Everyone talks badly about Robert Reffkin/Compass and our stand against the CCP.

It’s because the industry is so sensitive about the thought of agents hoarding their listings off-market to sell them to their own buyers or to buyers represented by other in-house agents. To what extent it is actually happening doesn’t matter – just the thought bugs people.

Off-market sales have happened at all brokerages since the beginning of time. But for those who believe that every home should be exposed to all buyers, it makes them think that shenanigans are in play.

On February 21st, I did this blog post where I described reasons for sellers and agents to sell off-market:

The allure of an insider deal can cause a buyer to pay more – they are sexy deals.

Buyers don’t have the benefit of open-market exposure to test the price.

It keeps the bozo agents from screwing up deals.

When forming opinions about off-market sales, let’s factor in the market conditions.

We are screaming towards a buyer’s market, and it’s already upon us in some areas. The last time we had a buyer’s market was fifteen years ago – which nobody remembers – and it’s been the exact opposite over the last five years.

You will know it’s a buyer’s market when you hear more people saying that it’s not a good time to sell.

It will lead to conversations like this: “Hey Jim, I’ve heard horror stories from friends and family who are trying to sell their home and nobody is coming by – they have no showings!”

“I don’t want that to happen to me, so sell my house by any means necessary. I still want all my money, and if you think selling my house off-market will accomplish that, then do it!”

When potential sellers see unsold listings stacking up, they are going to consider alternatives, but:

Selling to an instant-cash flipper might seem more enticing, except they want a 30% discount.

Renting the house out is a terrible idea if you think prices might go down later.

Going on the open market at less than the dream price doesn’t sound good either.

In a buyer’s market, the selling choices seem bleak. It causes potential sellers to jump at a sexy option like selling off-market – if that will get them their money. They aren’t going to take a discount off-market. Instead, they will imagine that it’s the best chance to sell for their price, which is all that matters to them.

Yesterday’s bombshell announcement that Ketchmark will be suing the brokerages that support the Clear Cooperation Policy should be the end of the CCP. Who wants more lawsuits?

Reffkin’s hardball stance against the CCP is very understandable when you consider how we got here.

The quasi-governing body known as the National Association of Realtors casually walks into a Missouri court room and gets their lunch handed to them. Then they settled on behalf of the brokerages? Who gave you the power to levy a $52 million fine against Compass without a chance to defend ourselves? Plus, you’ve done nothing to prevent future lawsuits from happening!

Unfortunately, the anger over how the NAR mis-handled the lawsuit/settlement has turned into a battle about the CCP, when they are two different things. If NAR would step up their game and end the threat of lawsuits while providing expert guidance on the CCP issue, then we might listen. But there is no faith that they will do anything, so we need to defend ourselves while providing our own solutions for our clients.

Reffkin is promoting Private Exclusives as part of a 3-Phase marketing plan in order to offer a comprehensive marketing solution. There is no push by Compass management to sell homes off-market. Behind the scenes, all we have is a simple one-liner list of homes throughout the county, and most of them have no photos, no descriptions, and can’t be shown because they are being prepared to go to market. That’s not a vibrant off-market sales environment – it’s just a parking lot. I struggle to even look at it because there’s nothing there. At least not yet.

Yesterday there were 287 Compass private exclusives in San Diego County, and there are 4,653 houses, condos, and mobilehomes actively for sale on the MLS today. How many PEs are going to sell off-market each month? Maybe five or ten? It’s the same at other brokerages and it’s been the norm for 100+ years.

But it has promise because the sellers are going to want an alternative in a buyer’s market.

Though the off-market listings might look sexy to buyers, they better get good help on pinpointing the value under the current market conditions. It is why buyers should embrace bidding wars – because when there isn’t one, it tells you something too.

Hat tip to CBMark to sending in this gem – it’s only $599,999 and open today!

