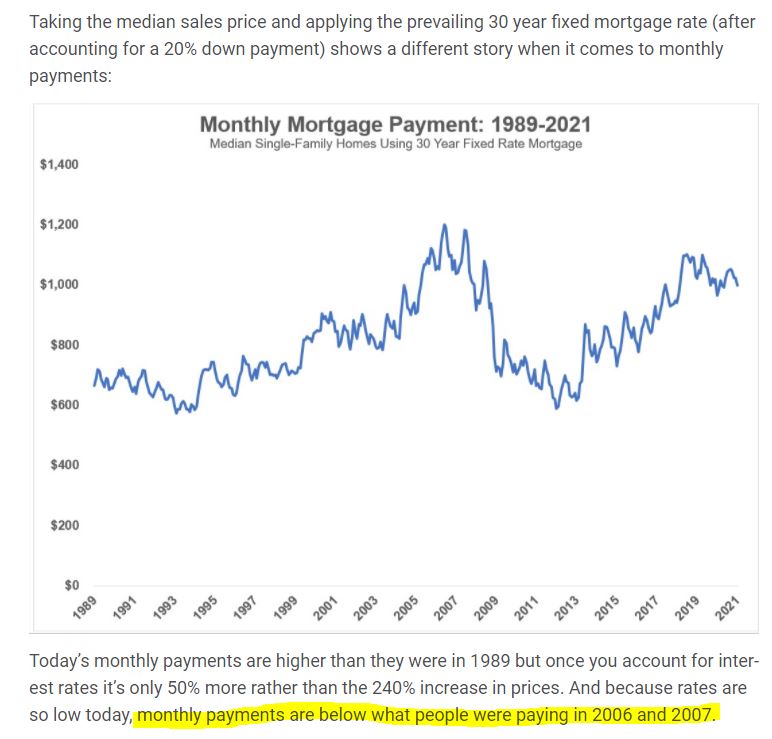

by Jim the Realtor | Mar 23, 2021 | 2021, Interest Rates/Loan Limits, Jim's Take on the Market, Mortgage Qualifying, Virus |

Thanks to just some guy’ for sending in this article comparing prices, rates, and inflation:

https://awealthofcommonsense.com/2021/03/what-if-housing-prices-arent-as-high-as-they-appear/

It’s a feel-good idea that inflation and lower rates can ease the pain of higher prices. But recent pricing has been really painful for buyers! Let’s apply the data to our local action (using 80% of MSP):

NSDCC Detached-Home Sales, February

| Year |

# of Sales |

Median SP |

Mortgage Rate |

Monthly Pmt |

| 2006 |

137 |

$833,000 |

6.25% |

$4,103 |

| 2015 |

171 |

$1,110,000 |

3.71% |

$4,092 |

| 2018 |

166 |

$1,289,005 |

4.33% |

$5,121 |

| 2021 |

226 |

$1,736,000 |

2.81% |

$5,714 |

It’s a nice idea, and higher rates did cool things down a bit in 2018. But today’s market is so explosive that we are blowing through all the usual stop signs – look at the number of sales!

My guess is that there will be additional sellers pulled forward from future years, just like with buyers – it’s too lucrative and tempting to find a way to sell now. Might it mirror the covid-recovery trend line?

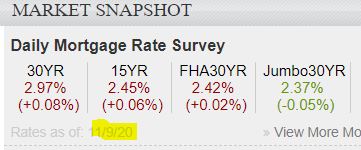

by Jim the Realtor | Nov 13, 2020 | Jim's Take on the Market, Mortgage Qualifying

There was a mistake in the rate-check I posted on Monday (above).

The jumbo rate quoted should have been 3.37%, not 2.37%.

This article discusses the spread between the conforming and jumbo rates, which has been closer until recently. It mostly comes down to lenders having few options where they can sell the jumbos loans, where the government will buy every conforming mortgage you can send them:

