O'Hara

June 12, 2025

Trustindex verifies that the original source of the review is Google.

A+ thank you

Lisa Tuomi

June 11, 2025

Trustindex verifies that the original source of the review is Google.

Many years ago, we purchased a home in Carlsbad, using a realtor that was recommended to us - Jim Klinge. Fast forward to 2025, we recently had the privilege of selling 2 homes in Carlsbad, CA and didn't hesitate to reach out to Jim and Donna Klinge of Klinge Realty Group to guide us through the sales. The transactions were very different, each with its own unique situation, opportunities and challenges. From start to finish, Donna and Jim helped navigate the pre-sale preparation, the listing, showing of the house, buyer negotiations, the final close and all of the paperwork and decisions in between. What stands out with both transactions is the professionalism of Jim and Donna (and their team), wonderful communication (timely, relevant, concise), their deep understanding of market dynamics (setting realistic expectations), their access to top-notch contractors, and last, their ability to guide us across the finish line successfully. We wouldn't hesitate to use Jim and Donna in the future and highly recommend them for anyone looking to buy or sell a property in North San Diego County.

Jerry Meyer

March 28, 2025

Trustindex verifies that the original source of the review is Google.

We sold a home with Jim and Donna and from beginning to end they were consummate professionals. Their initial walk through the property resulted in a list of items to be repaired or updated. They supplied a list of vendors and job quotes to do the repairs and updates. We originally wanted to sell ‘as is’ and just get it over with. They gave us a selling price for ‘as is’ and options for doing a few updates/repairs to doing it all with the selling price for each option. We agreed to do all they suggested and we sold for the exact price they predicted. For every dollar spent we got back more than $2 back in the selling price. And they got that price in a rising interest rate environment! Donna and Jim are extremely detailed and guide you through ever aspect of the sale. There were no surprises thanks to their guidance. We couldn’t be more pleased with their representation.

Thank you Donna and Jim,

Jerry and Mary

Heather Quejada

March 27, 2025

Trustindex verifies that the original source of the review is Google.

We have known Jim & Donna Klinge for over a dozen years, having met them in Carlsbad where our children went to the same school. As long time North County residents, it was a no- brainer for us to have the Klinges be our eyes and ears for San Diego real estate in general and North County in particular. As my military career caused our family to move all over the country and overseas to Asia, Europe and the Pacific, we trusted Jim and Donna to help keep our house in Carlsbad rented with reliable and respectful tenants for over 10 years.

Naturally, when the time came to sell our beloved Carlsbad home to pursue a rural lifestyle in retirement out of California, we could think of no better team to represent us than Jim and Donna. They immediately went to work to update our house built in 2004 to current-day standards and trends — in 2 short months they transformed it into a literal modern-day masterpiece. We trusted their judgement implicitly and followed 100% of their recommended changes. When our house finally came on the market, there was a blizzard of serious interest, we had multiple offers by the third day and it sold in just 5 days after a frenzied bidding war for 20% above our asking price! The investment we made in upgrades recommended by Jim and Donna yielded a 4-fold return, in the process setting a new high water mark for a house sold in our community.

In our view, there are no better real estate professionals in all of San Diego than Jim and Donna Klinge. Buying or selling, you must run and beg Jim and Donna Klinge to represent you! Our family will never forget Jim, Donna, and their whole team at Compass — we are forever grateful to them.

Lou F

March 27, 2025

Trustindex verifies that the original source of the review is Google.

WeI had the pleasure of working with Klinge Realty Group to sell our home in Carmel Valley, and I cannot recommend them highly enough!

Jim and Donna demonstrated exceptional professionalism, offering expert guidance on market conditions and pricing strategy, which resulted in a quick and successful sale.

Communication was prompt and we were well-informed throughout the entire process.

For anyone looking for a dedicated and knowledgeable real estate team, look no further!

---

William Sams

March 25, 2025

Trustindex verifies that the original source of the review is Google.

Donna and Jim Klinge of Klinge Realty Group have our highest possible recommendation. From Donna and Jim’s first visit to our house through closing their advice and counsel was candid and honest in all dealings. They kept us fully informed throughout the process. The house sold less than three days after listing with a two-week closing. My wife and I have sold several houses during our lives. This was by far the best experience. Klinge Reality is a premium service realtor. You can’t make a better choice for someone to sell your home fast and for top dollar.

Emily Hernandez

December 29, 2024

Trustindex verifies that the original source of the review is Google.

Donna and Jim provided exceptional support and professionalism throughout the entire process. We couldn't have been happier with their efforts. They made our house shine, and thanks to their expertise, it sold above the listing price in the very first weekend! Truly a fantastic experience from start to finish.

Jesus Adrian Sahagun

November 11, 2024

Trustindex verifies that the original source of the review is Google.

This year has been difficult on our family, mainly due to having to sell our home. Thankfully we knew God had a plan for us and working with the Klinge team was a key part of it. It was an obvious decision to work with them again after such an amazing experience when purchasing the same home we needed to sell. The challenge was, how will we do this in so little time with so much going on? Jim and Donna held our hand every step of the way. Whenever an unexpected issue arose they found and provided a solution. Never once did we feel pressured to make a decision and the Klinges were always reassuring after providing the information that the decision was ours to make. Despite the curve balls, they never panicked and exemplified the “can do” attitude, making us feel optimistic and taken care of. Their expertise and professionalism was superb. But of all the reasons to work with the Klinges, the most impactful and valuable is their compassion and genuine care for their clients. We pray that we can one day purchase our forever home and you better believe that Jim and Donna will be representing us - as long as they will have us of course. Thank you again Klinge team! Your execution, experience, and care are unmatched.

SABIHA PASHA

July 23, 2024

Trustindex verifies that the original source of the review is Google.

Jim and Donna were fantastic! Jim understanding my needs, recommending potential places, pointing out the pros and cons of each property was invaluable. Then when the offer was accepted Donna’s organized guidance through the inspections, paperwork etc made the whole process seem effortless.

So grateful that I had them on my side!