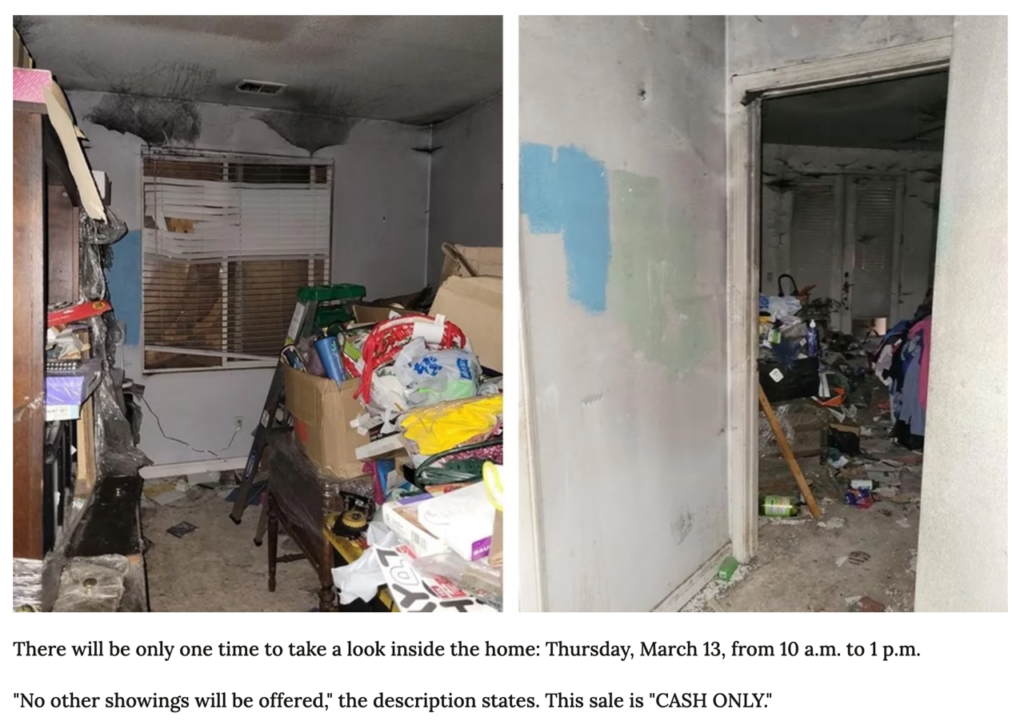

The problem with the hoarder home is more than just the mess inside and outside.

The hoarder home owner “harasses the children of my best friend, which is directly across the street from my house. Anybody that goes against her—she throws terror underneath their feet to get her way,” said Mead.

Last March, a San Diego city inspector went to the home. According to CBS8, Inspector Justin Welker found trash piles as high as 4 feet, rotting food, and signs of “rodent infestation.”

“Words cannot adequately describe the condition of the master toilet,” he wrote in his report. “It was smeared with brown filth and the stall floor covered in trash.”

He went on to describe the exterior: “The in-ground pool was partially filled with green water, presumably algae, which is a potential breeding ground for vectors, such as mosquitos.”

During that time, the homeowner also appeared in front of a civil court judge who was supposed to decide whether or not to send a court-appointed receiver to the property to clean it up, but the homeowner’s request for a continuance was granted.

The investigation by CBS8 found court filings dating to 2009.

Realtor.com has uncovered a recent anonymous complaint sent to the San Diego Police Department describing a “court ordered, sealed up hoarder home now taken over by homeless.” It was reported on Oct. 18, 2024. Realtor.com has reached out to the SDPD for more information.

Bidding wars can typically go up to 10% over the list price. Even a novice agent can pull it off just by having their listing on the open market. But buyers get jittery going any higher than +10% and without having a great agent assisting them, their bidding tends to sputter out.

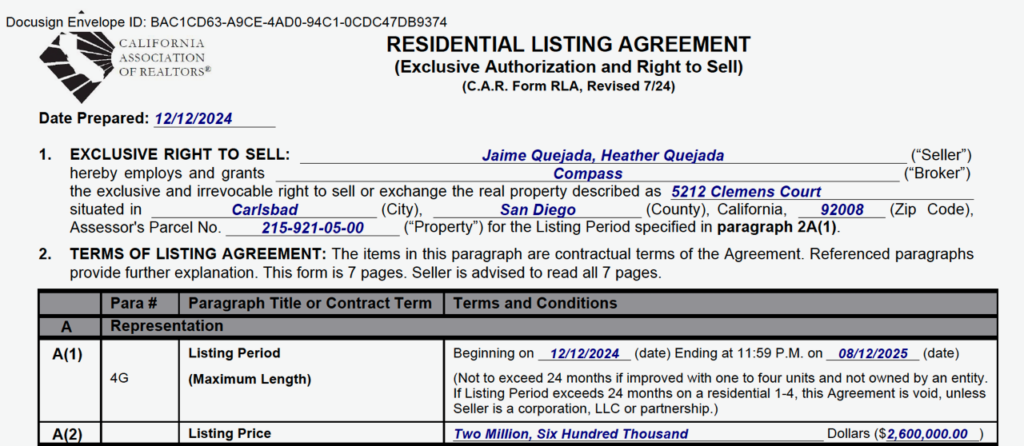

The last neighborhood sale was a model-match that closed for $2,060,000 the week before we launched, and because I wanted to be within $500,000 of the last sale, we decided to lower our original list price from $2,600,000 to $2,499,000 for Day One.