Link to Article

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

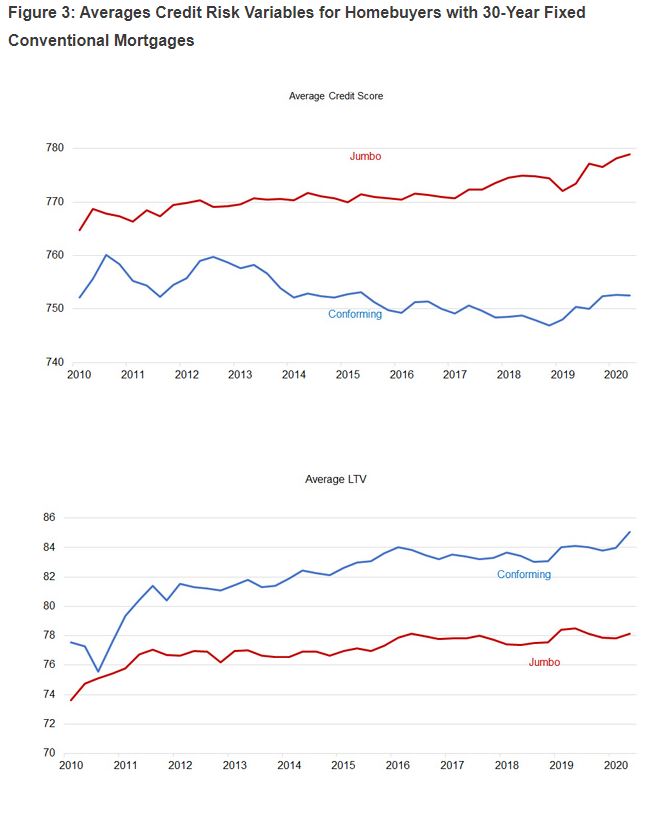

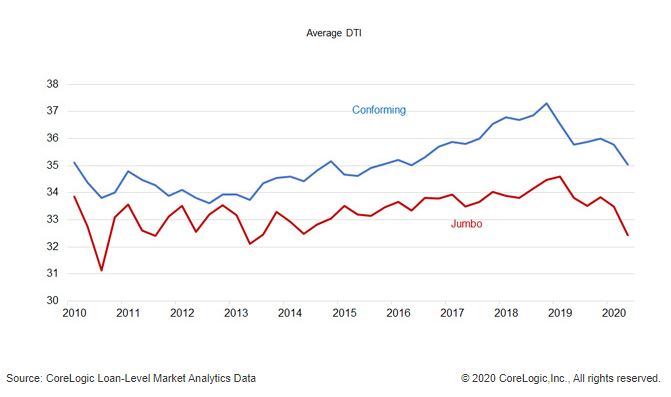

For anyone who might be concerned about mortgage defaults, I wanted to highlight these charts to show the risk level the banks are accepting on jumbo loans. This is the safest-looking data I’ve ever seen – it would take a catastrophic event for us to have a mortgage meltdown like we had last time:

A credit score of 775, equity over 20%, and a debt-to-income ratio under 33% is a dream borrower!

by Jim the Realtor | Sep 22, 2020 | Jim's Take on the Market, Market Buzz, Mortgage News, Mortgage Qualifying

We know that the ultra-low mortgage rates and tight inventory have been driving the market wild.

But here’s an extra boost – the strict mortgage underwriting that began in April is being relaxed:

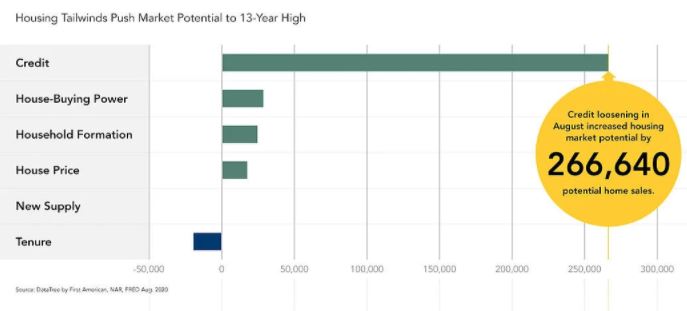

Credit Loosening: According to the NFCI credit index, a composite measure of credit conditions, credit tightened dramatically in mid-April to its most conservative level since 2009 due to the increased economic uncertainty driven by impacts from the pandemic. Since then, credit availability has loosened, even reaching pre-pandemic levels in August. This credit composite takes into consideration many different credit indicators, giving a comprehensive picture of credit conditions in the U.S. When lending standards are tight, fewer people can qualify for a mortgage to buy a home. Likewise, when standards are loose, more people can qualify for a mortgage and buy a home. Credit loosening in August compared with last month increased housing market potential by 266,640 potential home sales.

https://blog.firstam.com/economics/housing-market-potential-reaches-highest-level-since-2007

The graph above is somewhat misleading because they are only reflecting the month-over-month differences. The improvement of ‘house-buying power’ due to low rates has already been in place for months now, so the increase from July isn’t that dramatic.

