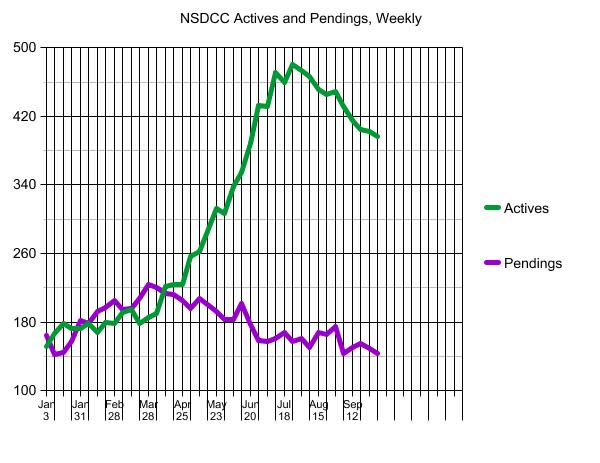

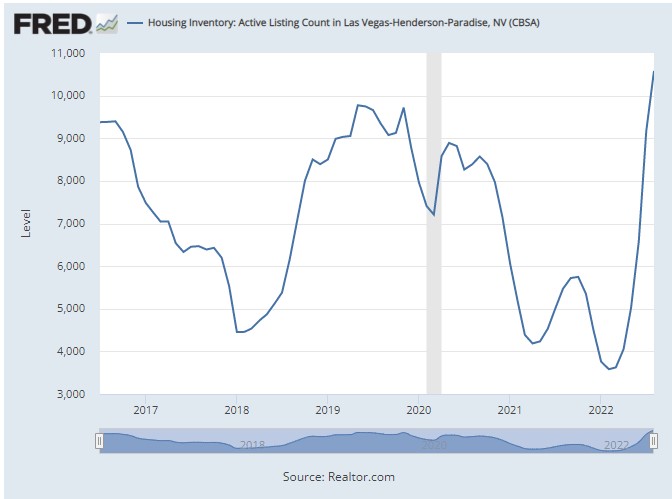

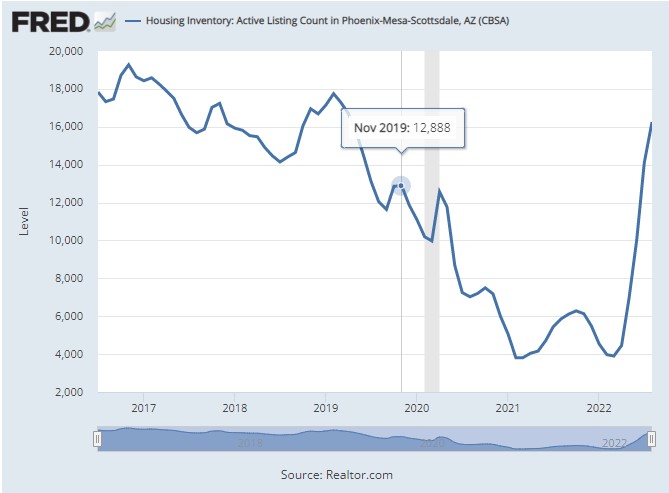

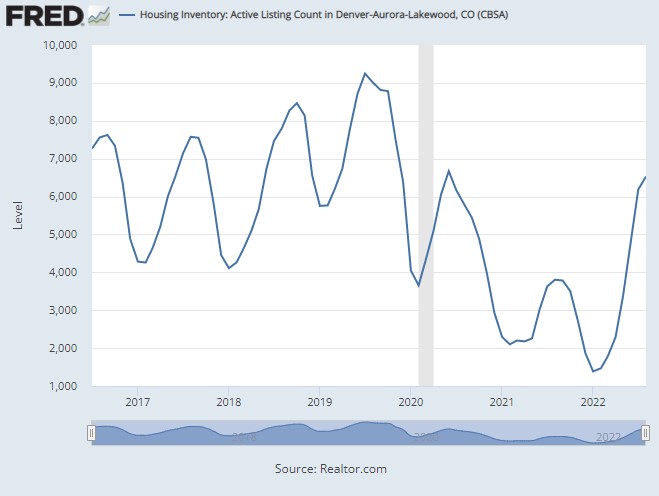

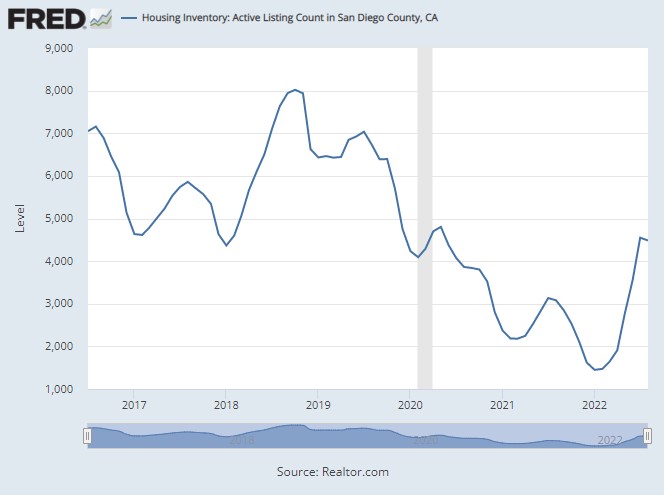

Hat tip to Mark for pointing out how much different our local inventory has performed, compared to other markets around the country. When you hear the doom and gloom from the national talking heads, this is what they are talking about:

Our inventory topped out in July, and has been declining since – where many other markets are exploding. In September, Las Vegas and Phoenix will probably set all-time highs for their number of homes for sale, where we are around half of our peak inventory numbers.

Super-custom estate with commanding ocean views from the best lot in the neighborhood! The previous owner had invested over $1,000,000 in upgrades, and these sellers added their own touches to create a magnificent property. Once through the private gates, it is immediately apparent that the attention to detail is paramount. Expert stone and woodwork set the stage for an elegant example of interior design, sure to impress the most discerning of palates. An open foyer shines in marble. Columned archways, hint at spacious parlors. Custom ironwork adorns the graceful, winding staircase – which frames a grand wine room. The entryway flows past the formal dining room and into an expansive family room – ideal