It looks like the hefty L.A. mansion tax is going to pass. Don’t be surprised if other cities and counties do the same and pit the rich people vs. everyone else under the guise of solving homelessness.

Measure ULA, the so-called “mansion tax,” is a ballot measure in California that would impose a one-time transfer tax on commercial and residential real estate sales valued at over $5 million.

The tax rate would be 4% for properties valued at $5 million to $10 million and would jump to 5.5% for properties valued at $10 million and above. Homeowners selling a $10 million property, for example, would face $550,000 in additional taxes on the sale.

Laura Raymond, organizer and spokesperson for the Yes on ULA campaign and director of the Alliance for Community Transit-Los Angeles (ACT-LA), a coalition of 42 organizations working toward transit and housing justice, said that the costs of the tax will be carried by the city’s wealthiest and the funds will benefit those most vulnerable.

“The cost-benefit tradeoff is a huge win, and one that will make our city not only more just but also a better place to live for everyone,” Ms. Raymond said.

If passed, the tax will go into effect in April 2023. Without a sunset clause, the tax would be permanent, though it would also be adjusted to keep pace with inflation. To avoid incurring these additional taxes, homeowners of multimillion-dollar estates looking to sell should act before next spring.

Those who don’t have a mortgage are particularly susceptible to fraudulent acts. Check out this free service being offered by the county to alert you! Hat tip just some guy!

Is title lock insurance a good investment?

Such insurance usually costs from $12 to $20 a month. But the San Diego County Assessor/Recorder/Clerk’s office now is offering the monitoring service at a far better price — free.

An announcement was made Friday that a real estate fraud notification service called “Owner Alert” is being activated for all homeowners who sign up for the service and register their parcel number.

“We timed this with the mailing of property tax bills,” says Jordan Marks, chief architect of the new service, noting that parcel numbers are easily available on the bills.

Through an electronic monitoring program, the county will notify property owners whenever their title is changed or a lien is attached.

“My goal is to sign up every San Diego property owner,” says Marks, chief deputy assessor. Marks, a Republican, is running against Democrat Barbara Bry to succeed retiring Ernest Dronenburg as head of the county’s Assessor-Recorder-Clerk’s Office in the Nov. 8 election.

Title theft is rare, but it does occur.

Patrick Ojeil, deputy district attorney in charge of real estate fraud in San Diego County, has 38 cases of potential title theft now under investigation.

Most of the time, he says, it is a family member or someone who knows the victim, such as a neighbor, a caregiver or an acquaintance, who tries to hijack the property title. But not always.

In 2015, a high-profile case came to light involving the bizarre theft of the title to Petco Park, appraised at the time for $539 million. A man, later determined to be mentally ill, had assumed title to the ballpark in 2013 by simply walking into the county recorder’s office and filing a fraudulently notarized title transfer form.

After the nefarious deed was discovered, perpetrator Derris McQuaig was charged with a felony. But a judge dismissed the case when McQuaig was determined to be mentally incompetent to stand trial. Instead, he was committed to Patton State Hospital in San Bernardino County.

No evidence was uncovered that McQuaig had plans to financially benefit from the title transfer, or that it was part of a larger scam. Nevertheless, it created a bureaucratic and legal headache for the city and the Padres and a challenge to get the title properly re-recorded.

What if you convert a vacation home to your primary residence, live there for at least two years and then sell it? Can you qualify for the full $250,000/$500,000 capital gains tax exclusion? No.

If you sell a main home that you previously used as a vacation home, some or all of the gain is ineligible for the home-sale exclusion. The portion of the gain that is taxed is based on the ratio of the period of time after 2008 that the home was used as a second residence or rented out to the total time that the seller owned the house. The remaining gain is eligible for the $250,000 or $500,000 home-sale exclusion.

If you hold rental property, the gain or loss when you sell is generally characterized as a capital gain or loss. If held for more than one year, it’s long-term capital gain or loss, and if held for one year or less, it’s short-term capital gain or loss. The gain or loss is the difference between the amount realized on the sale and your tax basis in the property.

The capital gain will generally be taxed at 0%, 15% or 20%, plus the 3.8% surtax for people with higher incomes. However, a special rule applies to gain on the sale of rental property for which you took depreciation deductions. When depreciable real property held for more than one year is sold at a gain, the rule requires that previously deducted depreciation be recaptured into income and taxed at a top rate of 25%. It’s known as unrecaptured Section 1250 gain, the number of its own federal tax code section.

Take this simple example: You bought a rental home for $300,000, deducted $109,000 of depreciation and sold the property for $500,000 this year. The first $109,000 of your $200,000 gain is unrecaptured Section 1250 gain that is taxed at a maximum rate of 25%, while the remaining $91,000 is taxed at the regular long-term capital gains tax rates.

