When we listed 365 Marine Street in La Jolla for $6,950,000, the price was very aggressive at $2,401/sf. A top agent called it ‘oceanfront pricing’. Here’s the strategy I employed to sell for top dollar at minimum risk!

Here is my home tour:

This was my tour of the super-custom features in the home:

It is so great having Kayla home. She grew up as a San Diegan, but she is a New Yorker now, living just blocks away from Times Square. Alicia was born in New York City, but is a La Jollan now and one of the 100 Greatest Artists of All-Time, having sold over 90 million records and winner of 15 Grammys!

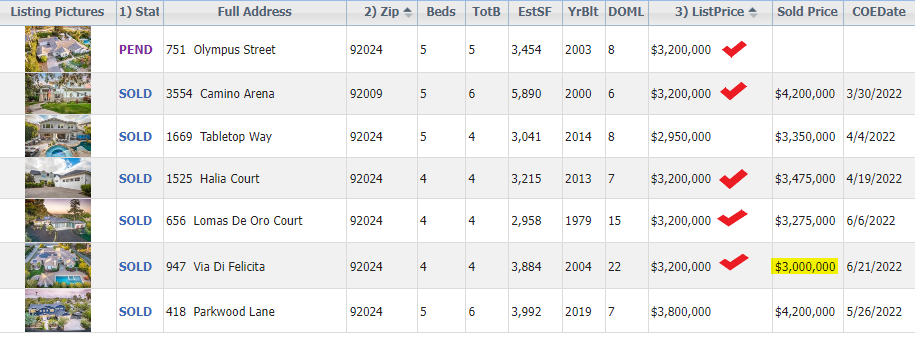

After she took five listings at the same price, I joked with the listing agent here that maybe every house was worth $3,200,000 now! I don’t think any of them were worth $3 million before this year, and this is the only one that has closed under list:

Hat tip to long-time reader Todd who we saw at the game last night – we did bug out early, but it was only to pick up Kayla at the airport. The Padres walked it off in the 11th inning!

Meanwhile, people are wondering where the local real estate market is going to end up.

For conditions to change much, sellers would have to panic, and dump on price. Otherwise, we will just be taking a leisurely stroll through Plateau City, admiring all the homes that aren’t selling.

Here are the favorite zip codes around North County – SE Carlsbad (92009), Encinitas (92024), Carmel Valley (92130), and Rancho Santa Fe (92067).

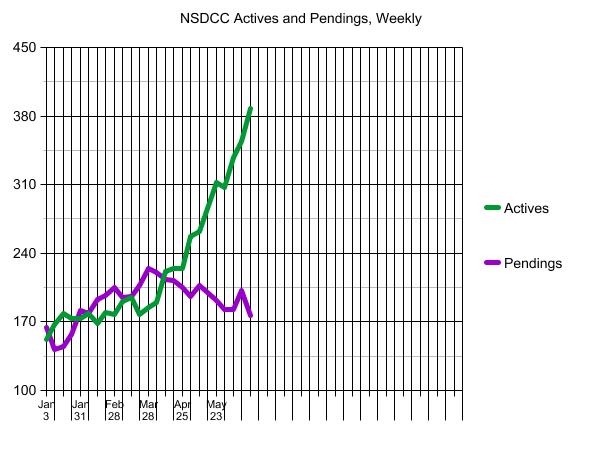

A few months ago, we had the lowest number of active listings of all-time:

While lately the number of the active listings have been growing steadily, they would have to double from this point before getting into the danger zone – but we’re going to run out of time before that happens.

Now that doom is being broadcast everywhere, sellers will decide that ‘now isn’t a good time to sell’, and by August they will quit listing their homes for sale.

There are 396 NSDCC active listings today (and 180 pendings), and we might hit 500 before August, but that will be the peak for 2022.

The market won’t keep getting worse – it will just taper off for rest of the year as buyers AND sellers lose interest. Instead, we’ll be talking about the playoffs and our first-place Padres going to the World Series!

We are having fewer sales between Carlsbad and La Jolla, but about the same percentage are closing over the list price as we’ve seen in the previous months of 2022:

NSDCC Detached-Home Sales, June (Month-to-Date)

Number of Sales: 104

Number of Sales Closed Over List: 68 (65%)

Average List Price of Over Lists: $2,298,732

Average Sales Price of Over Lists: $2,448,509

SP:LP = 107%

Median List Price of Over Lists: $2,100,000

Median Sales Price of Over Lists: $2,267,500

SP:LP = 108%

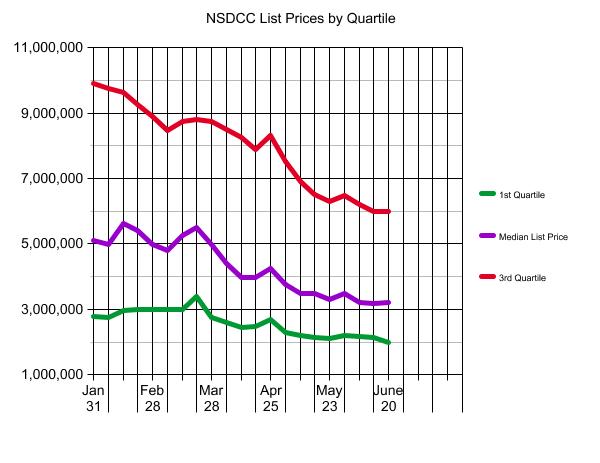

Can we say that the list pricing has come down much? Not really.

The median days-on market of those that closed over list was 8 days, so pretty much all of the buyers were into the higher mortgage-rate era when they made their decision.

I know it’s tempting for waiting buyers to think it’s going to get better, later – but so far, all that’s happened is fewer sales.

