What if you convert a vacation home to your primary residence, live there for at least two years and then sell it? Can you qualify for the full $250,000/$500,000 capital gains tax exclusion? No.

If you sell a main home that you previously used as a vacation home, some or all of the gain is ineligible for the home-sale exclusion. The portion of the gain that is taxed is based on the ratio of the period of time after 2008 that the home was used as a second residence or rented out to the total time that the seller owned the house. The remaining gain is eligible for the $250,000 or $500,000 home-sale exclusion.

If you hold rental property, the gain or loss when you sell is generally characterized as a capital gain or loss. If held for more than one year, it’s long-term capital gain or loss, and if held for one year or less, it’s short-term capital gain or loss. The gain or loss is the difference between the amount realized on the sale and your tax basis in the property.

The capital gain will generally be taxed at 0%, 15% or 20%, plus the 3.8% surtax for people with higher incomes. However, a special rule applies to gain on the sale of rental property for which you took depreciation deductions. When depreciable real property held for more than one year is sold at a gain, the rule requires that previously deducted depreciation be recaptured into income and taxed at a top rate of 25%. It’s known as unrecaptured Section 1250 gain, the number of its own federal tax code section.

Take this simple example: You bought a rental home for $300,000, deducted $109,000 of depreciation and sold the property for $500,000 this year. The first $109,000 of your $200,000 gain is unrecaptured Section 1250 gain that is taxed at a maximum rate of 25%, while the remaining $91,000 is taxed at the regular long-term capital gains tax rates.

Note that the unrecaptured Section 1250 gain can also apply to the sale of your main residence if you took depreciation deductions for it in the past, such as from a conversion from a rental home to your primary home or if you had an office in the home.

Capital losses from the sale of rental real estate can offset your capital gains, plus up to $3,000 of other income.

When real property used in a business or held for investment is exchanged for like-kind real property under Section 1031 of the tax code, all or part of the gain that would otherwise be triggered if the realty were sold can be deferred. This tax break doesn’t apply to main homes or vacation homes, but it can apply to rental real estate that you own.

The rules are very complicated and tricky, with many requirements to meet. Also, President Biden and Congress have proposed rules to limit the break. Make sure to talk to your tax adviser if you’re contemplating a like-kind swap.

See eight examples of the capital-gains tax when selling a home here:

With the number of sales taking a dive for the next few months – which could turn out to be a few years – we really don’t need as many realtors. Older agents who have been looking for a reason to retire sure have one now, especially if they believe all the gloom-and-doom:

In 2000, about 5 million homes changed hands — about the same number as 2022 is shaping up to be.

But in 2000, there were 766,000 realtors in America; in July of 2022, there were 1.6 million realtors!

One of the biggest shows of the year rolls into town on Tuesday, and many of us are still scratching our heads about who should headline. I paid to see the Psychedelic Furs play the OAT at SDSU back in the 1980s and always thought they were a fine punk band of the era, but they are old now!

If you are going to the show, make sure you get there early to see the preeminent band of the era:

If the reason the housing frenzy stalled was due to higher mortgage rates – and then mortgage rates come down – shouldn’t it ease the concerns? Unfortunately, the national doom-and-gloom is heavy and persuasive, and reliance on ivory-tower guesses can become a self-fulfilling prophecy.

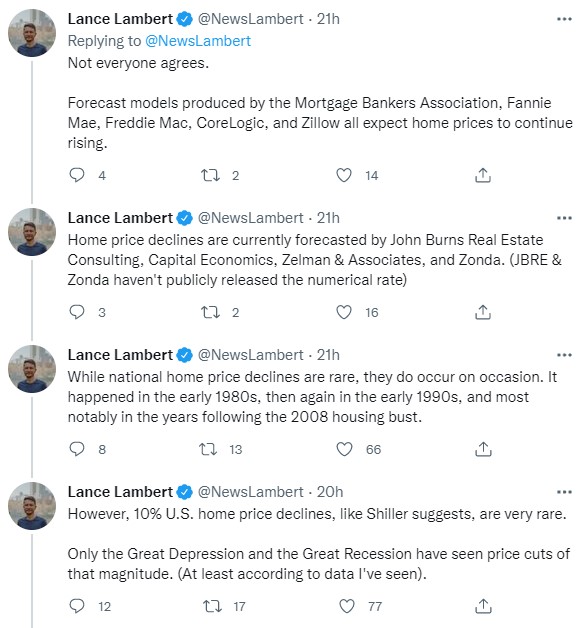

Shiller once again thinks the U.S. housing market is headed for trouble.

