A fantastic spin on higher mortgage rates by two economists – an excerpt:

Mark Fleming – That’s a great question, Odeta. And when we subtract the core CPI inflation rate from the 30-year, fixed mortgage rate, we find that, with air quotes here, mortgage rates are actually negative.

Odeta Kushi – Say what now? Here we’re talking about rates as high as 5%. And now you’re telling me rates are negative?

Mark Fleming – Yep, over the last half century, there have only been two other times when core inflation was higher than the 30-year, fixed mortgage rate. Both of those were in the 1970s.

Today, we’re experiencing the extremely rare phenomenon of real, negative mortgage rates. So, while we may expect rising mortgage rates to cool the market, real estate still looks cheap, given the high inflation, not to mention the appreciation benefits that people get from the stellar asset returns that we’ve experienced recently.

Okay, thinking like a finance guy for a hot minute here. If the price of everything is rising faster than the price of borrowing at a fixed rate, aka the negative real rate of mortgages, to own an asset that’s appreciating in value. Hmmm.

Odeta Kushi – Yeah, so a significant slowdown in purchase demand due to rising mortgage rates is not necessarily a foregone conclusion, not to mention that house prices, and even sales to a lesser extent, have shown to be pretty resilient in the face of rising mortgage rates. You can refer to our podcast episode 15, if you want to know more about this.

But the SparkNotes version is in four of the last six rising mortgage rate eras, the existing-home sales increased or only declined after prolonged resistance. Home prices show even more resiliency.

Apart from the 1994 rising-rate period when house prices declined slightly and briefly, house prices have always continued to rise, albeit more slowly, when rates have increased. That’s because home sellers would rather withdraw from the market, rather than sell at lower prices, a phenomenon we refer to as ‘downside sticky.’

Of course, relative rates matter and mortgage rates have been in the 2-to-3% range during most of the pandemic. So, rising to about 4% may have a larger impact than in the earlier periods. So, it’s unclear how much rising rates will cool the purchase market. But, how would rising rates cool the housing market anyway? By reducing affordability, of course, and causing buyers to pull back from the market. In other words, by cooling demand.

JtR: Let’s note that the highly-financed buyers don’t get much of a vote because in the bidding wars over quality properties, they are sent to the back of the line. The ‘cooling demand’ from financed buyers pulling back only means fewer offers. The market’s direction will be determined by the cash buyers, and/or the big-down-payment buyers who will shrug off higher payments when they hear a catchy buzz word like ‘negative mortgage rates’. The location/condition of the home will matter more to the sales price than rates.