Note that the unrecaptured Section 1250 gain can also apply to the sale of your main residence if you took depreciation deductions for it in the past, such as from a conversion from a rental home to your primary home or if you had an office in the home.

Capital losses from the sale of rental real estate can offset your capital gains, plus up to $3,000 of other income.

When real property used in a business or held for investment is exchanged for like-kind real property under Section 1031 of the tax code, all or part of the gain that would otherwise be triggered if the realty were sold can be deferred. This tax break doesn’t apply to main homes or vacation homes, but it can apply to rental real estate that you own.

The rules are very complicated and tricky, with many requirements to meet. Also, President Biden and Congress have proposed rules to limit the break. Make sure to talk to your tax adviser if you’re contemplating a like-kind swap.

See eight examples of the capital-gains tax when selling a home here:

SB 1105 has already passed in the state senate, and is being debated in the assembly. According to C.A.R., it will ‘grant vast, unchecked, taxing and bonding authority to an unelected Housing Agency Board in San Diego which would consist of 6 appointed representatives’. Huh? Anything that resembles a property tax is supposed to be approved by the voters!

This bill, the San Diego Regional Equitable and Environmentally Friendly Housing Act, would establish the San Diego Regional Equitable and Environmentally Friendly Affordable Housing Agency and would state that the agency’s purpose is to increase the supply of equitable and environmentally friendly housing in the County of San Diego by providing for significantly enhanced funding and technical assistance across the regional level for equitable and environmentally friendly housing projects and programs, equitable housing preservation, and rental protection programs, as specified. The bill would require a board composed of 6 voting members who are primary or alternate members of the San Diego Association of Governments, as specified, to govern the agency.

This bill would authorize the agency to, among other things, incur and issue indebtedness, place various measures on the ballot in the County of San Diego and its incorporated cities to raise and allocate funds, in accordance with applicable constitutional requirements, and to issue general obligation bonds secured by the levy of ad valorem property taxes, for purposes of producing and preserving equitable and environmentally friendly housing and supporting rental protection activities, as specified. Among the funding measures, the bill would authorize the agency to impose a parcel tax, a gross receipts business license tax, a special business tax, specified special taxes on real property, and a commercial linkage fee, as defined. The bill would also authorize local jurisdictions within San Diego County to impose a special documentary transfer tax, as specified, and authorize those local jurisdictions to remit proceeds of the tax to the agency to support the purposes of the agency. The bill would require that revenue generated by the agency pursuant to these provisions be used for specified housing purposes and require the agency to distribute those funds in accordance with specified requirements and subject to a specified priority. The bill would require the board to provide for regular financial audits of the agency’s accounts and records and to provide for financial reports.

The bill would require a development proponent for a development funded by the agency pursuant to these provisions to require, in contracts with construction contractors, that certain wage and labor standards will be met, including a requirement that all construction workers be paid at least the general prevailing rate of wages, as specified. The bill would require a development proponent to certify to the agency that those standards will be met in project construction. By expanding the crime of perjury, the bill would impose a state-mandated local program. The bill would also prohibit the agency from placing a measure on the ballot to raise revenue for the agency unless the agency has entered into a countywide project labor agreement with the San Diego County Building and Construction Trades Council, as specified.

The bill would include findings that changes proposed by this bill address a matter of statewide concern rather than a municipal affair and, therefore, apply to all cities in the County of San Diego, including charter cities.

The big concern for long-time homeowners today is having to pay capital-gains tax on the net profit that’s ABOVE the exempted $500,000 for married couples. While the 2-out-of-5-year rule that was passed in 1997 is due for some adjusting, there haven’t been any indications that the politicians will re-visit the issue.

What can homeowners do to minimize the tax owed?

Document Your Expenses. All home improvements (not repairs) and closing costs are added to your home’s cost basis (purchase price), which help to minimize the taxable gain.

Carry the Financing. Have a big equity position and don’t need all the money? Take payments from the buyer over time, instead of receiving all the cash at closing. Require a big down payment so you would receive a nice chunk up front, and then collect on a 5% mortgage over the next 5-10 years. You only pay tax on the money received, so structure it so you drop down into the 15% tax bracket for the first year:

Rent it out for a year and do a 1031 Exchange. After renting your home out for a year, you could trade it for another rental property and postpone the capital-gains tax indefinitely. You have to rent out the new home too for at least a year before occupying as your residence, so it is a 2+ year project – but hey, no tax! If you don’t need to live there, another alternative is to buy a property in an ‘opportunity zone’. Investors begin to enjoy a step up in basis after 5 years. After 10 years, the gains become tax-free!

Offset with capital losses from elsewhere. Business and stock losses can be included in the same tax return to offset the capital gains.

