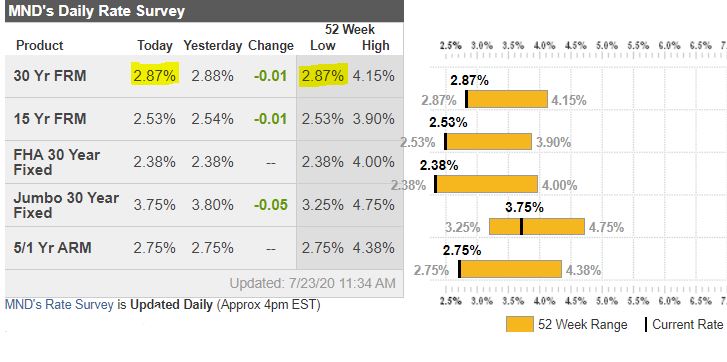

Mortgage rates were unchanged today for the average lender. That means they remain at all-time lows that are even lower than the all-time lows seen during the previous 3 business days. Even so, today’s underlying market movement might be a bit of a wake-up call for anyone waiting to lock an interest rate.

In general, the decision to lock or float a mortgage rate has had low consequences recently. While that will likely continue to be the case until the coronavirus situation meaningfully improves, it doesn’t mean we should fall asleep at the wheel. We need to remain vigilant for signs that the most recent all-time low mortgage rates are the last we’ll see for months or years.

Today served as a fairly non-threatening wake-up call in that regard–at least for those following the intraday movement in the bond market. Mortgage rates are ultimately dictated by the bond market. When yields move higher (and specifically when mortgage-backed bond prices are moving lower), we need to be on the lookout for mortgage rates to move up. That was exactly the sort of market movement we saw this morning, and it forces some of the risk takers out there to question how many times they will push their luck before finally resigning to lock.

There is NO WAY to know when rates have finally bottomed. So it’s best to decide a personal set of rules as to how you’ll approach the lock/float decision.

What can we know about the future? That’s tough because coronavirus has changed the playbook to some extent. In general, though, mortgage lenders are hesitant to drop rates very aggressively when they’re already at all-time lows. I can also tell you that, outside of an apocalyptic scenario, mortgage rates are highly unlikely to drop by more than half a percent (which is still significant). Even dropping by that much would require a significant deterioration in the covid narrative.

But how about we discuss this in a slightly simpler way. People always ask me for predictions, and I always tell them why it would be silly for me to provide and for them to put any stock in such things. What I CAN do is give you my sense of the most and least probable rate ranges within the next 3.5 months (presidential election will likely create new volatility for better or worse).

Most probable: 0.25 lower to 0.25 higher Somewhat probable: 0.25 to 0.50 higher Less probable: 0.25 to 0.5 lower OR 0.50 to 0.75 higher Improbable: >0.5 lower or greater than 0.75 higher

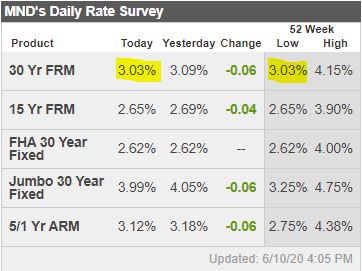

Please keep in mind that this is as of July 8, 2020. Things can and do change rapidly when it comes to pandemics and financial markets. That said, if your takeaway is that we’re slightly more likely to see a 0.5% move higher than a 0.5% move lower, that is indeed what I am saying. Again, it would take further deterioration in the covid narrative to reverse that order. That’s totally possible, but it’s not a given as of today.

The record-low rates probably haven’t helped the higher-end areas as much because the 30yr jumbo rate is higher – though you can pay to get into the mid-3s. An excerpt from MND:

How much of the strength in the housing market is due to mortgage rates holding near all-time lows?

Unequivocally, rates are helping housing numbers reach higher than they otherwise would be, but keep in mind, mortgages are much harder to get for certain scenarios right now. Beyond that, the home shopping process has challenges of its own that are keeping some would-be buyers sidelined for a bit longer.

The takeaway is that the bounce back in housing numbers is just like the bounce back in many other sectors of the economy. Things got bad enough that there was simply plenty of room for improvement.

No one is saying “everything’s fine now… back to business as usual!” Rather, many things are just quite a bit better than they were–so much so that we’re now in a position to debate whether the recovery narrative continues or cools off. That’s a debate that will remain open as long as COVID-19 numbers are pushing back on states’ lifting of quarantine measures.