for entertaining and complete with a functional bar and ocean view. A richly appointed, chef’s kitchen is at the ready, for functions large or small, and effortlessly incorporates the finest appliances, rich woods and exotic slab granite. Upstairs, a luxe master suite offers spa-like comfort- whether it’s relaxing in front of the fireplace or taking in your own private sunset, via the secluded balcony. Secondary rooms are beyond comfortable, and there is even a guest room, with en-suite bathroom, down stairs. Choose to step off the beaten path, once again, and take your place at the top of Aviara Point.

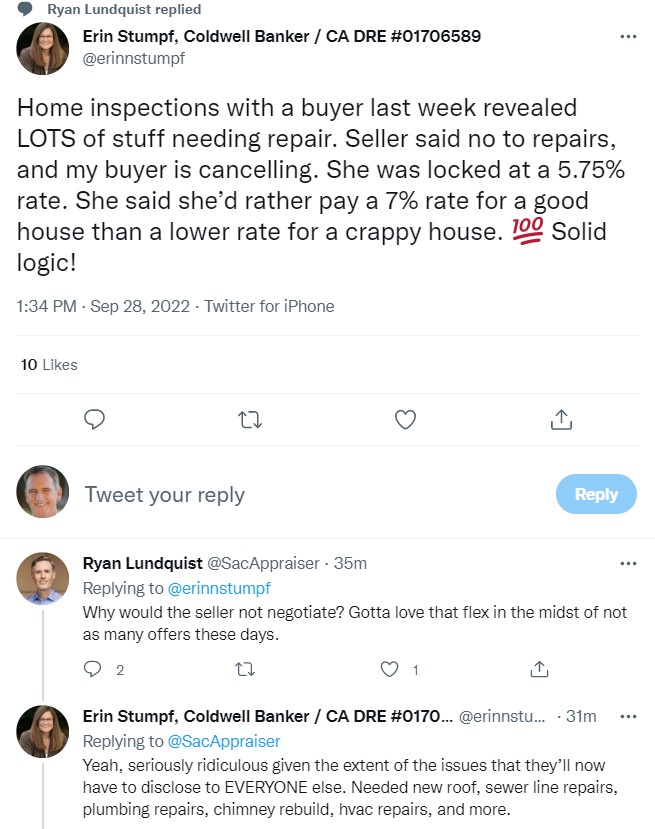

All of the home buyers who were willing to purchase a house ‘as-is’ with no repairs are sitting comfortably in their 3% golden handcuffs contemplating what else to fix.

None of today’s buyers – which is a whole new set of people – are going to tolerate that program.

It would be smart for home sellers to get in front of it. Completing a home inspection before going on the open market is an idea that’s been around for years, but the industry has been slow to adopt – we were always happy to take a chance!

But paying a few hundred dollars for an inspection report and then fixing the defects prior to going on the market provides significant benefits to the sellers:

It gives the buyers confidence that they aren’t buying a money pit when making their offer.