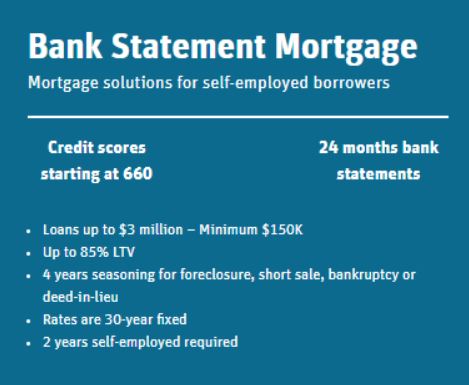

I’ve heard that the qualify-using-bank-statements mortgage is back, so that will add a few self-employed buyers who can’t qualify using their tax returns. More competition!

by Jim the Realtor | Jul 24, 2020 | Interest Rates/Loan Limits, Jim's Take on the Market, Mortgage News, Mortgage Qualifying |

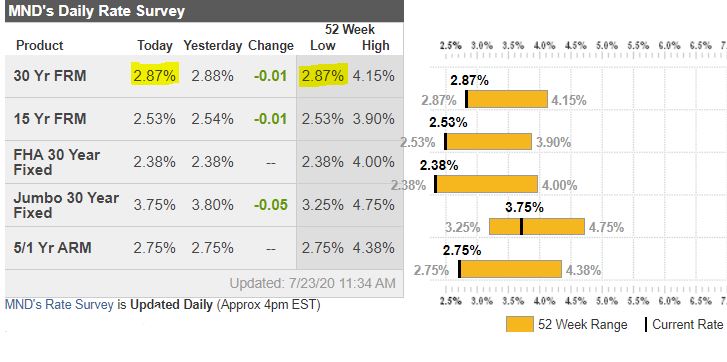

Today we should see another all-time-low record in mortgage rates!

What is the impact?

Here’s how it pencils:

If we just go back to the 52-week high of 4.75%, you could borrow $808,000 and pay $4,215/mo.

If you shopped around to get a 3.0% jumbo rate today, you’d pay a point or so, but you could borrow $1,000,000 and have a payment of $4,216 per month.

Within a 12-month period, the borrowing power has gone up from $808,000 to $1,000,000 with no change in payment!

This is why sellers don’t mind pushing their list prices – they want to share in the benefit!

by Jim the Realtor | Jun 17, 2020 | Jim's Take on the Market, Mortgage News, Mortgage Qualifying

More purchase apps reported today:

Buyers are rushing back into the housing market, enticed by record low mortgage rates and a pandemic-induced need to nest like never before.

Mortgage applications to purchase a home rose 4% last week from the previous week and were a remarkable 21% higher than one year ago, according to the Mortgage Bankers Association’s seasonally adjusted index. That was the ninth consecutive week of gains and the highest volume in more than 11 years.

“The housing market continues to experience the release of unrealized pent-up demand from earlier this spring, as well as a gradual improvement in consumer confidence,” said MBA economist Joel Kan.

Plus the loan-qualifying by bank statements (instead of tax returns) is coming back – though with 15% down payments, instead of 10%:

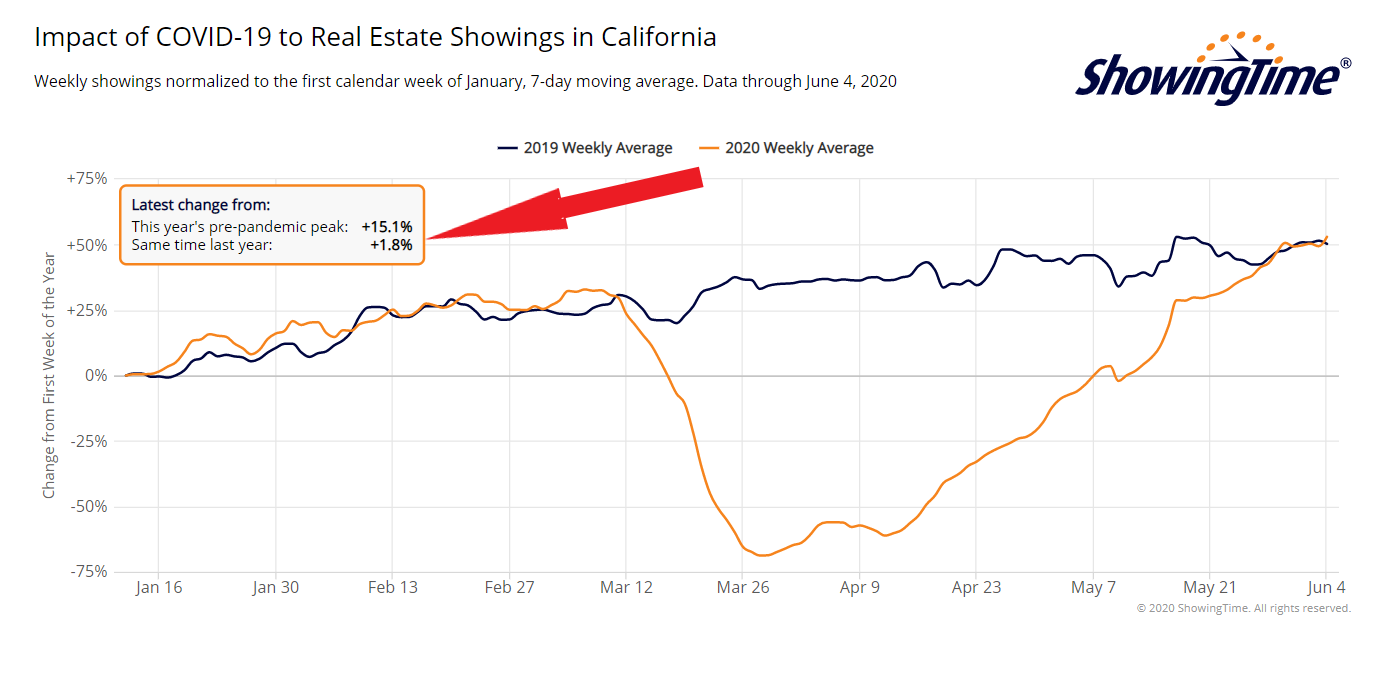

by Jim the Realtor | Jun 5, 2020 | Interest Rates/Loan Limits, Jim's Take on the Market, Market Surge, Mortgage News, Mortgage Qualifying, Showings |

Just like the price of gasoline, mortgage rates are very slow to come down, but they tend go up like a rocket – and with the surprising employment news today, we’ll probably get back into the mid-3s by Monday. We’ll see if the lowest rates in history were the sole reason why showings rebounded so quickly. From cnbc:

What’s good news for the U.S. economy is suddenly bad news for mortgage rates. A far-better-than-expected May employment report only added to a growing sell-off in the bond market, pushing yields to the highest level since March. Mortgage rates loosely follow the yield on the 10-year Treasury.

Rates have been rising this week, after sitting around a record low for the last two weeks. Friday, the average mortgage shopper may see rates on the 30-year fixed as much as a quarter point higher, according to Matthew Graham, COO of Mortgage News Daily, which runs daily averages from lenders.

For those with top-tier credit and financials, they may only see an eighth of a point increase, but for those with lower scores and down payments, the jump could be as much as 0.375%.

“It’s going to be ugly,” said Graham. “Today is the first time since the Covid-19 market reaction settled down in March that interest rates truly have a reason to panic. Until further notice, this looks like liftoff.”

This is not, of course, the last word in a mortgage market that has been on a rate roller-coaster ride fueled by a massive spike in mortgage delinquencies, an initially confusing and risk-ridden government bailout, and an overstressed loan servicing system. The mortgage bailout has been clarified, with parts rewritten to help servicers, the number of borrowers in forbearance plans is shrinking and mortgage companies are on a massive hiring spree.

(more…)

by Jim the Realtor | Jun 3, 2020 | Jim's Take on the Market, Market Conditions, Mortgage News, Mortgage Qualifying |

The coronavirus caused banks to pull back on lending, and one niche that was severely impacted was jumbo loans with less than 20% down payment. In early March, you could have borrowed $2,500,000 with 10% down, and by the end of March the max was down to $850,000.

We got lucky and found Dustin at Mission Fed, who is still funding the jumbos at 90%LTV up to $1.5M! My buyers thought he made the process simple and easy, and we closed escrow on the day Dustin predicted in the beginning. We couldn’t be more pleased with the service.