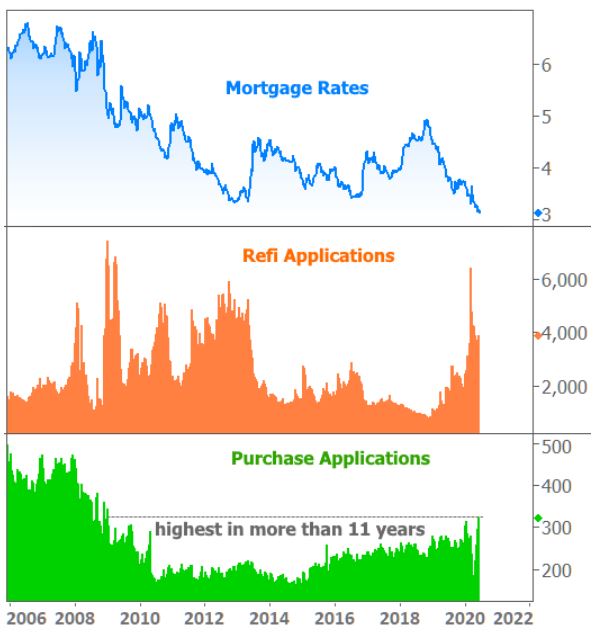

Buyers are rushing back into the housing market, enticed by record low mortgage rates and a pandemic-induced need to nest like never before.

Mortgage applications to purchase a home rose 4% last week from the previous week and were a remarkable 21% higher than one year ago, according to the Mortgage Bankers Association’s seasonally adjusted index. That was the ninth consecutive week of gains and the highest volume in more than 11 years.

“The housing market continues to experience the release of unrealized pent-up demand from earlier this spring, as well as a gradual improvement in consumer confidence,” said MBA economist Joel Kan.

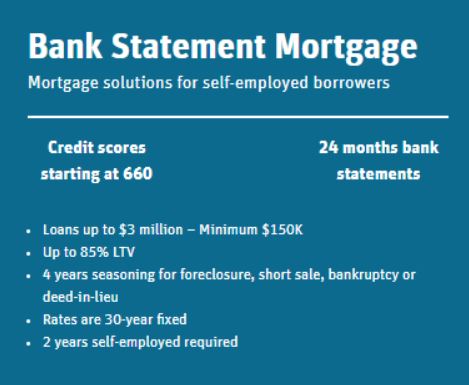

Plus the loan-qualifying by bank statements (instead of tax returns) is coming back – though with 15% down payments, instead of 10%:

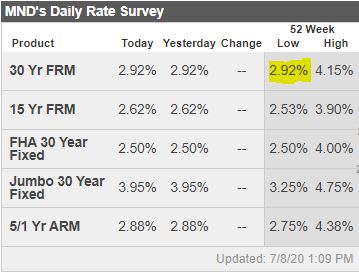

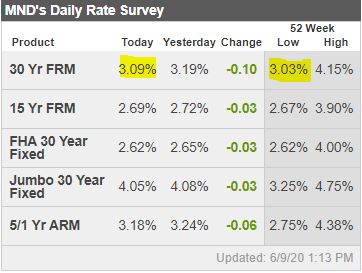

Mortgage rates moved lower again today, with the average lender erasing a good amount of the weakness seen last week. That’s good news considering rates hit all-time lows on the afternoon of June 1st (last Monday). After that, however, rates rose at their fastest pace in several months, raising some concern that the bond market (which underlies rates) was shifting gears in response to stronger-than-expected economic data.

It remains to be seen whether these past 2 days constitute a reversal in a negative trend or if they’re merely a token correction to last week’s rate spike. In other words, are things good or are they just noticeably less bad than they were? We won’t be able to answer this until we see how things play out in the coming days.

Tomorrow’s Fed announcement is the biggest potential flashpoint for volatility in the bond market this week. The Fed will certainly continue to buy Treasuries and mortgage-backed bonds. This is a key ingredient in keeping rates as low as they have been. Within the scope of “still buying bonds,” the Fed has some leeway in terms of how much it buys and how much it promises to buy. Some investors are looking for the Fed to firm up its bond buying commitment tomorrow, and that would likely help rates continue to calm down (as long as the promise is to keep buying as much as they have been).

