Buyers and sellers will be tempted to sit out the rest of the year, and the resulting environment could actually get quite boring as we’re all standing around watching sales drop.

We just need to survive until the 2023 Selling Season, because the market will really get sorted out!

“A father doesn’t tell you that he loves you. He shows you.” —Dimitri the Stoneheart

“A good father is one of the most unsung, unpraised, unnoticed, and yet one of the most valuable assets in our society.” – Billy Graham

“Dads are most ordinary men turned by love into heroes, adventurers, story-tellers and singers of song.” – Pam Brown

“My father gave me the most valuable gift anyone could give another person. He believed in me”.

Jim Valvano

“When my father didn’t have my hand, he had my back.” – Linda Poindexter

“In my career, there’s many things I’ve won and many things I’ve achieved but for me, my greatest achievement is my children and my family.”

David Beckham

“Any fool can have a child, but that doesn’t make you a father. It’s the courage to raise a child that makes a father.” – Barack Obama

“A father carries pictures where his money used to be.” – Steve Martin

Over the last few decades, the 30-yr fixed mortgage rate has run at 1.75% over the 10-yr yield – which if true today, it would put us at 5.0%, instead of 6.0%. Here’s what the MND thinks about the bond yields:

As for Treasuries, yields are now high enough as to be pricing in virtually all of the expected Fed rate hikes over the next year. Once that happens, the only way for them to go much higher is for the data to deteriorate further. Bottom line: if we can avoid upside inflation surprises like last Friday’s, we may have just seen the highest rates of the year.

If the bond yields settle down (the 10-year was 3.48% on Monday), and bring in more MBS buyers, then maybe the mortgage companies can give up the extra 1% spread they are sitting on today. Our chances of survival will be much more likely with 5% mortgage rates, then 6%!

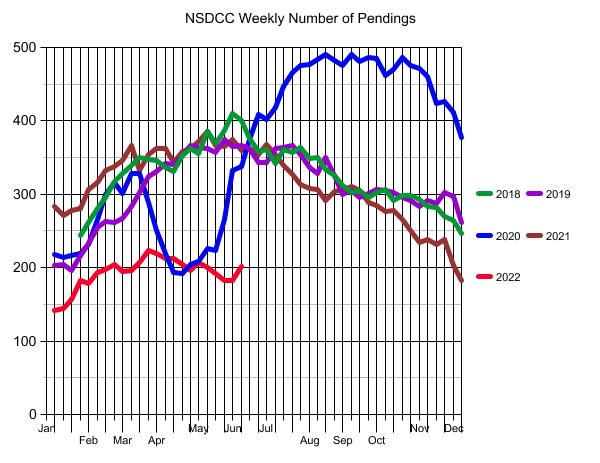

The California Association of Realtors said that the number of pendings has been falling.

They don’t give any other details or interpretations, so what will casual readers conclude?

The market must be coming apart!

Thanks C.A.R.!

But because pendings and sales are directly related to inventory, we must consider the impact of having fewer homes for sale. Look how dramatically the inventory has dropped recently, and yet we still had a good amount of sales, relatively:

NSDCC Detached-Homes

Year

Total Listings, Jan 1 to May 31

Total Sales, Jan 1 to May 31

Sales/Listings

2018

2,222

1,112

50%

2019

2,273

1,099

48%

2020

1,855

871

47%

2021

1,780

1,322

74%

2022

1,349

946

70%

In 2021, the frenzy was so hot that every house was selling, and the lower inventory wasn’t as obvious because the sales count was tremendous. But now that the number of homes for sale has really dried up, the impact on pendings and sales is more noticeable – at least for those who are willing to look that far.

This year has been really great! The rest of the year will probably be less great. It might even get back to 2018-2019 levels, which is fine – that’s the way it always was. We could handle worse if we had to.

