The first week after the realtor-lawsuit verdict went as expected – chaos, doom, and no sexy alternatives. It will take years to appeal, but it won’t matter how it turns out. Buyers are going to be paying their agents.

If sellers aren’t obligated to pay any commission to the buyer-agents, will they appreciate the benefit of incentivizing buyer-agents with a bounty, or reward? Probably not, unless their listing agent makes it very clear, and insists on it.

It is more likely that listing agents won’t push it, and because sellers naturally will want to pay less commission and not more, they will list for 2.5% or 3% and hope for the best. Both will shrug it off, and joke about how it’s about time commissions came down!

It will be a grave mistake.

Why? Because the buyer-broker agreement is a disaster:

Buyers won’t like it.

Agents won’t like it.

The market won’t like it.

Today’s buyers are picky, and you can’t blame them. They’ve had to endure +40% on prices, +200% on interest rates, and -50% on inventory…..talk about challenging!

The buyer-broker agreement will be a disaster because both agents and buyers will sign a short-term arrangement and hope the seller might kick in some of the commission. But then everyone will go back to doing it the same way we always have – refreshing your feed every hour and praying!

The real opportunity will be for buyers to hire an aggressive buyer-agent who does more than just watch the MLS. When a seller hires a listing agent, they get a thorough marketing campaign to source every potential buyer in the market. Buyer-agents can do the same, in reverse!

The buyer-agents who offer a rifle-shot soliciting of specific homes that fit the needs perfectly of their buyers will eventually find one. If an aggressive buyer-agent brings the complete package to the seller’s table without having to mess with a full listing, they will likely get an audience. It could even take the place of listing agents!

Because auctions aren’t close yet, this could be what changes the world of residential resales!

It will mean more off-market sales, which means more fuzzy comps because not much if anything is known about the home’s condition. But if it catches fire and the MLS or a rogue search portal insists on buyer-agents reporting everything about their sales including photos, we could still have a database full of accurate market data. But if we don’t, we don’t – good luck everybody!

Though the industry is reeling from the controversial lawsuit verdict last week, new listings and new sales keep happening every day – people want and need to move, thankfully.

We are too close to the end of the year to have any violent swings in the market. Anything that happens from now on will be blamed on the holidays. Thanksgiving is only 17 days away!

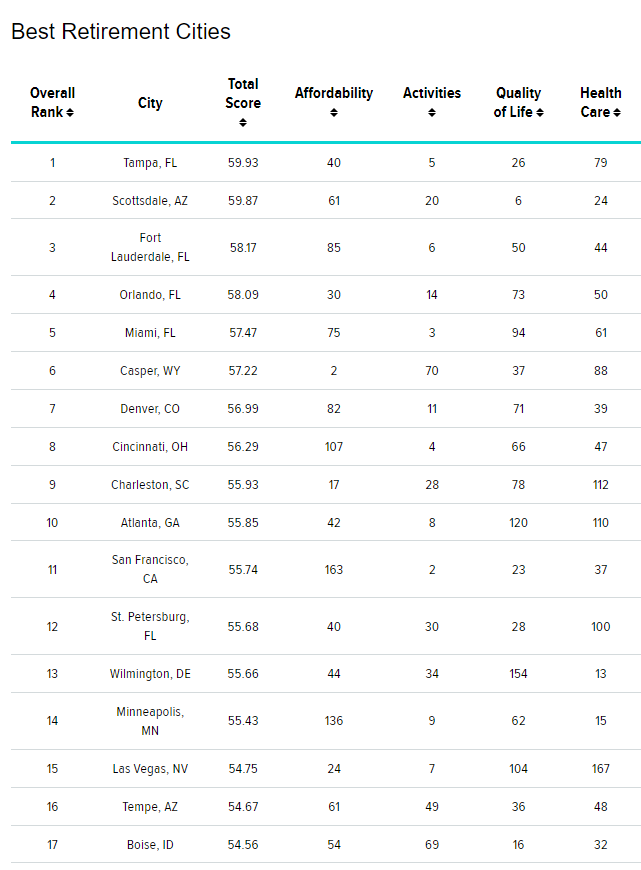

After putting in decades of hard work, we naturally expect to have financial security in our golden years. But not all Americans can look forward to a relaxing retirement. According to the Employee Benefit Research Institute’s 2023 Retirement Confidence Survey, 64% of workers reported feeling at least somewhat confident that they will have enough money to retire comfortably, but only 27% said they were “very confident.”