It demonstrates that the sellers have respect for the current marketplace.

It helps to avoid having to sell the home 2-3 times, each at a lower price.

Sellers and agents can do everything right and get into escrow with a buyer, only to have buyer’s remorse kill a deal over one stupid little thing. You know that the buyer’s family and friends have been telling them that they are making a big mistake, and that prices are going to drop – and at this point the buyers are looking for any reason to cancel.

Don’t give them one – even if you have to fix everything on the list!

Available to realtors in the on-going market shift is the chance to elevate their game from the frenzy era. My observations don’t come from being an old veteran because we are far removed from fax machines and the one-page contract (“press hard, there are four copies”). Instead, just basic common sense can reveal changes that would make it easier to sell a home in a tougher market.

Nobody had a problem getting showings and offers during the frenzy. But now it’s different, yet some of the same practices are still with us. You want more showings? Make your listing easier to show!

Two recent examples:

A. Early last Sunday morning, I received a request from a buyer to see six houses priced around $2 million later that afternoon. I guessed that only half of them would be available, and after calling/texting/emailing around to the listing agents, I was able to arrange TWO showings out of the six pursued.

B. Yesterday I had an all-time classic, though some version of this is fairly typical. In spite of the house looking vacant in the photos, the listing agent is requesting 24-hour notice to show. I call, but no answer, so I leave a voicemail. I’m having a busy day, so I had not sent a text yet when I get the call an hour later:

JtR: Hello, this is Jim, can I help you?

Agt: HELLO, you called me?

JtR: Hmmm, yeah maybe – what’s your name (I didn’t recognize the phone number)?

Agt: I’m so-and-so. Are you in real estate? (agent didn’t listen to my voicemail)

JtR: Yes, and I was calling about showing your listing tomorrow.

Agt: Text me your contact info. (I send my name, company, and license number).

The conversation is now changes over to text, instead of by phone.

JtR: I’d like to show your listing.

Agt: What time?

JtR: It’s looks vacant, does it matter?

Agt: Yes, the sellers have cameras, and they like to watch.

JtR: 3:30

Agt: Ok, I’ll send you instructions.

Next, this comes over by text:

Lights in most rooms are on timers (living room, bedrooms, and dining room), so please do not move those light switches. But Lights in the entry, kitchen, and bathrooms are NOT on timers, so you can turn those on, and then off, when done. If you want window blinds opened, turn slats 90 degrees open to let light in, but please do not raise the blinds. When done, turn all window slats fully closed to avoid sun damage. Use slider door in kitchen to access patio. Please turn slider door slats to perpendicular first before moving the slats to the right to go outside. There is a ROD in the door track, just remove it. Please return rod to door track, lock door, fully close blinds when done. And All must wear Booties and Masks and all supplies are in entry foyer. If booties have run out, take off shoes. Water is turned off until accepted offer, so let your party know to plan ahead, as toilet can not be used and no water to wash hands (sorry). Office upstairs could be turned into mirror image of adjacent bedroom. Solar panels are owned by Seller. FYI. Cameras are throughout home. Thanks so much for showing. If you have any questions, please ring my cell phone for faster reply and text too. Thank you!

I’m sure the agent is probably thinking that this is all helpful information. But all I’m thinking about is how difficult it would be to try and negotiate an offer with them – they will want everything to go their way. During the frenzy, buyer-agents accepted that the listing agents were going to beat the crap out of you, and we just had to take it. But not now.

Yet, have listing agents adjusted their approach?

When you list your home with me, I’ll tell you up front that it is in our best interest to show the home seven days a week with little or no notice. Not only do we have more showings, but it also sends the message to buyers and agent that we have respect, and want to make it easy to buy the home – with no cameras!

The local market conditions appear to be getting worse every day, mostly because the headline writers and social-media experts are piling on now. What can listing agents do?

When most agents are content to show their listings and then go wait by the phone, there are alternatives. Hat tip to our manager Steve Salinas for bringing up the Reverse Offer technique in our sales meeting!

For two years, the buyer-agents have just been telling their clients to bid hundreds of thousands of dollars OVER the list price, so now they may need some help with advising their buyer on how to proceed in this market. When a buyer shows some interest in the home, the listing agent can reach out to the buyer’s agent with more than just a casual request for feedback.

The Reverse Offer is where the listing agent suggests price and terms to the buyer-agent that might be the foundation of a potential deal. It needs to be handled tactfully, and with the seller’s knowledge so it’s not a breach of fiduciary or a waste of time.