Loan Originator Perspective

A big move back into the range for both treasuries and MBS today. Days like today make people want to wait to see if rates improve further. Chances are rates have room to go lower, but what tomorrow brings is anyone’s guess. The recommendation is to lock in as early in the loan process as possible, as long as you have a clear Closing date in place. –Gus Floropoulos, VP, The Federal Savings Bank

Bonds opened stronger, near their best levels ever this AM, before fading slightly following a weak treasury auction. Today’s rates are at (or almost at) all time lows. If you have the ability to lock at these levels, why not do so? –Ted Rood, Senior Originator, Bayshore Mortgage

Seems bonds have tested the top end of range and have rallied nicely over the last couple days. Based on my advice, my clients are taking advantage of today’s improved rate sheets and locking in. – Victor Burek, Churchill Mortgage

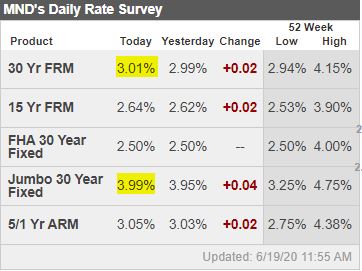

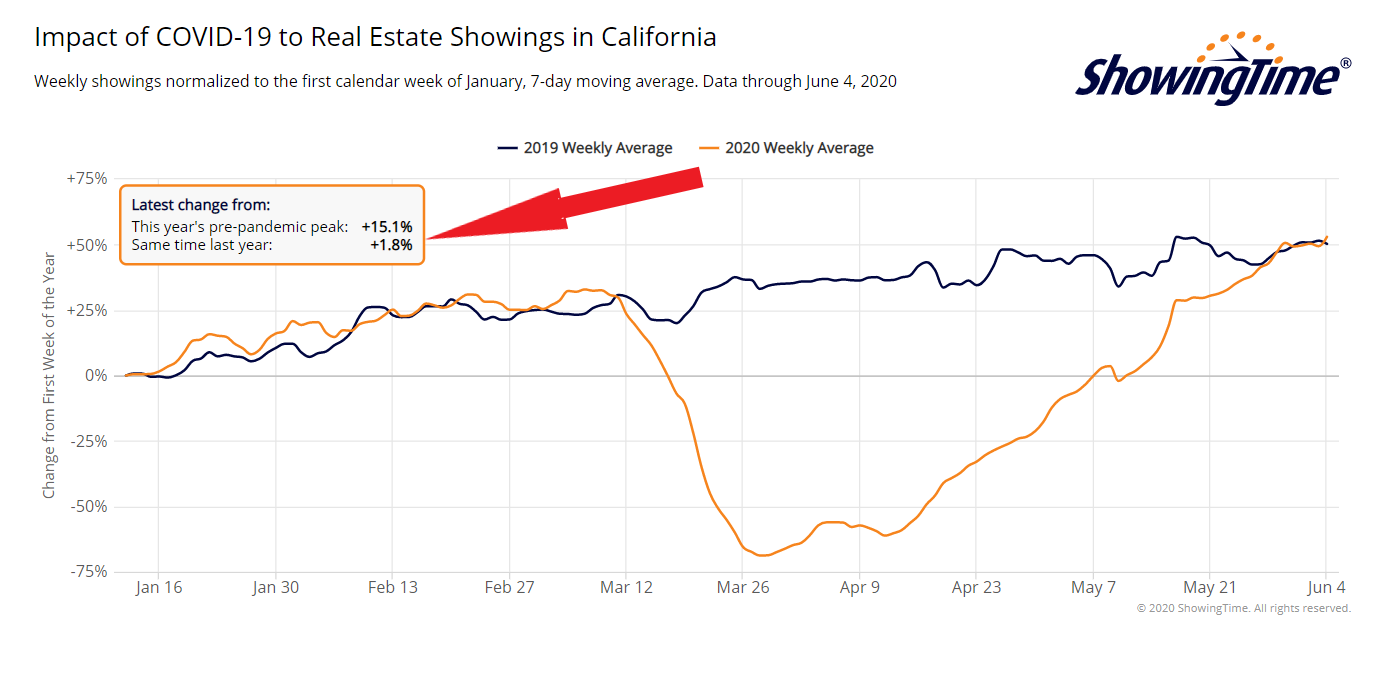

Just like the price of gasoline, mortgage rates are very slow to come down, but they tend go up like a rocket – and with the surprising employment news today, we’ll probably get back into the mid-3s by Monday. We’ll see if the lowest rates in history were the sole reason why showings rebounded so quickly. From cnbc:

What’s good news for the U.S. economy is suddenly bad news for mortgage rates. A far-better-than-expected May employment report only added to a growing sell-off in the bond market, pushing yields to the highest level since March. Mortgage rates loosely follow the yield on the 10-year Treasury.

