Nine-year-old G.T. Struck stepped in front of the upright headstone at Fort Rosecrans National Cemetery and waited.

His father, Thomas Struck, read out loud the name on the marker and handed the boy a small American flag attached to a pointed wooden stick.

G.T. put the toe of his right shoe at the base of the marker, measuring where the flag should go. He bent over and stuck it in the ground behind his right heel. Then he straightened up, bowed his head for a moment, and saluted.

The headline writers are having fun with the current real estate market. They must challenge each other with whom can come up with the most outrageous headline, regardless of what’s in the article.

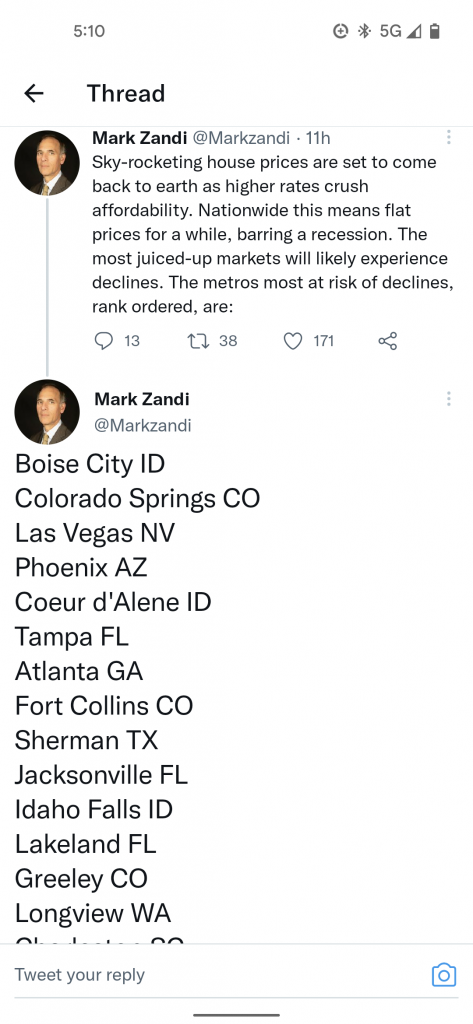

In this week’s article, he says, “that we’ve officially moved from a housing boom into a “housing correction.”

“The housing market has peaked…everything points to a rolling over of the housing market,” Zandi says. “In terms of home sales, they’re falling sharply. Housing demand is coming down fast. Home price growth [will] go flat here pretty quickly; we will see [home] price declines in a significant number of markets.”

But further into the article, they lay out the caveat that you see in every doomer article:

To be clear, Zandi doesn’t see a 2008-style housing bust or foreclosure crisis. While the spike in mortgage rates has pushed the housing market into the upper bounds of affordability, we don’t have the credit issues that plagued us last time. Homeowners are financially better off than they were in the lead-up to the 2008 financial crisis. This time around, Zandi says, we also don’t have widespread subprime mortgages. Also, if nationwide home prices do begin to plummet, he says, the Fed could always ease up on mortgage rates.

That said, Zandi says some regional housing markets have become historically “overvalued” and could see home prices decline 5% to 10% over the coming year. If a recession does come, Zandi says price drops in those markets could grow to between 10% to 20%.

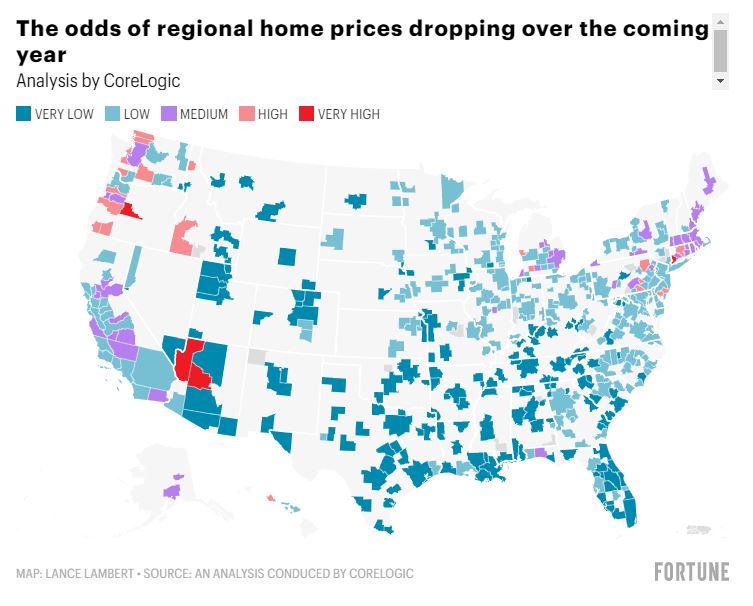

Buried further is the map (above) that shows the areas with the greatest odds of home-price declines. There aren’t many, and none are in California.