It can be as casual as mentioning any needs the seller might have in their exit plan, or for terms that would be advantageous to the buyer like seller financing or rate buydowns. But it can also be as formal as issuing written offers signed by the seller for the waiting buyers to consider – here’s more:

It’s worth considering because what’s the alternative? To just sit by the phone and hope it rings, and when it doesn’t, go tell the seller to dump on price?

This is the Wait-and-See period when buyers are so comfortable on the fence that it’s going to take something different to get them to buy a home. Dumping on price during the Wait-and-See period only makes the home buyers think that if they just wait longer, the prices will go down more.

Agents should offer their sellers some alternatives to that!

We were discussing the “mold” found by a home inspector, who wasn’t qualified to comment on the subject – though that didn’t stop him from trying to scare the daylights out of the buyer just so he could CYA.

I suggested that it was the garden-variety mildew that could be removed with a squirt of bleach and a wipe of a cloth. After all, it tested ‘dry’ and the minor stain under the kitchen sink looked like it was years old.

Of course, they asked, “What do you know about mold?”

Re-purposing commercial and industrial properties into residential developments is an idea that should have been fast-tracked years ago. Bills were signed by the governor yesterday, and they make it look like thousands of new homes will be built shortly.

But there is more to it, of course, since politicians and lobbyists are involved. They want unions to build them, and/or they want some or all of the homes to be for low-income housing.

For years, California state lawmakers have tried to reconcile warring views on what labor standards should be required of developers who’d be allowed to build housing more easily and quickly to combat the housing crisis.

Most recently that debate has splintered organized labor over two bills that both unlock commercial real estate for residential use. The Senate’s bill has the backing of the powerful state Building and Construction Trades Council, while the Assembly’s bill counts on support from affordable housing developers and the state’s Conference of Carpenters. The Legislature’s progress on housing for this session was framed as recently as last week as a battle between these two forces over the bill in the Assembly.

But following weeks of tense negotiations between the two unions over the labor provisions in the Assembly’s bill, the labor groups failed to hammer out a compromise.

So instead of choosing sides, leadership in the state Assembly and Senate simply gave their seal of approval to both bills. They opted to give developers two choices if they want to build housing where strip malls once were: Comply with stricter affordability standards or stricter labor standards.

Senate Pro Tem Toni Atkins, a San Diego Democrat, called the two-bill package “a monumental legislative agreement, and one of the most significant efforts to streamline and amplify housing production in decades.”

If passed, both bills would apply to overlapping sites — and leave the choice of which policy to use in the developer’s hands.

I am running short on videos – there are fewer homes for sale, and the list of homes worthy of a video is even shorter. We saw this one a couple of months ago, and it just closed on September 16th for $3,600,000, which was $100,000 over list. Knowing that, the video might be more intriguing now?

Trustindex verifies that the original source of the review is Google.

Jim & Donna Klinge helped us sell our home of 30 years in Ocean Hills. We were very happy with their service and would HIGHLY recommend them to anyone looking for an Honest, Knowledgeable, Skilled, Informed Efficient realty team. Both Jim & Donna were so helpful in different ways and complemented each others skills. Please refer to a more detailed review that we wrote on YELP. Thank You Both for all your help!!!

Jesse O'Hara

June 12, 2025

Trustindex verifies that the original source of the review is Google.

A+ thank you

Lisa Tuomi

June 11, 2025

Trustindex verifies that the original source of the review is Google.

Many years ago, we purchased a home in Carlsbad, using a realtor that was recommended to us - Jim Klinge. Fast forward to 2025, we recently had the privilege of selling 2 homes in Carlsbad, CA and didn't hesitate to reach out to Jim and Donna Klinge of Klinge Realty Group to guide us through the sales. The transactions were very different, each with its own unique situation, opportunities and challenges. From start to finish, Donna and Jim helped navigate the pre-sale preparation, the listing, showing of the house, buyer negotiations, the final close and all of the paperwork and decisions in between. What stands out with both transactions is the professionalism of Jim and Donna (and their team), wonderful communication (timely, relevant, concise), their deep understanding of market dynamics (setting realistic expectations), their access to top-notch contractors, and last, their ability to guide us across the finish line successfully. We wouldn't hesitate to use Jim and Donna in the future and highly recommend them for anyone looking to buy or sell a property in North San Diego County.

Jerry Meyer

March 28, 2025

Trustindex verifies that the original source of the review is Google.