If so many American workers are worried about their financial future, what other options provide a pathway to a comfortable retirement? For some, the only solution is to keep working. According to Gallup polling, workers in 2022 planned to retire at age 66 on average, compared to age 60 in 1995. The alternative? Relocate to an area where you can stretch your dollar without sacrificing your lifestyle.

Retirement isn’t all about the money, though. Retirees want to live in a place where they enjoy safety and access to good healthcare, especially in the wake of the COVID-19 pandemic. The ideal city will also have lots of ways to spend leisure time, along with good weather.

To help Americans plan an affordable retirement while maintaining the best quality of life, we compared the retiree-friendliness of more than 180 U.S. cities across 45 key metrics. Our data set ranges from the cost of living to retired taxpayer-friendliness to the state’s health infrastructure.

The latest lawsuit will cause people to consider different pay structures for realtors.

If realtors were paid less, could they at least get some of it up front? Yes, if approved by the commissioner:

Before a broker may solicit, advertise for and agree to receive an advance fee, the paperwork material is to be submitted to the Commissioner of the California Department of Real Estate (DRE) for approval at least 10 calendar days prior to use.

If the Commissioner, within 10 calendar days of receipt, determines the material might mislead clients, the Commissioner may order the broker to refrain from using the material.

To be approved, the advance fee agreement and any materials to be used with the agreement will:

Contain the total amount of the advance fee and the date or event the fees will become due and payable;

List a specific and complete description of the services to be rendered to earn the advance fee;

Give a definite date for full performance of the services described in the advance fee agreement; and

Contain no false, misleading or deceptive representations.

Further, the advance fee agreement may not contain a provision relieving the broker from an obligation to perform verbal agreements made by their employees or agents; or a guarantee the transaction involved will be completed.

It sounds like slipping a few thousand under the table won’t be tolerated! The paperwork involved will probably make the big brokerages shy away from the idea, but we should consider alternative ideas.

When tenants live in a property, they cause some degree of wear and tear. This can range from minimal scuffs on walls to more serious harm, such as stained carpets or broken appliances. It’s important to recognize that wear and tear is different from intentional damage or neglect by the tenants.

Landlords must think about factors like tenancy length, number of occupants, and property condition before the tenant moved in to decide what counts as normal wear and tear. A well-maintained property will get less wear and tear compared to one that has been neglected.

Here are frequently asked questions:

FAQ 1: What is wear and tear? It is the gradual deterioration of a property as a result of normal everyday use by tenants. It includes minor damages, deterioration, and natural aging of the property. Landlords cannot hold tenants responsible for the cost of repairing or replacing items due to normal wear and tear.

FAQ 2: How can landlords differentiate between degradation and tenant damage? Landlords should consider the overall condition of the property, the age of the item in question, and the length of the tenancy. Minor scuffs and marks are usually considered wear and tear, while significant damage caused by negligence or abuse is considered tenant damage.

FAQ 3: Can landlords deduct the cost of wear and tear from the security deposit? No. Security deposits are intended to cover intentional damages or neglect by tenants that go beyond normal use. Calculate depreciation to claim the correct amount from security deposits.

FAQ 4: How can landlords protect themselves? It is highly recommended for landlords to conduct a thorough move-in inspection with photographs will help in accurately determining any additional damages caused by the new tenant during their stay. Do an additional move-out inspection with photos when they leave.

FAQ 5: What can landlords do to prevent excessive wear and tear? Landlords can take several measures, such as, 1) regularly conducting property inspections, 2) providing clear guidelines on maintenance and care – especially for specific features of the property, such as hardwood floors or countertops, 3) promptly addressing repair requests, and 4) using durable and easy-to-maintain materials in the property.

Educating tenants about proper maintenance practices can help prevent unnecessary wear and tear too!

Commissions aren’t all the same, just like agents aren’t all the same. Different agents charge different rates because they do different things for the consumer. Commissions/fees range from $100 to 7%. Nice range!

So if all that matters is paying less for your agent, then shop around – there are plenty of discount agents. You might consider hiring the very best agent you can find – one who pays for themselves, and more.

This is the question that has never been answered by the industry:

“If agents employ different skill sets and services, why do they all get paid the same?