Here is a quick snapshot of some of the out of the box programs and jumbo programs at Mission Fed. This assumes a score of 720+ on an owner occupied purchase of a single family home:

- 0% down loans to $690,000 (*Not a VA loan. Anyone can qualify for this)

- 7/1 ARM at 3.125% with a 1% lender credit back for closing costs

- 10/1 ARM at 3.25% with a 1% lender credit back for closing costs

- 30 yr Fixed Jumbos with only 5% down

- 5% down up to a loan amount of $850,000 – Rate as low as 3.25%

- All on one loan. No need for a high rate HELOC

- 10% down payment up to loans of 1.5M

- 7/1 ARM at 3.125% with a 1% lender credit back for closing costs

- 10/1 ARM at 3.25% with a 1% lender credit back for closing costs

- 5/5 ARM @ 2.625% with a 1% lender credit back for closing costs

- 30 yr fixed jumbo at 3.25%

I like to help people, so I thought I’d mention him and his contact info for anyone reading who might be in the same fix. I don’t know any other lender offering these programs at these low rates – if you know someone, pass them along.

Dustin Gildersleeve · Mortgage Loan Originator at Mission FCU

Real Estate · NMLS #13509

Phone: 619-379-0196 · Fax: 858-777-3612

dusting@missionfed.com

To apply – www.missionfed.com/dustin

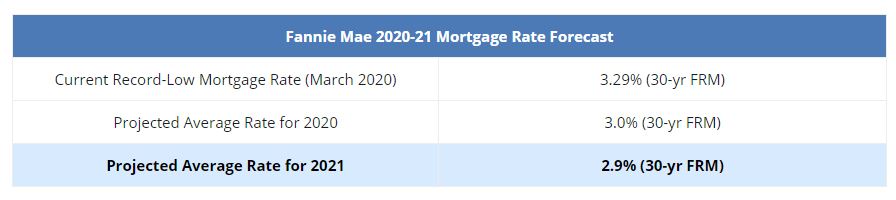

by Jim the Realtor | Apr 24, 2020 | Jim's Take on the Market, Mortgage News, Mortgage Qualifying

The thoughts of Fannie/Freddie were on my list of indicators, and it’s good to see them touting lower rates in the future. But 3% rates are either here now (if you pay points) or should be here shortly at no points.

The opinion from MDN:

Let’s get caveats out of the way upfront. No conversation about mortgage rates would be complete without a reminder that some lenders are very far removed from the averages. Moreover, even a lender is offering rates that are in line with today’s average, that may have been a completely different story at various points in the past. With that out of the way, yes, the average lender is now offering the lowest rates in several weeks for top tier, conventional 30yr fixed scenarios.

Speaking of top tier, how about some more caveats? As soon as we start adding risk factors to the mix, rates (or upfront loan costs) rise abruptly. In many cases, lenders aren’t even offering certain combinations of factors anymore. For instance, if you were hoping to get a cash-out loan, that’s quickly become much more expensive and in some cases impossible (at certain lenders). Similar story with lower FICO scores and investment properties.

The increased costs and decreased credit availability will continue to be an issue for the mortgage market. It will likely get worse before it gets better and we’ll need to see the breadth of the forbearance issue before having any hints of a shift in those trends.

But for the average “top tier” borrower, things aren’t too bad. You’d have to go back to at least April 9th to see lower rates. Most lenders are now in the low 3% range. FHA/VA rates are still frustratingly high for many lenders. ARMs aren’t even a consideration. 15yr fixed rates (which had been much higher than normal relative to 30yr rates) are finally starting to come back down for many lenders, but remain inexplicably elevated for others.

All of the above is a byproduct of the magical process of the world coming to terms with coronavirus. As far as the mortgage market is concerned, massive joblessness creates massive amounts of missed payments. Mortgage investors have quickly adjusted what they’re willing to buy and how much they’re willing to pay until they see the extent to which the missed payments cripple the industry. While tightening credit is frustrating for many consumers, it’s a natural law of the lending environment when joblessness ramps up, and joblessness has never ramped up so quickly. Lenders are doing what they need to do to avoid a collapse of the industry. People with jobs, but who also don’t have perfect credit files are unfortunately paying the price.

by Jim the Realtor | Apr 22, 2020 | Jim's Take on the Market, Mortgage Qualifying, Tips, Advice & Links

Generally, the cost of homeownership is under-stated. Let’s figure this to be around 0.175% of purchase price:

For many Americans, their expected mortgage payment may not be all that different from their current monthly rent. But even if you have a down payment saved up, you still may fall short when it comes to paying for all the monthly expenses of owning a home.