None of these analysts want to consider that to have home prices decline, there has to be sellers who will sell for less. It’s much more likely – like 10x more likely – that our market will just stall out as sellers wait it out, rather than take less. They’re not going to give it away!

Their most popular markets are suburban areas that are 30 minutes from the nearest city center? Sounds like Carlsbad/Encinitas! From Zillow:

Zillow’s most popular market so far this year is Woodinville, Washington. Burke, Virginia and Highlands Ranch, Colorado round out the top three.

Every city in Zillow’s latest 10-most-popular-markets list is a suburban area roughly 30 minutes from the nearest city center. Home values are growing faster in each of these suburbs than in the principal cities in their metro areas.

Remote work is a key reason suburban home values are now growing faster than those in urban areas as home buyers are prioritizing space and affordability over a short commute.

Zillow’s most popular market of early 2022 is Woodinville, Washington, leading a list of fast-growing suburbs as the most in-demand places of the first three months of the year. Following close behind were Burke, Virginia, in the Washington, D.C. area; Highlands Ranch, Colorado, outside of Denver; Westchase, Florida, near Tampa; and Edmonds, Washington, also in the Seattle metro.

The most popular markets so far this year paint a picture of how remote work has changed the U.S. housing landscape. Demand for suburban homes found an extra gear last summer, causing suburban home values to grow faster than home values in urban areas, a reversal from previous norms and from the first 15 months of the pandemic. Remote work is a driving force behind this shift, prompting home buyers to prioritize affordability and space over a short commute.

The suburbs that beat out all others to make the top 10 of Zillow’s most popular markets of Q1 are seeing home values grow faster on a quarterly basis than the principal city in their metro area, indicating stronger demand. Most of them have more expensive homes than their nearest major city, and several are significantly more expensive. Eight of the top 10 have a typical home value higher than their nearby principal city, and seven of those have a typical home value more than $150,000 higher.

Regionally, Havertown, Penn. outside of Philadelphia is Zillow’s most popular market in the Northeast, edging out four Boston suburbs: Billerica, Framingham, Waltham and Arlington. In the central region, Ballwin, Missouri,. is joined in the top five by Grand Rapids, Michigan, and three pricey Dallas suburbs: Coppell, Plano and Prosper. Denver suburbs dominated the mountain region, taking the top eight spots in Zillow’s rankings.

Someone posted this online, and I thought it was one of the most bizarre real estate photos ever. The tennis-court salesman in this neighborhood was really good!

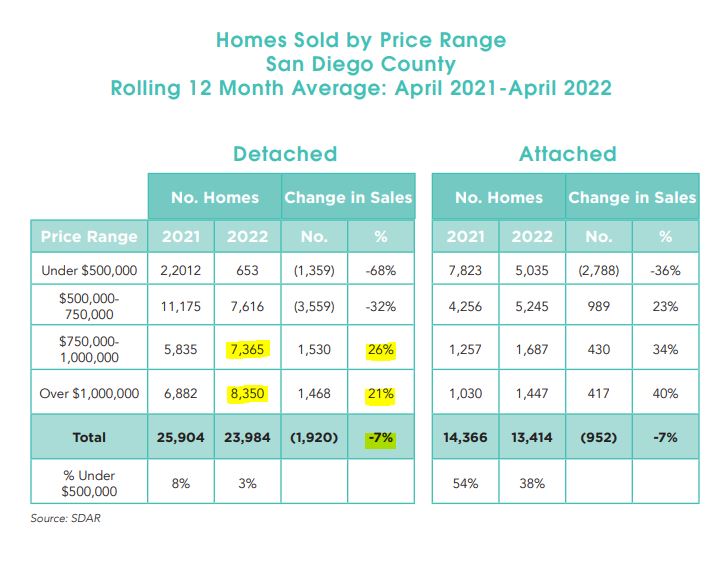

We’re going to be hearing for months about how sales are dwindling.

It’s mostly due to comparing 2022 stats to last year’s numbers, which were the most frenzied-up numbers ever. But it is also due to it being a market for the affluent now.

Look at the chart above. Even though sales are down 7% overall, the higher-end sales are booming:

San Diego County Detached-Home Sales, Jan 1 – May 31

Year

SD County Detached-Home Sales

Sales Over $1,000,000

2017

9,889

1,449

2018

9,154

1,570

2019

9,002

1,581

2020

7,683

1,496

2021

9,769

3,177

2022

8,267

3,786

As recently as 2019, the million-dollar sales were only 18% of the total sales count. This year, it’s 46%, and we still have a week more of sales plus late-reporters to record. It could hit 50%, just three year later!