After the open-house extravaganza, we received SIX offers!

I thought it could if I was able to coax them into believing that was the true value. I sent this to each agent:

Attached is the sellers’ request for your highest-and-best offer.

Some explanation is due.

We deliberately low-priced this home to attract the maximum interest immediately.

1. We had originally signed the listing at $2,600,000 in December.

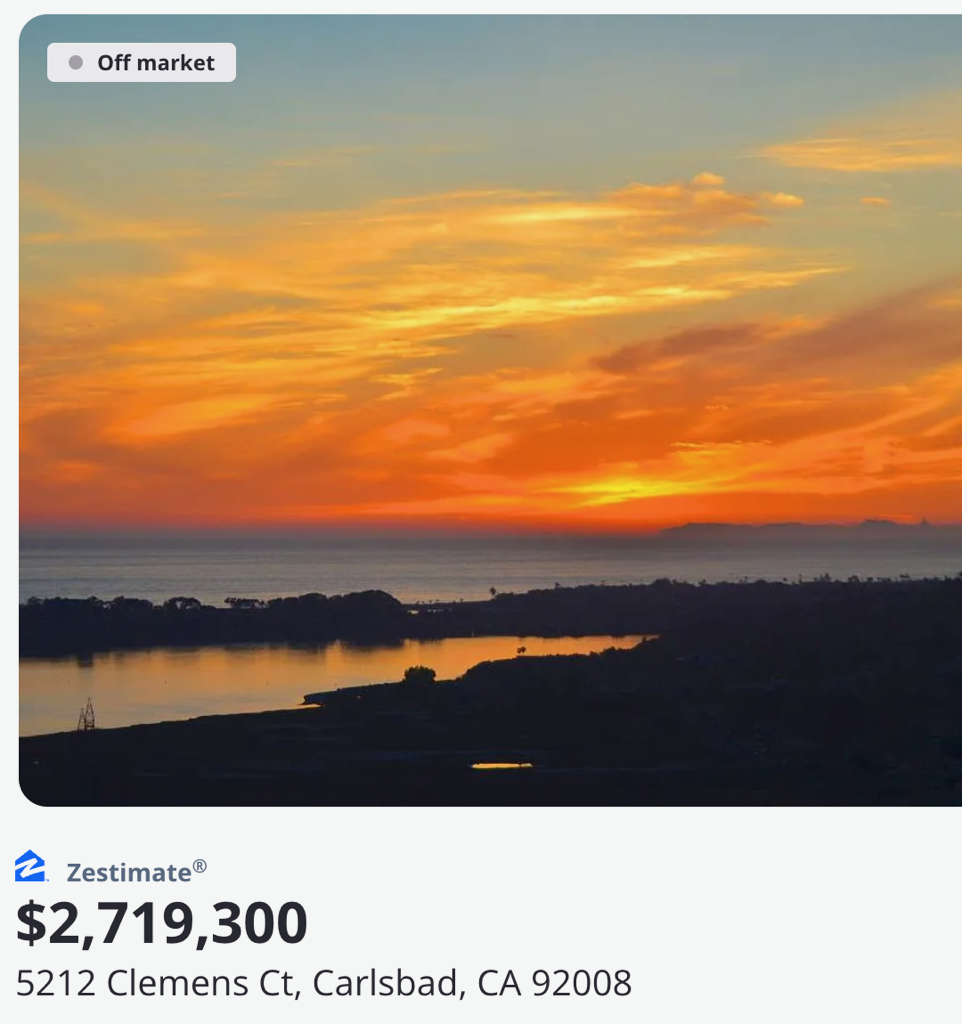

2. The zestimate on the day of MLS input was $2,719,300 (Zillow adjusts their zestimates to within a couple of bucks of the list price once a home is entered onto the MLS).

3. The homes at the end of Twain being built by Shea Homes will be in the $3,000,000 to $3,500,000 range, according to a neighbor. (I did not know that until yesterday).

Other premium homes:

I saw this one and while it was new it was jammed into the hillside with no view:

Nobody has the big ocean view that Clemens has, and now there are several comps in the $3 millions!

Bid with confidence! No matter what the price, you’re not paying too much.

This is where we see the difference between the regular agents and the real professional salespeople, of which there were two.

Most agents will just forward my plea to their buyers, and let their buyers come up with a price.

The real pros will adopt my thoughts and make them their own. Then they will advocate for their clients, and for those buyers who want a guaranteed win, the agent will lay out a solid strategy that will swamp the boat and blow out all other buyers. It’s what happened here!

