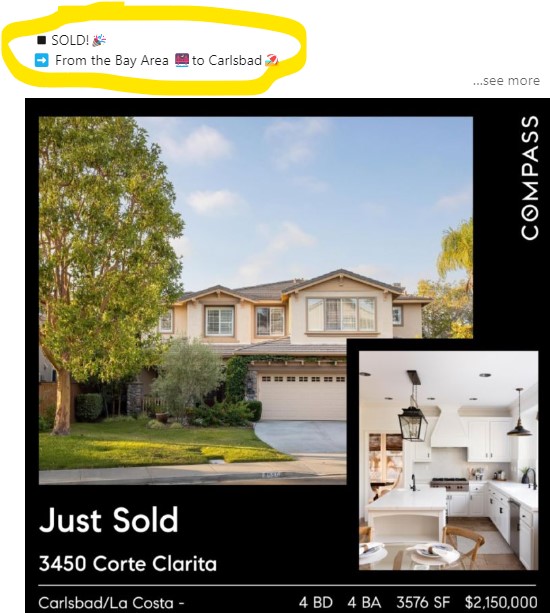

This ibuyer was new in the game and was hoping to make a splash. Somebody there should have known in June of this year that the frenzy was wrapping up before investing $2.5 million cash into a 20-year old basic tract house on a busier street on the fringe of La Costa Valley.

My advice has been clear all along: Spruce ’em up nicely, stage it, price it attractively, and hire me to be your agent. If they would have just done some of those things, this would have turned out better.

Instead, they did no improvements, priced it for what they paid, put it on the MLS as a coming-soon listing before they actually owned it, and then did SEVEN price reductions and THREE listing refreshes before closing escrow today for $1,900,000.

About 1-2 months ago I asked the listing agent if they would take $2,000,000 cash, and he said that the offers were coming in higher than that so….no. And then they close for $1,900,000. This is where the jimjamalama really pays off for sellers!

Sure, when they are higher-end luxury estates in Rancho Santa Fe owned by blog readers!

4124 Stonebridge Lane, Rancho Santa Fe

5 br/6.5 ba, 3,734sf

LP = $15,000 per month.

Stylish one-story contemporary home on 2.87 acres in gated Stonebridge that has recently-updated kitchen and baths, cantina doors, and hardwoods throughout! Pool/spa, solar, tankless water heater, large flat private backyard, and RV parking on site. The 4-car garage was converted to a br/office with full bath and are counted as the 5th bedroom and 6th full bathroom. Partially furnished – what you see in the photos is included. Water, pool maintenance and gardener provided by landlord.

The Uniform Holiday Bill (Public Law 90-363 (82 Stat. 250)) was signed on June 28, 1968, and was intended to ensure three-day weekends for Federal employees by celebrating four national holidays on Mondays: Washington’s Birthday, Memorial Day, Veterans Day, and Columbus Day. It was thought that these extended weekends would encourage travel, recreational and cultural activities and stimulate greater industrial and commercial production. Many states did not agree with this decision and continued to celebrate the holidays on their original dates.

The first Veterans Day under the new law was observed with much confusion on October 25, 1971. It was quite apparent that the commemoration of this day was a matter of historic and patriotic significance to a great number of our citizens, and so on September 20th, 1975, President Gerald R. Ford signed Public Law 94-97 (89 Stat. 479), which returned the annual observance of Veterans Day to its original date of November 11, beginning in 1978. This action supported the desires of the overwhelming majority of state legislatures, all major veterans service organizations and the American people.

Veterans Day continues to be observed on November 11, regardless of what day of the week on which it falls. The restoration of the observance of Veterans Day to November 11 not only preserves the historical significance of the date, but helps focus attention on the important purpose of Veterans Day: A celebration to honor America’s veterans for their patriotism, love of country, and willingness to serve and sacrifice for the common good.

There probably aren’t many people today who expect to see any frenzy left in the marketplace. But here’s a view from the street, looking at actual sales closed over the last 30 days.

At 22 minutes, this turned into a full-length feature film (sorry), but consider it an audio track about the current market conditions, with video evidence to support it.

It sure seemed like there was plenty of extra buffer built into the recent mortgage rates. With the CPI report coming out more favorable than expected, the markets reacted – and boom, a half-point drop!

If buyers get the feeling that both rates and prices are coming their way, it should keep them looking. If there were just a few more quality homes to sell!

It looks like the hefty L.A. mansion tax is going to pass. Don’t be surprised if other cities and counties do the same and pit the rich people vs. everyone else under the guise of solving homelessness.