It was mentioned in the recent lawsuit, and they presented it as part of their case:

72. Additionally, because the Rule requires a blanket offer, the Rule compels home sellers to make this financial offer without regard to the experience of the buyer-broker or the services or value they are providing — in other words, the Rule treats all buying brokers and their services the same. The seller is required to offer the same fee to a buyer-broker with little or no experience as that offered to a buyer-broker with twenty years of valuable experience. Accordingly, there is a significant level of uniformity in the payments that sellers must pay to buyer-brokers.

73. As a result, there is little relationship between the commission and quality of the service. “Skilled, experienced agents and brokers charge about the same price as agents with little experience and limited knowledge of how to best serve the consumer clients.” In a price-competitive market, less experienced and less skilled brokers and salespersons would be offering consumers lower commission rates, but they have no incentive to do so because of the Rule.

74. The Rule creates tremendous pressure on sellers to offer the “standard” supra-competitive commission that has long been maintained in this industry. Seller-brokers know that if the published, blanket offer is less than the “standard” commission, many buyer-brokers will “steer” home buyers to the residential properties that provide the higher standard commission.

The changes or fines from the lawsuit(s) probably won’t matter much today. Offering no commissions to buyer-agents is a nice idea, and you’d think it would cause agents to publicize the full set of productive services they offer to their buyers to convince them to pay the fee. Don’t get your hopes up.

Ideally, the consumer would research the detailed resumes and work histories of each prospective agent and make an informed decision. The agent pages on Zillow do provide the basics, but based on results, consumers aren’t using them much.

It’s why realtors have a lousy reputation – consumers keep hiring the inexperienced/bad agents, and the industry doesn’t mind because they make more profit off them.

These are getting into the lazy zone now because predicting 2% to 4% increases over the next 12 months doesn’t take any real forecasting – they are just safe guesses based on historical norms which flew out the window with rising rates about 18 months ago.

They might end of being right, but at what cost? Plunging sales. To conduct real price discovery we would need a surge of new listings to test the demand, if any. Having 100 or so sales every month in an area of 300,000 people will keep prices elevated because that’s not much of a test – the market is just barely alive.

The National Association of Realtors clearly underestimated the chances of losing this case – and the others to come. They must have thought that touting their 100-year old Code of Ethics was all that was needed to impress people, and instead they found out that it doesn’t.

What doesn’t get addressed is the common belief that realtors are overpaid.

It is a wide-spread belief. Even Joe Kernen, a guy who works 15 hours per week and gets paid between $3,000,000 and $22,000,000 per year (depending on the website), has to open his CNBC show today with the declaration that 6% commissions are too much, and 1% would be more like it.

This is what needs to be addressed. Can agents explain their value?

Listing agents are used to making a presentation to homeowners, but 80% of the time, the sellers have already decided on who they will hire so the presentation doesn’t have to be great. Buyer-agents rarely discuss what they do – they just have people jump in their car and go look at houses.

The judge and/or the Department of Justice will rule on future sellers paying the buyer-agent commission. If sellers are allowed to pay a commission to the buyer-agents, then their listing agent can counsel them properly on what rate to offer, and the status quo will endure. But it will be a game-changer if the sellers are no longer able to offer ANY commission to buyer-agents.

With the former, the listing agents will have to discuss the pros and cons in detail to the sellers, and agree to a comfortable amount. With the latter, the buyer-agents will have to create a presentation to convince their buyers to pay them directly. This will be a new practice, and they won’t be very good at it.

By the end of the day yesterday, I had already been notified of three different seminars being offered about using the Buyer-Broker Agreement. It sounds simple enough to the ivory-tower types – just get your buyers to pay you the commission! But they underestimate both sides.

Agents aren’t jumping at the chance to work with buyers in the current market.

It takes months or years for buyers to finally win the right home at the right price, and the abuse from the listing agents is mean and nasty along the way. Nobody plays by the same rules, and multiple offers are mishandled regularly, which delays the buyer finally getting a house.

The 2024 Selling Season will begin with buyer-agents pleading with their prospects to sign a contract to pay them a commission. It will only take a few months for this practice to get exposed. The buyers will be reluctant to sign, and those that do sign a contract will find out that it won’t change the outcome. It is still going to take months to find the right house, at the right price. There will still be the typical aggravations and shenanigans with the listing agents – most of whom now insist on buyers providing a bank statement and lender pre-approval letter just to see a house.