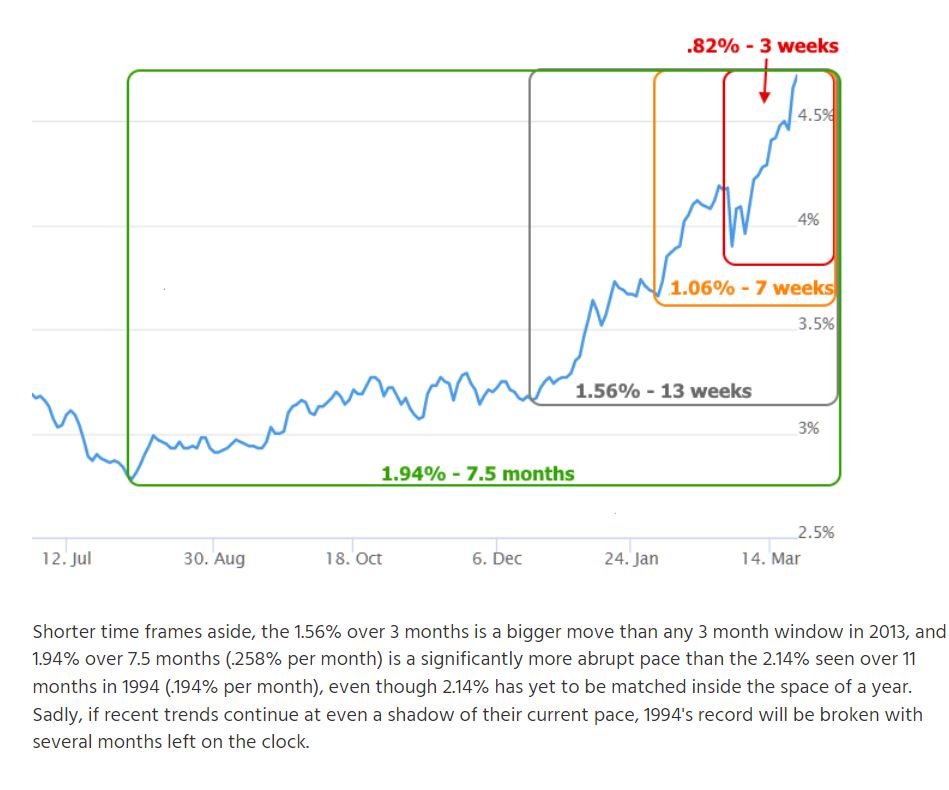

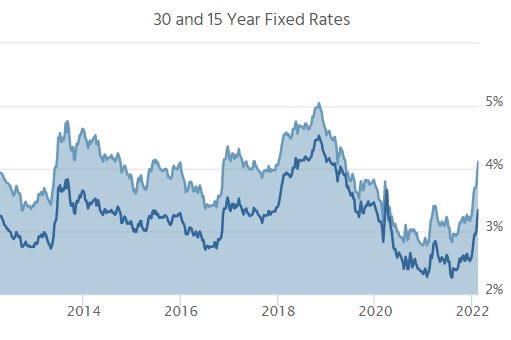

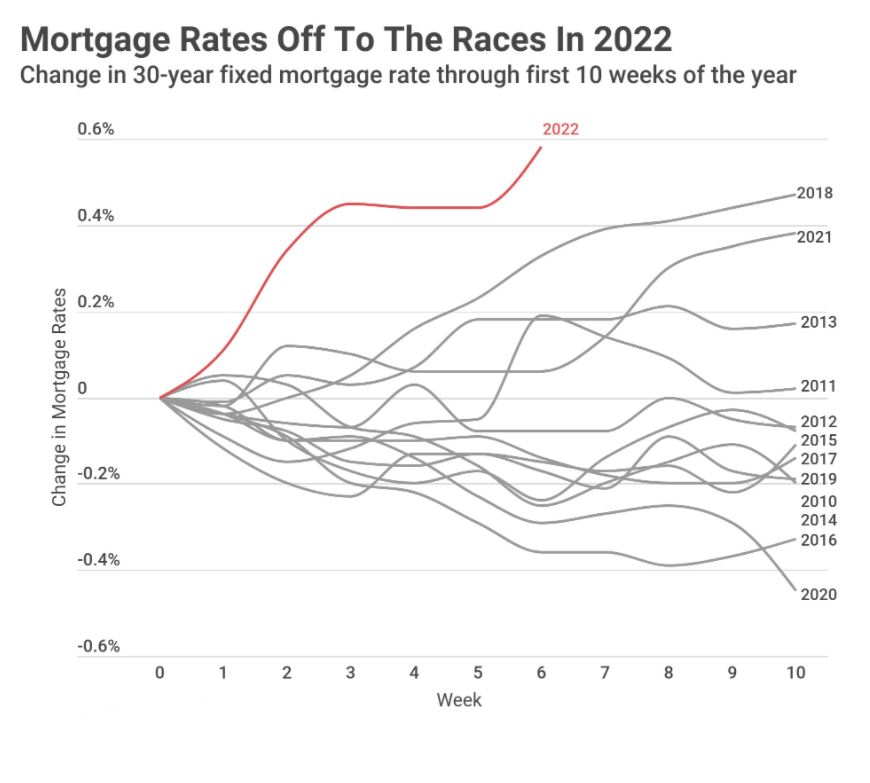

You can’t spend too much time reading/watching the news recently without being well aware of the relatively unprecedented surge in mortgage rates seen so far in 2022. In particular, the month of March was one the worst on record with one individual week in March tying a week in June 2013 as the worst in more than 25 years. All that to say, rates are much higher!