This is our third look this year at a house in the Ranch of Carlsbad – the other two closed over $4,000,000 (one famously at $1,000,000 over list). This property didn’t sell in the first month, probably due to the interior looking somewhat original and in the Ranch – where lots are at least a half-acre – buyers expect more usable yard. The listing went live on April 7th at $3,400,000, they lowered it a month later to $3,250,000, and then it went pending on May 27th. It closed three weeks later for $3,175,000, which is a modest 2% discount off list.

Seeing how the government got us into this, let’s note that they are willing to carry some of the burden of higher mortgage rates. At today’s rates, buyers can write off twice as much mortgage interest!

Signed in 2017, the Tax Cuts and Jobs Act (TCJA) changed individual income tax by lowering the mortgage deduction limit to loans of $750,000 and under.

Let’s compare the amount of interest that is deductible in the first year:

$750,000 @ 3% = $22,285.85

$750,000 @ 6% = $44,749.47

The 30-year fixed-rate mortgage payment for $750,000 @ 6% is $4,496.63. To qualify, a buyer would have to earn approximately $200,000 per year, which would put them in the 32% tax bracket.

It means today’s buyer would pay about $7,188 less in federal tax in the first year, or ~$600 per month.

The difference between the 3% and 6% mortgage payments is $1,334 per month. With the additional $600 per month in tax savings, it means Uncle Sam picks up about 45% of the difference!

Now he’s done it. Chairman Powell’s remarks yesterday (and my comments at bottom):

Rates were very low. A good place to start is rates were very very low for quite a while because of the pandemic and you know the need to do everything we could to support the economy when unemployment was 14% and the true unemployment rate was well higher than that. So …

And that … that was a, uh, rates were low and now they are coming back up to more normal or above levels. So … in the meantime, while rates were low and while demand was really high … obviously demand for housing changed from wanting to live in urban areas to some extent to living in single family homes in the suburbs. Famously. And so, the demand was just suddenly much higher.

So we saw prices moving up very very strongly for the last couple of years.

So that changes now. And rates have moved up. We are well aware that mortgage rates have moved up a lot. And you are seeing a changing housing market. We are watching it to see what will happen.

How much will it really affect residential investment? Not really sure.

How much will it affect housing prices? Not really sure. Obviously, we are watching that quite carefully. You’d think over time … There is a tremendous amount of supply in the housing market of unfinished homes … and as those come online …

Whereas the supply of finished homes, inventory of finished homes for sale is incredibly low. Historically low. So it’s a very tight market. So prices might keep going up for a while, even in a world where rates are up. So it’s a complicated situation and we watch it very carefully.

I’d say if you are homebuyer, somebody or a young person looking to buy a home, you need a bit of a reset. We need to get to back to a place where supply and demand are back together and where inflation is down low again, and mortgage rates are low again.

This will be a process were by ideally, we do our work in a way were the housing market settles in a new place. And housing and credit availability are at appropriate levels.

Good grief!

One of the most powerful players in the world is making moves that will negatively affect every American, and he’s not sure how it will turn out? Did you ask anyone? Did you seek advice from anybody who is actively involved with the real estate market (not economists) to get some opinions?

Certainly, someone from the real estate industry will help him out….like Larry:

Oh, ok great. In response to her question about whether home prices will go down, he said we should produce more oil to reduce gas prices and lower inflation so mortgage rates could come down and make homes more affordable. Thanks for clearing that up, Larry!

What nobody is considering is that SELLERS GET A VOTE. If potential home sellers think that the Fed is trying to tank the real estate market, then they won’t sell now – they will wait for better days ahead.

I talk to buyers and sellers every day. I’ve knocked 1,000+ doors this year in search of potential home sellers, and haven’t gotten a single listing. The ridiculously high price they can get today isn’t enough to get them to sell. If they think that we’ve past the peak, they really won’t move!

Buyers need a reset, alright. But this won’t be it!

This 1998 tract house sold for $2,440,000, or +$144,000 over list price (+6%). The +6% should be about the maximum from now on. Heck, these are selling for the same money as they were getting next door in the Ranch of Carlsbad last summer!