Because the local inventory is will be ultra-low, the desperation will cause buyers to blame their agent. It is a fact of life with both sellers and buyers – if they don’t get the outcome they want, it’s too easy to blame their agent (especially when it is true most of the time).

Will sellers and buyers be more diligent about who they hire?

They never have been – they just grab an agent and hope for the best. They don’t know the right questions to ask; they don’t want to waste time investigating thoroughly; and besides, the buyers just want a house, and the sellers just want their money.

This is where each agent and the industry at large could go a long way towards providing a solution.

If there was an outpouring of explanations on how the business works, what to expect, and why a consumer should pay the fee, it would help. Maybe write a blog or something!

Without a delberate attempt to educate everyone, the business will gravitate to the lowest common denominator – single agency, where buyers go direct to the listing agent, and the benefits of buyer-agency are slowly forgotten. Next year will be the phase-out stage.

It will be the next step towards auctions becoming the way to sell houses!

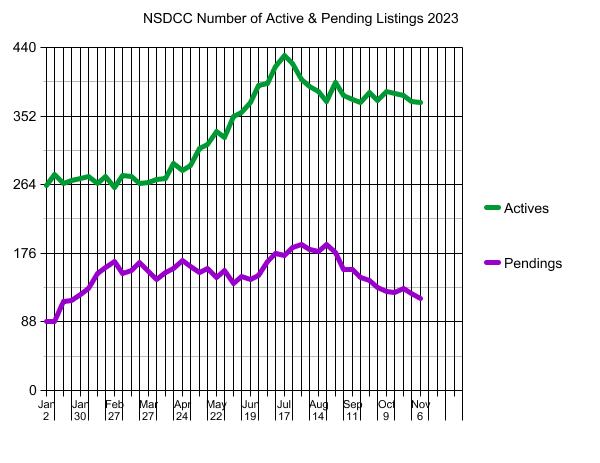

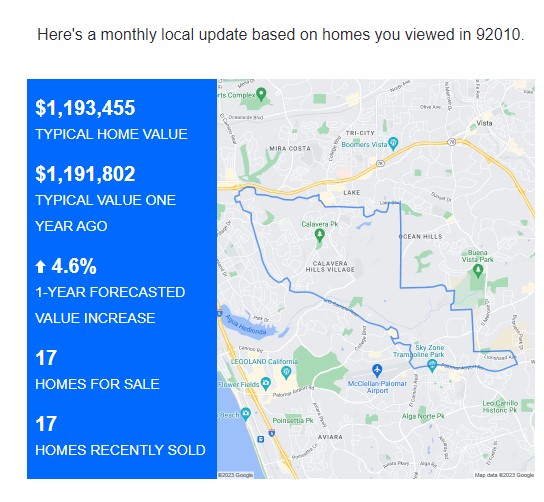

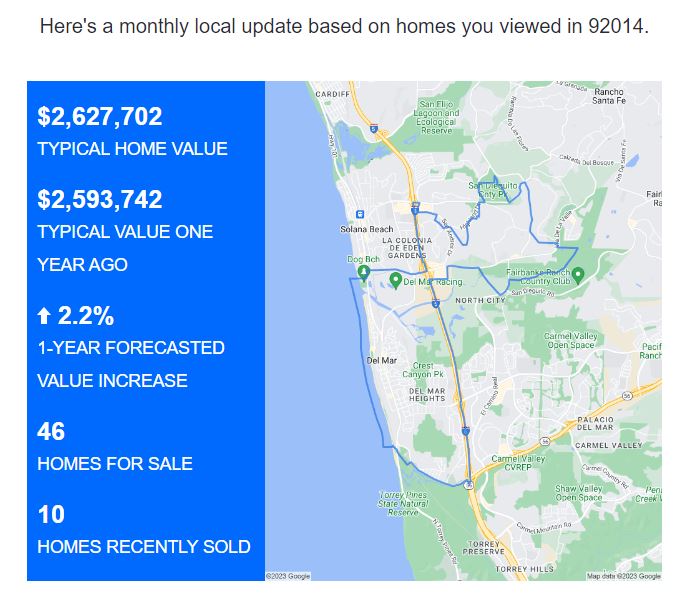

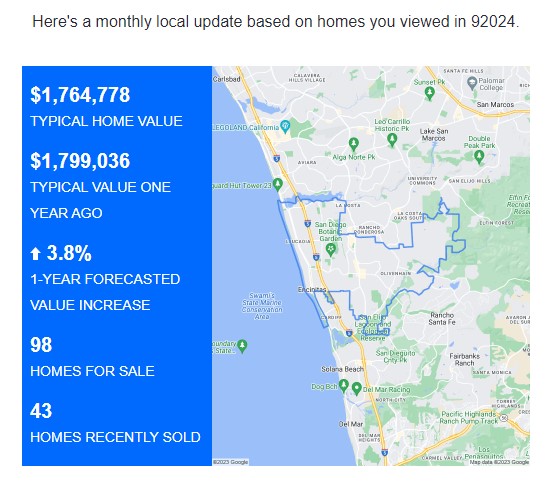

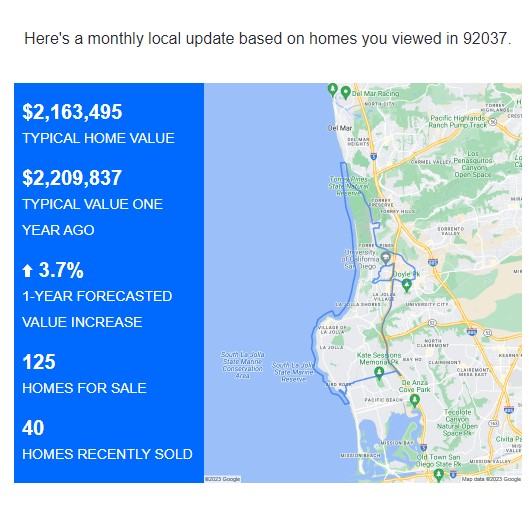

They update the previous month’s stats on the first of month, so here’s the latest for Carmel Valley, Carlsbad, and Encinitas:

Encinitas had an crazy price bump in June, but toss that stat out and the pricing looks fairly steady. There just aren’t enough homes for sale that deserve the money. Until sales bottom, having the pricing hold up will be a challenge, especially with sellers enjoying the unnaturally high appreciation rate over the last 3+ years – if they have to give back 5% to 10% to make a deal, it won’t hurt them much.

Trustindex verifies that the original source of the review is Google.

A+ thank you

Lisa Tuomi

June 11, 2025

Trustindex verifies that the original source of the review is Google.