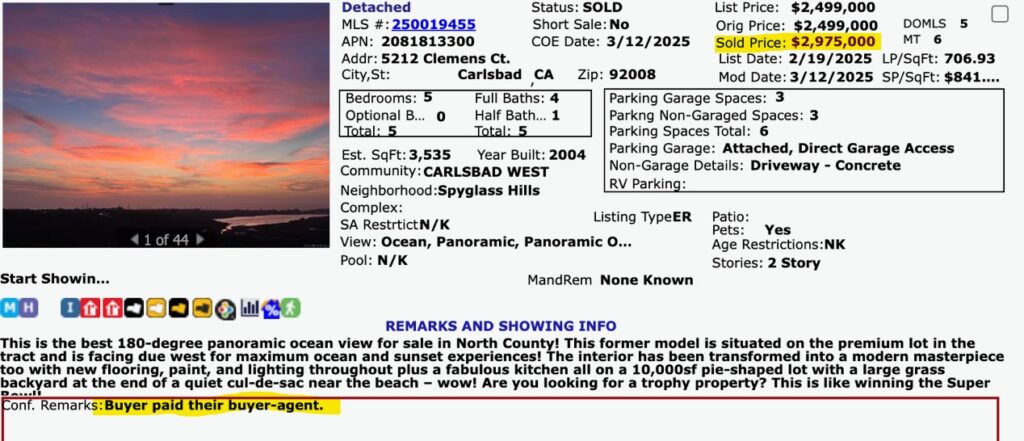

LP = $2,499,000

SP = $2,975,000 cash, 15-day escrow, waived all contingencies in the offer, and the buyer paid their buyer-agent’s commission.

The last debacle by Ketchmark cost Compass $52 million – there is no way that we will keep putting ourselves at risk of more lawsuits. It’s why Robert Reffkin has been so adamant about disolving the Clear Cooperation Policy, even though he doesn’t state it often enough.

Once the CCP is gone, there won’t really be any reason for the National Association of Realtors to stick around much longer. Their blunder of taking the lawsuit too casually and losing it AND forcing a settlement on the big brokerages should cost them their jobs.

I’ll be at a two-day conference next month where the CEO of NAR will be speaking. I know she is going to gloss over this and say everything will be fine – I’m hoping for a chance to ask a couple of questions!

Soon we will be back to pocket listings and in-house sales being the norm, and putting homes on the MLS will be a last resort for many agents.

Every year it gets worse for homebuyers, and this will be the 2025 gut-punch for them.

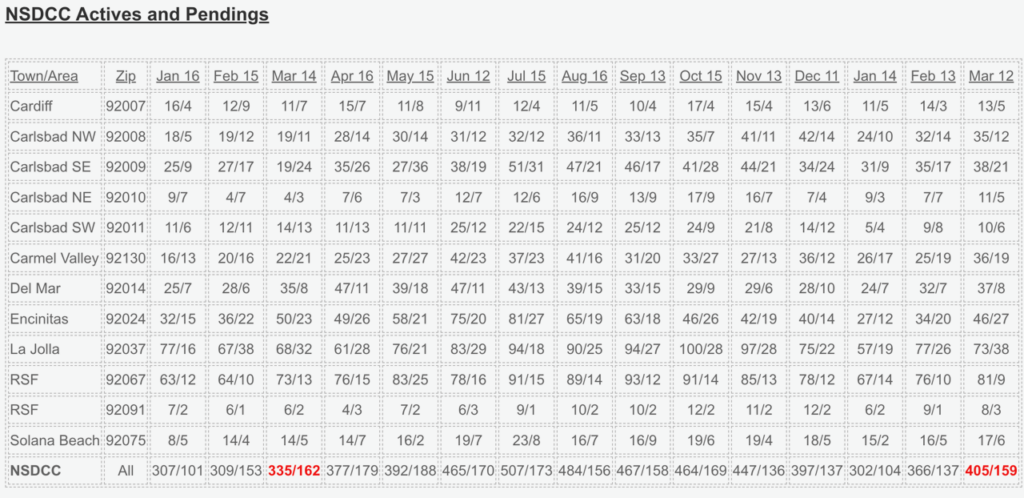

Frenzy may not sound applicable these days…..but look at La Jolla getting off to a hot start and leading the pack with 38 pendings, just like last year!

The 92067 is angling towards their pre-covid standard with a 9:1 ratio of actives-to-pendings. Our normal gauge of a healthy market is a 2:1 ratio, but hey, it’s different in the Ranch.

The total number of pendings is about the same as a year ago, in spite of there being +21% more active listings today. Buyers are willing and able to ignore the OPTs!

Sociologist Ray Oldenburg coined the term “third places” to describe informal, neutral locations outside of home (first place) and work/school (second place). These locations are used for social interactions, gatherings, and community building. Examples include parks, beaches, cafes, bars, gyms, libraries, and even some restaurants.