Rates have been rising this week, after sitting around a record low for the last two weeks. Friday, the average mortgage shopper may see rates on the 30-year fixed as much as a quarter point higher, according to Matthew Graham, COO of Mortgage News Daily, which runs daily averages from lenders.

For those with top-tier credit and financials, they may only see an eighth of a point increase, but for those with lower scores and down payments, the jump could be as much as 0.375%.

“It’s going to be ugly,” said Graham. “Today is the first time since the Covid-19 market reaction settled down in March that interest rates truly have a reason to panic. Until further notice, this looks like liftoff.”

This is not, of course, the last word in a mortgage market that has been on a rate roller-coaster ride fueled by a massive spike in mortgage delinquencies, an initially confusing and risk-ridden government bailout, and an overstressed loan servicing system. The mortgage bailout has been clarified, with parts rewritten to help servicers, the number of borrowers in forbearance plans is shrinking and mortgage companies are on a massive hiring spree.

The coronavirus caused banks to pull back on lending, and one niche that was severely impacted was jumbo loans with less than 20% down payment. In early March, you could have borrowed $2,500,000 with 10% down, and by the end of March the max was down to $850,000.

We got lucky and found Dustin at Mission Fed, who is still funding the jumbos at 90%LTV up to $1.5M! My buyers thought he made the process simple and easy, and we closed escrow on the day Dustin predicted in the beginning. We couldn’t be more pleased with the service.

Here is a quick snapshot of some of the out of the box programs and jumbo programs at Mission Fed. This assumes a score of 720+ on an owner occupied purchase of a single family home:

0% down loans to $690,000 (*Not a VA loan. Anyone can qualify for this)

7/1 ARM at 3.125% with a 1% lender credit back for closing costs

10/1 ARM at 3.25% with a 1% lender credit back for closing costs

30 yr Fixed Jumbos with only 5% down

5% down up to a loan amount of $850,000 – Rate as low as 3.25%

All on one loan. No need for a high rate HELOC

10% down payment up to loans of 1.5M

7/1 ARM at 3.125% with a 1% lender credit back for closing costs

10/1 ARM at 3.25% with a 1% lender credit back for closing costs

5/5 ARM @ 2.625% with a 1% lender credit back for closing costs

30 yr fixed jumbo at 3.25%

I like to help people, so I thought I’d mention him and his contact info for anyone reading who might be in the same fix. I don’t know any other lender offering these programs at these low rates – if you know someone, pass them along.

Dustin Gildersleeve · Mortgage Loan Originator at Mission FCU

Washington, D.C. – Today, to support borrowers and mortgage servicers, the Federal Housing Finance Agency (FHFA) announced that Fannie Mae and Freddie Mac (the Enterprises) have issued temporary guidance regarding the eligibility of borrowers who are in forbearance, or have recently ended their forbearance, looking to refinance or buy a new home.

Borrowers are eligible to refinance or buy a new home if they are current on their mortgage (i.e. in forbearance but continued to make their mortgage payments or reinstated their mortgage). Borrowers are eligible to refinance or buy a new home three months after their forbearance ends and they have made three consecutive payments under their repayment plan, or payment deferral option or loan modification.

“Homeowners who are in COVID-19 forbearance but continue to make their mortgage payment will not be penalized,” said Director Mark Calabria. “Today’s action allows homeowners to access record low mortgage rates and keeps the mortgage market functioning as efficiently as possible.”

FHFA is also extending the Enterprises previously announced ability to purchase single-family mortgages in forbearance. The Enterprises are now able to buy forborne loans, with note dates on or before June 30, 2020, as long as they are delivered to the Enterprises by August 31, 2020 and have only one mortgage payment has been missed. The previous policy was set to expire on May 31, 2020.

Fannie Mae and Freddie Mac also extended their moratorium on foreclosures and evictions until at least June 30, 2020. The foreclosure moratorium applies to Enterprise-backed, single-family mortgages only. The current moratorium was set to expire on May 17th.