Many years ago, we purchased a home in Carlsbad, using a realtor that was recommended to us - Jim Klinge. Fast forward to 2025, we recently had the privilege of selling 2 homes in Carlsbad, CA and didn't hesitate to reach out to Jim and Donna Klinge of Klinge Realty Group to guide us through the sales. The transactions were very different, each with its own unique situation, opportunities and challenges. From start to finish, Donna and Jim helped navigate the pre-sale preparation, the listing, showing of the house, buyer negotiations, the final close and all of the paperwork and decisions in between. What stands out with both transactions is the professionalism of Jim and Donna (and their team), wonderful communication (timely, relevant, concise), their deep understanding of market dynamics (setting realistic expectations), their access to top-notch contractors, and last, their ability to guide us across the finish line successfully. We wouldn't hesitate to use Jim and Donna in the future and highly recommend them for anyone looking to buy or sell a property in North San Diego County.

Jerry Meyer

March 28, 2025

Trustindex verifies that the original source of the review is Google.

We sold a home with Jim and Donna and from beginning to end they were consummate professionals. Their initial walk through the property resulted in a list of items to be repaired or updated. They supplied a list of vendors and job quotes to do the repairs and updates. We originally wanted to sell ‘as is’ and just get it over with. They gave us a selling price for ‘as is’ and options for doing a few updates/repairs to doing it all with the selling price for each option. We agreed to do all they suggested and we sold for the exact price they predicted. For every dollar spent we got back more than $2 back in the selling price. And they got that price in a rising interest rate environment! Donna and Jim are extremely detailed and guide you through ever aspect of the sale. There were no surprises thanks to their guidance. We couldn’t be more pleased with their representation.

Thank you Donna and Jim,

Jerry and Mary

Heather Quejada

March 27, 2025

Trustindex verifies that the original source of the review is Google.