The Beach-Barber Tract is probably my favorite neighborhood in La Jolla, and is an eclectic mix of new and old that are close to both the beach AND village. A block down from our sale is this teardown that just sold for $6,000,000. The seller also owned the house next door to it, and he was the one who bought Mitt’s home – and just moved across the street!

Let’s break down the active and pending listings by zip code is to give you a closer look at the neighborhood stats. We’re going to have more active listings simply because the the list prices were all based on red-hot frenzy conditions (comps + 5% or more), and we’re past the red-hot days.

NSDCC Actives and Pendings

Town/Area

Zip Code

Feb 27

Mar 16

May 5

Jun 20

Cardiff

92007

5/7

6/4

7/7

13/5

Carlsbad NW

92008

6/9

8/10

15/10

27/10

Carlsbad SE

92009

15/29

8/33

20/27

47/25

Carlsbad NE

92010

1/5

2/6

7/14

17/11

Carlsbad SW

92011

2/11

4/12

8/16

19/19

Carmel Valley

92130

10/31

10/30

22/25

50/18

Del Mar

92014

15/32

17/10

24/13

30/8

Encinitas

92024

15/32

17/28

24/32

46/26

La Jolla

92037

53/38

55/35

51/32

72/24

Rancho Santa Fe

92067

45/22

47/24

49/22

52/25

Rancho Santa Fe

92091

2/2

5/2

2/0

3/2

Solana Bch

92075

6/6

3/10

9/7

12/5

NSDCC

All Above

179/205

182/204

238/205

388/178

The selling season started early in 2022, and was cooking by the end of February. Let’s group the different areas based on how their pendings are holding up.

Frenzy-ish:

Carlsbad SW – A few houses finally went up for sale, and buyers responded.

Rancho Santa Fe – The active listings aren’t growing like in the other high-end areas of Del Mar and La Jolla, and the number of pendings are very impressive. It was once normal when the Ranch had a 10:1 ratio between actives and pendings!

Normal-ish:

Everyone else, except……

Crash Zone

Carmel Valley – which has always had more pendings than actives over the last two years – and sometimes twice as many pendings! While having 50 actives and 18 pendings anywhere else would be a win, in the CV it feels like a meltdown.

Here they are:

(I tried to sort those by price order, but all they have is sort by date added)

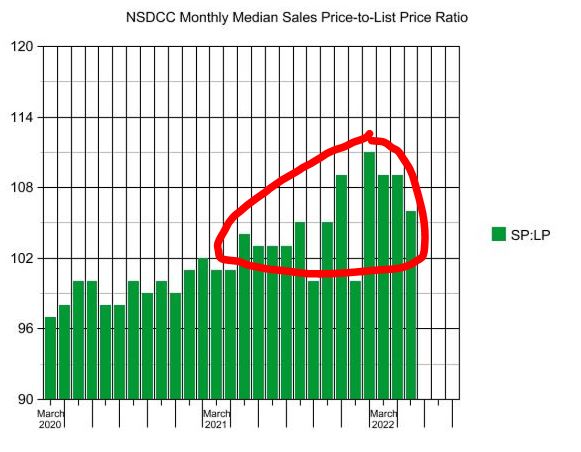

This nonsense about every buyer paying way over list price has to stop. If the SP:LP was around 100% we’d be elated, yet it was 111%, 109%, and 109% in the February-April stretch.

So far in June, the SP:LP is 107% for the 104 detached-home sales between Carlsbad and La Jolla!

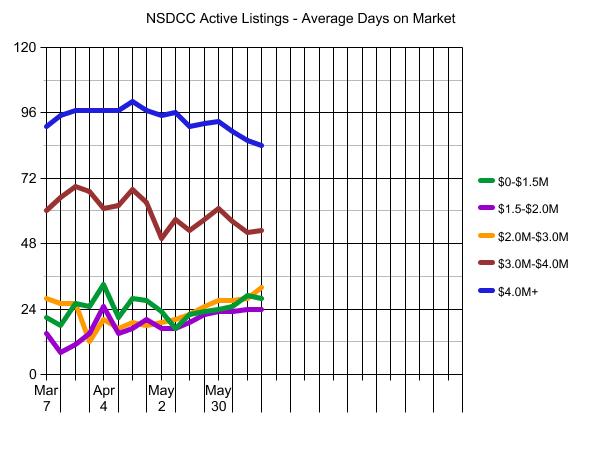

We can also track the average market times too. Any upward trends here would indicate market slowing – it’s early so nothing too startling yet:

The hottest of the red-hot was in 2020, when we had 400+ pendings from June 22nd to November 30th – with a peak of 491 pendings on 9/7/2020. Today we have 178 pendings.

Buyers thought this was a holiday weekend, and sellers didn’t!

It was the week that the actives-to-pendings ratio between La Jolla and Carlsbad crossed back over the ideal 2:1 range, which is what we have observed to be the sign of a healthy market in the past.

Last week: 354/202, or 1.75

This week: 388/177, or 2.19

Here is the breakdown by price range:

NSDCC Actives and Pendings

Price Range

Active Listings

Pending Listings

A/P

0-$1.5M

46

22

2.1

$1.5-$2.0M

57

41

1.4

$2.0-$3.0M

91

59

1.5

$3.0-$4.0M

52

26

2.0

$4.0M+

148

35

4.2

The high-end firmly believes that it takes longer to sell the uber-expensive homes, so they are happy to wait for their magic moment – and typically have the resources to do so.

I wrote offers for buyers around the $2,000,000 range, and both listing agents claimed to have multiple offers. It may take longer to reach an accepted offer these days as listing agents wait for better deals to arrive, so let’s check back on the pendings in a couple of days.

This is what Plateau City looks like – plenty of unsolds preferring to sit, than reduce.