Bird Rock View

I do video tours for out-of-town clients – it’s a virtual showing to help buyers decide if they need to get on a plane. If it’s a hot one, I’ll tell you:

I do video tours for out-of-town clients – it’s a virtual showing to help buyers decide if they need to get on a plane. If it’s a hot one, I’ll tell you:

The reason the talks broke down between Zillow and our local Sandicor MLS is because Zillow wants to keep and own the data we provide. The board members turned them down, but Zillow has made deals with most brokerages independently, which probably include them keeping the data.

You can see where they are going – they want to use their algorithms to predict everything. Eventually, won’t they be telling you how much to pay?

http://blogs.wsj.com/cio/2016/11/11/zillow-develops-neural-network-to-see-like-a-home-buyer/

Data scientists at Zillow Group are developing complex computer programs that detect specific attributes in photographs of homes, which could aid in estimating their value.

Advances in deep learning, big data and cloud computing have converged to allow the online real estate database firm and others to develop technology that mimics how the human brain processes visual images–a concept still in its early stages and once limited to only the largest technology companies.

It’s a daunting task, but one that could have wide-ranging impacts as enterprises look to extract meaning from giant databases of photographs.

Digital photographs from sources like real estate listings and online photos are invaluable in accurately estimating a home’s value, Zillow Group executives say. Humans are far better than computers at recognizing the features within a photo that could boost price, but the challenge is sifting through those photos at scale.

Data scientists at the company are developing convolutional neural networks, computer systems designed to mimic the human brain, trained to correlate specific collections of image pixels with valuation signals. For example, if granite countertops and stainless steel are identified in a photograph, that will automatically signal an increase in price.

“It’s essentially trying to code, in the pattern of a neural network, what we as humans can infer just by looking at the image,” said Stan Humphries, chief analytics officer, who heads the firm’s 100-person analytics division.

Neural networks require heavy computing power and in order to develop the technology, Zillow Group uses graphical processing units and cloud-based services from Amazon Web Services. The affordability of cloud-based services for enterprises has made it possible to develop technologies like neural networks that were previously unattainable.

Excerpted from MND:

http://www.mortgagenewsdaily.com/

“Taper tantrum” refers to the market’s reaction to the revelation that the Fed would begin reducing the pace of its asset purchases in mid-2013. For most of us, that’s as bad as it gets for bond markets. Even for those who lived through the brutal weeks in April 1987, the worst 3 days of the taper tantrum represented a more abrupt change in yields in terms of the percentage of gains erased compared to the worst 3 days in 1987.

It’s scary to consider, then, that the past 3 days (Wed, Thu, and today) have actually seen a bigger intraday yield spike than the worst 3 days of the taper tantrum! The fact that we can even begin to compare this move to the taper tantrum puts it in a league of extraordinary sell-offs that have rarely been seen in modern bond market history. It’s worth noting, however, that most of those extraordinary sell-offs were precipitated by the recent juxtaposition of long-term or all-time low yields.

What do higher rates mean for the NSDCC real estate market?

If you are thinking of selling in the next six months, you should put your home on the market today, while the uncertainty is still relatively unknown. I can be reached at (858) 997-3801!

Trump was less than impressive on 60 Minutes last night, and way too vague. It doesn’t sound like he will be saying anything to calm the markets, and any new economic policy will take months – or years – to implement.

It is virtually irresistible for home buyers to wait-and-see if prices come down. They will expect some trade-off for the higher rates, but our casually-motivated sellers are going to think lower prices are somebody else’s problem.

Higher rates will have an impact on keeping deals together too. Once a buyer secures a property and opens escrow, then their lender delivers the bad news – boom, the payments turned out to be higher than expected. The home inspection will be the last straw, and if the sellers take the repair requests too casually, deals will be dying.

It’s hard to imagine that the robust momentum we’ve enjoyed while rates have been in the mid-3’s will continue with rates in the 4’s. Something has to give.

The media won’t be helping either:

http://www.cnbc.com/2016/11/14/trump-effect-pushes-mortgage-rates-to-4.html

Get Good Help!

How did the Trump shock-and-awe affect our market last week? Let’s compare the first two readings of new pendings in November:

| Year | |

| 2013 | |

| 2014 | |

| 2015 | |

| 2016 |

Previous years didn’t have a presidential election, let alone the biggest upset in the history of the world. Mortgage rates had their worst week ever, and yet the market didn’t tank – new pendings were only off 21% YoY.

We’ll see if they stick!

Click on the ‘Read More’ link below for the NSDCC active-inventory data:

The ‘Crescent’ sold again in September, this time for $11,100,000, which is the highest sale ever in the 92024. It surpasses the previous high sale of the same property, $10,500,000, in March, 2014.

Rarely do I smell cigarette smoke in houses for sale any more. H/T daytrip!

http://theweek.com/articles/659711/how-quitting-smoking-help-sell-home

Have you ever been touring a home as a potential buyer and known within a few minutes that the house was not for you? Something left a poor impression on you that nothing else about the house could overcome. Think about that experience when you are on the other end of the transaction, preparing to sell your house.

It can be hard to spot the weak points in your own home, so let this list of top buyer turnoffs help you realistically assess your home before you list it for sale.

Consider these turnoffs from a buyer’s point of view:

Who knows — perhaps after you do all this work, you may decide to keep your house! At the very least, you will have improved the likelihood of selling your house and reaping the rewards of your foresight and hard work.

A comment left at the WSJ site: “Prairie mixed with Craftsman”

http://www.wsj.com/articles/modern-or-contemporary-whats-the-difference-in-home-styles-1478790617

John Stewart, residential committee chair of the American Institute of Architects, helps explain the difference. Modern homes and décor have the simple lines and “stripped-down” aesthetic of 1940s, ’50s and ’60s modernism, said Mr. Stewart, an architect in San Carlos, Calif. Other qualities associated with modern design: cube-shaped structures with flat roofs, monochromatic color palettes, low-key furnishings and a greater use of exposed steel and concrete. Modern “is probably the original contemporary style,” said Mr. Stewart.

Contemporary homes are often more playful in combining materials and bright colors, explained Sheila Schmitz, editor of home-design website Houzz. Some may include a dramatic black-and-white palette. Interiors are flooded with natural light and floor plans emphasize indoor-outdoor living. When it comes to spotting home décor, “those terms are really good starting points to start a conversation, and then kind of go from there,” she says.

This is pretty funny – and believable! Love the booty hat!

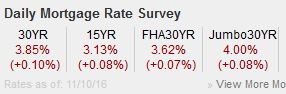

Buyers aren’t going to be happy about rates starting with a four….which we will probably see by next week:

http://www.mortgagenewsdaily.com/consumer_rates/677946.aspx

Mortgage rates continued a relentless move higher today, as financial markets continue rapidly adjusting the price of new realities (more on that in a moment). The average 30yr fixed rate quote surged another eighth of a point today (a huge move, relative to the average 24 hours), bringing the 2-day total to 0.25%. That’s nearly unheard of in modern economic history.

(NOTE: There are several articles floating around today that say rates have only risen 0.03% week-over-week. These are based on Freddie Mac’s weekly survey which has not yet captured the volatility of the past 2 days, due to its sampling methodology).

The last time rates moved a quarter point higher in 2 days was during the throes of the taper tantrum in mid-2013. Incidentally, the following 2 days also saw a quarter point spike, bringing rates a total of 0.5% higher in 4 short days. Those were the worst 4 days for mortgage rates on record.

Are you looking for an experienced agent to help you buy or sell a home?

Contact Jim the Realtor!

CA DRE #01527365, CA DRE #00873197