We have known Jim & Donna Klinge for over a dozen years, having met them in Carlsbad where our children went to the same school. As long time North County residents, it was a no- brainer for us to have the Klinges be our eyes and ears for San Diego real estate in general and North County in particular. As my military career caused our family to move all over the country and overseas to Asia, Europe and the Pacific, we trusted Jim and Donna to help keep our house in Carlsbad rented with reliable and respectful tenants for over 10 years.

Naturally, when the time came to sell our beloved Carlsbad home to pursue a rural lifestyle in retirement out of California, we could think of no better team to represent us than Jim and Donna. They immediately went to work to update our house built in 2004 to current-day standards and trends — in 2 short months they transformed it into a literal modern-day masterpiece. We trusted their judgement implicitly and followed 100% of their recommended changes. When our house finally came on the market, there was a blizzard of serious interest, we had multiple offers by the third day and it sold in just 5 days after a frenzied bidding war for 20% above our asking price! The investment we made in upgrades recommended by Jim and Donna yielded a 4-fold return, in the process setting a new high water mark for a house sold in our community.

In our view, there are no better real estate professionals in all of San Diego than Jim and Donna Klinge. Buying or selling, you must run and beg Jim and Donna Klinge to represent you! Our family will never forget Jim, Donna, and their whole team at Compass — we are forever grateful to them.

Lou F

March 27, 2025

Trustindex verifies that the original source of the review is Google.

WeI had the pleasure of working with Klinge Realty Group to sell our home in Carmel Valley, and I cannot recommend them highly enough!

Jim and Donna demonstrated exceptional professionalism, offering expert guidance on market conditions and pricing strategy, which resulted in a quick and successful sale.

Communication was prompt and we were well-informed throughout the entire process.

For anyone looking for a dedicated and knowledgeable real estate team, look no further!

---

William Sams

March 25, 2025

Trustindex verifies that the original source of the review is Google.

Donna and Jim Klinge of Klinge Realty Group have our highest possible recommendation. From Donna and Jim’s first visit to our house through closing their advice and counsel was candid and honest in all dealings. They kept us fully informed throughout the process. The house sold less than three days after listing with a two-week closing. My wife and I have sold several houses during our lives. This was by far the best experience. Klinge Reality is a premium service realtor. You can’t make a better choice for someone to sell your home fast and for top dollar.

Emily Hernandez

December 29, 2024

Trustindex verifies that the original source of the review is Google.

Donna and Jim provided exceptional support and professionalism throughout the entire process. We couldn't have been happier with their efforts. They made our house shine, and thanks to their expertise, it sold above the listing price in the very first weekend! Truly a fantastic experience from start to finish.

Jesus Adrian Sahagun

November 11, 2024

Trustindex verifies that the original source of the review is Google.

This year has been difficult on our family, mainly due to having to sell our home. Thankfully we knew God had a plan for us and working with the Klinge team was a key part of it. It was an obvious decision to work with them again after such an amazing experience when purchasing the same home we needed to sell. The challenge was, how will we do this in so little time with so much going on? Jim and Donna held our hand every step of the way. Whenever an unexpected issue arose they found and provided a solution. Never once did we feel pressured to make a decision and the Klinges were always reassuring after providing the information that the decision was ours to make. Despite the curve balls, they never panicked and exemplified the “can do” attitude, making us feel optimistic and taken care of. Their expertise and professionalism was superb. But of all the reasons to work with the Klinges, the most impactful and valuable is their compassion and genuine care for their clients. We pray that we can one day purchase our forever home and you better believe that Jim and Donna will be representing us - as long as they will have us of course. Thank you again Klinge team! Your execution, experience, and care are unmatched.

SABIHA PASHA

July 23, 2024

Trustindex verifies that the original source of the review is Google.

Jim and Donna were fantastic! Jim understanding my needs, recommending potential places, pointing out the pros and cons of each property was invaluable. Then when the offer was accepted Donna’s organized guidance through the inspections, paperwork etc made the whole process seem effortless.

So grateful that I had them on my side!

Anu Koberg

July 13, 2024

Trustindex verifies that the original source of the review is Google.

We first found Jim through his blog at bubbleinfo.com, which really showcased his knowledge of SoCal real estate. Since then we've done three transactions with Jim and Donna, and they are an incredible full service agency, with Jim's deep market insight and Donna's deft contract and project management. We trust them implicitly in their analysis and strategy, which is based on years of experience. They're always available and on top of things, and we strongly recommend them to anyone.