Yet the total number of 2022 sales will only be 10% to 12% behind those in 2021, the craziest year ever.

Plus, if there were more quality homes for sale priced over $1,000,000, we’d have even more sales!

Last week, reader TOB talked about a buyer he knew who walked away from a deal over the Rampart fireplace. Here’s a list of other issues that might be deal-killers, but we try to find a way to solve them before giving up!

While the pandemic and world war are raging, the stock market is diving into bear territory, and all media is burying the real estate market, I put two listings on the open market for four days and get three offers on each and sell them both for over list at a time when people are wondering how far will prices drop.

Who do you want in your corner? Contact Jim the Realtor today!

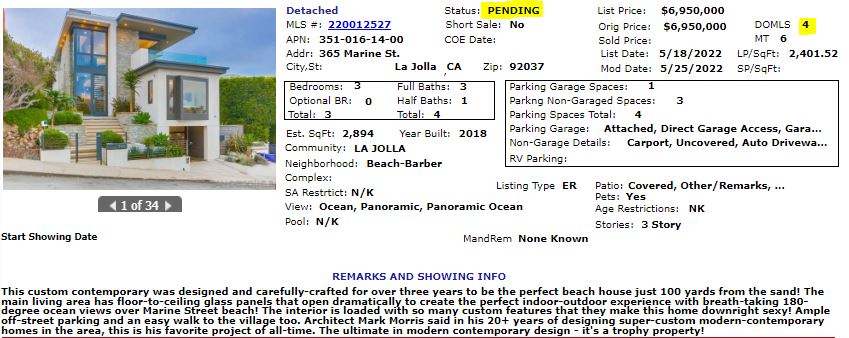

It is a true honor to have listed for sale my favorite home of all-time!

365 Marine St., La Jolla

3 br/3.5 ba, 2,894sf

YB: 2018

LP = $6,950,000 – SP = $7,750,000

This custom contemporary was designed and carefully-crafted for over three years to be the ultimate beach house just 100 yards from the sand! The main living area has floor-to-ceiling glass panels that open dramatically to create the perfect indoor-outdoor experience with breath-taking 180-degree ocean views over Marine Street beach! The interior is loaded with so many custom features that they make this home downright sexy! Ample off-street parking and an easy walk to the village too. Architect Mark Morris said in his 20+ years of designing super-custom modern-contemporary homes in the area, this is his favorite project of all-time. The ultimate in modern contemporary design – it’s a trophy property!

Trustindex verifies that the original source of the review is Google.

Jim & Donna Klinge helped us sell our home of 30 years in Ocean Hills. We were very happy with their service and would HIGHLY recommend them to anyone looking for an Honest, Knowledgeable, Skilled, Informed Efficient realty team. Both Jim & Donna were so helpful in different ways and complemented each others skills. Please refer to a more detailed review that we wrote on YELP. Thank You Both for all your help!!!

Jesse O'Hara

June 12, 2025

Trustindex verifies that the original source of the review is Google.

A+ thank you

Lisa Tuomi

June 11, 2025

Trustindex verifies that the original source of the review is Google.

Many years ago, we purchased a home in Carlsbad, using a realtor that was recommended to us - Jim Klinge. Fast forward to 2025, we recently had the privilege of selling 2 homes in Carlsbad, CA and didn't hesitate to reach out to Jim and Donna Klinge of Klinge Realty Group to guide us through the sales. The transactions were very different, each with its own unique situation, opportunities and challenges. From start to finish, Donna and Jim helped navigate the pre-sale preparation, the listing, showing of the house, buyer negotiations, the final close and all of the paperwork and decisions in between. What stands out with both transactions is the professionalism of Jim and Donna (and their team), wonderful communication (timely, relevant, concise), their deep understanding of market dynamics (setting realistic expectations), their access to top-notch contractors, and last, their ability to guide us across the finish line successfully. We wouldn't hesitate to use Jim and Donna in the future and highly recommend them for anyone looking to buy or sell a property in North San Diego County.

Jerry Meyer

March 28, 2025

Trustindex verifies that the original source of the review is Google.