“Home prices haven’t fallen since the 2007–09 recession. Right now things look almost as bad,” Shiller said. “Existing home sales are down. Permits are down. A lot of signs that we’ll see something. It may not be catastrophic, but it’s time to consider that.”

A drop in home prices, Shiller says, looks very possible.

“The Chicago Mercantile Exchange has a futures market for home prices…That’s in backwardation now; [home] prices are expected to fall by something a little over 10% by 2024 or 2025. That’s a good estimate,” Shiller told Yahoo Finance. “The risks are heightened right now for buying a house.”

While Shiller thinks a double-digit decline in home prices is possible, many in the industry don’t agree. Over the coming year, home prices are expected to rise. That’s according to forecast models produced by the Mortgage Bankers Association, Fannie Mae, Freddie Mac, CoreLogic, and Zillow. Meanwhile, modest home price declines are currently being forecast by John Burns Real Estate Consulting, Capital Economics, Zelman & Associates, and Zonda.

Why do some industry insiders think home price declines are unlikely? For starters, the country outlawed the subprime mortgages that sank the market a decade ago. Not to mention, homeowners are less debt-burdened this time around. Back in 2007, mortgage debt service payments accounted for 7.2% of U.S. disposable income. Now it’s just 3.8%.

There’s another reason some firms refuse to get bearish on home prices: a historic undersupply of homes.

“Our economists have been chiming in on this for a bit now: The market is slowing down, but homes aren’t getting cheaper anytime soon. Price growth will slow/flatten (when compared to the breakneck start of the year), but the lack of supply is a fundamental pressure that will keep values aloft,” Will Lemke, Zillow’s spokesperson, tells Fortune.

In the eyes of housing bears, firms like Zillow are underestimating the possibility of oversupply. In their view, there’s a chance all those spec homes under construction could see markets like Atlanta, Austin, and Dallas get oversupplied in 2023. If that happens, it would put downward pressure on home prices.

“Housing is believed to be structurally undersupplied, but we run the risk of finding more homes on the market than buyers in the near term due to cyclical factors. I think there’s full awareness that in some markets, an increase in inventory may hit at a bad time—a time where demand has notably pulled back,” Ali Wolf, chief economist at Zonda, tells Fortune. “We are not under the belief that home prices only go up…Our forecast calls for a modest drop in housing prices.”

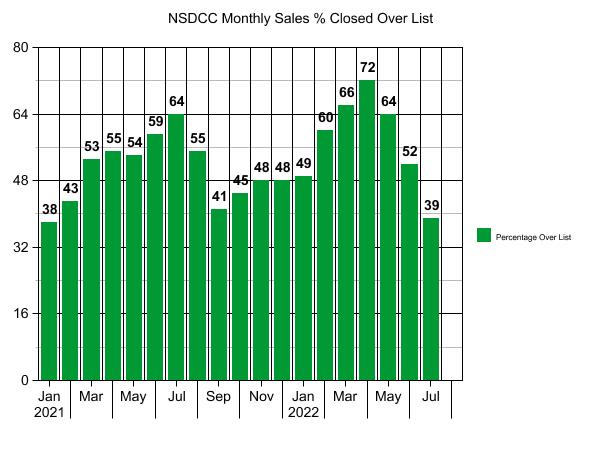

The graph above shows how the 2021 off-season wasn’t off by much, with nearly half of the Nov-Jan sales closing over their list price. We probably won’t see that happen this year!

On the street, it feels like the off-season is already here, which is fine. The seasonality has been topsy-turvy ever since the pandemic started, so we can handle a longer off-season this year. The outcome will be determined by what the listing agents are telling their sellers.

Are they saying that this is the start of a long downward slide, and sellers should hit the panic button and dump on price to get out while they can? If so, shame on them. If 39% of the buyers who closed in July were still paying over the list price, then it suggests that what we are experiencing is an inventory problem – there aren’t many superior houses for sale at decent prices, and the gap between them and inferior houses hasn’t adjusted enough yet.