The higher borrowing costs have had the same impact they always have when it comes to refinance applications. In this week’s Mortgage Application Survey from the Mortgage Bankers Association (MBA), refis dropped another 10 percent, and are now 62 percent lower than the same week last year.

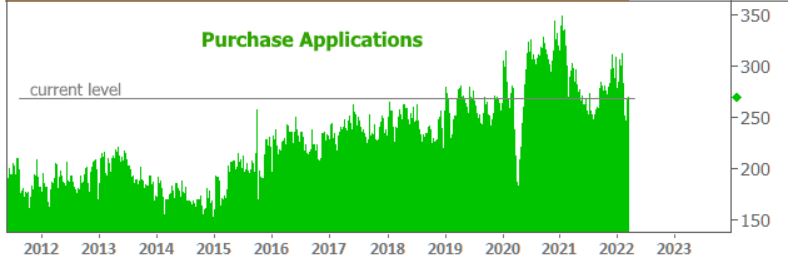

The purchase market remains a different story.

While purchase applications also declined last week, they are only 9 percent below the same week last year and still higher than most of the past decade before the Covid. Keep in mind that the survey only tracks applications, so by the time all-cash demand is factored into the purchase market, housing demand has yet to show any major panic over the rising rate environment.

We are in the midst of the fastest increase in mortgage rates in history.

It was only 6-8 months ago that home buyers were financing their purchase with a 30-year fixed rate in the twos. Now they are in the fours!

We had the lowest rates ever due to the pandemic. They aren’t coming back.

It is natural for home sellers to think it might be better to wait until later – especially if they tested the market with an aspirational price, and the home didn’t sell.

But the 30-year fixed rates are heading above 5%, which won’t bode well for buyers OR sellers.

What are other alternatives?

Sellers offer to buy down the interest rate for buyers (guarantee a lower rate).

Sellers complete more repairs/upgrades to stand out from others.

Sellers offer a larger commission to the buyer-agents.

Get an adjustable-rate mortgage.

I’ve already seen adjustable-rate mortgages starting at 2.375% for ten years, up to $1,600,000 with a 10% down payment. When buyers compare those to a 30-year fixed payment, they will be very tempted.

We don’t need the frenzy to last forever – we just need to get comfortable with a post-frenzy market.