Third places are meant to facilitate social interaction with people outside our normal circle of family and coworkers. No one is forced to be there and cost should not prevent or prohibit people from attending. It is a place where we can interact with members of our community, both friends and strangers, and it acts as a meeting ground to build relationships with people of our community.>

For Americans, it can seem difficult to identify and utilize third places in our local communities. With a heavy reliance on cars for transportation and an increase in screen time and social media, it is not as easy to find yourself in a third place in today’s America compared to European cities 100 years ago. However, it’s still possible and imperative to build a sense of community and happiness!

Here are some of my favorite third places in San Diego:

Peace, Love, & Yoga – My family has been taking yoga classes here for well over 15 years and I love it here! My mother Donna is known by most teachers and I feel at home here, even though I don’t attend classes regularly. They have a very relaxed vibe and everyone, both teachers and students, is extremely friendly and welcoming. It’s a great workout but the people here make it an amazing third place. Even Jim goes once in a while!

Communal Coffee – This coffee shop is a recent find for me and has my favorite coffee ever – a sweet mint cold brew. While their drinks and food are delicious, it also has a great community feel to it. Last time I was there, I met a friend for breakfast and she brought her dog – we ended up chatting with another dog owner as the puppies interacted! With their open layout and bustling business, Communal is another local spot to create a sense of community.

Kate Sessions Memorial Park – Located just north of Pacific Beach, it provides 180 degree views of downtown, Mission Bay, Point Loma, and the ocean. Many people I know spend time here and there always seems to be people hanging out and enjoying the 79-acre park!

Liberty Station – A former naval training center turned cultural hub! It features a variety of shops, restaurants, art galleries, and open spaces where people can gather. It’s a great spot to meet people, whether for food, culture, or just to relax.

All Beaches – Once the weather gets warmer, there’s no better place to be than at the beach! Whether you’re laying on the sand, catching some waves, or walking along the coast, our San Diego beaches are a great way to get outside, spend time with loved ones, meet new people, and enjoy the place we call home!

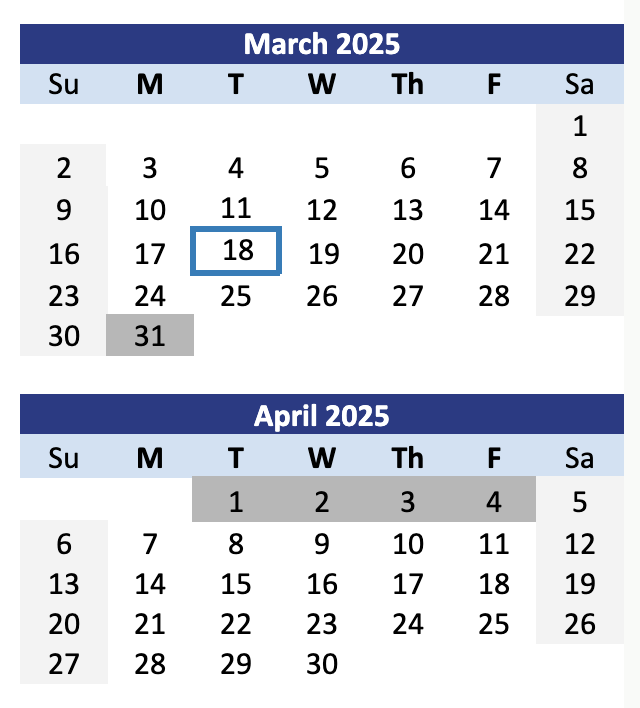

When deciding on a date to launch a new listing, we try our best to work around the rain. The open-house results are best during our typical sun-shiny day!

We also consider the school calendar.

It sure would be nice if the schools are line up their calendars and have spring break at the same time, but they don’t. Here are the differences:

San Dieguito HS, San Diego, and Vista: March 31-April 4

Carlsbad, Oceanside: April 7-11

Poway: April 14-18

Escondido: April 10-21

Do you avoid launching a new listing on BOTH weekends around those dates? Ideally, yes but this is primetime selling season. I can’t burn two full weekends!

Do you base the decision on where the home is located, figuring that the likely buyers will be renting nearby? Or where the likely buyers may live now, and from where they are moving up/down?

I’m thinking about doing a Thursday open house to give buyers a chance to see the home before leaving town. Or do the serious buyers stay home this year so they don’t miss anything? When I was a kid, we never went anywhere – you’ll survive!