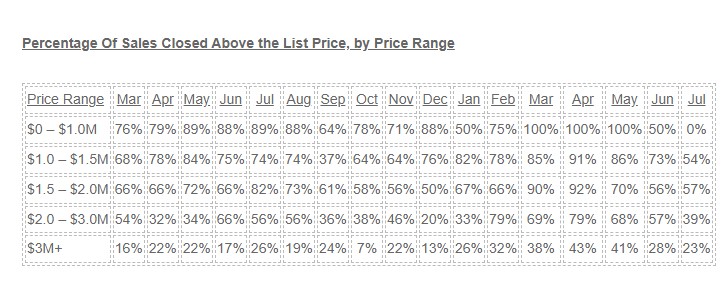

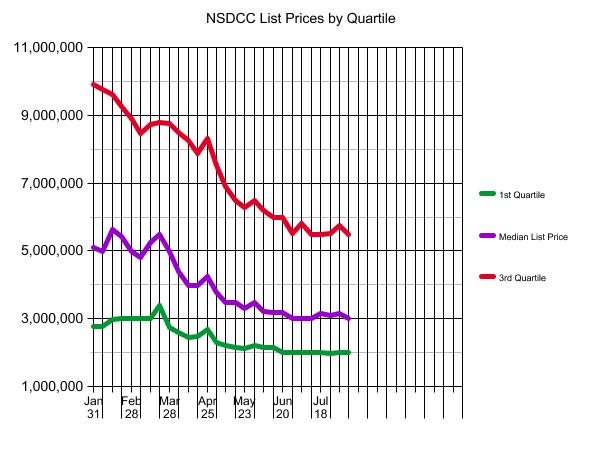

Here is the breakdown by price range:

There was only one sale under $1,000,000, and it was a mobile home. Most of the homes sold between $1,000,000 and $2,000,000 closed for more than their list prices, and the sales above $2 million were still competitive. The group of salable homes is smaller than before, but the great ones are still being bid up.

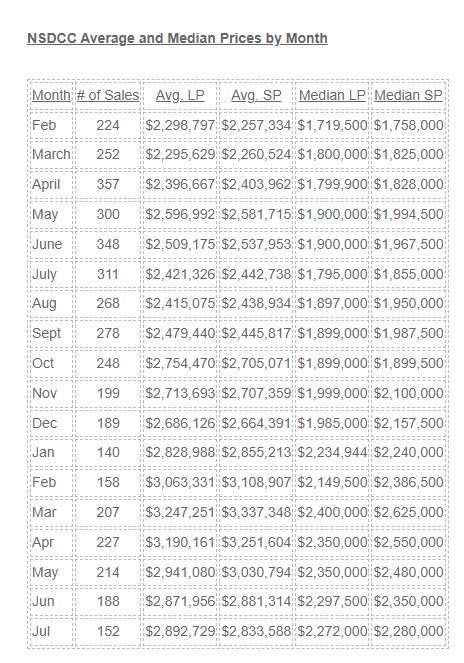

The average and median sales prices are closer to the list prices now, suggesting that those who do bid over the list price aren’t going over by much:

For an industry that has never figured out how to properly handle a bidding war, it is a miracle that this many homes are still selling over list. This was our big chance to incorporate a true auction format, but it will pass us by, unfortunately.

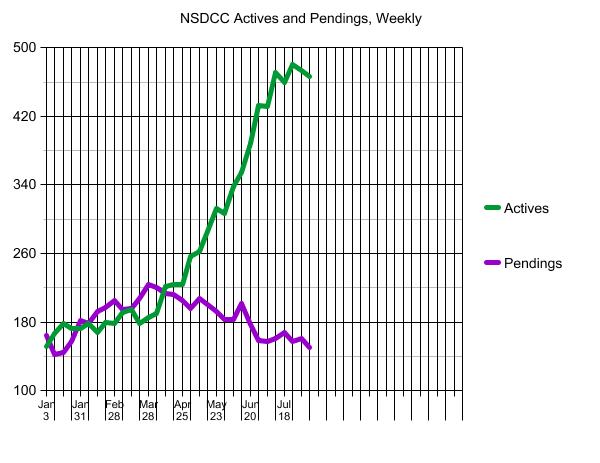

Inventory tends to be seasonal in nature, so we’ve probably seen the peak for 2022.

We’ve probably seen the peak number of pendings for this year too!

Today, there are only 151 homes in escrow, and in July we had 152 sales. It’s feasible that we will have fewer than 100 NSDCC sales in a coming month…..or months!

It doesn’t do any good to lower your price if there are no buyers. Sellers of superior homes should wait it out and take their chances later….because the next selling season is right around the corner.