Click here to see if your mortgage is owned by Fannie Mae:

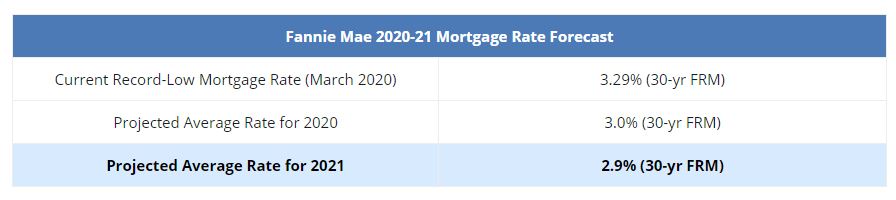

The thoughts of Fannie/Freddie were on my list of indicators, and it’s good to see them touting lower rates in the future. But 3% rates are either here now (if you pay points) or should be here shortly at no points.

Let’s get caveats out of the way upfront. No conversation about mortgage rates would be complete without a reminder that some lenders are very far removed from the averages. Moreover, even a lender is offering rates that are in line with today’s average, that may have been a completely different story at various points in the past. With that out of the way, yes, the average lender is now offering the lowest rates in several weeks for top tier, conventional 30yr fixed scenarios.

Speaking of top tier, how about some more caveats? As soon as we start adding risk factors to the mix, rates (or upfront loan costs) rise abruptly. In many cases, lenders aren’t even offering certain combinations of factors anymore. For instance, if you were hoping to get a cash-out loan, that’s quickly become much more expensive and in some cases impossible (at certain lenders). Similar story with lower FICO scores and investment properties.

The increased costs and decreased credit availability will continue to be an issue for the mortgage market. It will likely get worse before it gets better and we’ll need to see the breadth of the forbearance issue before having any hints of a shift in those trends.

But for the average “top tier” borrower, things aren’t too bad. You’d have to go back to at least April 9th to see lower rates. Most lenders are now in the low 3% range. FHA/VA rates are still frustratingly high for many lenders. ARMs aren’t even a consideration. 15yr fixed rates (which had been much higher than normal relative to 30yr rates) are finally starting to come back down for many lenders, but remain inexplicably elevated for others.

All of the above is a byproduct of the magical process of the world coming to terms with coronavirus. As far as the mortgage market is concerned, massive joblessness creates massive amounts of missed payments. Mortgage investors have quickly adjusted what they’re willing to buy and how much they’re willing to pay until they see the extent to which the missed payments cripple the industry. While tightening credit is frustrating for many consumers, it’s a natural law of the lending environment when joblessness ramps up, and joblessness has never ramped up so quickly. Lenders are doing what they need to do to avoid a collapse of the industry. People with jobs, but who also don’t have perfect credit files are unfortunately paying the price.

Millions of borrowers may be unable to pay their mortgages as the coronavirus continues to crush the U.S. economy. But there is a government back-up plan. The CARES Act just signed into law allows borrowers to skip payments for up to a year and then have those payments tacked on to the end of their loans.

There’s one hitch: the $2 trillion stimulus package states that borrowers need not provide any proof of financial hardship. They can simply say they can’t pay.

In an interview Wednesday, the chief regulator of mortgage giants Fannie Mae and Freddie Mac, FHFA Director Mark Calabria, begged borrowers to be honest.

“We’re operating on the honor system. We are asking and we’re putting together a script for servicers. This is supposed to be limited to if you’ve lost your job, you’ve lost income. Please, if you haven’t lost your job, continue paying. If you can pay your mortgage please do so because we really need to focus on the people who can’t.”

There will be some accountability: borrowers will have to provide documentation when they set up their repayment plans. Lying then would be considered fraud, a spokesperson for the FHFA said.

Calabria estimated that up to 2 million borrowers could be applying for loan forbearance by May and said that mortgage servicers, as well as Fannie and Freddie, could handle that if it was just for a few months. After that, there could be problems.

“If this goes beyond two or three months and we start to get worse than that, then that’s going to be a lot of strain, and certainly we’re going to start to see some firms get into a lot of liquidity trouble,” he added.

While the mortgage market was much healthier going into this crisis than it was going into the subprime mortgage crisis, there is still one very vulnerable area: FHA loans. These are low down payment loans to borrowers with lower credit scores, and they are insured by the federal government.

“The truth is that subprime really didn’t as much go away as it went into FHA, so you have a lot of FHA borrowers who I think are vulnerable. The real question is the duration of this,” Calabria said.

“If this is something that goes on for six months or more, then I think you’re going to continue to see a lot of stress, and I would really emphasize the place to look right now is the FHA market, with the credit quality of their borrowers,” he said. “They’re really going to be the first canary in the coal mine in terms of what the broader implications are going to be.”