We sold a home with Jim and Donna and from beginning to end they were consummate professionals. Their initial walk through the property resulted in a list of items to be repaired or updated. They supplied a list of vendors and job quotes to do the repairs and updates. We originally wanted to sell ‘as is’ and just get it over with. They gave us a selling price for ‘as is’ and options for doing a few updates/repairs to doing it all with the selling price for each option. We agreed to do all they suggested and we sold for the exact price they predicted. For every dollar spent we got back more than $2 back in the selling price. And they got that price in a rising interest rate environment! Donna and Jim are extremely detailed and guide you through ever aspect of the sale. There were no surprises thanks to their guidance. We couldn’t be more pleased with their representation.

Thank you Donna and Jim,

Jerry and Mary

Heather Quejada

March 27, 2025

Trustindex verifies that the original source of the review is Google.

We have known Jim & Donna Klinge for over a dozen years, having met them in Carlsbad where our children went to the same school. As long time North County residents, it was a no- brainer for us to have the Klinges be our eyes and ears for San Diego real estate in general and North County in particular. As my military career caused our family to move all over the country and overseas to Asia, Europe and the Pacific, we trusted Jim and Donna to help keep our house in Carlsbad rented with reliable and respectful tenants for over 10 years.

Naturally, when the time came to sell our beloved Carlsbad home to pursue a rural lifestyle in retirement out of California, we could think of no better team to represent us than Jim and Donna. They immediately went to work to update our house built in 2004 to current-day standards and trends — in 2 short months they transformed it into a literal modern-day masterpiece. We trusted their judgement implicitly and followed 100% of their recommended changes. When our house finally came on the market, there was a blizzard of serious interest, we had multiple offers by the third day and it sold in just 5 days after a frenzied bidding war for 20% above our asking price! The investment we made in upgrades recommended by Jim and Donna yielded a 4-fold return, in the process setting a new high water mark for a house sold in our community.

In our view, there are no better real estate professionals in all of San Diego than Jim and Donna Klinge. Buying or selling, you must run and beg Jim and Donna Klinge to represent you! Our family will never forget Jim, Donna, and their whole team at Compass — we are forever grateful to them.

Lou F

March 27, 2025

Trustindex verifies that the original source of the review is Google.

WeI had the pleasure of working with Klinge Realty Group to sell our home in Carmel Valley, and I cannot recommend them highly enough!

Jim and Donna demonstrated exceptional professionalism, offering expert guidance on market conditions and pricing strategy, which resulted in a quick and successful sale.

Communication was prompt and we were well-informed throughout the entire process.

For anyone looking for a dedicated and knowledgeable real estate team, look no further!

---

William Sams

March 25, 2025

Trustindex verifies that the original source of the review is Google.

Donna and Jim Klinge of Klinge Realty Group have our highest possible recommendation. From Donna and Jim’s first visit to our house through closing their advice and counsel was candid and honest in all dealings. They kept us fully informed throughout the process. The house sold less than three days after listing with a two-week closing. My wife and I have sold several houses during our lives. This was by far the best experience. Klinge Reality is a premium service realtor. You can’t make a better choice for someone to sell your home fast and for top dollar.

Emily Hernandez

December 29, 2024

Trustindex verifies that the original source of the review is Google.

Donna and Jim provided exceptional support and professionalism throughout the entire process. We couldn't have been happier with their efforts. They made our house shine, and thanks to their expertise, it sold above the listing price in the very first weekend! Truly a fantastic experience from start to finish.

Jesus Adrian Sahagun

November 11, 2024

Trustindex verifies that the original source of the review is Google.

This year has been difficult on our family, mainly due to having to sell our home. Thankfully we knew God had a plan for us and working with the Klinge team was a key part of it. It was an obvious decision to work with them again after such an amazing experience when purchasing the same home we needed to sell. The challenge was, how will we do this in so little time with so much going on? Jim and Donna held our hand every step of the way. Whenever an unexpected issue arose they found and provided a solution. Never once did we feel pressured to make a decision and the Klinges were always reassuring after providing the information that the decision was ours to make. Despite the curve balls, they never panicked and exemplified the “can do” attitude, making us feel optimistic and taken care of. Their expertise and professionalism was superb. But of all the reasons to work with the Klinges, the most impactful and valuable is their compassion and genuine care for their clients. We pray that we can one day purchase our forever home and you better believe that Jim and Donna will be representing us - as long as they will have us of course. Thank you again Klinge team! Your execution, experience, and care are unmatched.

SABIHA PASHA

July 23, 2024

Trustindex verifies that the original source of the review is Google.

Jim and Donna were fantastic! Jim understanding my needs, recommending potential places, pointing out the pros and cons of each property was invaluable. Then when the offer was accepted Donna’s organized guidance through the inspections, paperwork etc made the whole process seem effortless.

So grateful that I had them on my side!