Move every time your net gain rises up to $500,000. You may have to take a hit this time, but to avoid having to pay capital-gains tax again in the future, move more often. 🙂

Dying correctly. The burden of being the remaining spouse after a full life together can be devastating, but at least he/she will have the cost basis increased to the home’s value on the day of death – with no capital-gains tax owed. Make sure to have your family trust named as owner of the home.

Wait until your home’s value goes down. This isn’t likely to happen, so focus on 1-6 above!

Virtually every long-time homeowner has seen their equity rise enough in the last 12 months to cover their tax exposure, and didn’t that feel like free money? Instead of fretting over having to pay the government, just enjoy the ample amount left over – you made more than they did! Or utilize the tips above.

I spoke with Jordan at the San Diego County Tax Assessor’s office about their Prop 19 processing. He said they have received about 1,000 requests since Prop 19 went into effect last April 1st, and have completed about half of them. He said there is a backlog of 6-9 months because they are appraising/analyzing every property in question to ensure compliance.

There were 36,936 sales of attached and detached homes in San Diego County since April 1, 2021, so the 1,000 requests (3%) gives us a feel for how effective Prop 19 has been in getting seniors to move (not very).

From Liam at the LAT:

Rose Liebermann opened her property tax bill and did a double take.

The $15,584 she owes on her new West Hills home was almost four times as much as the taxes on her previous house in Granada Hills where she had lived for more than 30 years.

“This bill, when I saw it, I said, ‘This can’t be real,’ ” said Liebermann, 71, a clinical social worker.

It wasn’t supposed to be that way. Proposition 19, narrowly approved by California voters in 2020, gives older homeowners a property tax break when they move. Specifically, it allows those 55 and older to blend the taxable value of their previous home with the value of a new, more expensive home they purchase, resulting in significant tax savings.

But processing delays at the Los Angeles County assessor’s office have left property owners like Liebermann facing hefty tax bills that must be paid while they wait for their applications to be approved.

Nearly a year after the law took effect, the assessor’s office has not completed any of the 1,271 applications it has received to recalculate the property taxes for older and disabled homeowners under the law, according to the agency. And it hasn’t finished any of the nearly 3,700 applications for parent-to-child and grandparent-to-grandchild inheritances, the other major piece of the tax measure.

Liebermann moved last summer because she wanted to help her daughter, Natasha Gershon, who is divorced and raising two young children, including a 10-year-old son with autism. Believing the tax measure would make it possible for her to afford a nicer place, Liebermann decided to buy the larger single-family home in West Hills where they all could live.

Liebermann has since borrowed money through a refinance loan to help pay the property tax and to build an accessory dwelling unit for herself.

When calculating how much your home has increased in value, you have to identify its COST BASIS – meaning anything and everything that you spent to pay for the product. The IRS defines a capital improvement as a home improvement that adds market value to the home, prolongs its useful life or adapts it to new uses. Minor repairs and maintenance jobs like changing door locks, repairing a leak or fixing a broken window do not qualify as capital improvements.

Capital improvements and things you can put in your COST BASIS include:

The price you paid for the property, including settlement costs, such as: title fees, legal fees, recording fees, survey fees, and any transfer taxes or fees you paid in connection with the purchase.

Additions: An added extra bedroom or bathroom, a deck on the back of the home, a new garage, an added porch or patio….anything that adds value to your home.

Lawn and grounds improvements: Value-adding landscaping projects, driveway or walkway construction, a new fence or retaining wall, adding a swimming pool, etc can qualify as property improvements.

Exterior improvements: New windows, a new roof, and new siding are examples. Any and all renovation costs including ANY and ALL costs related to that renovation work.

Insulation: This includes insulation in the attic, inside walls, under floors, or around pipes and ductwork.

Systems: Installing a new heating or air conditioning system, new ductwork, adding a central vacuuming system, wiring improvements, installing a security system, solar, geothermal, generators, batteries, and putting in lawn irrigation are improvements.

Plumbing: Installing a septic system, water heater, or soft water system adds value.

Interior improvements: New appliances, kitchen renovations, new flooring/carpeting, the installation of a fireplace, etc.

If you needed to make home improvements in order to sell your home, you can deduct those expenses as selling costs as long as they were made within 90 days of the closing. Your COST BASIS does NOT include hazard insurance premiums, moving expenses, or any mortgage-related charges (mortgage insurance, credit report fees, and appraisal costs are out) and general repairs that are essential to keep something working do not qualify. Yard maintenance, HOA fees, and real estate taxes don’t count. Always check with your accountant.