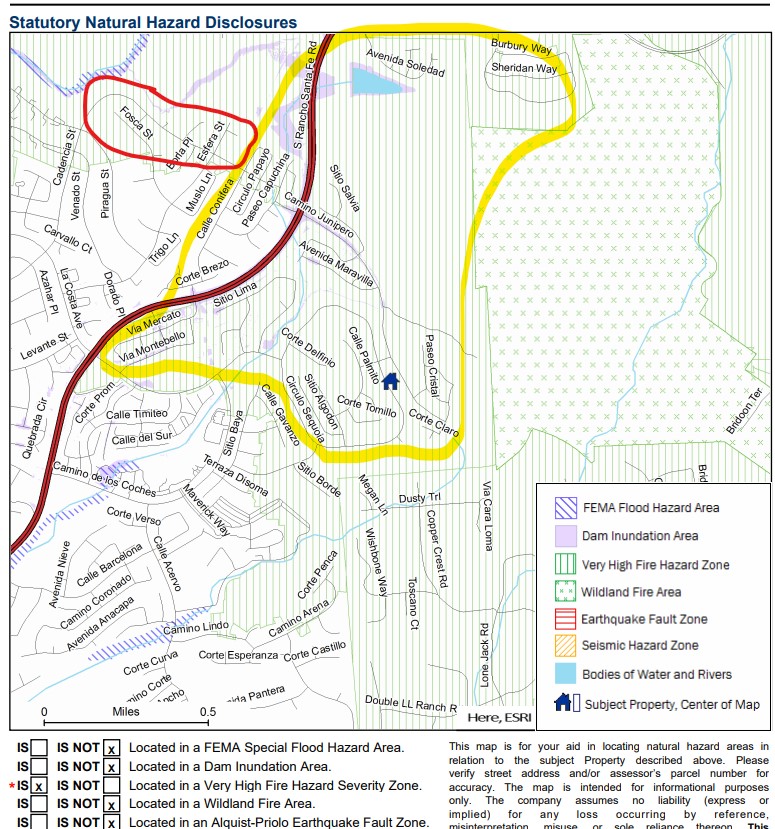

Our full-price buyers backed out of their purchase of my new listing in La Costa Oaks due to fear of fire. I was there in 1997 when the last fire blew through La Costa – you may remember me being interviewed by Susan Taylor on NBS that night – so I’m aware of the danger.

While my listing is in the fire zone, but let’s look at it realistically. For this house to catch fire, the new houses in front would have to burn first, and the fire would have to overwhelm the excellent fire-fighting techniques employed by the best fire crew around who are well-prepared for wildfires and would arrive on scene before this house get touched.

You could also get hit by an asteroid, but do you look up at the sky all day? No – go get fire insurance and enjoy life. The California Fair Plan is the last resort for fire insurance and they will always be there for you.

As a result, we’ll be doing open house tomorrow 12-3, come on by!

Here is the Natural Hazard Zone Disclosure map – there are hundreds of homes included in the very high fire hazard zone, yet the risk of burning down is extremely unlikely for the vast majority. Where homes burned in the 1996 fire is circled in red, and all of the homes within the yellow border have been built since:

Yesterday I joined Molly of Real Talk Media for a couple of thoughts about next year’s market:

The key to market conditions will be the inventory – no surprise there.

If there was a surge of newer McMansions for sale that were upgraded, well-presented, and had decent backyards, it would light the market on fire, mostly because we haven’t had many of those.

But it is more likely that we will have more of what we’ve had lately – homes for sale that are of the scratch-and-dent variety. They are ok, but not the premium creampuffs that every buyer desires.

The higher-end market will probably struggle a bit as sellers and agents slip back into the old normal where they ‘list ’em high and let them ride’, believing that it takes months to sell a more-expensive home. It doesn’t, but if you don’t have to sell, have plenty of time, and you’re not going to give it away, it is a fine strategy. Call Opendoor and see what they say.

There will be fewer realtors overall, and hardly anyone working with buyers – it’s too hard, and too time-consuming. With less good help, the price will really need to be right for buyers to proceed on their own.

Pricing? We don’t have a good way to measure, just bad ways. The median sales price will probably trend downward due to fewer of the higher-end sales. But sales of the sub-$3,000,000 creampuffs between La Jolla and Carlsbad will determine whether the median sales price goes up or down.