Measure ULA, the so-called “mansion tax,” is a ballot measure in California that would impose a one-time transfer tax on commercial and residential real estate sales valued at over $5 million.

The tax rate would be 4% for properties valued at $5 million to $10 million and would jump to 5.5% for properties valued at $10 million and above. Homeowners selling a $10 million property, for example, would face $550,000 in additional taxes on the sale.

Laura Raymond, organizer and spokesperson for the Yes on ULA campaign and director of the Alliance for Community Transit-Los Angeles (ACT-LA), a coalition of 42 organizations working toward transit and housing justice, said that the costs of the tax will be carried by the city’s wealthiest and the funds will benefit those most vulnerable.

“The cost-benefit tradeoff is a huge win, and one that will make our city not only more just but also a better place to live for everyone,” Ms. Raymond said.

If passed, the tax will go into effect in April 2023. Without a sunset clause, the tax would be permanent, though it would also be adjusted to keep pace with inflation. To avoid incurring these additional taxes, homeowners of multimillion-dollar estates looking to sell should act before next spring.

Could we have a decent spring selling season next year?

Is there any precedent of our market settling down that quickly?

Home sales had been struggling for months, and then the Lehman Brothers collapse in September, 2008 helped to trigger the Great Recession, and millions of foreclosures and short sales.

Yet, just seven months later, home pricing hit the bottom in San Diego (see graph above).

We are enduring a once-in-a-lifetime spike in mortgage rates that are rightfully taking some time to digest. But people need to move, and by next spring, many will be buying and selling homes around here.

The Fed will have slowed down by then, the political landscape looks like it will drift more towards the center, and realtors are figuring it out that you have to have a spectacular-looking home with an attractive price to have a chance at selling. All will play a role in giving home buyers more confidence.

My listing from two weeks ago that generated 18 offers – 17 of them financed – and got bid up by 27% over the list price is proof that, in spite of the common perception that the market is dead, there is a strong demand right under the surface, just waiting for the right house, at the right price.

Those who were reading this blog in the 2008-2013 will remember how negative we were about the market, and how long it would take before it bottomed out – most figured it would be years and years. True, we aren’t going to get the government stimulus this time, but I don’t think we need it.

There will be a lot of skepticism in the market – and most people will wait until others go first before they think of entering the market themselves. We probably won’t ever see the sizzling frenzy conditions again, but a healthy semi-surge for a couple of months next spring seems like a good possibility. If it happens, it will be because sellers and agents got smart about selling in the post-frenzy era.

Let’s don’t get into modern-day politics because there is no civil discourse any more. Instead, let’s reminisce how it used to be – above is Part 2 of the famous Reagan interview from January, 1975. Part 1 is here:

A benefit of prices going up so fast in early 2022 was that future sellers may not have noticed – and they might be happy to sell for 2021 prices next year. But there are other items that will complicate the matter:

With sales are down as much as 50%, the evidence used to determine values will be as thin as ever.

Most of the listings are not selling. It’s been so long since that has happened – what do you do?

Players will want to believe old principals – namely, it takes longer to sell now.

There will be no change in the perception of realtors’ ability to help.

Higher mortgage rates are here to stay. No help is coming, which is unusual in recent history.

The only hope is that there will be enough decline in pricing between now and March that buyers will be pleasantly surprised, and proceed with their plans to purchase. Working in our favor are the lousy tools we use to measure ‘pricing’, and how nobody wants to look any deeper.

It was here that I estimated that sales prices would have to come down by 30% to fully offset the effect of higher rates. I suggested that it would be a comfortable ride if that happened over the next five years, because sellers today shouldn’t mind getting 0.5% to 1% less than the last guy. It’s the cumulative effect of years’ worth of prices dropping that could see declines of 30% or more.

Will there be sellers who go for a 30% hit next year? Very doubtful, and most would rather wait it out for years before surrendering that much equity – and they may decide to never move.

What might revive the market next spring are reports that prices are 10% to 20% lower.

The sales volume will be hitting all-time lows over the next 2-3 months – there are only 2,756 houses for sale in the county today – and only the highly-motivated sellers will be getting out. If the median sales price drops 2% per month, by March it will be around $770,000, or 16% lower than it was in May!

It may not impress everyone, but it should be enough to get buyers to take a look around! Of course, a lower median sales price is a lousy gauge and it doesn’t mean prices have dropped everywhere. There will be plenty of new listings priced really high, but will buyers keep in the fight? They should, because there will be 10% to 20% of the sellers who really need to move – you just need to dig them out.