When you buy a home, you have to pay property taxes, insurance and maintenance costs on top of your mortgage payment, Suzy Orman says. Plus, if you put less than 20% of the home’s purchase price as the down payment, you’ll also have to pay private mortgage insurance, or PMI, to offset the risk your lender is taking in approving you for a home loan.

Those costs add up. Orman estimates that these extra, but necessary expenses, will cost you an additional 45% over your mortgage, just to keep your home.

In order to figure out if you can afford to buy, Orman says first-time homebuyers should test their finances. “I want you to play house,” says Orman.

Let’s assume you pay $1,000 in rent and estimate that your mortgage will cost about the same.

Over the next six to eight months, take $450 a month and put it in a savings account on the first of every month. That’s in addition to the eight-month emergency fund and the 20% down payment that Orman recommends having in place before you even start to look at local real estate ads.

“If in six to eight months from now, you are able to do it on time every single month, you can afford that home,” Orman says. Plus, after eight months, you’ll have almost $4,000 to put toward your closing costs.

Link to Article

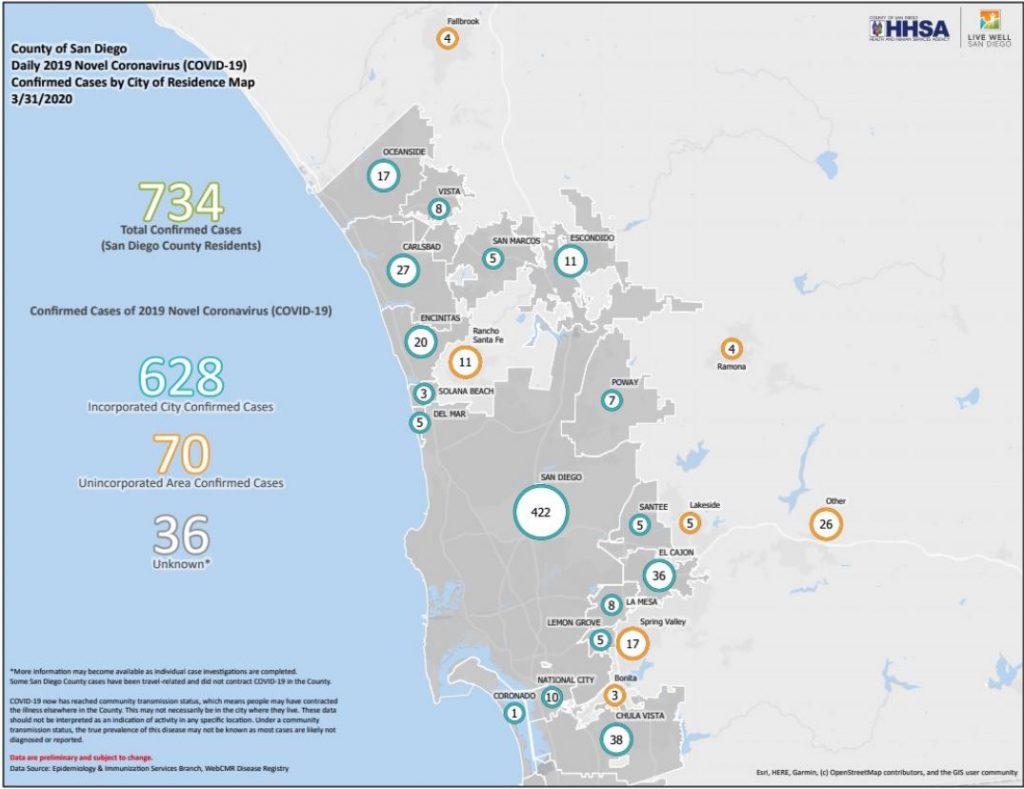

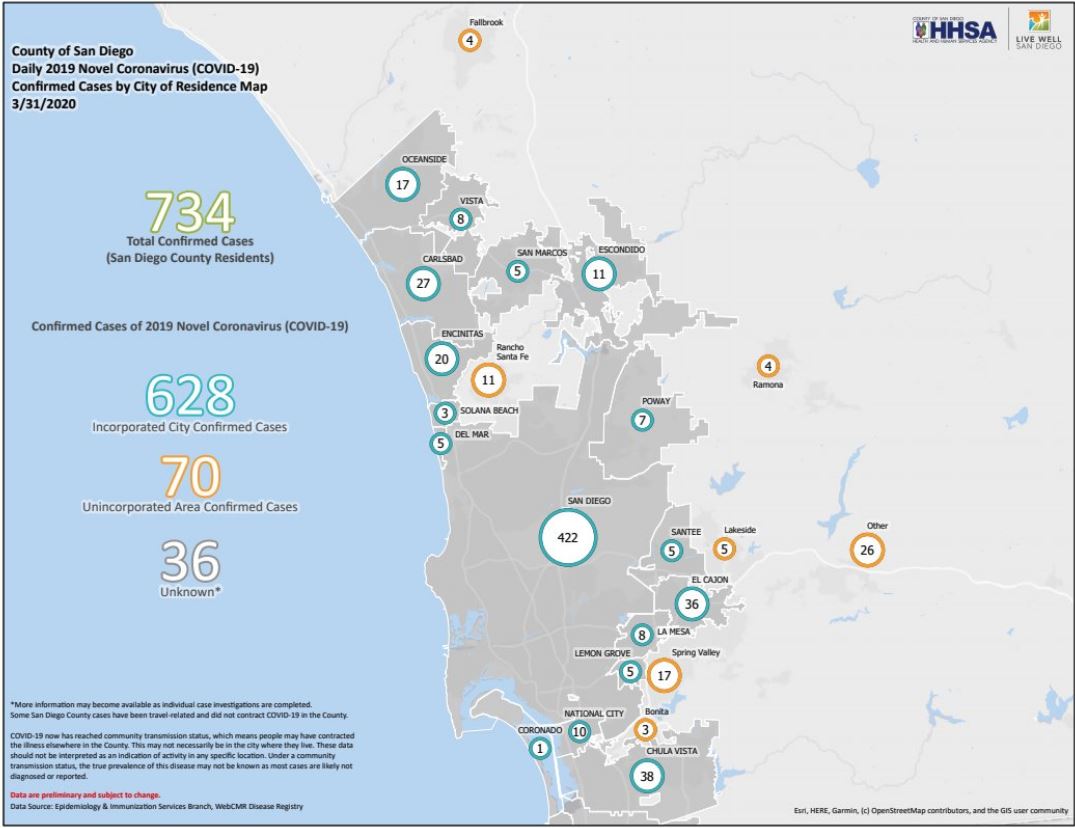

by Jim the Realtor | Mar 31, 2020 | Jim's Take on the Market, Mortgage News, Mortgage Qualifying |

Lenders have been pulling back on their willingness to loan money around the fringes:

Any loan that’s not right down the middle of the conventional spectrum raises questions about how it will impact lenders as they navigate what is easily the largest and fastest surge of forbearances the mortgage market has ever seen. Every loan raises questions. Due to their servicing rules or risk profiles, some loans raise more questions than others. Those loans have been absolutely demolished by an absence of investor demand. To reiterate, lower demand among investors = higher rates.

In essence, despite extraordinarily high prices on the bonds that underlie the top tier mortgage debt, much of the mortgage market is broken by the volatility and uncertainty surrounding COVID-19. Some parts will heal quickly as bondholders better understand their forbearance protections. Other parts will face a tougher road due to the impending recession (high LTVs especially). In all cases, TIME and STABILITY (in markets, the economy, and epidemiology) will be required before rates and product offerings return to where they were.

In just the last 2-3 weeks, many loan programs have been cut back or eliminated. The biggest impact on our market will be jumbo loans (>$701,500) which now need at least a 20% down payment in almost all cases – especially those loan amounts over $1,000,000.

As recently as three weeks ago, you could have bought a house for $2,500,000 with a 10% down payment.

Link to MND Article

More sellers are retreating as well.

In the 71 days between January 1st and March 11th, there were 99 detached-home listings between La Jolla and Carlsbad that were cancelled, withdrawn, or put on hold.

In the twenty days since March 12th, there have been 106 houses taken off the market.