Keeping tabs of these costs throughout the lifetime of a house is wise.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

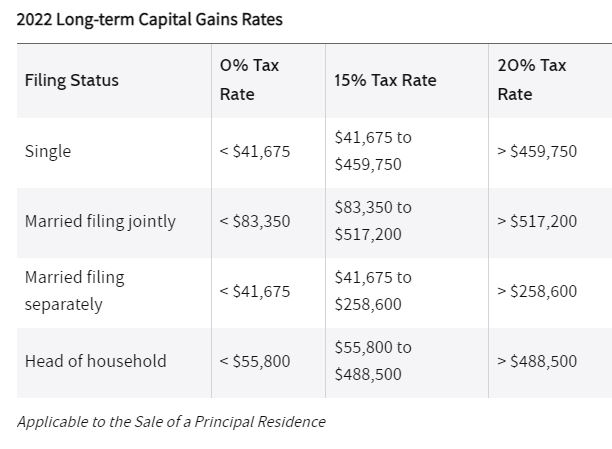

How do you calculate the capital-gains tax when selling?

Subtract your COST BASIS, commissions, and closing costs from your sales price to determine the taxable gain. Those who lived in the home for two out of the last five years can also subtract the $250,000 exemption if single (or $500,000 if two people), and then the rest is the taxable amount. Long-term capital gains — that is, gains on assets held for a at least a year – are generally taxed at a lower rate than earned income (money that you get from working).

In 2022, the IRS ranges are as follows:

0 Percent – $0-$41,675 Single/$0-$83,350 Married

15 Percent – $41,676-$459,750 Single/$83,351-$517,200 Married

20 percent – $459,751+ Single/$517,201 Married

The State of California will take their chunk too. Check with your tax adviser!

How do you get the $500,000 tax exemption on the net profit from the sale of your home?

If you and your spouse file tax returns jointly, and if both meet the “use test.” That means you both lived in the house as your primary residence for at least two of the five years leading up to the date of sale (and at least one of you are on title). Here is the IRS rule:

You can exclude being taxed on $500,000 of the capital-gains from the sale of your primary residence if all of the following are true:

1. You are married and file a joint return for the year.

2. Either you or your spouse meets the ownershiptest.

3. Both you and your spouse meet the use test during the 2-year period ending on the date of the sale.

4. During the 2-year period ending on the date of sale, neither you nor your spouse excluded gain from the sale of another home.

Should a spouse pass away, the surviving spouse has two years from the date of death to sell the home and receive the full $500,000 exemption from capital-gains tax – as long as they haven’t remarried.

If you wanted proof that the tight-inventory era will persist – and possibly get worse – over the next few years…..well, here you go. As prices have risen sharply, so has home equity – which means the long-time owners can be looking at a six-figure tax hit, even after the 2-out-of-5-year tax exemption.

While you can make the case that the capital-gains tax gets paid with the same-and-seemingly free money created by the recent home-price appreciation, Americans have a real aversion to paying taxes. Especially in six-figure amounts!

The long-timers who might consider selling their home are smart to calculate the potential capital-gains tax first. For most, it will probably be the last straw!

I’ve seen two new listings mention that their close of escrow must be after April 1st!

We are within range now, so hopefully we’ll see more Prop 19 sellers putting their home on the market in the coming weeks and months. The California Association of Realtors still says that this will benefit ‘millions of seniors’ and will open up ‘tens of thousands’ of new homebuying opportunities:

Removes location and price restrictions on property tax transfers for homeowners who are 55+, severely disabled, or victims of wildfire or natural disaster and allows them to transfer the property tax base of their existing home to a new home anywhere in California, regardless of price (with an adjustment upward to their tax basis if the replacement property is of greater value).

Creates housing opportunities to build more senior housing and retirement communities for millions of seniors and Baby Boomers to retire with Prop 19’s tax benefits.

Generates homebuying opportunities for tens of thousands of renters, young families, and first-time homeowners.

Provides new revenues annually for fire protection, emergency response, local government, and school districts.

For those who like to move, you can transfer your old tax basis up to three times (though there is conflicting commentary on whether disaster and contamination victims would get three chances or continue to be allowed just one transfer).

Other nuances:

If you buy a more-expensive home, the difference between the sales prices is added to the tax basis. Example: If you sell for $800,000 and buy at $900,000, the extra $100,000 is added to the old tax basis.

You can buy the new home first, and then sell the old one.

If the sale or purchase of a primary residence takes place before April 1, 2021, and the subsequent sale or purchase takes place within two years and on or after April 1, 2021, then you may qualify. The Association is seeking clarification – check with your attorney.

The ballot measure eliminated the parent-to-child and grandparent-to-grandchild exemption in cases where the child or grandchild does not use the inherited property as their principal residence, such as using a property as a rental house or a second home. When the inherited property is used as the recipient’s principal residence but is sold for $1 million more than the property’s taxable value, an upward adjustment in assessed value would occur.

The C.A.R. is working with the state to create a streamlined process to easily transfer the old tax basis. There are rumblings about additional legislation being needed to clarify other points – stay tuned!