For Shadash – very few home purchases around the coast were financed with FHA, but when Trump makes a big deal out of cancelling the Biden gravy train, it will have repercussions. A free article from the WSJ:

The problems began when the Obama administration eased underwriting standards by enabling more home buyers whose debt payments exceed 43% of income to qualify for government-backed loans. Such borrowers are risky because they might not be able to make payments if their income drops or expenses rise.

As home prices climbed, the Federal Housing Administration insured more loans to financially stretched borrowers with as little 3.5% down. No skin off lenders’ backs if borrowers later defaulted, since the mortgages were backed by the government.

In 2007, 35% of new FHA borrowers had debt-to-income ratios above 43%. By 2020, 54% did. As housing prices and inflation surged, borrowers became more stretched. The FHA kept insuring mortgages to borrowers who were increasingly leveraged. About 64% of FHA borrowers last year exceeded the 43% threshold.

The FHA loan portfolio is far riskier than it was before the 2008 housing crisis. The American Enterprise Institute’s Ed Pinto and Tobias Peter estimate that 79% of FHA first-time borrowers have a month or less in financial reserves—not enough to make mortgage payments if their household expenses rise, as most have owing to inflation.

No surprise, many are missing payments, especially recent borrowers. About 7.05% of FHA mortgages issued last year went seriously delinquent—90 or more days past when a payment is due—within 12 months. That’s more than at the 2008 peak of the subprime bubble (7.02%).

Under the guise of Covid relief, the Biden administration masked the growing troubles in the housing market by paying off borrowers and mortgage servicers to prevent foreclosures. Of the 52,531 FHA loans last year that went seriously delinquent within their first year, only nine resulted in foreclosure.

The FHA instituted a program that pays mortgage servicers to make borrowers’ missed payments for them. Missed payments are added to the loan’s principal, but without interest. The FHA also pays servicers to cut monthly payments for delinquent borrowers by 25% for three years, with the payment reductions also added to the principal without interest.

Consider a borrower who misses five $4,000 monthly mortgage payments. The servicer will add the $20,000 in missed payments to the mortgage and reduce monthly payments by $1,000 for three years—adding another $36,000 to their mortgage. So the borrower is $56,000 deeper in debt, though with no additional interest. If he misses payments again, the servicer rinses and repeats, getting paid $1,750 every time it lathers up. The FHA also lets servicers charge borrowers legal fees—typically several thousand dollars—that are added to the mortgage principal.

The FHA made 556,841 “incentive payments” to servicers over the past year to prevent foreclosures—nearly as many as the new mortgages it insured. Government-backed mortgage relief has become a cash cow for servicers, some of which originated the risky loans they are paid not to foreclose. Moral hazard, anyone?

One result is that many FHA borrowers owe more than their original mortgage and more than their homes are worth. They are essentially trapped in their homes even if they want to sell and move.

Another result is that home prices keep increasing because borrowers who don’t pay their mortgages—and never should have qualified for loans—can’t get foreclosed on or be forced to sell their homes. Getting foreclosed on these days is like flunking out of college—it takes effort. You have to reject repeated offers for mortgage relief.

Government-sponsored enterprises Fannie Mae and Freddie Mac instituted similar “home retention” programs for delinquent borrowers with the Biden administration’s blessing. The cost of their mortgage relief gets socialized in higher rates charged to home buyers whose mortgages they guarantee.

Taxpayers are on the hook if the FHA insurance fund—financed by premiums on mortgages it backs—goes broke paying off borrowers and servicers to prevent foreclosures. The FHA annual report to Congress doesn’t disclose the cost of such payments, and the agency didn’t furnish them on my request. Perhaps the Department of Government Efficiency could dig into its financial books.

The Biden administration built a house of cards that could collapse if Trump officials dare to end the mortgage giveaways, as they should. Foreclosures would inevitably increase, which could cause home prices to fall sharply in lower-income neighborhoods with more FHA mortgages. More borrowers would then fall underwater, ballooning taxpayer losses, though homes might also become more affordable for people who don’t already own them.

But what a mess. And who will get blamed? Not the folks who inflated the bubble.