We sold a home with Jim and Donna and from beginning to end they were consummate professionals. Their initial walk through the property resulted in a list of items to be repaired or updated. They supplied a list of vendors and job quotes to do the repairs and updates. We originally wanted to sell ‘as is’ and just get it over with. They gave us a selling price for ‘as is’ and options for doing a few updates/repairs to doing it all with the selling price for each option. We agreed to do all they suggested and we sold for the exact price they predicted. For every dollar spent we got back more than $2 back in the selling price. And they got that price in a rising interest rate environment! Donna and Jim are extremely detailed and guide you through ever aspect of the sale. There were no surprises thanks to their guidance. We couldn’t be more pleased with their representation.

Thank you Donna and Jim,

Jerry and Mary

Heather Quejada

March 27, 2025

Trustindex verifies that the original source of the review is Google.

We have known Jim & Donna Klinge for over a dozen years, having met them in Carlsbad where our children went to the same school. As long time North County residents, it was a no- brainer for us to have the Klinges be our eyes and ears for San Diego real estate in general and North County in particular. As my military career caused our family to move all over the country and overseas to Asia, Europe and the Pacific, we trusted Jim and Donna to help keep our house in Carlsbad rented with reliable and respectful tenants for over 10 years.

Naturally, when the time came to sell our beloved Carlsbad home to pursue a rural lifestyle in retirement out of California, we could think of no better team to represent us than Jim and Donna. They immediately went to work to update our house built in 2004 to current-day standards and trends — in 2 short months they transformed it into a literal modern-day masterpiece. We trusted their judgement implicitly and followed 100% of their recommended changes. When our house finally came on the market, there was a blizzard of serious interest, we had multiple offers by the third day and it sold in just 5 days after a frenzied bidding war for 20% above our asking price! The investment we made in upgrades recommended by Jim and Donna yielded a 4-fold return, in the process setting a new high water mark for a house sold in our community.

In our view, there are no better real estate professionals in all of San Diego than Jim and Donna Klinge. Buying or selling, you must run and beg Jim and Donna Klinge to represent you! Our family will never forget Jim, Donna, and their whole team at Compass — we are forever grateful to them.

Lou F

March 27, 2025

Trustindex verifies that the original source of the review is Google.

WeI had the pleasure of working with Klinge Realty Group to sell our home in Carmel Valley, and I cannot recommend them highly enough!

Jim and Donna demonstrated exceptional professionalism, offering expert guidance on market conditions and pricing strategy, which resulted in a quick and successful sale.

Communication was prompt and we were well-informed throughout the entire process.

For anyone looking for a dedicated and knowledgeable real estate team, look no further!

---

William Sams

March 25, 2025

Trustindex verifies that the original source of the review is Google.

Donna and Jim Klinge of Klinge Realty Group have our highest possible recommendation. From Donna and Jim’s first visit to our house through closing their advice and counsel was candid and honest in all dealings. They kept us fully informed throughout the process. The house sold less than three days after listing with a two-week closing. My wife and I have sold several houses during our lives. This was by far the best experience. Klinge Reality is a premium service realtor. You can’t make a better choice for someone to sell your home fast and for top dollar.

Emily Hernandez

December 29, 2024

Trustindex verifies that the original source of the review is Google.

Donna and Jim provided exceptional support and professionalism throughout the entire process. We couldn't have been happier with their efforts. They made our house shine, and thanks to their expertise, it sold above the listing price in the very first weekend! Truly a fantastic experience from start to finish.

Jesus Adrian Sahagun

November 11, 2024

Trustindex verifies that the original source of the review is Google.

This year has been difficult on our family, mainly due to having to sell our home. Thankfully we knew God had a plan for us and working with the Klinge team was a key part of it. It was an obvious decision to work with them again after such an amazing experience when purchasing the same home we needed to sell. The challenge was, how will we do this in so little time with so much going on? Jim and Donna held our hand every step of the way. Whenever an unexpected issue arose they found and provided a solution. Never once did we feel pressured to make a decision and the Klinges were always reassuring after providing the information that the decision was ours to make. Despite the curve balls, they never panicked and exemplified the “can do” attitude, making us feel optimistic and taken care of. Their expertise and professionalism was superb. But of all the reasons to work with the Klinges, the most impactful and valuable is their compassion and genuine care for their clients. We pray that we can one day purchase our forever home and you better believe that Jim and Donna will be representing us - as long as they will have us of course. Thank you again Klinge team! Your execution, experience, and care are unmatched.

SABIHA PASHA

July 23, 2024

Trustindex verifies that the original source of the review is Google.

Jim and Donna were fantastic! Jim understanding my needs, recommending potential places, pointing out the pros and cons of each property was invaluable. Then when the offer was accepted Donna’s organized guidance through the inspections, paperwork etc made the whole process seem effortless.

So grateful that I had them on my side!