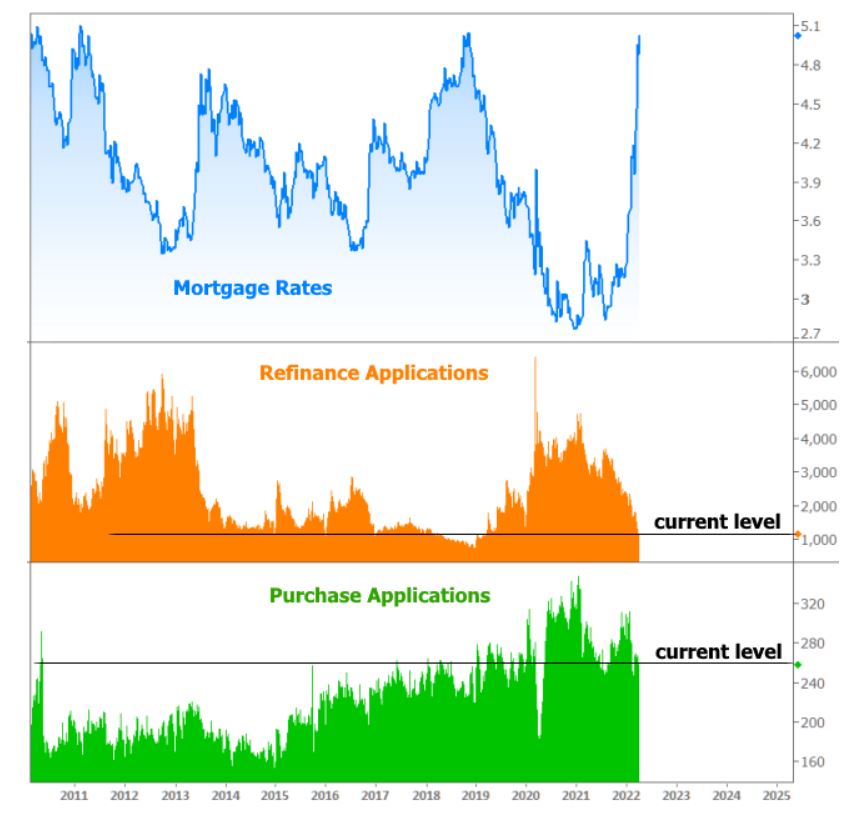

The Mortgage Bankers Association (MBA) released its latest mortgage application numbers this morning and the modest movement belies the drama unfolding in the world of mortgage rates. As usual, the MBA does a good job of capturing average rate movement week to week and they correctly identified last week’s big spike to the highest levels since the first half of 2019.

Despite the surge, mortgage applications didn’t respond in a major way. Refi applications only fell 3% from the previous week. Purchase applications actually managed a small uptick of 1% after last week’s more substantial 9% improvement. But context matters.

As seen in the following chart, refi applications have declined massively from Summertime highs and even more massively from the high levels at the beginning of 2021. MBA notes this week’s tally is 49% lower than the same week last year. The news is less dire on the purchase side. Applications are still lower than most of the past few months, but higher than most of the late summertime months from 2021:

Speaking of context mattering, a longer term chart of the same data really helps put the magnitude of this most recent rate spike into perspective. It’s not an exaggeration to say it’s now the sharpest move higher that any of us have seen in more than a decade (the overall size is about the same as 2016-2018, but this one has happened in roughly 6 short months… not only that, but 2016-2018 was really a 2-parter).

The other takeaways from the chart include the notion that the purchase market is still firing on all cylinders relative to most of the past decade (even then, we can responsibly conclude it would be even higher if not for the low inventory situation) and that refi demand doesn’t have much farther to fall before hitting the historical bottom. In fact, due to the immense equity build-up of the past 2 years, the doldrums of 2017-2018 may not be a relevant baseline this time around.

We gave credit to the ultra-low rates when they were in the 2%-range for helping to create the frenzy. Likewise, higher rates will have something to do with the way the market turns out in 2022.

It’s not because the payment are so much different. When the rate changes from 3.0% to 3.85% on a $1,000,000 loan, the payment only changes $472 per month.

The change will be because of the effect that higher rates have on market psychology.

We’re not going to get a memo on the day when buyers decide that they have had enough.

We know what signs to look for – higher market times, declining SP:LP ratios, and a growing amount of active (unsold) listings – to recognize when the market conditions are adjusting, and it’s been quiet so far.

Harder to measure is how quickly the demand could subside.

With the quality homes fetching an average of five offers each (roughly), then for every sale there is probably 2-3 losers that are literally priced out or voluntarily quit the race. At that rate, the demand could be cut in half or less within a couple of months.

Add the war in the Ukraine, rates well into the 4s, and list prices starting at 10% above the comps, and you have all the ingredients needed for a slowdown. Because the market is so hyped up, there will be ample overshoot and the frenzy should last into summer. But everyone knows it won’t last forever.

Rising rates may discourage the regular home buyers, but they aren’t the market-makers. All that matters is how many of the desperate-buyers-full-of-cash are left, and with the new listings trickling in, we only need a few!

It’s Thursday and thus time once again for Freddie Mac’s weekly mortgage rate survey. An industry standard report dating back to the 70s, Freddie’s survey rate is standby for multiple news organizations to print their once-a-week mortgage rate color. The net effect is the appearance of a deafening consensus in financial media regarding the going 30yr fixed rate.

The problem is that all of those sources are simply reporting Freddie’s survey headline. The bigger problem is that Freddie’s survey headline often gives the wrong impression about where rates are and how they’ve been moving. This is a logical consequence of the methodology. Freddie sends the survey out on Monday, gets most of it’s responses on Mon/Tue, and then reports “this week’s mortgage rates” on Thursday.