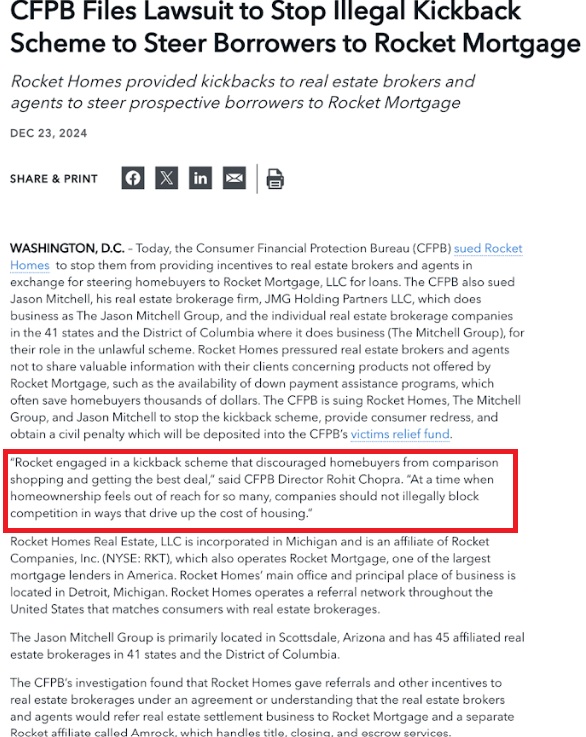

We saw the lawsuit filed against Rocket over a kickback scheme that was declared to be politically motivated and was dismissed by the Trump DOJ last month.

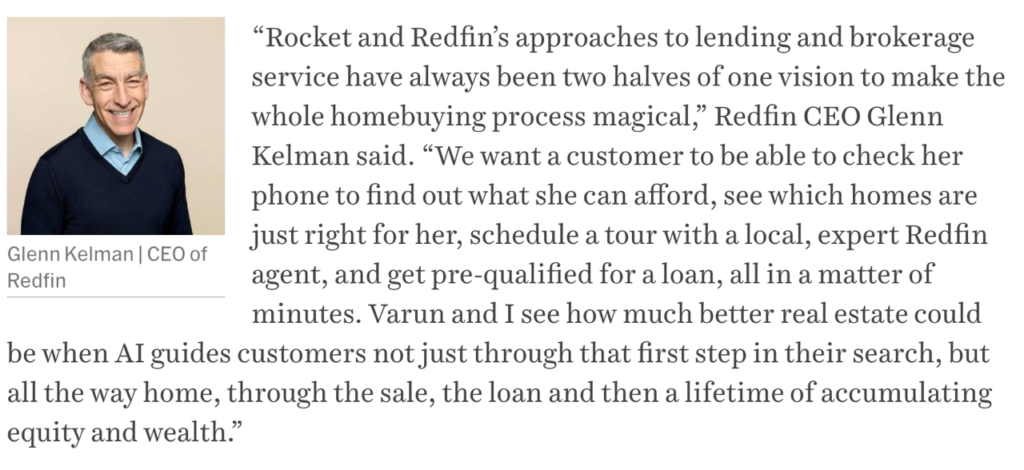

But Glenn must have wanted a piece of that, and two weeks later, he jumps in bed with them:

Of course, he gets cute with his She pronoun and AI reference and you have to wonder how they will be leading their sheeple into a mortgage?

It’s one thing when a brokerage has an affiliated mortgage company for convenience, but when the mortgage company OWNS you?

Oh, and those experts? All I remember is when a Redfin agent showed my $2,000,000+ listing, and I asked her is she was new at the company.

Trustindex verifies that the original source of the review is Google.

Jim & Donna Klinge helped us sell our home of 30 years in Ocean Hills. We were very happy with their service and would HIGHLY recommend them to anyone looking for an Honest, Knowledgeable, Skilled, Informed Efficient realty team. Both Jim & Donna were so helpful in different ways and complemented each others skills. Please refer to a more detailed review that we wrote on YELP. Thank You Both for all your help!!!

Jesse O'Hara

June 12, 2025

Trustindex verifies that the original source of the review is Google.

A+ thank you

Lisa Tuomi

June 11, 2025

Trustindex verifies that the original source of the review is Google.

Many years ago, we purchased a home in Carlsbad, using a realtor that was recommended to us - Jim Klinge. Fast forward to 2025, we recently had the privilege of selling 2 homes in Carlsbad, CA and didn't hesitate to reach out to Jim and Donna Klinge of Klinge Realty Group to guide us through the sales. The transactions were very different, each with its own unique situation, opportunities and challenges. From start to finish, Donna and Jim helped navigate the pre-sale preparation, the listing, showing of the house, buyer negotiations, the final close and all of the paperwork and decisions in between. What stands out with both transactions is the professionalism of Jim and Donna (and their team), wonderful communication (timely, relevant, concise), their deep understanding of market dynamics (setting realistic expectations), their access to top-notch contractors, and last, their ability to guide us across the finish line successfully. We wouldn't hesitate to use Jim and Donna in the future and highly recommend them for anyone looking to buy or sell a property in North San Diego County.

Jerry Meyer

March 28, 2025

Trustindex verifies that the original source of the review is Google.

We sold a home with Jim and Donna and from beginning to end they were consummate professionals. Their initial walk through the property resulted in a list of items to be repaired or updated. They supplied a list of vendors and job quotes to do the repairs and updates. We originally wanted to sell ‘as is’ and just get it over with. They gave us a selling price for ‘as is’ and options for doing a few updates/repairs to doing it all with the selling price for each option. We agreed to do all they suggested and we sold for the exact price they predicted. For every dollar spent we got back more than $2 back in the selling price. And they got that price in a rising interest rate environment! Donna and Jim are extremely detailed and guide you through ever aspect of the sale. There were no surprises thanks to their guidance. We couldn’t be more pleased with their representation.

Thank you Donna and Jim,

Jerry and Mary

Heather Quejada

March 27, 2025

Trustindex verifies that the original source of the review is Google.

We have known Jim & Donna Klinge for over a dozen years, having met them in Carlsbad where our children went to the same school. As long time North County residents, it was a no- brainer for us to have the Klinges be our eyes and ears for San Diego real estate in general and North County in particular. As my military career caused our family to move all over the country and overseas to Asia, Europe and the Pacific, we trusted Jim and Donna to help keep our house in Carlsbad rented with reliable and respectful tenants for over 10 years.

Naturally, when the time came to sell our beloved Carlsbad home to pursue a rural lifestyle in retirement out of California, we could think of no better team to represent us than Jim and Donna. They immediately went to work to update our house built in 2004 to current-day standards and trends — in 2 short months they transformed it into a literal modern-day masterpiece. We trusted their judgement implicitly and followed 100% of their recommended changes. When our house finally came on the market, there was a blizzard of serious interest, we had multiple offers by the third day and it sold in just 5 days after a frenzied bidding war for 20% above our asking price! The investment we made in upgrades recommended by Jim and Donna yielded a 4-fold return, in the process setting a new high water mark for a house sold in our community.

In our view, there are no better real estate professionals in all of San Diego than Jim and Donna Klinge. Buying or selling, you must run and beg Jim and Donna Klinge to represent you! Our family will never forget Jim, Donna, and their whole team at Compass — we are forever grateful to them.

Lou F

March 27, 2025

Trustindex verifies that the original source of the review is Google.

WeI had the pleasure of working with Klinge Realty Group to sell our home in Carmel Valley, and I cannot recommend them highly enough!

Jim and Donna demonstrated exceptional professionalism, offering expert guidance on market conditions and pricing strategy, which resulted in a quick and successful sale.

Communication was prompt and we were well-informed throughout the entire process.

For anyone looking for a dedicated and knowledgeable real estate team, look no further!

---

William Sams

March 25, 2025

Trustindex verifies that the original source of the review is Google.

Donna and Jim Klinge of Klinge Realty Group have our highest possible recommendation. From Donna and Jim’s first visit to our house through closing their advice and counsel was candid and honest in all dealings. They kept us fully informed throughout the process. The house sold less than three days after listing with a two-week closing. My wife and I have sold several houses during our lives. This was by far the best experience. Klinge Reality is a premium service realtor. You can’t make a better choice for someone to sell your home fast and for top dollar.

Emily Hernandez

December 29, 2024

Trustindex verifies that the original source of the review is Google.

Donna and Jim provided exceptional support and professionalism throughout the entire process. We couldn't have been happier with their efforts. They made our house shine, and thanks to their expertise, it sold above the listing price in the very first weekend! Truly a fantastic experience from start to finish.

Jesus Adrian Sahagun

November 11, 2024

Trustindex verifies that the original source of the review is Google.

This year has been difficult on our family, mainly due to having to sell our home. Thankfully we knew God had a plan for us and working with the Klinge team was a key part of it. It was an obvious decision to work with them again after such an amazing experience when purchasing the same home we needed to sell. The challenge was, how will we do this in so little time with so much going on? Jim and Donna held our hand every step of the way. Whenever an unexpected issue arose they found and provided a solution. Never once did we feel pressured to make a decision and the Klinges were always reassuring after providing the information that the decision was ours to make. Despite the curve balls, they never panicked and exemplified the “can do” attitude, making us feel optimistic and taken care of. Their expertise and professionalism was superb. But of all the reasons to work with the Klinges, the most impactful and valuable is their compassion and genuine care for their clients. We pray that we can one day purchase our forever home and you better believe that Jim and Donna will be representing us - as long as they will have us of course. Thank you again Klinge team! Your execution, experience, and care are unmatched.

SABIHA PASHA

July 23, 2024

Trustindex verifies that the original source of the review is Google.

Jim and Donna were fantastic! Jim understanding my needs, recommending potential places, pointing out the pros and cons of each property was invaluable. Then when the offer was accepted Donna’s organized guidance through the inspections, paperwork etc made the whole process seem effortless.

So grateful that I had them on my side!