The net effect is that the survey ends up comparing Mon/Tue rates to last week’s Mon/Tue rates. Oftentimes, that doesn’t matter. If rates aren’t moving very much from day to day, the numbers will be relatively accurate as well as the week-over-week change. It’s when volatility surges that the mixed signals show up. And volatility is surging!

Rates aren’t merely changing a lot from day to day, they’re changing multiple times per day in many recent occasions. This week’s landscape was especially troublesome for the Freddie survey because Monday’s rates were, by far, the lowest. In fact, after adjusting for the upfront points and the fact that many of Freddie’s respondents probably didn’t even look past last Friday’s rate offerings before responding, the 3.85% headline isn’t too terribly far from reality.

To be clear, rates are no longer anywhere close to that low. The average lender is now definitively up and over 4.25% for the first time since early 2019. In other words, today’s rates are the highest in almost 3 years.

Last Friday was an interesting day for mortgage rates and the broader bond market. Rates began the day roughly in line with Thursday’s latest levels, but bonds lost ground throughout the morning. Multiple lenders adjusted rates higher before 1:30pm. After that, headlines made the rounds regarding the potential Russian invasion of Ukraine, which sent bond yields lower. By the end of the day, many lenders adjusted rates slightly lower.

The new week began with Russian Foreign Minister Lavrov making a series of comments that helped to moderate the more dire tone from Friday. Markets followed in lock step with rates rising to undo a majority of Friday’s improvement. This left the average mortgage lender roughly in line with Friday’s highs. That equates to 30yr fixed rates over 4.0% for most scenarios.

Russia/Ukraine headlines continued throughout the day. Although this did cause some volatility at times, markets progressively tuned out. Moreover, geopolitical risk is not destined to be the key market moving consideration unless things get appreciably worse. Even then, the primary narrative remains focused on inflation and the Fed’s evolving policy response.

The Super Bowl is complete, and the spring selling season begins today!

Judging by the quick jump in the total number of pendings, homebuyers aren’t waiting around. Mortgage rates have risen faster than any time in the last dozen years, and the number of homes for sale is scary low:

There was heavy activity over the weekend, and on the hot buys, the offers seemed to be starting at 10% over the list prices – which is now the new normal. Waiving contingencies and giving sellers free rentbacks for 60 days will be part of the landscape for the next few months.

Will rising rates cool off the market? Only for those who are on the fringes and sensitive to payment shock. The affluent – the buyers who are controlling the market – are less impacted, and a measly 1% rise in your loan rate only changes the payment by $1,116 per month on a $2,000,000 mortgage.

How long will the 2022 frenzy last?

It should stay hot until one of the following happens:

Mortgage rates hit 5%

A flood of inventory

Mid-summer

By summertime, the pool of highly-motivated buyers should be diminishing, and we’ll be left with those who haven’t been willing to pay these prices. Remember that when you see another crazy-high sales price, there was only one buyer who was willing to pay that much – the rest all wanted to pay less!

The big monthly jobs report is something that typically matters a great deal to rates.

Oddly enough, today’s jobs report was NOT seen having much of an impact for a few reasons. First off, analysts expected a much weaker number due to Omicron’s likely impact. Moreover, the Fed is almost exclusively focused on inflation right now as opposed to the labor market (employment and prices are the 2 key parts of the Fed’s job description). In short, no matter what today’s jobs numbers turned out to be, they weren’t likely to impact the market’s view of the Fed’s reaction.

All of that is now out the window, sort of. Although there are several important caveats regarding major seasonal adjustments, the jobs numbers were so much higher than the average forecast that markets were forced to respond. Fed rate hike expectations increased briskly and bond yields surged to their highest levels in more than 2 years.

If we disregard the once-in-a-lifetime volatility seen in March 2020 (and we absolutely should), today’s mortgage rates are now in line with the highs seen in October 2019. The average lender is now quoting conventional 30yr fixed rates in the 3.75-3.875% neighborhood. That’s a full eighth of a point higher than yesterday, and more than a full percentage point higher than the lowest rates in August 2021. Many less than perfect loan scenarios will see rates over 4%.